Global Tubeless Tire Market Size, Share, Growth Analysis By Type (Radial Tubeless Tires, Bias Tubeless Tires), By Vehicle Type (Passenger Cars, Commercial Vehicles, Two-Wheelers), By Distribution Channel (Aftermarket, OEM), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179868

- Number of Pages: 360

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

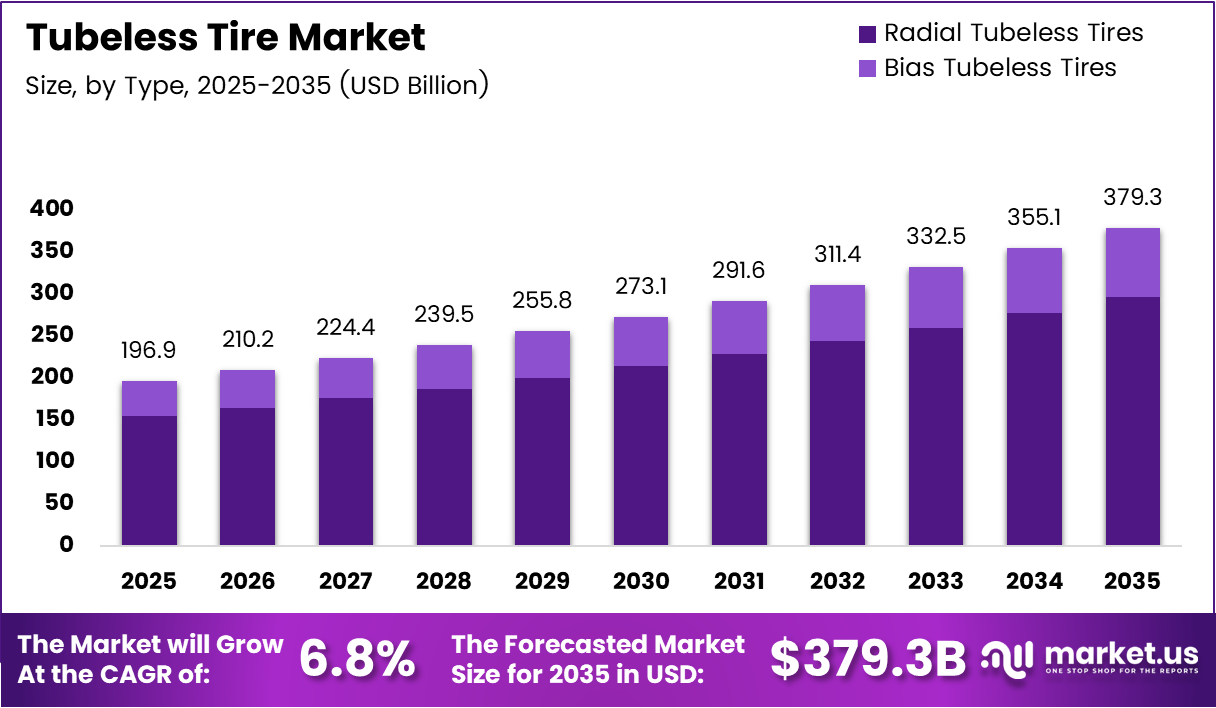

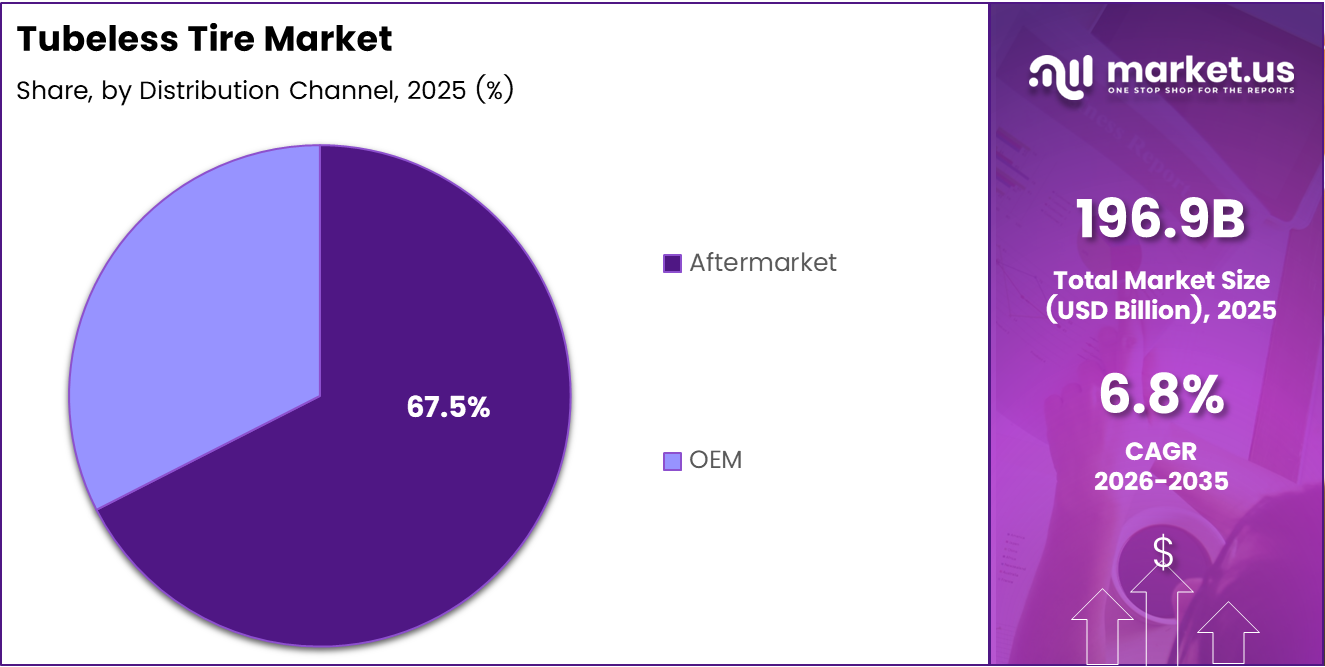

Global Tubeless Tire Market size is expected to be worth around USD 379.3 Billion by 2035 from USD 196.9 Billion in 2025, growing at a CAGR of 6.8% during the forecast period 2026 to 2035.

The tubeless tire market covers pneumatic tires that eliminate the inner tube by forming an airtight seal directly between the tire and rim. This design reduces the risk of sudden deflation and lowers rotational mass. Passenger cars, commercial vehicles, and two-wheelers all benefit from this construction across OEM and aftermarket channels.

Vehicle manufacturers globally accelerate integration of tubeless technology into new models, driven by tightening fuel economy mandates and consumer preference for lower maintenance. Radial tubeless designs now account for 78.3% of market share by type, reflecting a structural shift away from bias-ply alternatives that cannot meet modern performance standards.

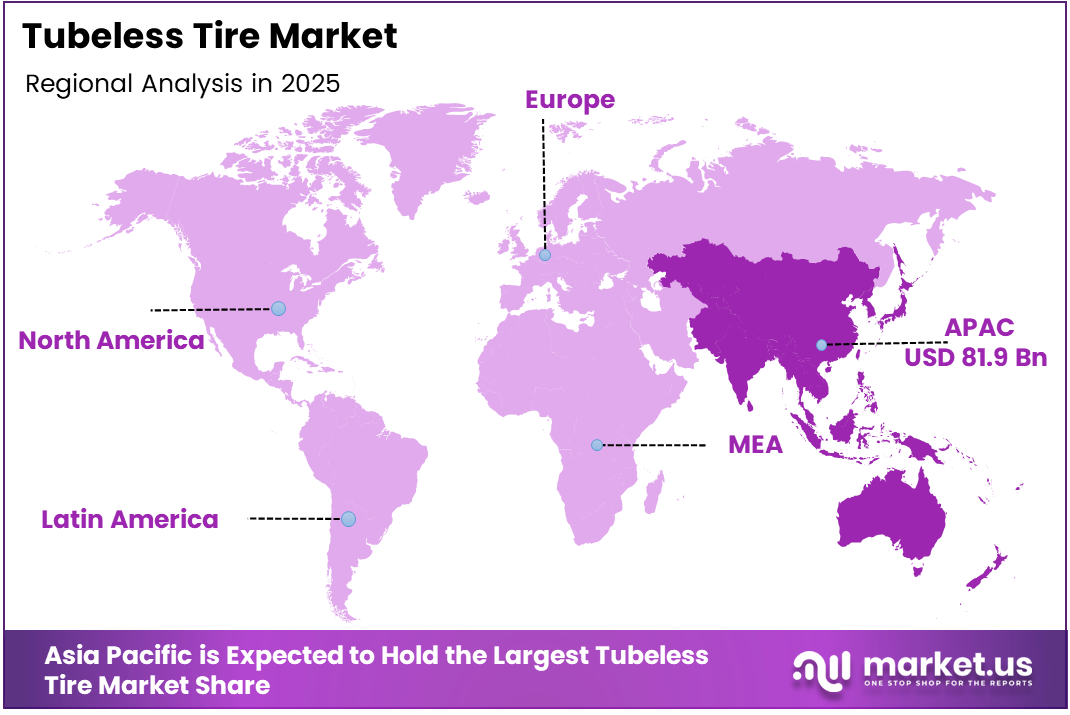

Asia Pacific anchors market expansion with a 41.60% share valued at USD 81.9 Billion. The region’s combination of high vehicle production volumes, large two-wheeler populations, and expanding middle-class car ownership creates a concentration of demand that no other geography currently replicates.

Government regulations across major economies mandate minimum fuel efficiency and safety benchmarks that bias-ply tires cannot meet. This regulatory pressure effectively pushes both OEMs and fleet operators toward tubeless radial adoption, compressing the timeline for technology transition in commercial segments.

According to Bicycle Rolling Resistance, real-world rolling resistance tests on road tubeless tires record coefficients as low as ~0.00459 at ~80 psi — a key quantified efficiency metric where lower values mean less energy lost to deformation. This performance advantage translates directly into fuel savings and extended tire lifespan, reinforcing the commercial case for tubeless adoption across vehicle categories.

According to Cycling Weekly, independent sealant testing in 2025 confirmed that top tubeless sealants sealed holes up to ~7 mm in diameter at ~70 psi under standardized puncture conditions. This performance threshold directly addresses fleet operators’ primary concern — unplanned downtime — and accelerates tubeless specification in commercial procurement decisions.

Key Takeaways

- The global tubeless tire market was valued at USD 196.9 Billion in 2025 and is forecast to reach USD 379.3 Billion by 2035.

- The market advances at a CAGR of 6.8% over the forecast period 2026 to 2035.

- By Type, Radial Tubeless Tires lead with 78.3% market share in 2025.

- By Vehicle Type, Passenger Cars dominate with 56.1% share in 2025.

- By Distribution Channel, the Aftermarket segment holds 67.5% of the market in 2025.

- Asia Pacific commands the largest regional share at 41.60%, valued at USD 81.9 Billion.

Product Analysis

Radial Tubeless Tires dominate with 78.3% due to superior fuel efficiency and regulatory compliance.

In 2025, Radial Tubeless Tires held a dominant market position in the By Type segment of the Tubeless Tire Market, with a 78.3% share. Radial construction delivers lower rolling resistance and better heat dissipation than bias alternatives, making it the default specification for OEM vehicle programs targeting fuel economy mandates. This structural advantage locks in radial preference at the design stage, before aftermarket dynamics even apply.

Bias Tubeless Tires serve niche off-road and heavy-load applications where sidewall rigidity outweighs rolling efficiency concerns. Their stiffer construction handles irregular terrain and sustained lateral stress better than radial designs. However, their declining share in passenger and commercial categories signals that application-specific demand — not broad market preference — now sustains this segment.

Vehicle Type Analysis

Passenger Cars dominate with 56.1% due to high global production volumes and fuel economy mandates.

In 2025, Passenger Cars held a dominant market position in the By Vehicle Type segment of the Tubeless Tire Market, with a 56.1% share. Consumer demand for ride comfort, fuel efficiency, and reduced puncture risk drives OEM adoption of tubeless radial tires across entry-level to premium segments. This breadth of fitment across price points creates a highly stable demand base that competitors in other vehicle categories cannot match.

Commercial Vehicles represent the segment where total cost of ownership arguments most strongly favor tubeless adoption. Fleet operators prioritize minimizing unplanned downtime, and tubeless designs reduce blowout risk on high-load axles. As electrification enters commercial fleets, low-rolling-resistance tubeless tires become a specification requirement rather than an upgrade option.

Two-Wheelers carry particular strategic weight in Asia Pacific markets, where motorcycles and scooters constitute the primary personal transport category for hundreds of millions of users. Tubeless adoption in two-wheelers accelerates as urban road quality improves and consumers recognize the safety advantage of controlled deflation over sudden blowouts at speed.

Distribution Channel Analysis

Aftermarket dominates with 67.5% due to high tire replacement frequency and consumer choice flexibility.

In 2025, the Aftermarket channel held a dominant market position in the By Distribution Channel segment of the Tubeless Tire Market, with a 67.5% share. Tires require replacement multiple times across a vehicle’s lifespan, and consumers increasingly use digital platforms to compare brands, read performance reviews, and place orders. This behavior concentrates purchasing power outside OEM contracts and creates a competitive arena where brand loyalty and pricing directly shape margin outcomes.

OEM distribution channels lock in volume through long-term automotive supply agreements, where price negotiation happens at contract stage rather than at point of sale. OEM relationships provide tire manufacturers with brand visibility at vehicle launch, directly influencing which brands consumers seek out during aftermarket replacement cycles. Winning OEM fitment, therefore, functions as a forward investment in future aftermarket share.

Key Market Segments

By Type

- Radial Tubeless Tires

- Bias Tubeless Tires

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Two-Wheelers

By Distribution Channel

- Aftermarket

- OEM

Drivers

Rising Vehicle Production, Safety Mandates, and Radial Technology Adoption Propel Tubeless Tire Demand

Global vehicle production volumes climb each year, directly expanding the base of new vehicles requiring tubeless tire fitment at factory stage. Passenger car output leads this expansion, and OEM procurement agreements for tubeless radial tires are established years before a model reaches showrooms. This forward-booking structure gives tire manufacturers predictable volume visibility that commodity suppliers rarely enjoy.

Consumer awareness of tubeless advantages — specifically reduced puncture risk and lower maintenance cost — now shapes purchasing decisions at the retail level. According to Cycling News, the 2025 Specialized S-Works Turbo TLR tubeless road tire achieved a 10% reduction in rolling resistance versus its predecessor. This measurable, independently verified performance gain strengthens the consumer case for tubeless adoption across vehicle categories, extending beyond specialist cycling into mainstream automotive.

Government safety and fuel economy regulations in the EU, North America, and key Asian markets now set performance thresholds that bias-ply tires structurally cannot meet. Regulatory compliance is no longer optional — it is a minimum market-entry requirement. Consequently, vehicle manufacturers design new platforms around tubeless radial specifications from the outset, eliminating bias-ply as a viable OEM option in regulated segments.

Restraints

High Raw Material Costs and Retrofit Complexity Limit Adoption Speed in Price-Sensitive and Legacy Segments

Premium synthetic rubber compounds, specialized steel belting, and precision rim manufacturing all contribute to tubeless tire production costs that significantly exceed conventional tube-type alternatives. For manufacturers serving price-sensitive emerging markets, these input costs compress margins to levels that make profitable volume growth difficult without sacrificing product quality or market positioning.

Retrofitting tubeless tires onto vehicles designed for tube-type systems requires rim replacement or modification, specialized mounting equipment, and trained technicians. This technical barrier adds cost and complexity for both service providers and end users. Independent repair shops in developing markets often lack the tools and training needed, effectively limiting tubeless penetration to newer vehicle fleets and organized service networks.

The combined effect of high upfront costs and retrofit complexity creates a two-speed adoption pattern: rapid uptake in premium and new-vehicle segments, slow penetration in older fleet categories and price-sensitive markets. For investors, this means tubeless market growth concentrates in higher-value segments rather than spreading uniformly, which affects total addressable market calculations for mass-market positioning strategies.

Growth Factors

Electric Vehicles, Smart Sensor Integration, and Sustainable Manufacturing Open High-Value Revenue Channels

Electric vehicles impose stricter tire performance requirements than combustion counterparts, particularly around rolling resistance, because energy recuperation budgets are fixed and range is a primary purchase concern. Tire manufacturers that develop EV-specific tubeless designs with optimized low-resistance compounds position themselves for preferred supplier status in one of the fastest-expanding vehicle segments globally.

In January 2025, Michelin launched the MICHELIN Pro5 tire with Tubeless Ready construction, reporting a ~35% improvement in forward resistance compared with its predecessor. This launch demonstrates that performance engineering investment in tubeless design yields commercially communicable results — quantified gains that procurement teams and performance-oriented buyers can act on directly rather than relying on brand reputation alone.

Self-sealing tire technologies and run-flat capabilities extend the functional envelope of tubeless systems, addressing the final objection from fleet operators who value uninterrupted operations. Additionally, IoT-connected tire sensors enable real-time pressure and wear monitoring, which shifts tire management from reactive replacement to predictive scheduling. This operational shift creates recurring software and service revenue streams that pure hardware manufacturers currently leave uncaptured.

Emerging Trends

E-Commerce Growth, Airless Prototypes, and AI-Driven Fleet Management Reshape the Tubeless Tire Value Chain

Digital retail platforms now enable consumers to compare tubeless tire specifications, read independent test data, and complete purchases without visiting a physical store. This channel shift transfers pricing power from distributors to informed consumers and forces tire brands to compete on measurable performance metrics published in public reviews. Manufacturers that invest in third-party performance validation gain a structural advantage in this transparent sales environment.

Continental extended its ContiLifeCycle range in January 2025 with the Conti Eco Gen 5 and Conti Urban HA 5 tires, adding RFID-enabled digital sensors for fleet pressure monitoring and lifecycle management. This integration of hardware and data services illustrates how leading tire manufacturers embed themselves into fleet operations, converting a one-time tire sale into an ongoing service relationship that builds switching costs and stabilizes revenue.

According to Cycling News, 2026 comparative reviews of tubeless road tires consistently report lower measured rolling resistance than equivalent tubed setups under controlled lab conditions. This persistent, independently verified performance gap signals that tubeless technology has moved from early-adopter territory into established engineering consensus — a transition that accelerates specification by conservative buyers such as fleet managers and government procurement agencies.

Regional Analysis

Asia Pacific Dominates the Tubeless Tire Market with a Market Share of 41.60%, Valued at USD 81.9 Billion

Asia Pacific commands 41.60% of the global tubeless tire market, valued at USD 81.9 Billion in 2025. China, India, Japan, and South Korea combine the world’s largest vehicle production bases with vast two-wheeler populations, creating demand density that no other region approaches. Rising household incomes across Southeast Asia further expand the passenger car and premium replacement tire segments.

North America Tubeless Tire Market Trends

North America benefits from mature automotive infrastructure, high per-capita vehicle ownership, and strict federal fuel economy standards that mandate radial tubeless adoption across passenger and light commercial categories. The U.S. aftermarket channel — supported by organized retail networks and strong digital commerce — sustains premium tire brand pricing and drives consistent replacement cycle volumes.

Europe Tubeless Tire Market Trends

Europe’s stringent EU emission and labeling regulations require tire manufacturers to meet defined rolling resistance, wet grip, and noise standards on all products sold within the bloc. These compliance requirements effectively set the minimum performance bar at a level that favors advanced tubeless radial designs. Germany’s automotive manufacturing cluster amplifies OEM fitment volumes across premium and mass-market vehicle segments.

Middle East and Africa Tubeless Tire Market Trends

Middle East and Africa present a mixed market structure: Gulf states sustain demand for premium passenger vehicle tires through high car ownership and extreme temperature operating conditions that stress conventional tire construction. Sub-Saharan Africa, by contrast, operates with older vehicle fleets where the cost of tubeless retrofit remains a barrier, concentrating near-term demand in new vehicle imports and organized fleet operators.

Latin America Tubeless Tire Market Trends

Latin America’s tubeless tire market concentrates in Brazil and Mexico, where domestic vehicle production and growing consumer spending support both OEM and aftermarket channels. Infrastructure investment in road quality across major urban corridors reduces the off-road use cases that historically favored bias-ply tires, progressively tilting replacement demand toward tubeless radial designs in the region’s largest economies.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Apollo Tyres Ltd. positions itself as a value-performance competitor in emerging markets, particularly India and Southeast Asia, where price sensitivity coexists with improving road infrastructure. Its manufacturing scale in these regions allows cost structures that global premium players cannot replicate at equivalent quality tiers, giving Apollo a structural advantage in high-volume replacement segments across Asia and parts of Africa.

Bridgestone Corporation differentiates through deep OEM relationships with global automotive manufacturers, securing fitment contracts that translate into brand recognition at the consumer replacement stage. Its investment in run-flat and IoT-enabled tire technologies aligns directly with fleet electrification trends, positioning Bridgestone to capture higher-margin service contracts as commercial fleets adopt connected vehicle platforms.

CEAT Limited concentrates strategic resources on the two-wheeler and passenger car segments across India and select international markets, where its regional distribution strength enables faster shelf availability than multinational competitors. This geographic focus reduces exposure to premium segment margin compression while allowing CEAT to deepen share in high-unit-volume replacement categories that sustain aftermarket revenue consistently across economic cycles.

Continental AG leverages its dual position as a tire manufacturer and automotive technology supplier to integrate digital sensor systems directly into tire products. Its January 2025 launch of RFID-enabled tires under the ContiLifeCycle range demonstrates a deliberate move toward data-as-a-service revenue, embedding Continental into fleet management workflows and creating subscription-oriented income streams alongside conventional tire sales.

Key Players

- Apollo Tyres Ltd.

- Bridgestone Corporation

- CEAT Limited

- Continental AG

- Giti Tire Pte. Ltd.

- Goodyear Tire & Rubber Company

- Hankook Tire & Technology Co., Ltd.

- Michelin Group

- Pirelli & C. S.p.A.

- Yokohama Rubber Company, Limited

Recent Developments

- January 2025 — Michelin launched the MICHELIN Pro5 bicycle tire featuring Tubeless Ready construction, reporting a ~35% improvement in forward resistance compared with its predecessor. This performance-focused tire targets road cyclists and long-distance riders, reinforcing Michelin’s technical leadership in the high-performance tubeless segment.

- March 2025 — Continental AG introduced the Grand Prix TR, a new road tire with tubeless-ready technology and 4-ply construction designed for strong puncture protection. The product targets broader road use across training and commuting categories, extending Continental’s tubeless portfolio beyond premium performance into everyday consumer segments.

- January 2025 — Continental extended its ContiLifeCycle tire range by launching the Conti Eco Gen 5 and Conti Urban HA 5 tires with optimized rolling resistance and optional RFID digital sensors for fleet pressure monitoring and lifecycle management. This launch supports fleet operators in reducing unplanned downtime while advancing Continental’s sustainability and connected-tire service strategy.

Report Scope

Report Features Description Market Value (2025) USD 196.9 Billion Forecast Revenue (2035) USD 379.3 Billion CAGR (2026-2035) 6.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Radial Tubeless Tires, Bias Tubeless Tires), By Vehicle Type (Passenger Cars, Commercial Vehicles, Two-Wheelers), By Distribution Channel (Aftermarket, OEM) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Apollo Tyres Ltd., Bridgestone Corporation, CEAT Limited, Continental AG, Giti Tire Pte. Ltd., Goodyear Tire & Rubber Company, Hankook Tire & Technology Co., Ltd., Michelin Group, Pirelli & C. S.p.A., Yokohama Rubber Company, Limited Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Apollo Tyres Ltd.

- Bridgestone Corporation

- CEAT Limited

- Continental AG

- Giti Tire Pte. Ltd.

- Goodyear Tire & Rubber Company

- Hankook Tire & Technology Co., Ltd.

- Michelin Group

- Pirelli & C. S.p.A.

- Yokohama Rubber Company, Limited

Our Clients

- 179868

- Feb 2026