Global Ultra Cruise and City-Street Autonomous Driving Market Size, Share, Growth Analysis, Autonomy Level (Level 2 ADAS, Level 3 ADAS), Operational Design Domain (Highway-Only Systems, City-Street Capable Systems, Comprehensive/Door-to-Door Systems), Sensor Technology (Camera-Based Systems, Radar-Based Systems, LIDAR Enabled Systems, Multi-Sensor Fusion Systems), End Use (Private/Personal Use, Ride-Hailing and Shared Mobility, Commercial Fleets), Vehicle (Passenger Vehicle (Sedan, Hatchback, SUV), Commercial Vehicle (LCV, MCV)), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179041

- Number of Pages: 324

- Format:

-

keyboard_arrow_up

Quick Navigation

- Market Overview

- Key Takeaways

- Autonomy Level Analysis

- Operational Design Domain Analysis

- Sensor Technology Analysis

- End Use Analysis

- Vehicle Analysis

- Key Market Segments

- Drivers

- Restraints

- Growth Factors

- Emerging Trends

- Regional Analysis

- Key Regions and Countries

- Key Company Insights

- Recent Developments

- Report Scope

Market Overview

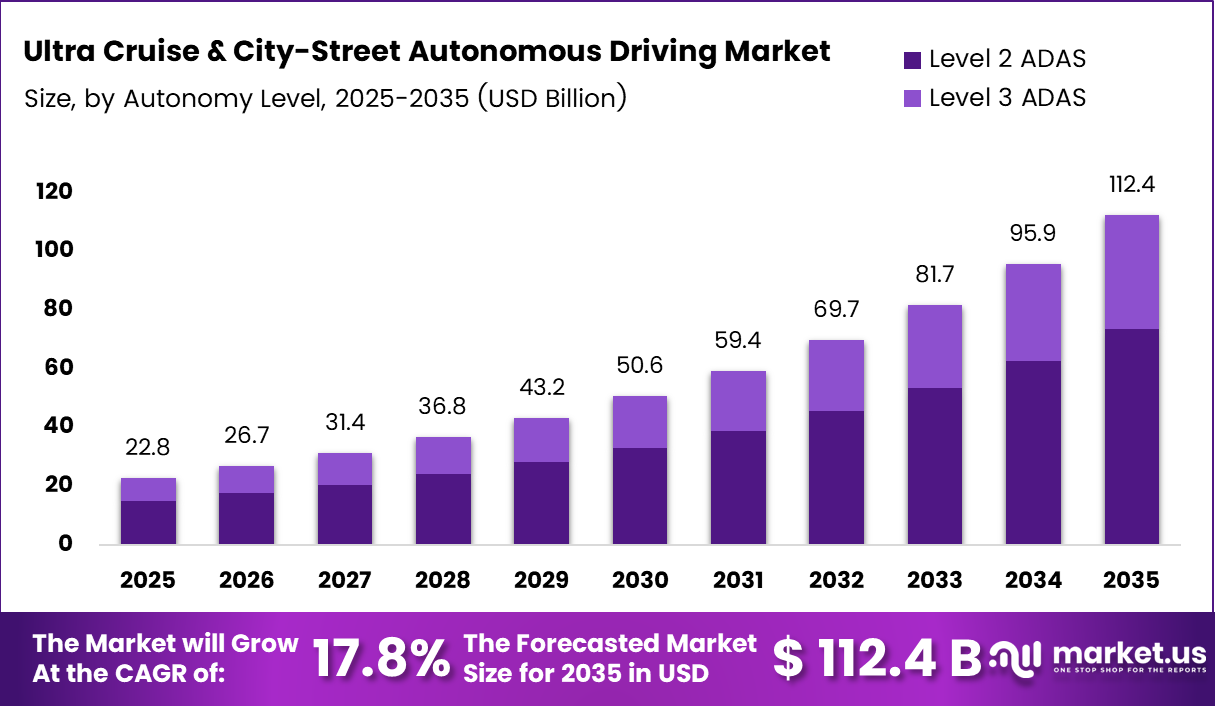

Global Ultra Cruise and City-Street Autonomous Driving Market size is expected to be worth around USD 112.4 Billion by 2035 from USD 22.8 Billion in 2025, growing at a CAGR of 17.3% during the forecast period 2026 to 2035.

The ultra cruise and city-street autonomous driving market encompasses advanced driver assistance and fully autonomous systems designed for both highway and urban road environments. These systems integrate AI perception, high-performance computing, and sensor technologies to enable hands-free or driverless vehicle operation across varying road conditions.

Autonomous driving technology spans multiple levels of vehicle intelligence, from Level 2 partial automation to full self-driving capability. Moreover, city-street autonomous systems represent the next frontier, extending beyond structured highway environments into complex urban scenarios with pedestrians, intersections, and unpredictable traffic patterns.

Growth in this market is closely tied to rising OEM investment in end-to-end autonomous platforms. Automakers are increasingly integrating AI-driven perception systems and high-performance onboard computing to meet consumer demand for enhanced road safety and convenience in dense city traffic.

Governments across major economies are actively supporting autonomous vehicle programs through regulatory frameworks and testing approvals. Consequently, this policy momentum is accelerating market readiness and enabling broader deployment of advanced driver assistance and autonomous systems on public roads.

Strategic partnerships between automakers, semiconductor firms, and AI software developers are further shaping market expansion. Additionally, smart city infrastructure investment is enabling vehicle-to-infrastructure communication, which strengthens the operational reliability of autonomous systems in real-world urban environments.

According to Edmunds, GM’s Ultra Cruise system is designed to enable hands-free driving in 95% of all driving scenarios, using sensor fusion across more than 400,000 miles of mapped roads in the U.S. and Canada. According to Road to Autonomy, the autonomy economy index returned 1.24% in December 2024, reflecting steady investor confidence in the sector’s long-term growth trajectory.

Key Takeaways

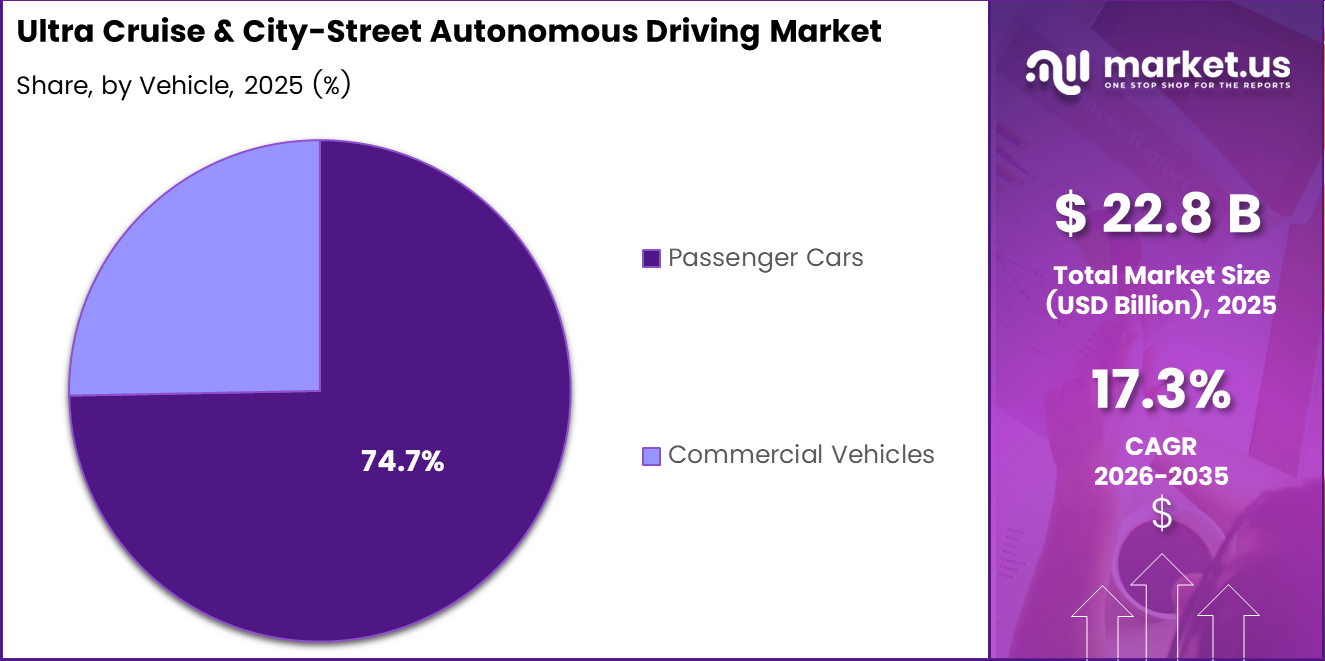

- The Ultra Cruise and City-Street Autonomous Driving Market was valued at USD 22.8 Billion in 2025.

- The market is projected to reach USD 112.4 Billion by 2035, growing at a CAGR of 17.3%.

- By Autonomy Level, Level 2 ADAS dominates with a market share of 65.3%.

- By Operational Design Domain, Highway-Only Systems hold the largest share at 56.6%.

- By Sensor Technology, Camera-Based Systems lead with a 38.5% share.

- By End Use, Private/Personal Use accounts for the largest share at 61.2%.

- By Vehicle, Passenger Vehicles dominate with a share of 74.7%.

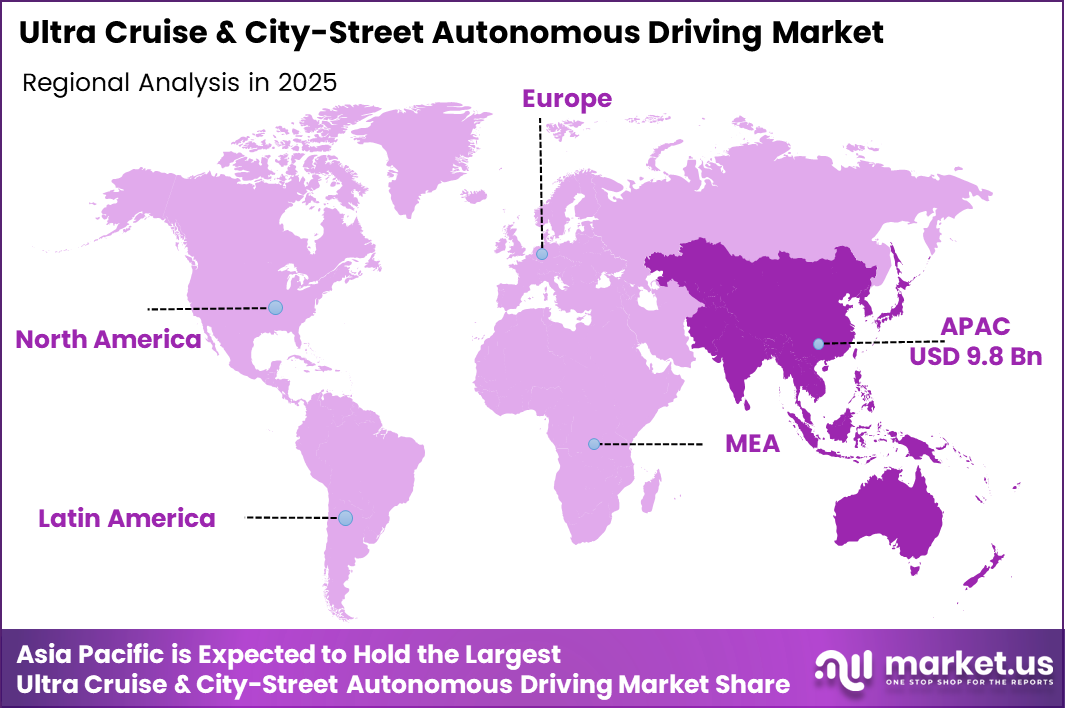

- Asia Pacific leads the regional landscape with a 43.20% market share, valued at USD 9.8 Billion.

Autonomy Level Analysis

Level 2 ADAS dominates with 65.3% due to its widespread OEM adoption and cost accessibility across mainstream vehicle segments.

In 2025, Level 2 ADAS held a dominant market position in the Autonomy Level segment of the Ultra Cruise and City-Street Autonomous Driving Market, with a 65.3% share. This segment leads due to its broad availability across mid-range and premium vehicles. Moreover, established regulatory acceptance and driver familiarity have made Level 2 systems the most commercially viable autonomy offering today.

Level 3 ADAS represents the next stage of autonomous capability, where the vehicle can manage most driving tasks under defined conditions without driver intervention. However, adoption remains limited by regulatory constraints and liability frameworks in several markets. Consequently, deployment is currently concentrated in premium segments and select geographies with favorable testing approvals and infrastructure readiness.

Operational Design Domain Analysis

Highway-Only Systems dominate with 56.6% due to structured road environments that enable reliable and consistent autonomous operation.

In 2025, Highway-Only Systems held a dominant market position in the Operational Design Domain segment of the Ultra Cruise and City-Street Autonomous Driving Market, with a 56.6% share. These systems benefit from predictable road conditions, lane markings, and limited pedestrian interaction. Therefore, they remain the most mature and commercially deployed autonomous domain available to consumers today.

City-Street Capable Systems are gaining traction as automakers push autonomy beyond structured highways into complex urban environments. Additionally, advancements in AI perception and real-time mapping are improving system performance at intersections and in mixed traffic. This segment is expected to see accelerated growth as regulatory approvals expand for urban autonomous operation.

Comprehensive/Door-to-Door Systems represent the most advanced operational domain, enabling full autonomous travel across all road types without driver involvement. However, this segment remains in early-stage commercialization due to the technical complexity and high validation requirements involved. Moreover, ongoing partnerships between automakers and AI software firms are critical to bringing these systems to broader markets.

Sensor Technology Analysis

Camera-Based Systems dominate with 38.5% due to their cost efficiency and compatibility with existing vehicle architectures.

In 2025, Camera-Based Systems held a dominant market position in the Sensor Technology segment of the Ultra Cruise and City-Street Autonomous Driving Market, with a 38.5% share. These systems offer high-resolution visual data at relatively low cost, making them the preferred baseline sensor for most OEMs. Consequently, camera technology remains the most widely deployed sensing solution across autonomy levels.

Radar-Based Systems provide robust object detection across various weather and lighting conditions, complementing camera inputs in multi-sensor architectures. Moreover, radar is particularly valued for its reliability in detecting vehicles and obstacles at highway speeds. Therefore, it is a standard component in most Level 2 and Level 3 ADAS deployments globally.

LIDAR Enabled Systems deliver precise three-dimensional environment mapping, which is essential for higher-level autonomous operation. However, historically high costs have limited adoption to premium vehicles and fleet-based programs. Additionally, ongoing manufacturing innovations are expected to reduce LIDAR pricing, enabling wider integration in mainstream autonomous platforms over the forecast period.

Multi-Sensor Fusion Systems combine camera, radar, and LIDAR inputs to create a comprehensive and redundant perception layer for autonomous vehicles. This approach significantly improves system reliability in complex urban environments. Furthermore, sensor fusion is increasingly recognized as the foundational architecture for achieving robust autonomous performance across all operational design domains.

End Use Analysis

Private/Personal Use dominates with 61.2% due to strong consumer demand for autonomous safety features in personal vehicles.

In 2025, Private/Personal Use held a dominant market position in the End Use segment of the Ultra Cruise and City-Street Autonomous Driving Market, with a 61.2% share. Consumer appetite for driver assistance features in personal vehicles continues to grow. Moreover, OEM integration of advanced autonomy features as standard or optional packages has accelerated adoption across multiple vehicle price points.

Ride-Hailing and Shared Mobility represents a high-growth end-use segment, driven by the deployment of autonomous vehicles in commercial ride services. Additionally, partnerships between autonomous technology developers and mobility platforms are expanding operational coverage in urban centers. Consequently, this segment is expected to scale rapidly as regulatory frameworks mature and public trust in autonomous ride services increases.

Commercial Fleets are increasingly adopting autonomous driving systems to improve delivery efficiency, reduce driver costs, and enhance route safety. Therefore, logistics and freight operators are actively piloting autonomous technology for last-mile and long-haul applications. However, full commercialization depends on resolving regulatory, insurance, and operational reliability challenges specific to commercial vehicle environments.

Vehicle Analysis

Passenger Vehicles dominate with 74.7% due to high consumer adoption and OEM integration of autonomy features across sedan, hatchback, and SUV models.

In 2025, Passenger Vehicles held a dominant market position in the Vehicle segment of the Ultra Cruise and City-Street Autonomous Driving Market, with a 74.7% share. This category covers personal-use vehicles where autonomous features are most commercially advanced. Moreover, strong consumer interest in safety and convenience is driving OEM investment across all passenger vehicle body types.

Within passenger vehicles, Sedan models have historically been early adopters of advanced driver assistance features due to their premium positioning. Additionally, Hatchback variants are increasingly incorporating Level 2 ADAS as automakers target broader consumer segments. Furthermore, SUV platforms benefit from larger vehicle architecture, which supports more complex sensor arrays and computing hardware for higher-level autonomy integration.

Commercial Vehicles represent a growing application area for autonomous driving technology, particularly in freight and urban delivery contexts. Therefore, LCV Light Commercial Vehicles are seeing early-stage integration of driver assistance systems for last-mile logistics. Additionally, MCV (Medium Commercial Vehicles) are being evaluated for autonomous fleet management applications across regulated urban and highway corridors.

Key Market Segments

By Autonomy Level

- Level 2 ADAS

- Level 3 ADAS

By Operational Design Domain

- Highway-Only Systems

- City-Street Capable Systems

- Comprehensive/Door-to-Door Systems

By Sensor Technology

- Camera-Based Systems

- Radar-Based Systems

- LIDAR Enabled Systems

- Multi-Sensor Fusion Systems

By End Use

- Private/Personal Use

- Ride-Hailing and Shared Mobility

- Commercial Fleets

By Vehicle

- Passenger Vehicle

- Sedan

- Hatchback

- SUV

- Commercial Vehicle

- LCV

- MCV

Drivers

Rising OEM Investment and AI Integration Drive Ultra Cruise Autonomous Driving Market Growth

Automakers are making significant investments in end-to-end autonomous driving platforms designed for both urban and highway environments. These investments are accelerating the development of production-ready systems. Moreover, competitive pressure among OEMs is pushing faster technology integration across multiple vehicle segments and price points.

Growing consumer demand for enhanced safety in dense city traffic is a key commercial driver for this market. Consequently, automakers are prioritizing driver assistance systems that reduce collision risk in complex road environments. Additionally, insurance incentives and safety ratings are further encouraging adoption of advanced autonomous features in new vehicles.

The integration of high-performance computing and AI perception systems is enabling more reliable real-time decision-making in autonomous vehicles. Therefore, chip manufacturers and AI software firms are partnering with OEMs to deliver scalable onboard processing power. Furthermore, regulatory programs supporting autonomous vehicle testing are creating a structured path for system validation and commercial deployment.

Restraints

High System Costs and Real-World Reliability Challenges Restrain Autonomous Driving Market Adoption

The cost of developing and deploying autonomous driving systems remains a significant barrier for mass market adoption. Sensors, software validation, and redundancy requirements substantially increase vehicle production costs. Consequently, full autonomy features are largely limited to premium vehicle segments, slowing the pace of broader commercialization across mid-range and entry-level markets.

Real-world reliability of autonomous systems in complex urban environments continues to be a major concern for both regulators and consumers. Additionally, unpredictable scenarios such as construction zones, erratic pedestrian behavior, and poor weather conditions expose current system limitations. Therefore, ensuring consistent safety performance across all operational conditions remains a critical technical challenge for the industry.

Software validation and system certification processes are lengthy and resource-intensive, further adding to market entry barriers. Moreover, liability frameworks for autonomous vehicle incidents remain undefined in many jurisdictions, creating commercial hesitation among OEMs and technology providers. Consequently, until clearer legal and regulatory standards are established, deployment timelines for advanced autonomous systems may be extended.

Growth Factors

Democratization of Autonomy and Smart Infrastructure Expansion Accelerate Market Growth

The expansion of autonomous features from premium vehicles to mass market segments represents a significant growth opportunity for this market. Additionally, as technology costs decline, mid-range and economy vehicle buyers are becoming viable targets for Level 2 and Level 3 ADAS integration. Therefore, volume growth in mainstream vehicle production could substantially increase overall market size over the forecast period.

Smart city infrastructure development is enabling vehicle-to-infrastructure communication, which directly enhances the operational capabilities of autonomous driving systems. Moreover, government-backed smart road initiatives in key markets are creating favorable conditions for autonomous vehicle deployment. Consequently, cities investing in connected infrastructure are becoming pilot zones for advanced autonomous technology commercialization and testing.

Strategic partnerships between automakers, semiconductor companies, and AI software providers are enabling faster and more cost-effective platform development. Furthermore, the growth of autonomous ride-hailing and shared mobility fleets in urban centers is creating scalable demand for city-street capable autonomous systems. Therefore, fleet-based deployment models are emerging as a key commercialization pathway for next-generation autonomous driving technology.

Emerging Trends

City-Street Autonomy and Sensor Fusion Adoption Define Next Phase of Market Evolution

The transition from highway-only autonomy to city-street navigation capabilities is a defining trend shaping the market’s next growth phase. Moreover, this shift requires more sophisticated AI perception, faster processing, and improved mapping accuracy for urban environments. Therefore, OEMs and technology developers are prioritizing city-capable system development as the benchmark for future autonomous vehicle platforms.

The adoption of over-the-air software updates is transforming how autonomous systems are improved and maintained post-deployment. Additionally, continuous remote updates allow manufacturers to enhance performance, fix issues, and expand operational domains without requiring physical service interventions. Consequently, this approach is becoming a standard feature in connected autonomous vehicles across premium and mainstream segments alike.

Increased use of sensor fusion, combining camera, radar, and LIDAR technologies, is becoming the industry standard for reliable autonomous perception. Furthermore, scalable autonomy platforms supporting multiple vehicle models are gaining traction as OEMs seek to reduce development costs across their portfolios. Therefore, unified hardware and software architectures are emerging as a strategic priority for automakers aiming to deploy autonomy at scale.

Regional Analysis

Asia Pacific Dominates the Ultra Cruise and City-Street Autonomous Driving Market with a Market Share of 43.20%, Valued at USD 9.8 Billion

Asia Pacific holds the largest share of the global market at 43.20%, valued at USD 9.8 Billion in 2025. The region benefits from strong government support for autonomous vehicle programs in China, Japan, and South Korea. Moreover, rapid urbanization, advanced manufacturing capabilities, and increasing OEM activity are collectively driving substantial regional market growth.

North America Ultra Cruise and City-Street Autonomous Driving Market Trends

North America is a key innovation hub for autonomous driving technology, with the United States hosting some of the world’s most active autonomous testing programs. Additionally, major OEMs and technology companies are headquartered in the region, accelerating commercial deployment. Consequently, regulatory frameworks for autonomous vehicles are among the most developed, supporting faster commercialization timelines compared to other regions.

Europe Ultra Cruise and City-Street Autonomous Driving Market Trends

Europe represents a mature and highly regulated market for autonomous driving systems, with strong OEM presence in Germany, France, and the United Kingdom. Moreover, European automakers are investing heavily in Level 2 and Level 3 ADAS platforms to meet EU safety mandates. Therefore, regional demand for advanced driver assistance technology is expected to grow steadily through the forecast period.

Latin America Ultra Cruise and City-Street Autonomous Driving Market Trends

Latin America is an emerging market for autonomous driving technology, with Brazil and Mexico leading early-stage adoption. However, infrastructure limitations and regulatory uncertainty continue to slow market development in the region. Additionally, growing vehicle sales and increasing OEM interest in connected vehicle platforms are expected to support gradual autonomous feature integration over the coming years.

Middle East and Africa Ultra Cruise and City-Street Autonomous Driving Market Trends

The Middle East and Africa region is at an early stage of autonomous driving adoption, with smart city initiatives in the GCC providing the most developed deployment environment. Moreover, government-led smart mobility programs in Saudi Arabia and the UAE are creating demand for advanced vehicle technologies. Consequently, long-term infrastructure investment is expected to gradually support wider autonomous system integration in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

BMW is a leading player in the ultra cruise and autonomous driving market, with significant investment in integrated ADAS platforms across its vehicle lineup. The company focuses on combining AI-based perception with premium vehicle engineering. Moreover, its ongoing development programs for Level 3 capable systems reflect a clear strategic commitment to urban and highway autonomous driving.

Continental is a major Tier-1 supplier driving innovation in autonomous vehicle components, including radar, camera, and sensor fusion systems. The company’s broad technology portfolio positions it as a key enabler for OEMs developing scalable autonomy platforms. Additionally, Continental’s partnerships with global automakers are accelerating the integration of advanced driver assistance technology across multiple vehicle segments and regions.

General Motors (GM) has established itself as a frontrunner in the autonomous driving space through its Ultra Cruise system, which targets hands-free driving across an expanding network of mapped roads. Furthermore, GM’s strategic consolidation of its autonomous vehicle business reflects a focused approach to deploying personal vehicle autonomy at scale. Consequently, its sensor fusion architecture is considered among the most commercially advanced in the industry.

Mercedes-Benz Group is actively pursuing Level 3 autonomous driving commercialization, having received regulatory approval for conditional automation in select markets. Therefore, the company holds a distinctive position as an early certified deployer of legally recognized autonomous systems. Moreover, its investment in software-defined vehicle architecture supports continuous over-the-air improvement of autonomous driving capabilities across its model range.

Key Players

- BMW

- Continental

- General Motors (GM)

- Mercedes-Benz Group

- Mobileye

- Nissan Motor

- NVIDIA

- Stellantis

- Toyota Motor

Recent Developments

- February 2025 – General Motors completed its acquisition of Cruise, the autonomous vehicle business, as part of a strategic pivot to developing autonomous technology for personal vehicles rather than robotaxis. This move signals a significant shift in GM’s long-term autonomy commercialization strategy.

- December 2024 – Waymo announced an expansion of its autonomous ride-hailing service to Miami, marking a key milestone in the company’s geographic growth strategy. Additionally, WeRide launched robotaxis on the Uber platform in Abu Dhabi, and Tesla began rolling out FSD version 13 to its vehicle fleet.

Report Scope

Report Features Description Market Value (2025) USD 22.8 Billion Forecast Revenue (2035) USD 112.4 Billion CAGR (2026-2035) 17.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered Autonomy Level (Level 2 ADAS, Level 3 ADAS), Operational Design Domain (Highway-Only Systems, City-Street Capable Systems, Comprehensive/Door-to-Door Systems), Sensor Technology (Camera-Based Systems, Radar-Based Systems, LIDAR Enabled Systems, Multi-Sensor Fusion Systems), End Use (Private/Personal Use, Ride-Hailing and Shared Mobility, Commercial Fleets), Vehicle (Passenger Vehicle (Sedan, Hatchback, SUV), Commercial Vehicle (LCV, MCV)) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape BMW, Continental, General Motors (GM), Mercedes-Benz Group, Mobileye, Nissan Motor, NVIDIA, Stellantis, Toyota Motor Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Ultra Cruise & City-Street Autonomous Driving MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Ultra Cruise & City-Street Autonomous Driving MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- BMW

- Continental

- General Motors (GM)

- Mercedes-Benz Group

- Mobileye

- Nissan Motor

- NVIDIA

- Stellantis

- Toyota Motor

Our Clients

- 179041

- Feb 2026