Quick Navigation

Report Overview

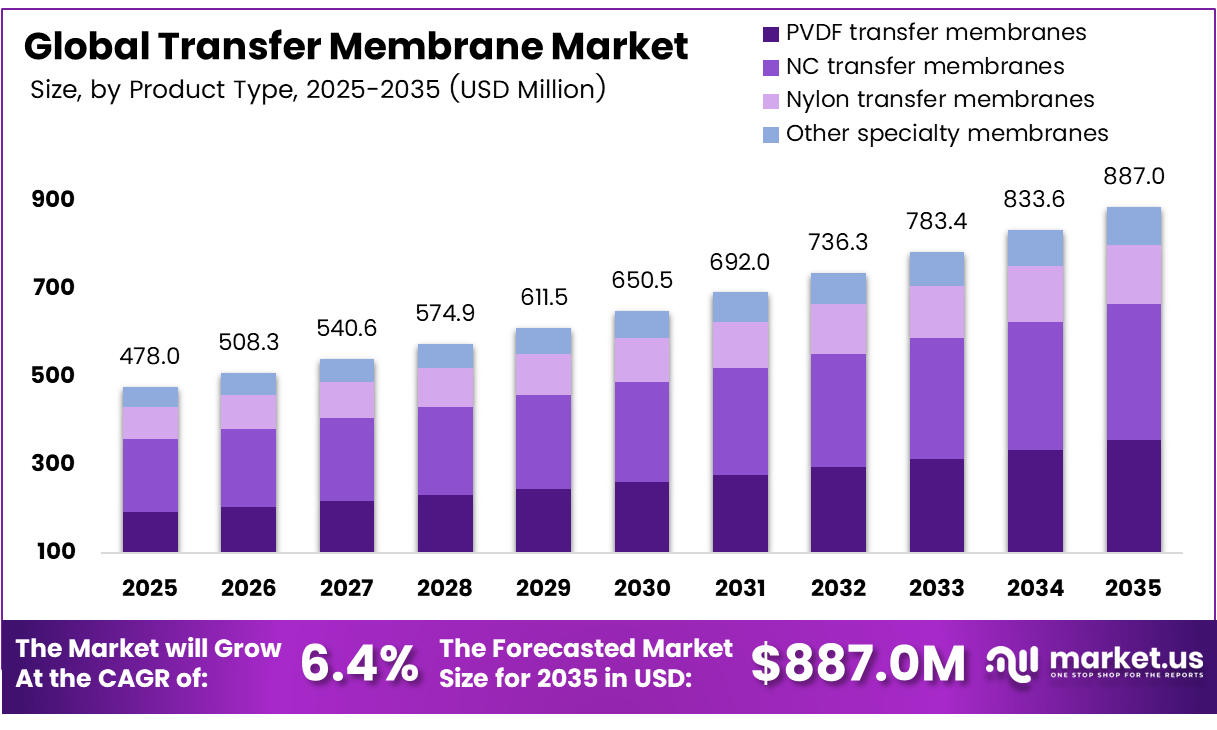

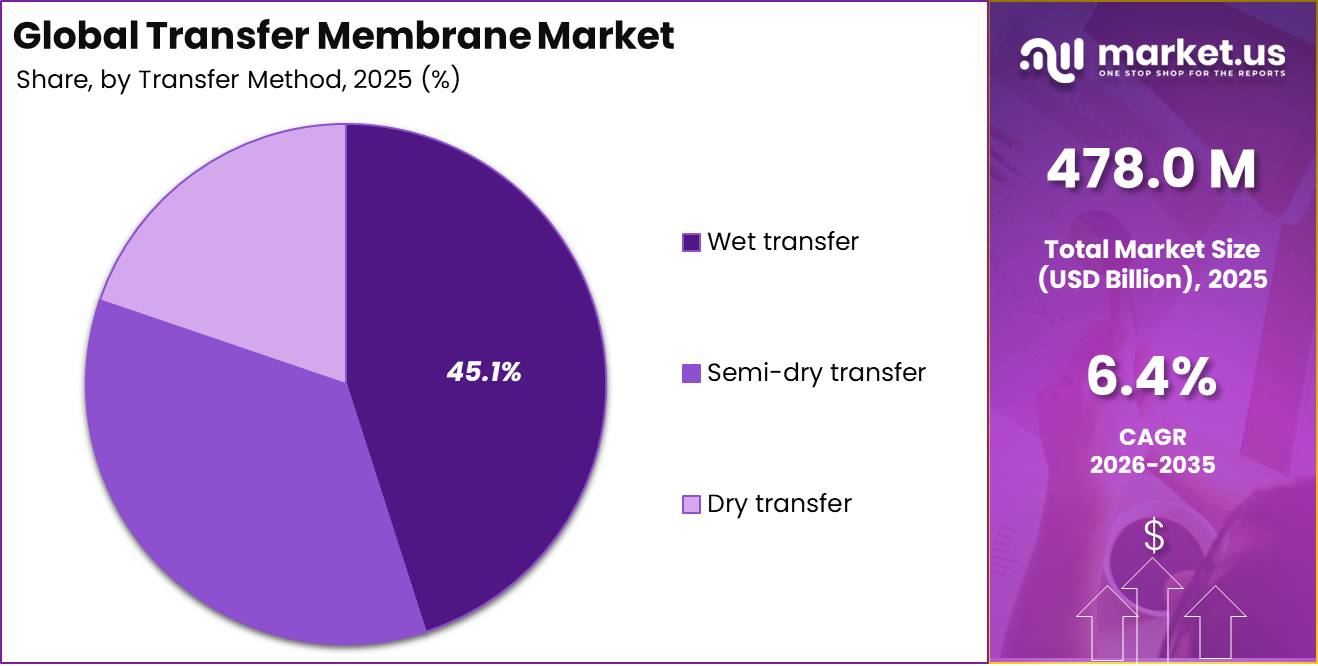

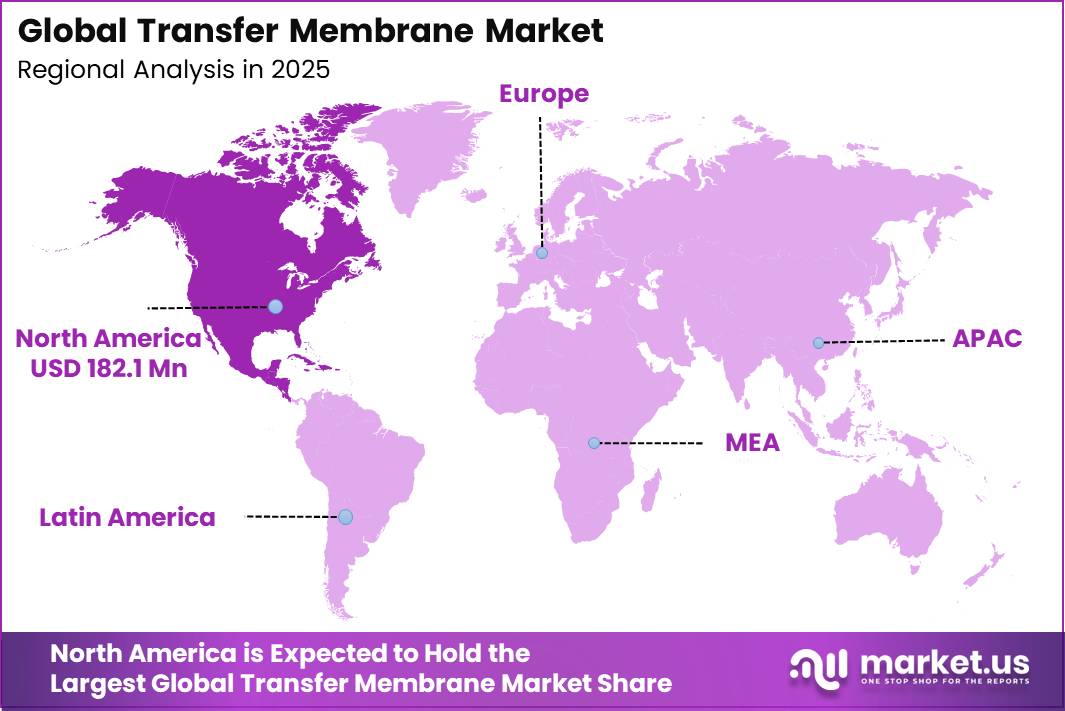

The Global Transfer Membrane Market size is expected to be worth around US$ 478.0 Million by 2025, from US$ 422.0 Million in 2024, growing at a CAGR of 6.4% during the forecast period from 2026 to 2035, reaching US$ 887.0 Million by 2035. North America held a dominant market position, capturing more than a 38.1% share, holding USD 182.1 Million in revenue.

Transfer Membranes, which include products like PVDF, Nitrocellulose, and Nylon, are very thin and porous membranes that are used for important processes in molecular biology research, such as Western Blotting, Southern Blotting, Northern Blotting, and Protein Sequencing. Transfer Membranes function by extracting proteins or nucleic acids from a gel into a solid surface membrane, where they can be analyzed. They differ from other filter materials in that transfer membranes must provide good protein binding ability, low background, chemical resistance, and reproducibility in laboratory experiments.

The growth in the transfer membrane market is attributed to the rise in biopharmaceutical research & development pipeline around the world, growing incidences of chronic and infectious diseases that require improved protein analysis capabilities, and rising application of proteomic and genomic analysis in scientific institutions and healthcare settings.

Growth in governmental investment in life sciences research, such as the US National Institute of Health annual budget surpassing $47 billion and the EU Horizon Europe research funding program, creates a robust institutional demand base for lab consumables like transfer membranes that work irrespective of economic instability.

For instance, in 2024, the European Federation of Pharmaceutical Industries and Associations (EFPIA) reported that the European pharmaceutical industry invested approximately €55 billion in R&D activities, creating sustained and large-scale institutional demand for high-quality laboratory consumables, including PVDF and nitrocellulose transfer membranes across drug discovery and quality control workflows.

Key Takeaways

- The global Transfer Membrane market was valued at approximately US$ 478.0 million in 2025.

- The global Transfer Membrane market is expected to reach US$ 887.0 million by 2035.

- The Compound Annual Growth Rate (CAGR) of the market would be at 6.4% between 2026 and 2035.

- The product segment’s market share was represented by 40.1% in the case of PVDF membranes.

- In terms of the transfer method segment, Wet Transfer was dominant with a market share of 45.1%.

- Western Blotting led the application segment, accounting for 55.4% of total application revenue.

- Pharmaceutical & Biotechnology is the leading end-user segment with 40.2% market share because of the heavy need for protein analysis in their drug discovery and quality control process.

- North America is leading in the market with 38.1% share of global revenue because of high R&D investments and the presence of pharmaceutical, biotech, and academic institutes in North America.

Product Analysis

PVDF Membranes Lead the Market Owing to Superior Protein Binding and Chemical Stability

Membranes based on polyvinylidene difluoride (PVDF) have been dominating the segment in terms of revenue contribution at 40.1%. High protein-binding capacity, solvent-resistance properties of PVDF, as well as its suitability for several detection technologies, such as chemiluminescence and fluorescence, make these membranes preferred options in pharmaceutical and proteomics laboratories.

An important characteristic of PVDF membranes is that they can be stripped and reused multiple times and still perform effectively, which makes them a perfect fit for laboratory conditions. For instance, according to Merck, Immobilon-P PVDF membranes demonstrate protein-binding capacity of up to 294 μg/cm², which means better performance compared to other types of membrane filters. Rising adoption of fluorescent detection techniques also supports the growing popularity of PVDF membranes among researchers.

For instance, Merck KGaA’s Immobilon-P PVDF membranes are used by over 2,000 pharmaceutical and academic research laboratories globally, with the product line generating consistent double-digit year-on-year reorder volumes driven by its validated performance in chemiluminescent and fluorescent Western blotting workflows.

Nitrocellulose (NC) membranes, at 34.9% revenue share is the fastest-growing type, which is favored by diagnostic labs due to their low background noise, cost-effectiveness, and quick protein-binding capabilities. Nylon membranes contribute 15.3%, while the rest of the market is covered by other specialty membranes that find use in advanced research projects.

Transfer Method Analysis

Wet Transfer Dominates Due to High Reliability and Efficient Protein Transfer Performance

The Wet Transfer category leads in the transfer method category, holding 45.1% of the market share. This category is propelling the overall revenue generation of the market due to its unrivalled capacity for full and reproducible transfer of high molecular weight proteins, which is an indispensable criterion that has to be fulfilled for drug discovery, biomarker validation, and diagnostic confirmations within the pharmaceutical and clinical lab segments.

For instance, in 2024, according to reports by Bio-Rad Laboratories, their Trans-Blot Turbo wet transfer system, which cut down the time required for protein transfer from many hours to less than 10 minutes, is currently being used by over 1,500 pharmaceutical and academic research labs in North America and Europe, where scientists have noted complete large molecular weight protein transfer capability unmatched by semi-dry systems at target sizes larger than 250 kDa.

The Semi-Dry Transfer is the fastest-growing type of transfer technology, accounting for 35.2% of the market, as it can be rapidly adopted because of its shorter processing time and compatibility with automated lab equipment. On the other hand, Dry Transfer, with a market share of 19.8%, is highly attractive because of the absence of the need for buffer solutions in transferring proteins, as well as its suitability for fast transfer procedures. The dry transfer procedure is ideal for point-of-care diagnostic testing, as well as field tests.

Application Analysis

Western Blotting Remains the Leading Application across Proteomics and Diagnostic Research

The Western blotting technique contributes 55.4% toward the total application revenues of the global market. This dominance is due to its ability to identify and quantify individual protein targets present in complex biological samples.

The technique can identify a single target protein from a pool of over 300,000 proteins. Due to its precise nature, this technique finds wide applications such as in confirmatory HIV tests, cancer marker discovery, and drug quality control. In light of projected 2.04 million new cases of cancer in America alone in 2025, according to American Cancer Society statistics, the need for high-quality protein detection methods, such as western blotting, as well as transfer membrane, is likely to witness strong growth.

The Southern blotting technique is experiencing rapid growth in terms of revenues owing to rising use in genetic fingerprinting, paternity tests, genetic disorder diagnosis, and forensic genomics areas that have received rising investments from healthcare and law enforcement agencies globally. The Northern blotting technique is mainly applied for conducting RNA expression studies. The Protein sequencing and amino acid analysis technique is widely used in quality-controlled environments.

End-User Analysis

Pharmaceutical & Biotechnology Companies Drive Market Growth through Expanding R&D Activities

The contribution from pharma and biotech companies to the revenues generated through sales of transfer membranes amounts to 40.2%. They utilize transfer membranes in drug discovery processes, quality control checks, biomarker validation studies, and regulatory testing, which in turn necessitate the use of quality membrane products.

Significantly, investments within this industry remain large, such that according to the European Federation of Pharmaceutical Industries and Associations (EFPIA), the amount spent by the European pharmaceutical industry on R&D in 2024 was about €55 billion. This, in turn, increases demand for laboratory equipment such as transfer membranes. Pharma companies acquire their membranes regularly in large, standard sizes, thus making this the most lucrative end-user category.

For instance, in 2024, Merck KGaA’s MilliporeSigma division reported that pharmaceutical and biotechnology companies accounted for over 55% of its total Immobilon PVDF membrane sales volume globally, with multi-year framework supply agreements covering QC testing workflows representing the highest-value procurement contracts within its life science consumables portfolio.

Key Market Segments

By Product

- Polyvinylidene Difluoride (PVDF) Transfer Membranes

- Nitrocellulose (NC) Transfer Membranes

- Nylon Transfer Membranes

- Other Specialty Membranes

By Transfer Method

- Wet Transfer

- Semi-Dry Transfer

- Dry Transfer

By Application

- Western Blotting

- Southern Blotting

- Northern Blotting

- Protein Sequencing and Amino Acid Analysis

- Others

By End User

- Academic and Research Institutes

- Pharmaceutical and Biotechnology Companies

- Diagnostic Laboratories and Clinical Labs

- Others

Market Dynamics

Challenge

The transfer membrane market faces a growing constraint from the shortage of skilled life sciences and laboratory professionals. In the United States, laboratories require approximately 10,000 new medical laboratory professionals each year, while accredited training programs produce only about 5,000 graduates annually, creating a 50% workforce gap. The issue is further intensified by an aging workforce, with more than 60% of laboratory professionals nearing retirement, and a 15% decline in medical laboratory training programs over the past decade. Additionally, the broader life sciences sector is projected to require 133,000 additional qualified professionals by 2030 to support ongoing research, diagnostics, and biopharmaceutical activities.

This talent shortage affects operational efficiency across research laboratories and biopharma manufacturing facilities that rely heavily on transfer membrane consumables. Competition among biopharmaceutical companies, contract research organizations, and biotech startups has increased hiring costs, driving specialist salaries up by 12–18% and raising employee training expenses by 20–30%. As laboratories struggle to fill critical scientific and quality-control positions, research throughput and diagnostic testing capacity are reduced, slowing the consumption rate of transfer membranes and limiting the market’s ability to achieve its full growth potential.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| PVDF/Fluoropolymer Raw Material Volatility | ~-0.9% | Global; acute in the EU, North America, and non-integrated producers | Short term (≤ 2 years) |

| PFAS Regulatory Compliance Burden | ~-0.7% | EU regulatory hubs, North America (US multi-state), APAC export corridors | Medium term (2–4 years) |

| Life Sciences Skilled Workforce Deficit | ~-0.6% | North America core, Western EU academic-industrial hubs | Long term (≥ 4 years) |

| Geopolitical Supply Concentration Risk | ~-0.8% | APAC (China VDF/PVDF dominance), US–China trade corridors | Medium term (2–4 years) |

| NIH/Public R&D Funding Compression | ~-0.5% | North America core; spillover to EU grant-dependent research | Medium term (2–4 years) |

| Automation-Reproducibility Integration Gap | ~-0.4% | Global; concentrated in APAC emerging lab infrastructure | Long term (≥ 4 years) |

Opportunity

The transfer membrane market has a growing opportunity in sustainable and environmentally friendly membrane materials as regulatory and procurement requirements increasingly favor low-toxicity and recyclable laboratory consumables. Restrictions under the EU’s REACH framework on solvents such as N-methyl-2-pyrrolidone (NMP) and dimethylformamide (DMF) are pressuring manufacturers to adopt alternative production methods.

Research on next-generation membrane materials has demonstrated promising performance characteristics, with PLA-based membranes produced using DMSO and deep eutectic solvents achieving water flux of 1,138 L/m²·h, approximately twice the performance of conventional solvent-cast membranes, alongside 96% oil rejection rates and 80% flux recovery ratios.

Manufacturers that develop ISO-certified green membrane platforms based on renewable polymers, green solvents, and recyclable designs could command 20–35% pricing premiums in environmentally regulated markets. Such products would also be well-positioned to benefit from sustainability-focused research funding programs, including more than EUR 5 billion in EU Horizon Europe life sciences funding streams that prioritize sustainable laboratory consumables and reagents.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Lateral Flow Assay (LFA) Membrane Supply Integration | +1.8% | North America, EU, APAC emerging markets | Short term (≤ 2 years) |

| Veterinary & Agri-Diagnostics POC Membrane Expansion | +1.2% | North America, EU, Southeast Asia | Short–Medium term (1–3 years) |

| Spatial Biology & Next-Gen Proteomics Platform Adjacency | +1.5% | North America (core), EU, Japan | Medium term (2–4 years) |

| Single-Use Bioprocessing Membrane-as-a-System Roll-Up | +2.2% | North America, EU (Germany, Switzerland) | Medium term (2–4 years) |

| Sustainable / Green Membrane Material Differentiation | +0.9% | EU (regulatory-first), North America | Medium–Long term (3–5 years) |

| M&A-Driven Vertical Integration into APAC Life Science Supply Chains | +1.6% | China, India, South Korea, Southeast Asia | Long term (≥ 4 years) |

Driver

The revised Urban Wastewater Treatment Directive in Europe, effective from 1 January 2025, is increasing demand for advanced membrane technologies by expanding wastewater treatment requirements and introducing stricter controls on nutrients, PFAS, microplastics, and other micropollutants.

For membrane suppliers, the directive creates opportunities in advanced filtration, water reuse, and monitoring applications. The inclusion of the polluter-pays principle, which requires pharmaceutical and cosmetics producers to fund at least 80% of advanced micropollutant removal costs, further strengthens market demand by supporting ongoing operational spending in addition to capital investments.

The European Commission’s estimate of approximately €6.6 billion in annual benefits by 2040 highlights the economic significance of the framework, while its regulatory model may influence future wastewater treatment upgrades in the Asia-Pacific and other regions.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Biologics scale-up raises high-value membrane turns | +2.1% | North America core, EU, Japan, South Korea, China biologics hubs | Short term (≤ 2 years) |

| Annex 1 sterility compliance increases validation-grade demand | +1.6% | EU core, UK spill-over, North America regulated exports | Short term (≤ 2 years) |

| Single-use and intensified processing lift membrane consumption per line | +1.4% | North America core, EU, APAC bioprocessing corridors | Medium term (2–4 years) |

| Urban wastewater micropollutant rules expand advanced membrane pull | +1.8% | EU core, water-stressed APAC corridors, selective Middle East spill-over | Medium term (2–4 years) |

| Regional capacity localization reduces supply risk and adoption friction | +1.0% | North America core, Japan supply base, EU strategic buyers | Short term (≤ 2 years) |

| PFAS and micropollutant monitoring tightens replacement and upgrade cycles | +0.9% | EU core, North America selective, advanced APAC municipalities | Medium term (2–4 years) |

Restraint

PFAS-related regulatory scrutiny is emerging as a restraint for the transfer membrane market because membrane products are increasingly evaluated within broader fluoropolymer, laboratory, and water-testing compliance frameworks. The EU’s recast Drinking Water Directive introduced mandatory PFAS monitoring requirements from January 2026, while the broader EU PFAS restriction process continues to advance through regulatory review stages.

These compliance obligations increase operating costs and slow product development cycles, particularly for smaller suppliers that may need to invest heavily in reformulation, validation, and material-substitution programs. Compliance activities can add significant annual overhead and extend product change-control timelines by 6–12 months, reducing commercialization speed and increasing barriers to market entry.

Consequently, many OEM and laboratory customers are favoring larger, compliance-ready suppliers, creating a competitive disadvantage for smaller vendors and contributing to an estimated 0.8 percentage-point reduction in market CAGR, particularly across Europe and highly regulated North American markets.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Membrane raw-material volatility | -0.9% | NA, EU, China, India | Short term (≤ 2 years) |

| PFAS and polymer compliance risk | -0.8% | EU core, NA regulated labs | Medium term (2–4 years) |

| Diagnostic/IVD certification drag | -0.7% | EU, UK, export hubs in APAC | Medium term (2–4 years) |

| Supplier concentration in nitrocellulose/PVDF | -0.8% | Global, acute in EU-APAC corridors | Short term (≤ 2 years) |

| Lab budget tightening and CapEx deferral | -0.6% | North America, Western Europe | Short term (≤ 2 years) |

| Workflow substitution by membrane-light assays | -0.7% | US, EU, Japan, Korea | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Trade Policy Dynamics, Supply Chain Concentration, and Research Funding Frameworks Reshaping the Global Transfer Membrane Market

The geopolitical trends impact the transfer membrane market through issues in the supply of raw materials, funding mechanisms, and access to various regional markets. The production of specialist polymers such as PVDF and more advanced nitrocellulose is highly centralized in a few countries, including the US, Germany, and Japan, exposing the segment to risks whenever there is geopolitical instability in the regions.

The geopolitics between the US and China has helped develop independent biopharmaceutical chains that have made China’s life sciences sector less reliant on Western products from membrane producers. On a positive note, the geopolitical tailwinds for the segment are evident in the form of governmental initiatives aimed at promoting research funding, including the European Union’s Horizon Europe program, as well as research efforts in the US valued at above US$ 679 billion per year.

Export control regulations of biotechnology materials pose regulatory challenges for producers working in regions considered sensitive by their governments. Nevertheless, increasing bilateral agreements in life sciences between the EU, the US, and Asian-Pacific nations have been gradually creating new institutional customers.

Regional Analysis

North America Leads the Global Transfer Membrane Market, Driven by Strong Biopharmaceutical Ecosystem

North America represents the leading market with a 38.1% global revenue share in 2025, holding USD 182.1 Million in revenue, driven by the United States as the world’s most advanced biopharmaceutical research and manufacturing hub. The region’s dominant position in the global transfer membrane market is underpinned by several structural advantages that competing regions have not yet replicated at an equivalent scale or institutional depth.

The presence of robust diagnostic facilities for management of chronic diseases such as cancer, cardiovascular disease, and autoimmune diseases further ensures recurring clinical needs for membranes outside the research cycle, coupled with North America’s stringent US FDA regulatory regime, which ensures defined membrane validation guidelines.

For instance, in 2024, the National Cancer Institute (NCI) allocated over US$ 6.9 billion toward cancer research programs across US academic and clinical institutions, directly sustaining demand for Western blotting transfer membranes used in protein biomarker discovery and oncology diagnostic confirmation workflows throughout North America.

Europe holds roughly 24% of global market share, owing to its wide scope of publicly financed research initiatives, state-of-the-art biotechnology centers in Germany, France, and the UK, along with robust EU-level research spending via the initiative, Horizon Europe. The region with the highest growth rate of 5.94% CAGR is Asia Pacific, powered by increased production of biopharmaceuticals, backed by government initiatives in life science, and increasing academic research capabilities in China, India, South Korea, and Japan.

Key Regions and Countries Covered in this Report

North America

- U.S.

- Canada

Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of Asia Pacific

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC Countries

- South Africa

- Rest of Middle East & Africa

Key Players Analysis

Competitors among transfer membrane makers focus on their ability to differentiate themselves through technology innovation, novel materials, and reliable supply chain management in order to maintain a position within the industry, which requires absolute consistency in laboratory-grade product performance.

One such area is continuous innovation into material, for example, next-generation PVDFs with better binding properties, very low background nitrocellulose membranes, and fluorescently optimized membranes. Another area is integration into workflows through the use of bundle packages of membranes, buffers, and detectors.

Vertical integration of specialty polymers can help mitigate the risk of supply chain issues during geopolitical instability in chemical manufacturing. Geographical capacity expansion in the Asia-Pacific market can help them align with the rapidly growing needs of both biopharmaceutical and academic research customers in that region. Other strategies involve lot-to-lot consistency certification, GMP documentation, and contracts with major pharmaceutical procurement agencies.

Market Key Players

- Merck KGaA

- Thermo Fisher Scientific Inc.

- Bio-Rad Laboratories Inc.

- Danaher Corporation

- PerkinElmer Inc.

- Abcam plc

- Santa Cruz Biotechnology Inc.

- ATTO Corporation

- Azure Biosystems Inc.

- Advansta Inc.

- GVS S.p.A.

- GE Healthcare / Cytiva

- Macherey-Nagel GmbH & Co. KG

- Carl Roth GmbH + Co. KG

- Axiva Sichem Biotech

- Cobetter Filtration

- HiMedia Laboratories

- Others

Recent Developments

- In January 2026, Thermo Fisher Scientific enhanced its Pierce protein blotting portfolio with membranes that are compatible with automated wet transfer systems, cutting transfer time by 40% for clinical research. This launch responds to the increasing demand from pharmaceutical quality control laboratories in North America and Europe for time-efficient, validated blotting workflows that integrate to the automated laboratory infrastructure already in place.

- In March 2026, Bio-Rad Laboratories introduced Low-fluorescence nitrocellulose membranes optimized for multiplex fluorescent Western blotting to meet the growing demand from oncology biomarker research labs for high-sensitivity, low-background protein detection across multiple targets. This announcement solidifies Bio-Rad’s position as the industry leader in fluorescence detection as labs transition from chemiluminescence to multiplex fluorescent imaging operations.

- In April 2026, Cytiva (Danaher) signed a multi-year supply agreement with a top-5 global biopharmaceutical company for Amersham Protran PVDF membranes across QC testing processes, bolstering Cytiva’s institutional supply chain leadership in the premium pharmaceutical membrane category. Large biopharmaceutical procurement departments continue to favor proven, GMP-certified PVDF membrane vendors, as seen by this arrangement.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 478.0 Million |

| Forecast Revenue (2035) | US$ 887.0 Million |

| CAGR (2026-2035) | 6.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (PVDF, Nitrocellulose, Nylon, Other Specialty Membranes), By Transfer Method (Wet Transfer, Semi-Dry Transfer, Dry Transfer), By Application (Western Blotting, Southern Blotting, Northern Blotting, Protein Sequencing & Amino Acid Analysis, Others), By End User (Academic & Research Institutes, Pharmaceutical & Biotechnology Companies, Diagnostic Laboratories & Clinical Labs, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC – China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America – Brazil, Mexico & Rest of Latin America; Middle East & Africa – GCC, South Africa & Rest of MEA |

| Competitive Landscape | Merck KGaA, Thermo Fisher Scientific, Bio-Rad Laboratories, Danaher (Cytiva/Pall), PerkinElmer (Revvity), Abcam, Santa Cruz Biotechnology, ATTO Corporation, Azure Biosystems, Advansta, GVS S.p.A., Macherey-Nagel, Carl Roth, Axiva Sichem Biotech, Cobetter Filtration, HiMedia Laboratories, and Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |