Quick Navigation

Report Overview

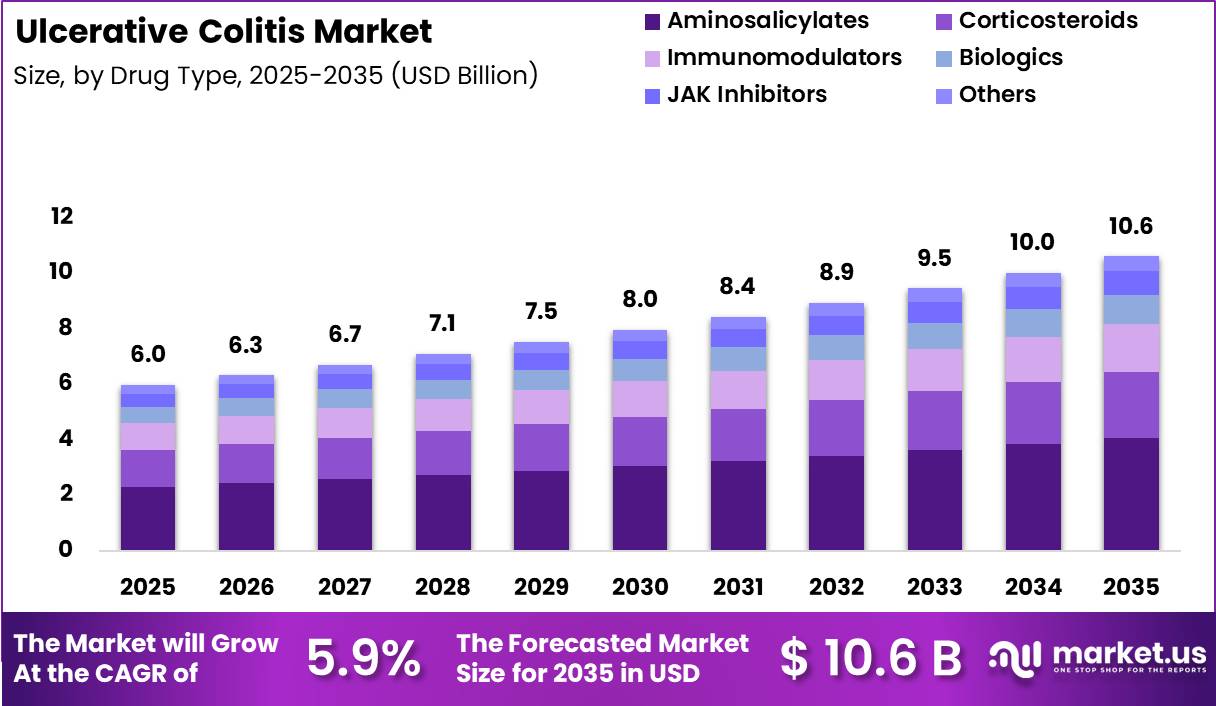

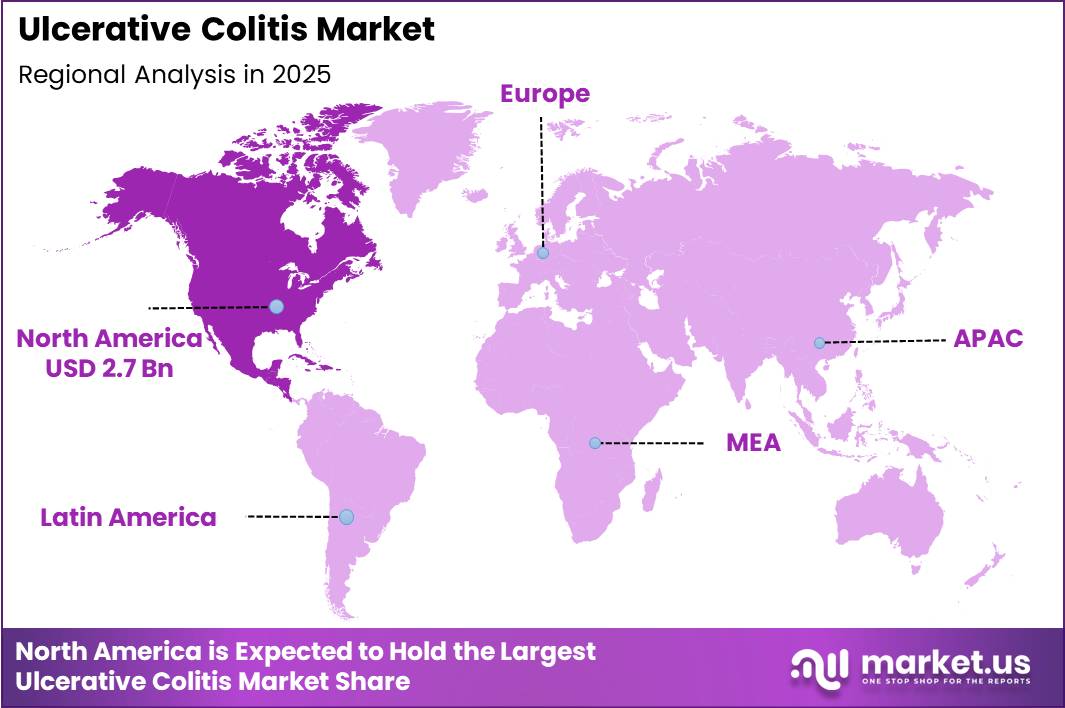

Global Ulcerative Colitis Market size is expected to be worth around US$ 10.6 Billion by 2035 from US$ 6.0 Billion in 2025, growing at a CAGR of 5.9% during the forecast period from 2026 to 2035. In 2025, North America led the market, achieving over 44.5% share with a revenue of US$ 2.7 Billion.

Ulcerative colitis is a chronic inflammatory bowel disease (IBD) characterized by persistent inflammation and ulcer formation in the mucosal lining of the colon and rectum. The disease follows a relapsing-remitting course and is associated with symptoms such as bloody diarrhea, abdominal pain, rectal bleeding, fatigue, weight loss, and an urgent need for bowel movements.

According to the U.S. Centers for Disease Control and Prevention (CDC), ulcerative colitis is the most common form of inflammatory bowel disease and represents a significant healthcare burden due to its lifelong nature and requirement for long-term disease management. The increasing prevalence of ulcerative colitis across both developed and emerging economies has become a major factor driving demand for effective therapeutic interventions.

The CDC estimates that between 2.4 million and 3.1 million people in the United States are living with inflammatory bowel disease, including ulcerative colitis, while the National Institute of Diabetes and Digestive and Kidney Diseases (NIDDK) reports that approximately 600,000–900,000 individuals in the U.S. are affected by ulcerative colitis.

The global burden of ulcerative colitis has been rising steadily, supported by urbanization, dietary changes, environmental exposures, and improved disease recognition. Epidemiological studies indicate that ulcerative colitis incidence ranges from 9 to 20 cases per 100,000 population annually, with prevalence reaching 156–291 cases per 100,000 population in several developed regions.

The disease most commonly develops between the ages of 15 and 30 years, although it can occur at any age. Advances in diagnostic technologies, including colonoscopy, endoscopy, imaging modalities, and biomarker testing, have improved early detection rates and facilitated timely treatment initiation.

The ulcerative colitis market is being transformed by the increasing adoption of advanced biologic therapies and targeted small-molecule drugs. Biologics targeting tumor necrosis factor (TNF), integrins, and interleukin pathways have significantly improved treatment outcomes for patients with moderate-to-severe disease.

In addition, ongoing research into novel immunomodulatory therapies, expanding regulatory approvals, and rising healthcare expenditure are enhancing treatment accessibility and supporting sustained growth of the ulcerative colitis therapeutic landscape worldwide.

Key Takeaways

- Market Size: Global Ulcerative Colitis Market size is expected to be worth around US$ 10.6 Billion by 2035 from US$ 6.0 Billion in 2025.

- Market Share: The market growing at a CAGR of 5.9% during the forecast period from 2026 to 2035.

- Drug Type Analysis: Aminosalicylates are expected to dominate the market, accounting for 38.5% of the total market share in 2025.

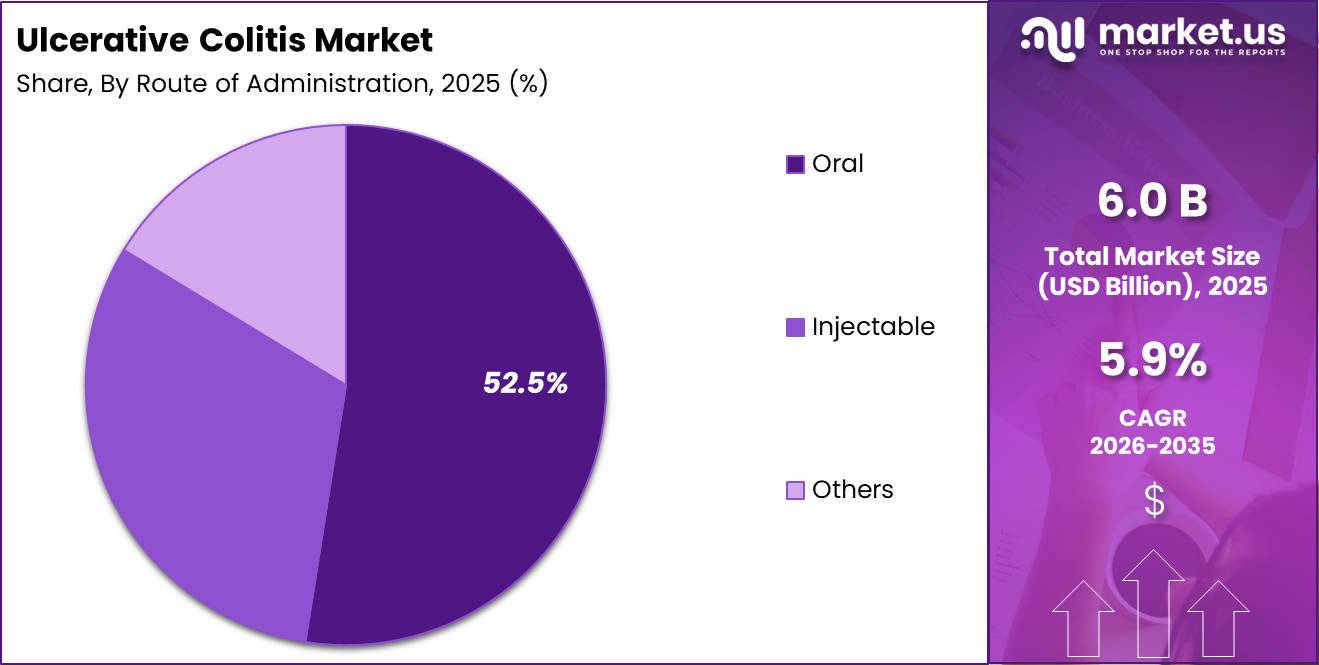

- Route of Administration Analysis: The Oral segment is projected to hold the largest market share of 52.5% in 2025

- End User Analysis: Hospitals are expected to dominate the market with a 48.5% share in 2025.

- Regional Analysis: In 2025, North America led the market, achieving over 44.5% share with a revenue of US$ 2.7 Billion.

Drug Type Analysis

The drug type segment of the Ulcerative Colitis market is categorized into Aminosalicylates, Corticosteroids, Immunomodulators, Biologics (Anti-TNF, Anti-Integrin, Anti-IL-23), JAK Inhibitors, and Others. Aminosalicylates are expected to dominate the market, accounting for 38.5% of the total market share in 2025. Their leading position is attributed to their widespread use as first-line therapy for mild-to-moderate ulcerative colitis, favorable safety profile, and long-term effectiveness in maintaining disease remission. These therapies continue to be extensively prescribed due to their proven clinical outcomes and cost-effectiveness.

Biologics represent a rapidly expanding segment, supported by increasing adoption among patients with moderate-to-severe disease and growing availability of advanced targeted therapies. Anti-TNF agents maintain a significant presence, while Anti-Integrin and Anti-IL-23 therapies are gaining traction due to enhanced efficacy and improved safety profiles. Corticosteroids remain important for short-term management of acute disease flares, although their long-term use is limited by adverse effects.

Immunomodulators continue to serve as maintenance therapies in selected patient populations. Meanwhile, JAK inhibitors are witnessing increasing demand owing to their oral administration and rapid therapeutic response. The Others segment includes emerging therapies and combination treatment approaches that contribute to market diversification.

Route of Administration Analysis

Based on route of administration, the Ulcerative Colitis market is segmented into Oral, Injectable, and Others. The Oral segment is projected to hold the largest market share of 52.5% in 2025, driven by strong patient preference for convenient and non-invasive treatment options. Oral therapies, including aminosalicylates, corticosteroids, immunomodulators, and newer JAK inhibitors, are widely prescribed due to ease of administration, improved treatment adherence, and suitability for long-term disease management. The growing availability of advanced oral formulations has further strengthened the segment’s market position.

The Injectable segment represents a substantial share of the market, primarily supported by the increasing utilization of biologic therapies for moderate-to-severe ulcerative colitis. Injectable biologics, including anti-TNF, anti-integrin, and anti-IL-23 agents, offer targeted therapeutic benefits and are increasingly recommended for patients who do not adequately respond to conventional treatments. Rising clinical acceptance of biologics and favorable treatment outcomes continue to support segment growth.

The Others segment includes rectal formulations such as enemas, foams, and suppositories, which are particularly beneficial for localized disease management. Although smaller in market size, these therapies remain important in specific treatment settings and are often used in combination with systemic therapies to enhance clinical effectiveness.

End User Analysis

Based on end user, the Ulcerative Colitis market is segmented into Hospitals, Specialty Clinics (Gastroenterology), Homecare Settings, and Others. Hospitals are expected to dominate the market with a 48.5% share in 2025, owing to their comprehensive diagnostic capabilities, multidisciplinary treatment infrastructure, and ability to manage complex and severe ulcerative colitis cases. Hospitals serve as primary centers for biologic infusions, advanced disease monitoring, surgical interventions, and emergency care, making them the preferred treatment setting for a large patient population.

Specialty Clinics, particularly gastroenterology-focused centers, represent a significant segment due to increasing demand for specialized inflammatory bowel disease management. These clinics offer personalized treatment plans, continuous patient monitoring, and access to advanced therapeutic options, contributing to their growing adoption among patients seeking specialized care.

Homecare Settings are gaining importance as healthcare systems increasingly emphasize patient-centered and cost-efficient care models. The availability of self-administered therapies, telehealth support, and remote disease monitoring technologies is facilitating treatment outside traditional healthcare facilities. This trend is particularly evident among patients receiving long-term maintenance therapy.

The Others segment includes ambulatory care centers, academic research institutions, and community healthcare facilities that support diagnosis, treatment, and follow-up care, thereby contributing to the overall expansion of the ulcerative colitis treatment landscape.

Key Market Segments

By Drug Type

- Aminosalicylates

- Corticosteroids

- Immunomodulators

- Biologics (Anti-TNF, Anti-Integrin, Anti-IL-23)

- JAK Inhibitors

- Others

By Route of Administration

- Oral

- Injectable

- Others

By End User

- Hospitals

- Specialty Clinics (Gastroenterology)

- Homecare Settings

- Others

Driving Factors

The increasing burden of inflammatory bowel disease (IBD), including ulcerative colitis, is a major driver of the ulcerative colitis market. Growing disease prevalence, increasing healthcare utilization, and the need for long-term disease management have led to higher demand for effective treatment options. Ulcerative colitis is a chronic condition that often requires lifelong monitoring, medication adjustments, and periodic diagnostic assessments, creating sustained demand for pharmaceutical therapies and healthcare services.

According to the U.S. Centers for Disease Control and Prevention (CDC), the prevalence of IBD in the United States is estimated at approximately 2.4 million to 3.1 million people. The CDC also reported that total annual healthcare costs associated with IBD reached approximately USD 8.5 billion in 2018, highlighting the substantial economic burden of these diseases. Rising healthcare expenditures are largely attributed to increased use of biologic therapies, specialist consultations, hospitalizations, and diagnostic procedures.

Furthermore, epidemiological data published by the U.S. National Library of Medicine indicate that ulcerative colitis has an annual incidence of approximately 9–20 cases per 100,000 population, with the highest disease occurrence observed among individuals aged 15–30 years.

The expanding patient population, combined with increasing healthcare spending and greater adoption of advanced therapies, continues to support growth in the ulcerative colitis market.

Trending Factors

A significant trend in the ulcerative colitis market is the transition from conventional anti-inflammatory therapies toward biologics, biosimilars, and targeted immune-modulating treatments. Modern treatment strategies increasingly focus on achieving long-term remission, mucosal healing, and improved quality of life rather than merely controlling symptoms. This shift is supported by continuous innovation in immunology and gastrointestinal disease research.

The U.S. Food and Drug Administration (FDA) has approved multiple biologic therapies for moderate-to-severe ulcerative colitis. Recent healthcare data indicate that at least eight biologic agents have been approved for ulcerative colitis treatment, including anti-TNF agents, integrin inhibitors, and interleukin inhibitors. These therapies provide targeted control of inflammatory pathways and have demonstrated superior remission outcomes compared with traditional therapies in many patient groups.

Another emerging trend is the development of biosimilars, which improve treatment affordability while maintaining clinical effectiveness. Simultaneously, precision medicine approaches involving genetic profiling, microbiome analysis, and biomarker-guided treatment selection are gaining attention. Ongoing clinical trials continue to evaluate next-generation therapies capable of achieving higher remission rates, with some recent studies reporting clinical remission in approximately 40% of treated patients.

Restraining Factors

Despite significant therapeutic advancements, the high cost of treatment remains a major restraint in the ulcerative colitis market. Biologic therapies and advanced targeted treatments often require long-term administration, increasing the overall economic burden on patients, healthcare providers, and reimbursement systems. Since ulcerative colitis is a chronic disease with periods of relapse and remission, many patients require continuous therapy for years to maintain disease control.

Biologic drugs are generally prescribed for moderate-to-severe disease and frequently involve intravenous infusions or injectable formulations administered over extended periods. Although these therapies have improved clinical outcomes, their acquisition and administration costs remain substantially higher than conventional corticosteroids and aminosalicylates. Additionally, patients receiving biologics require regular monitoring for adverse effects, including serious infections such as tuberculosis and hepatitis B, further increasing healthcare expenditures.

Treatment response variability also presents a challenge. Clinical evidence suggests that approximately 20% to 40% of ulcerative colitis patients may not achieve adequate benefit from standard therapies, necessitating treatment switching or combination approaches.

In low- and middle-income countries, limited reimbursement coverage, insufficient specialist availability, and delayed diagnosis further restrict access to advanced therapies. These factors collectively constrain treatment adoption and create barriers to broader market expansion despite increasing disease prevalence.

Opportunity

The growing emphasis on personalized medicine and the expanding pipeline of innovative therapies present substantial opportunities in the ulcerative colitis market. Advances in molecular biology, immunology, and microbiome research are improving understanding of disease mechanisms and enabling the development of highly targeted treatments. These innovations are expected to address unmet clinical needs among patients who do not respond adequately to existing therapies.

Government-supported research institutions such as the NIDDK and the National Institutes of Health continue to fund studies exploring genetic, immune-system, and microbiome-related factors associated with ulcerative colitis. Such initiatives support the identification of novel therapeutic targets and biomarkers that can improve treatment selection and patient outcomes.

Another major opportunity lies in the expansion of biosimilars and oral targeted therapies, which can improve accessibility and reduce healthcare costs. The increasing number of clinical trials evaluating next-generation agents is expected to strengthen the treatment pipeline

Furthermore, rising awareness of inflammatory bowel diseases, improved healthcare infrastructure, and growing adoption of precision medicine approaches across developed and emerging economies are expected to create favorable conditions for future market development.

Regional Analysis

North America dominated the global Ulcerative Colitis market in 2025, accounting for over 44.5% of total market revenue and reaching a valuation of US$ 2.7 billion. The region’s leadership can be attributed to the high prevalence of ulcerative colitis, advanced healthcare infrastructure, and widespread access to innovative biologic and targeted therapies.

The presence of major pharmaceutical companies, strong reimbursement frameworks, and increasing adoption of personalized treatment approaches have further supported market growth across the United States and Canada. Continuous research activities, favorable regulatory approvals, and growing awareness regarding early diagnosis and disease management have also contributed to the region’s strong market position.

Europe represented the second-largest regional market, supported by a significant patient population, well-established healthcare systems, and increasing investments in inflammatory bowel disease research. Countries such as Germany, the United Kingdom, France, and Italy have witnessed growing adoption of advanced treatment options, driving market expansion.

The Asia Pacific region is projected to register the fastest growth during the forecast period. Rising healthcare expenditure, improving diagnostic capabilities, expanding healthcare access, and increasing awareness of gastrointestinal disorders are key factors fueling demand. Emerging economies, particularly China, India, and Japan, are expected to create substantial growth opportunities for market participants.

Meanwhile, Latin America and the Middle East & Africa are experiencing gradual market development, supported by improving healthcare infrastructure, increasing disease awareness, and expanding access to specialized treatment options.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

The Ulcerative Colitis market is characterized by the presence of several global pharmaceutical companies focused on expanding their gastrointestinal and immunology portfolios through innovative therapies and strategic investments. Leading market participants include AbbVie Inc., Johnson & Johnson, Pfizer Inc., Takeda Pharmaceutical Company Limited, Eli Lilly and Company, and Bristol Myers Squibb. These companies are actively investing in research and development to introduce advanced biologics, JAK inhibitors, and targeted therapies that improve treatment outcomes and patient quality of life.

Strategic collaborations, acquisitions, and clinical trial expansions remain key growth strategies adopted by market participants to strengthen their competitive positions. Additionally, companies are focusing on obtaining regulatory approvals for novel therapies and expanding their geographic presence in emerging markets.

The increasing emphasis on precision medicine, personalized treatment approaches, and next-generation immunotherapies is expected to intensify competition and drive innovation within the global Ulcerative Colitis market over the coming years.

Market Key Players

- AbbVie Inc.

- Johnson & Johnson

- Pfizer Inc.

- Takeda Pharmaceutical Company Limited

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- Novartis AG

- Merck & Co., Inc.

- Amgen Inc.

- UCB S.A.

- Celgene Corporation (BMS)

- AstraZeneca plc

- Ferring Pharmaceuticals

- Salix Pharmaceuticals

- Others

Recent Developments

- AbbVie (January, 2025): At the start of 2025, AbbVie highlighted that SKYRIZI and RINVOQ together drove about USD 5 billion of growth in 2024 and captured roughly 50% share across inflammatory bowel disease indications, including Crohn’s disease and ulcerative colitis. Management explicitly positioned these assets as the core growth engines of the post-HUMIRA immunology portfolio, signalling sustained commercial investment and label-expansion focus in UC over the medium term.

- Johnson & Johnson (May, 2025): New long-term QUASAR extension data for TREMFYA in ulcerative colitis showed 72% of patients in clinical remission at Week 92, with 99% of those patients remaining corticosteroid-free for at least eight weeks, and endoscopic remission in 43% of patients at Week 92. This durable efficacy profile in a difficult-to-treat moderate-to-severe UC population strengthens J&J’s value proposition versus earlier biologic classes and supports premium pricing and persistent use.

- Pfizer (April, 2026): The European Commission granted approval for VELSIPITY (etrasimod), Pfizer’s S1P receptor modulator, for patients aged 16 years and older with moderate-to-severe active ulcerative colitis who have failed conventional or biologic therapy. This EU decision gives Pfizer a differentiated once-daily oral option in UC and intensifies competition with Bristol-Myers Squibb’s Zeposia in the advanced oral immunology segment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 6.0 Billion |

| Forecast Revenue (2035) | US$ 10.6 Billion |

| CAGR (2026-2035) | 5.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Drug Type (Aminosalicylates, Corticosteroids, Immunomodulators, Biologics (Anti-TNF, Anti-Integrin, Anti-IL-23), JAK Inhibitors, Others) By Route of Administration (Oral, Injectable, Others) By End User (Hospitals, Specialty Clinics (Gastroenterology), Homecare Settings, Others) |

| Regional Analysis | North America – The US, Canada; Europe – Germany, France, U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America |

| Competitive Landscape | AbbVie Inc., Johnson & Johnson, Pfizer Inc., Takeda Pharmaceutical Company Limited, Bristol-Myers Squibb Company, Eli Lilly and Company, Novartis AG, Merck & Co., Inc., Amgen Inc., UCB S.A., Celgene Corporation (BMS), AstraZeneca plc, Ferring Pharmaceuticals, Salix Pharmaceuticals, Others, |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |