Global Toothpaste Market Size, Share, Growth Analysis By Product Type (Conventional, Herbal, Whitening & Sensitive), By End User (Adults, Kids), By Distribution Channel (Supermarket/Hypermarket, Independent Retail Stores, Pharmacies, Online Stores, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181803

- Number of Pages: 329

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

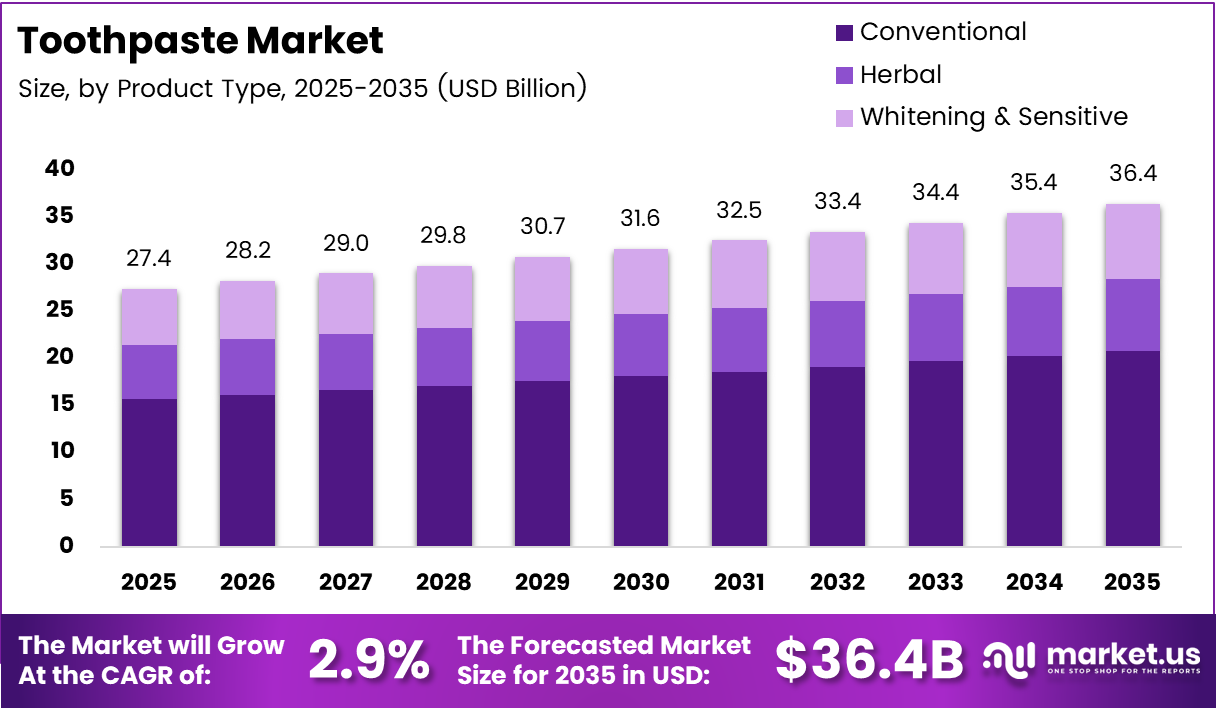

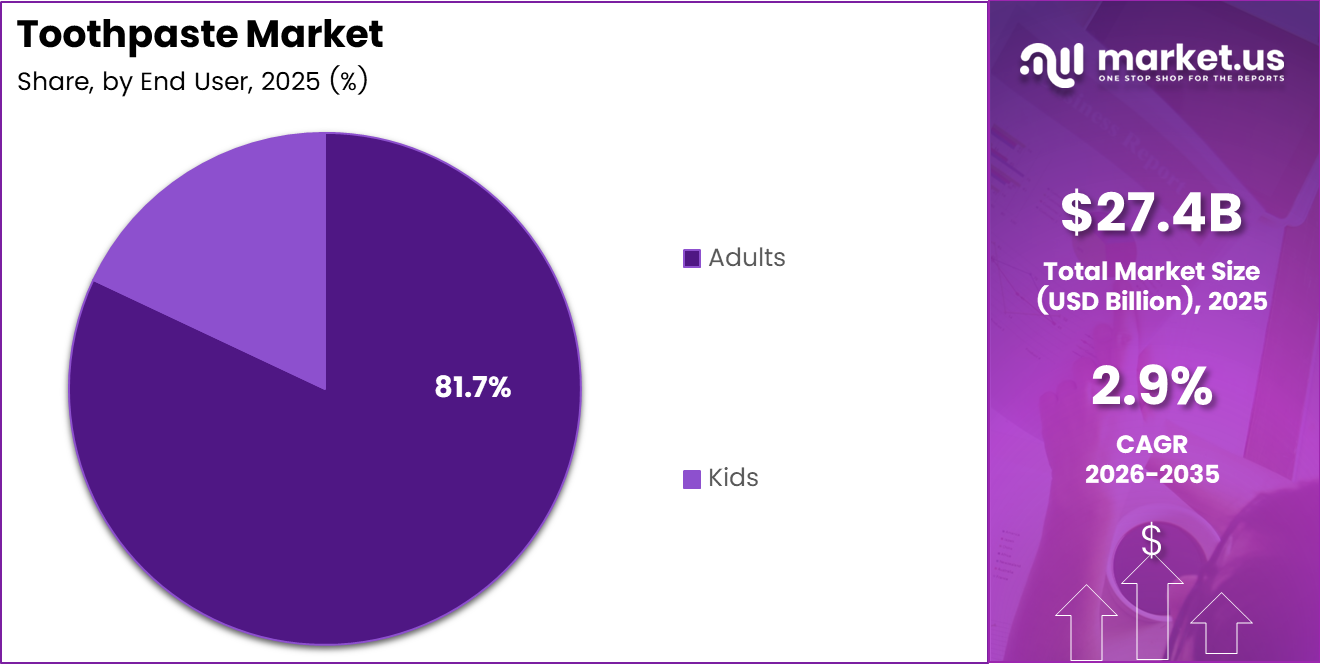

Global Toothpaste Market size is expected to be worth around USD 36.4 Billion by 2035 from USD 27.4 Billion in 2025, growing at a CAGR of 2.9% during the forecast period 2026 to 2035.

The toothpaste market sits at the intersection of everyday consumer necessity and health-driven premiumization. Buyers across income segments purchase oral care products consistently, which creates a structurally stable revenue base. However, the real growth pressure comes from consumers actively trading up to specialized formulations — whitening, sensitivity relief, and herbal variants — that carry higher margins.

Urbanization in emerging economies accelerates this shift. As disposable incomes rise in markets across Asia, Africa, and Latin America, consumers move away from basic fluoride paste toward products with functional and wellness claims. This behavioral pattern expands both the addressable market and the average selling price, creating compounding revenue impact for brands positioned in the premium tier.

Government-backed oral health campaigns in several countries now actively shape purchasing behavior. Health ministries in India, Brazil, and Southeast Asian nations have integrated toothpaste use into public hygiene mandates, effectively expanding the addressable population. For manufacturers, these campaigns reduce the cost of market education and accelerate first-time adoption in underpenetrated rural zones.

In 2024, Unilever launched the Pepsodent Expert range of specialist toothpastes, including the GumExpert variant clinically proven for gum health improvement. This move reflects a broader industry pivot — brands are increasingly anchoring commercial claims on clinical validation, raising the bar for product development and signaling to buyers that therapeutic benefit, not just hygiene, now drives purchase decisions.

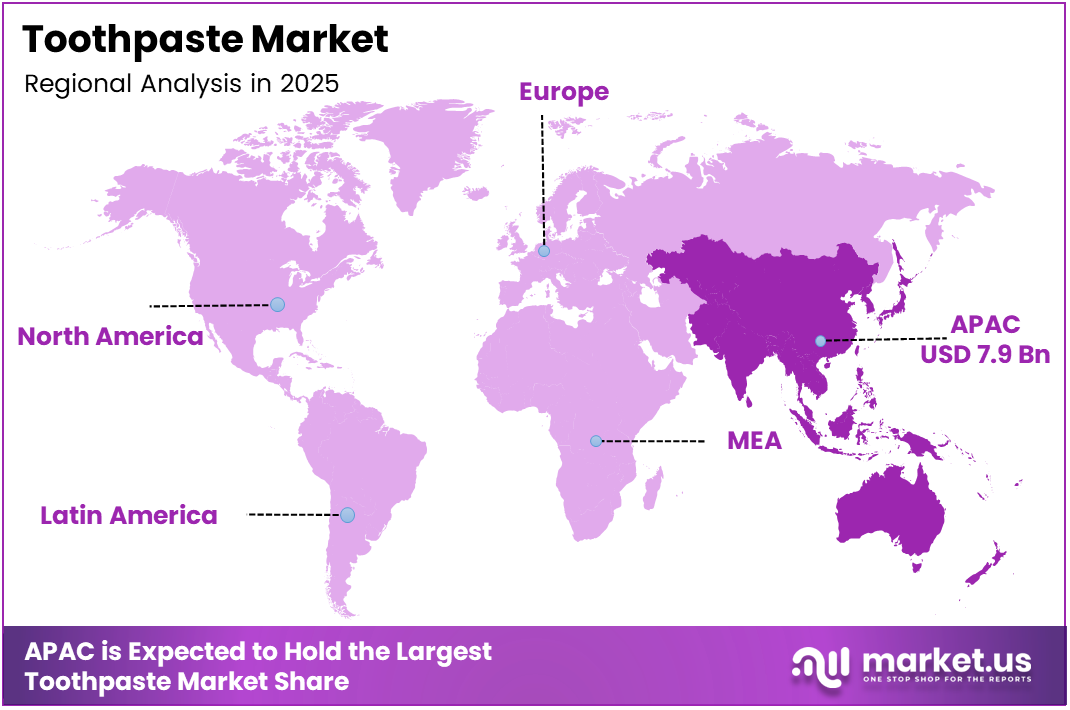

According to market data, the Asia Pacific region holds a 43.70% share of the global toothpaste market, valued at USD 7.9 Billion. This concentration reflects the region’s scale advantage — population density, rising middle-class income, and accelerating urban retail infrastructure all converge to make APAC the single most consequential growth arena for toothpaste brands over the next decade.

According to segmentation data, the Conventional toothpaste segment commands 57.2% of the market by product type. This dominance tells us that most buyers still prioritize familiar formulations and accessible price points over premium alternatives. However, the fastest revenue growth sits in herbal and specialized segments, meaning the market’s value expansion will outpace its volume expansion as product mix shifts upward.

Taken together, these signals point to a two-speed market: stable, high-volume conventional sales providing the revenue floor, while premium and functional segments drive incremental margin growth. Investors and brand managers who understand this duality will allocate R&D and distribution resources more precisely than those who treat the market as a single, uniform category.

Key Takeaways

- The global toothpaste market was valued at USD 27.4 Billion in 2025 and is forecast to reach USD 36.4 Billion by 2035.

- The market advances at a CAGR of 2.9% over the forecast period 2026 to 2035.

- By Product Type, Conventional toothpaste leads with a 57.2% market share in 2025.

- By End User, Adults dominate with an 81.7% share of total market consumption.

- By Distribution Channel, Supermarket/Hypermarket holds the largest share at 45.8%.

- Asia Pacific dominates regional performance with a 43.70% share, valued at USD 7.9 Billion.

Product Type Analysis

Conventional toothpaste dominates with 57.2% due to widespread affordability and mass consumer familiarity.

In 2025, Conventional toothpaste held a dominant market position in the By Product Type segment of the Toothpaste Market, with a 57.2% share. This leadership reflects deeply embedded purchasing habits and broad retail availability rather than innovation-led demand. For brand managers, this segment offers volume stability but limited margin expansion — the real pricing power lies in adjacent categories.

Herbal toothpaste serves as the fastest-shifting value segment within oral care. Consumer preference for natural, fluoride-free formulations has pulled investment from both established conglomerates and Ayurvedic-focused challenger brands. In September 2025, Unilever expanded its Signal brand with new herbal variants across Asia, confirming that multinational players now treat herbal as a strategic priority rather than a niche offering.

Whitening and Sensitive toothpaste carries the highest perceived value among functional sub-categories. Buyers in this segment actively seek clinically backed claims, driving premium pricing and repeat loyalty. Consequently, this segment attracts disproportionate R&D investment from major brands because even modest share gains translate into outsized margin improvement relative to conventional product lines.

End User Analysis

Adults dominate with 81.7% due to consistent daily use across the entire adult population.

In 2025, Adults held a dominant market position in the By End User segment of the Toothpaste Market, with an 81.7% share. This near-total dominance reflects universal oral hygiene behavior among working-age and senior populations. Moreover, adults increasingly purchase specialized formulations — whitening, sensitivity, and herbal — which elevates the average transaction value and strengthens revenue per user compared to standard household purchases.

Kids toothpaste differentiates through flavor innovation, safe-to-swallow formulations, and pediatric branding. While the segment accounts for a smaller revenue share, it carries strategic importance as a brand entry point — parents who trust a brand for their children frequently carry that loyalty into adult product purchases. Additionally, demographic growth in emerging markets expands the addressable kids segment meaningfully over the forecast period.

Distribution Channel Analysis

Supermarket/Hypermarket dominates with 45.8% due to high footfall and multi-brand shelf availability.

In 2025, Supermarket/Hypermarket held a dominant market position in the By Distribution Channel segment of the Toothpaste Market, with a 45.8% share. This channel dominates because it allows side-by-side brand comparison, supports impulse purchase behavior, and benefits from promotional pricing. For manufacturers, shelf positioning in major hypermarket chains remains the single most consequential placement decision in the go-to-market strategy.

Independent Retail Stores serve as the primary access point in semi-urban and rural markets where organized retail infrastructure remains underdeveloped. These outlets stock fewer SKUs and rely on distributor relationships rather than brand-led merchandising. However, their proximity to cost-sensitive consumers keeps them structurally relevant, particularly in South and Southeast Asian markets where modern trade penetration remains incomplete.

Pharmacies differentiate through association with therapeutic and clinical oral care products. Consumers who purchase sensitivity or medicated toothpaste specifically seek pharmacy channels because of the implied professional endorsement. This channel commands a narrower but more loyal buyer segment, and brands with clinical positioning benefit disproportionately from pharmacy shelf presence.

Online Stores enable direct-to-consumer access and support subscription models that reduce churn. E-commerce platforms allow newer herbal and premium brands to build a national footprint without the capital cost of physical retail expansion. Additionally, algorithm-driven discovery exposes health-conscious shoppers to specialized formulations they may never encounter on a conventional retail shelf.

Others encompasses convenience stores, direct sales, and institutional channels such as dental clinics and corporate wellness programs. While this category holds a smaller share individually, institutional dental channel placement carries high credibility because a dentist-recommended product benefits from a trust transfer that no advertising campaign can replicate cost-effectively.

Key Market Segments

By Product Type

- Conventional

- Herbal

- Whitening & Sensitive

By End User

- Adults

- Kids

By Distribution Channel

- Supermarket/Hypermarket

- Independent Retail Stores

- Pharmacies

- Online Stores

- Others

Drivers

Health Campaigns and Functional Demand Accelerate Toothpaste Adoption Across Consumer Segments

Global oral hygiene awareness campaigns, led by health ministries and dental associations, have systematically expanded the consumer base for toothpaste across developing markets. According to segmentation data, Adults represent 81.7% of end users — a figure that reflects near-universal habitual purchase behavior. This near-saturation among adults means market expansion now depends on frequency of trade-up, not first-time adoption.

Consumers are actively shifting toward specialized formulations addressing sensitivity and whitening needs. This shift matters because functional products carry meaningfully higher price points than standard paste, expanding revenue without requiring equivalent volume growth. Brands that front-load investment in clinical validation gain a durable pricing advantage because buyers in the sensitivity and whitening segment respond to evidence, not promotions.

Rising disposable incomes in emerging economies compound this effect. Urban consumers in India, Southeast Asia, and Africa now access premium oral care that was previously out of reach. In September 2025, Unilever expanded its Signal brand with new herbal variants across Asia, confirming that multinational brands are deploying premium portfolio extensions precisely where income growth and aspirational purchasing converge.

Restraints

Counterfeit Products and Price Barriers Limit Penetration of Advanced Toothpaste Formulations

Counterfeit and substandard toothpaste products remain a serious structural barrier in developing markets. These products undercut legitimate brands on price while eroding consumer trust in the category overall. For premium and herbal brands specifically, the presence of fake alternatives creates a credibility gap that suppresses trial among price-sensitive buyers who cannot easily verify product authenticity at the point of purchase.

High pricing on advanced formulations — particularly whitening, sensitivity, and herbal variants — restricts access among lower-income consumer cohorts. This creates a bifurcated market where volume sits at the low end and value sits at the premium end, with limited overlap. Brands attempting to bridge this gap through mid-tier positioning face margin compression from both directions simultaneously.

Colgate’s achievement of 101% plastic waste collection under Extended Producer Responsibility in FY 2025 illustrates that sustainability compliance adds operational cost for manufacturers. While environmentally necessary, these compliance investments increase production costs that are difficult to pass through in markets where buyers already resist price increases — further compressing margins in price-sensitive distribution channels.

Growth Factors

E-Commerce Expansion and Demographic-Specific Segments Open New Revenue Channels for Oral Care Brands

Online retail channels remove the geographic and capital constraints that historically limited specialty toothpaste brands to urban, organized retail markets. Brands with herbal, pediatric, or elderly-specific formulations can now reach consumers in tier-2 and tier-3 cities without physical distribution networks. According to distribution data, Supermarket/Hypermarket currently controls 45.8% of sales — online’s expansion directly challenges this concentration and redistributes channel power over the forecast period.

Personalized oral care delivered via digital platforms represents a structurally new revenue stream. Subscription models, AI-driven product recommendations, and custom formulation services are emerging as differentiated offerings that command premium pricing and reduce churn. Additionally, personalization data gives brands direct consumer insight that traditional retail channels never provided, enabling more precise product development and targeted marketing spend.

Haleon’s investment of £65 million to build a new oral care manufacturing site in Shanghai — supporting Sensodyne and Parodontax production expansion — signals that major players are committing capital to meet anticipated demand growth in Asia. This facility investment reflects a strategic read that APAC’s premiumization trajectory justifies long-cycle infrastructure spending, and that brands without regional manufacturing scale will face cost disadvantages as competition intensifies.

Emerging Trends

Zero-Waste Formats, Ayurvedic Formulations, and Bio-Active Ingredients Reshape the Toothpaste Product Landscape

Toothpaste tablets and zero-waste delivery formats are gaining commercial traction as eco-conscious consumers reject single-use plastic tubes. This format shift is not merely a sustainability gesture — it opens new retail channels including refill stores, subscription boxes, and premium health retailers that conventional tube formats cannot access. Brands entering this space early establish format ownership before the category standardizes.

The boom in Ayurvedic and traditional medicine-based oral care in Asia Pacific reflects a deeper consumer trust realignment. Buyers increasingly treat ancient formulation systems as evidence of efficacy rather than tradition alone. This trend benefits India-origin brands with established Ayurvedic credentials, but multinational players are rapidly acquiring or licensing heritage formulations to participate in this segment’s revenue growth.

Integration of bio-active and clinically proven ingredients — including hydroxyapatite, activated charcoal, and probiotic compounds — is shifting buyer expectations toward therapeutic outcomes. According to segmentation data, the Conventional segment still holds 57.2% share, but the direction of new product launches moves consistently toward functional ingredients. Early movers who establish clinical credibility in bio-active formulations will define the premium positioning benchmark as the market’s product mix continues to shift.

Regional Analysis

Asia Pacific Dominates the Toothpaste Market with a Market Share of 43.70%, Valued at USD 7.9 Billion

Asia Pacific commands a 43.70% share of the global toothpaste market, valued at USD 7.9 Billion, driven by the region’s population scale, accelerating middle-class expansion, and government oral health mandates in markets like China and India. The region also hosts several high-growth Ayurvedic and herbal brand ecosystems that attract both domestic capital and multinational acquisition interest, making it the most contested competitive arena in the category.

North America Toothpaste Market Trends

North America sustains a mature but high-value position in the global toothpaste market, underpinned by strong consumer spending on premium and specialized oral care. The region’s well-established dental care system actively drives clinical product recommendations, supporting above-average adoption of whitening and sensitivity formulations. Organized retail infrastructure and advanced e-commerce penetration further concentrate purchasing power in channels that favor premium SKUs.

Europe Toothpaste Market Trends

Europe’s toothpaste market benefits from stringent product safety regulations that raise the barrier for substandard products and reward brands with verified clinical claims. Western European consumers show strong preference for natural ingredient formulations and sustainable packaging, trends that align with the broader portfolio shift toward herbal and zero-waste delivery formats. Germany, France, and the UK function as lead markets where new product concepts prove commercial viability before wider European rollout.

Middle East and Africa Toothpaste Market Trends

The Middle East and Africa region presents a dual market structure: GCC countries show demand patterns comparable to premium Western markets, while Sub-Saharan Africa remains primarily conventional and price-driven. Rising urbanization rates and expanding organized retail in countries like South Africa, Nigeria, and Kenya are gradually widening the accessible market for mid-tier products. This structural divergence within the region requires distinct pricing and channel strategies from brands operating across both sub-markets.

Latin America Toothpaste Market Trends

Latin America offers meaningful volume upside as urban household incomes rise and organized retail expands beyond major metropolitan centers. Brazil and Mexico anchor regional demand and serve as primary test markets for new product launches. However, currency volatility and price sensitivity in smaller markets constrain premium product penetration, meaning most regional volume growth continues to concentrate in conventional formulations at accessible price tiers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Amway positions its oral care portfolio within a broader wellness ecosystem, leveraging its direct-selling distribution model as a structural differentiator. Unlike mass-market competitors dependent on retail shelf placement, Amway delivers products directly to end consumers through a network of independent business owners. This model creates higher customer retention but limits market breadth, making Amway most effective in markets with mature direct-selling cultures.

Dabur International Ltd occupies a distinctive strategic position by anchoring its oral care identity in Ayurvedic heritage. As consumer preference for herbal and natural formulations accelerates across Asia and the Middle East, Dabur’s formulation credibility becomes a commercial asset that synthetic-first competitors cannot replicate quickly. The brand’s challenge is scaling its herbal positioning into Western markets where Ayurvedic authority requires significant consumer education investment.

Colgate-Palmolive Company operates with unmatched global distribution reach and brand recognition, giving it a structural advantage in conventional and mid-tier toothpaste segments. In FY 2025, three of Colgate’s Indian manufacturing plants — Sri City, Sanand, and Goa — achieved Net Zero Water status, demonstrating that the company integrates sustainability into operations at a scale few competitors can match, reinforcing its positioning with regulators and ESG-focused institutional buyers.

Johnson & Johnson approaches the oral care market through a clinical and therapeutic lens, aligning its products with health system recommendations and professional dental channels. This positioning commands a loyalty premium among consumers who prioritize evidence-based oral health outcomes over cosmetic claims. However, the company’s narrower portfolio focus means it captures less share in the mass-market conventional segment, concentrating its competitive advantage in the higher-margin specialist tier.

Key Players

- Amway

- Dabur International Ltd

- Colgate Palmolive Company

- Johnson & Johnson

- Glaxosmithkline Plc

- Patanjali Ayurved Ltd

- Procter & Gamble

- Henkel Ag & Co

- Arms & Hammer

- Unilever

Recent Developments

- September 2024 — Haleon announced plans to increase its stake in its Chinese joint venture to 88% ownership through a USD 637 million investment, signaling a strategic commitment to direct market control in China’s fast-growing oral care segment.

- June 2025 — Haleon completed the full acquisition of its TSKF joint venture in China with an investment of approximately £700 million, gaining direct control of its Over-the-Counter business and consolidating its premium oral care position in Asia’s largest market.

- FY 2025 — Colgate transitioned its entire toothpaste portfolio in India to 100% recyclable tubes using patented technology open-sourced globally, becoming the first and only company in India to achieve this milestone and setting a new industry benchmark for sustainable packaging compliance.

- January 2025 — Colgate’s Sanand Plant expanded on-site solar capacity by 0.250 MW DC, generating 350,000 kWh of green energy annually and boosting renewable electricity usage by 2%, with projected yearly savings of USD 28,000 in energy costs.

- FY 2025 — Colgate’s Goa Plant replaced fixed-speed chillers with energy-efficient magnetic bearing chillers using variable speed drives, reducing chiller energy consumption by 40% and achieving overall plant energy savings of 1,450,000 kWh, representing a 12% plant-level energy reduction.

Report Scope

Report Features Description Market Value (2025) USD 27.4 Billion Forecast Revenue (2035) USD 36.4 Billion CAGR (2026-2035) 2.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Conventional, Herbal, Whitening & Sensitive), By End User (Adults, Kids), By Distribution Channel (Supermarket/Hypermarket, Independent Retail Stores, Pharmacies, Online Stores, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Amway, Dabur International Ltd, Colgate Palmolive Company, Johnson & Johnson, Glaxosmithkline Plc, Patanjali Ayurved Ltd, Procter & Gamble, Henkel Ag & Co, Arms & Hammer, Unilever Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Amway

- Dabur International Ltd

- Colgate Palmolive Company

- Johnson & Johnson

- Glaxosmithkline Plc

- Patanjali Ayurved Ltd

- Procter & Gamble

- Henkel Ag & Co

- Arms & Hammer

- Unilever

Our Clients

- 181803

- Mar 2026