Quick Navigation

Report Overview

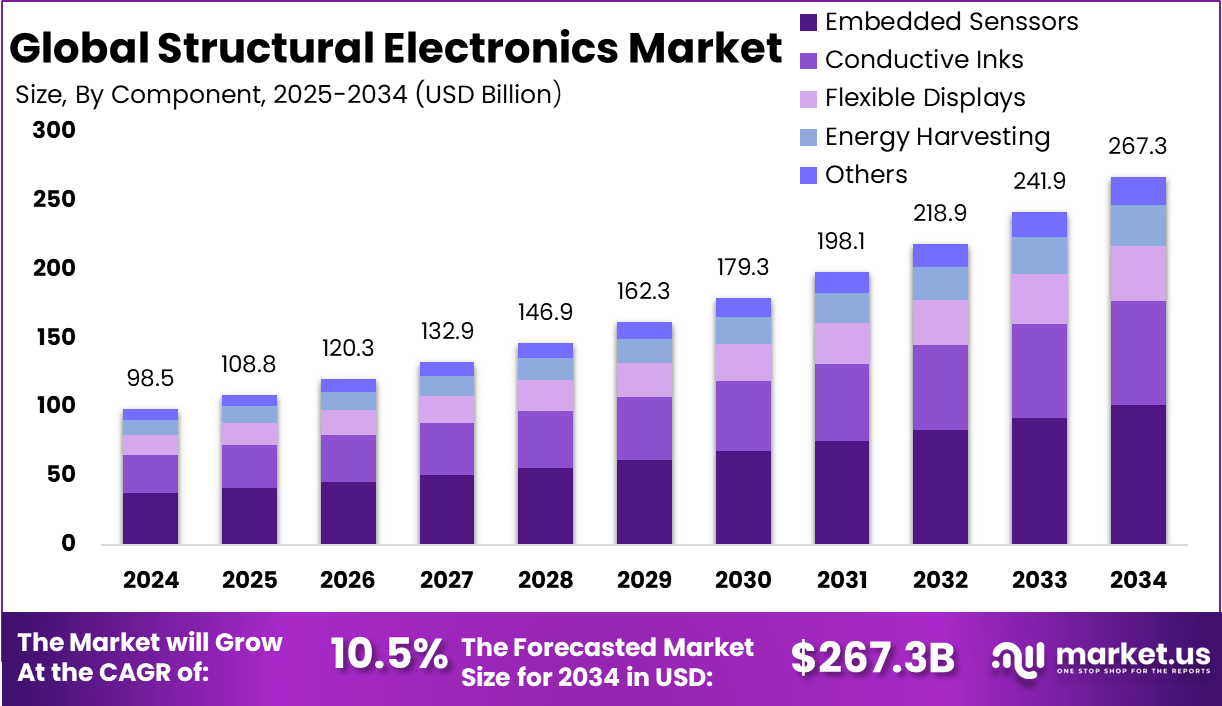

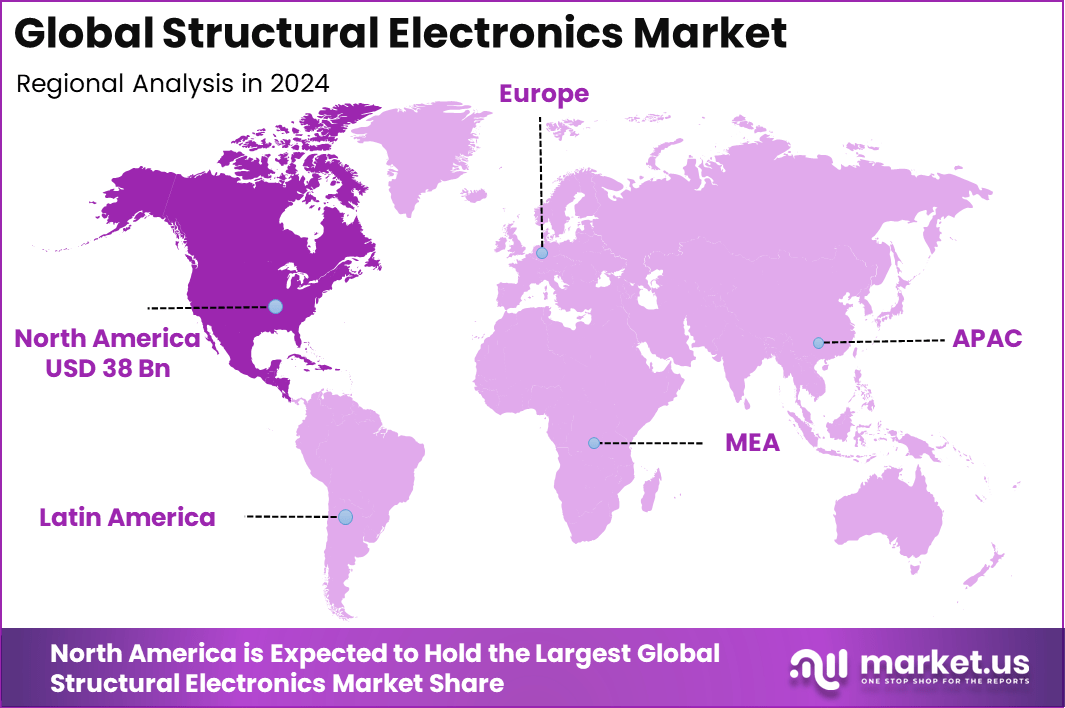

The Global Structural Electronics Market size is expected to be worth around USD 267.3 billion by 2034, from USD 98.5 billion in 2024, growing at a CAGR of 10.5% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 38.6% share, holding USD 38 Billion in revenue.

The structural electronics market is experiencing significant growth, driven by the integration of electronic functionalities directly into structural components. This innovation is transforming industries by enabling the development of lighter, more efficient, and multifunctional products.

Key drivers of this market include the rising demand for lightweight and compact electronic devices, advancements in material science, and the increasing adoption of electric vehicles (EVs) and wearable technologies. The automotive and aerospace sectors, in particular, are leveraging structural electronics to reduce weight and improve fuel efficiency.

The demand for structural electronics is escalating across various sectors. In the automotive industry, the integration of sensors and circuits into vehicle bodies enhances safety and performance. The aerospace sector benefits from weight reduction and increased reliability. Consumer electronics are seeing a surge in demand for flexible and wearable devices, which rely on structural electronics for functionality.

For instance, In March 2025, TactoTek, a Finnish leader in In-Mold Structural Electronics (IMSE®) technology, secured $60 million in funding led by Nidoco AB, part of Virala Group. This investment aims to accelerate the global adoption of IMSE® technology by expanding customer-facing operations and streamlining solution delivery processes.

The funding round attracted a consortium of financial and strategic investors, including Elo Mutual Pension Insurance Company, 3M Ventures, European Investment Bank, and Kyocera Corporation. TactoTek plans to utilize this capital to enhance its technology platform, support global expansion, and strengthen its leadership in sustainable electronics solutions.

Key Takeaway

- In 2024, the embedded sensors segment led the market, capturing a 38% share, due to its critical role in enabling real-time performance monitoring and adaptive electronic functionalities within structural materials.

- The polymer segment emerged as the most dominant material type, accounting for 52% of the market share, driven by its lightweight properties, flexibility, and cost-efficiency in automotive and aerospace integration.

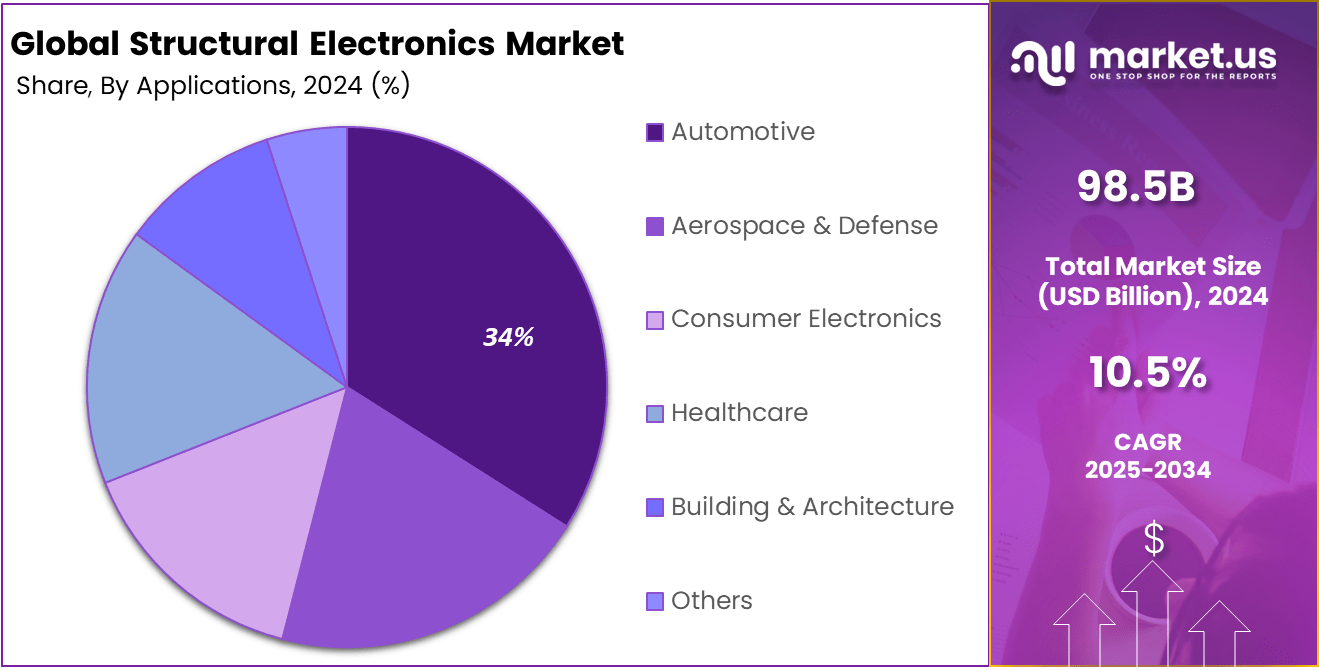

- By application, the automotive sector commanded a 34% share in 2024, fueled by the rising use of embedded electronics in EVs, ADAS, and smart interiors to enhance both safety and design flexibility.

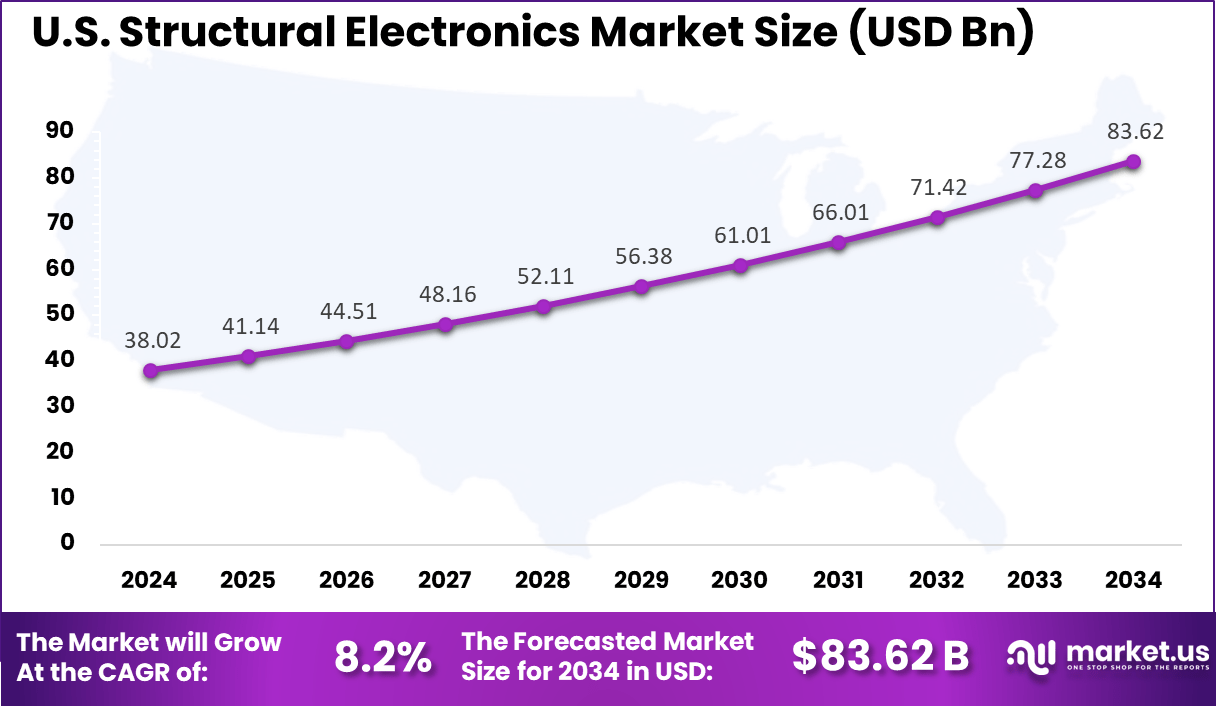

- The U.S. structural electronics market was valued at USD 38.02 billion in 2024, reflecting strong momentum and is expected to grow at a CAGR of 8.2%, supported by advanced manufacturing capabilities and increased investment in smart mobility solutions.

- North America remained the global leader, capturing over 38.6% share of the structural electronics market in 2024, underpinned by robust R&D, presence of key players, and high demand from the automotive and aerospace sectors.

U.S. Market Size

The US Structural Electronics Market is valued at approximately USD 38.2 Billion in 2024 and is predicted to increase from USD 56.38 Billion in 2029 to approximately USD 83.62 Billion by 2034, projected at a CAGR of 8.2% from 2025 to 2034.

The expansion can be largely attributed to increasing adoption of structural electronics in the automotive, aerospace, and consumer electronics sectors, where the need for lightweight, flexible, and space-saving solutions continues to grow.

As manufacturers look for ways to enhance design freedom and improve product efficiency without adding bulk, structural electronics are becoming an integral part of next-generation product development across the U.S. industrial landscape.

For instance, In November 2023, NextFlex awarded $6.5 million to support Flexible Hybrid Electronics (FHE) projects targeting extreme environments and sustainability. The funding backs innovations like 3D multilayer electronics, reliable temperature-resistant interconnects, and in-mold electronics for automotive use. These efforts aim to boost structural electronics manufacturing and strengthen the U.S. position in advanced technologies.

In 2024, North America held a dominant market position in the global Structural Electronics Market, capturing more than a 38.6% share, holding USD 38 Billion in revenue. A combination of technological innovation, strategic alliances, and a strong emphasis on sustainability are driving the structural electronics market’s notable expansion in North America.

An atmosphere that is favorable to the development of structural electronics has been created by the region’s strong infrastructure and large investments in research and development. Further driving market expansion has been the growing need for lightweight, multipurpose components in sectors including consumer electronics, automotive, and aerospace.

For instance, In August 2023, TactoTek partnered with Universal Recycling Technologies (URT) to create a recycling ecosystem for in-mold structural electronics (IMSE). This collaboration focuses on sustainable recycling of production waste and end-of-life components, supporting broader adoption of IMSE technology. The initiative highlights North America’s drive to advance structural electronics through eco-friendly and innovative practices.

Component Analysis

In 2024, the Embedded Sensors segment held a dominant market position in the structural electronics market, capturing more than a 38% share. This leadership is attributed to the increasing integration of sensors into structural components across various industries, including automotive, aerospace, and consumer electronics.

The demand for real-time monitoring and data collection has driven the adoption of embedded sensors, enabling functionalities such as structural health monitoring, predictive maintenance, and enhanced safety features. Advancements in sensor miniaturization and wireless communication technologies have further facilitated their seamless incorporation into complex structures without compromising design or functionality.

For instance, In January 2025, Texas Instruments (TI) launched the AWRL6844 60GHz mmWave radar sensor, featuring built-in edge AI to enable functions such as seat belt alerts, child presence detection, and intrusion monitoring – all within a single chip. This breakthrough reduces reliance on multiple sensors, cuts vehicle costs by around $20 per unit, and strengthens the role of embedded systems in modern automotive applications.

The automotive industry, in particular, has witnessed significant growth in the use of embedded sensors for applications like tire pressure monitoring, airbag deployment systems, and advanced driver-assistance systems (ADAS). Similarly, in aerospace, embedded sensors are crucial for monitoring the integrity of aircraft structures, thereby enhancing safety and reducing maintenance costs.

Material Analysis

In 2024, the polymers segment held a dominant market position in the structural electronics market, capturing more than a 52% share. This leadership is attributed to the increasing integration of polymers into structural components across various industries, including automotive, aerospace, and consumer electronics.

The demand for lightweight, flexible, and cost-effective materials has driven the adoption of polymers, enabling functionalities such as structural health monitoring, energy harvesting, and enhanced safety features. Advancements in polymer science and processing technologies have further facilitated their seamless incorporation into complex structures without compromising design or functionality.

In October 2024, researchers at Northwestern University introduced a new class of biodegradable polymers inspired by nature and plastics. These materials are designed to deliver high performance while minimizing environmental harm, supporting the structural electronics industry’s push toward sustainability.

Application Analysis

In 2024, the automotive segment held a dominant position in the structural electronics market, capturing more than a 34% share. This leadership is primarily attributed to the increasing integration of electronic functionalities directly into vehicle structures, enhancing performance, safety, and design flexibility.

The shift towards electric vehicles (EVs) and autonomous driving technologies has accelerated the adoption of structural electronics, as these vehicles require advanced systems for energy efficiency, weight reduction, and real-time data processing.

For instance, In March 2025, Valeo partnered with TactoTek to integrate IMSE® technology into next-generation automotive lighting systems. This collaboration focuses on developing advanced interior and exterior lighting features, including visual alerts for ADAS, dynamic displays with color effects, and customizable elements like logos

Automotive manufacturers are leveraging structural electronics to embed sensors, circuits, and energy storage components into the vehicle’s body and interior surfaces. This integration reduces the need for separate electronic modules, leading to lighter vehicles with improved fuel efficiency and reduced emissions.

Key Market Segments

By Component

- Embedded Sensors

- Conductive Inks

- Flexible Displays

- Energy Harvesting

- Others

By Material

- Polymers

- Composites

- Metals

By Application

- Automotive

- Aerospace & Defense

- Consumer Electronics

- Healthcare

- Building & Architecture

- Others

Drivers

Demand for Lightweight, Multi-Functional Materials

The structural electronics market is significantly driven by the increasing demand for lightweight, multi-functional materials, particularly in the automotive and aerospace sectors. These industries prioritize weight reduction to enhance fuel efficiency and performance.

Structural electronics integrate electronic functionalities directly into load-bearing structures, eliminating the need for separate electronic components and thereby reducing overall weight. This integration not only contributes to weight savings but also enhances design flexibility and functionality.

Restraint

High Manufacturing Costs and Technological Complexity

Despite the promising advantages, the structural electronics market faces significant restraints due to high manufacturing costs and technological complexities. The integration of electronic components into structural materials requires advanced manufacturing techniques, such as in-mold electronics and 3D printing, which involve substantial capital investment and specialized expertise.

These factors contribute to elevated production costs, making it challenging for widespread adoption, especially among small and medium-sized enterprises. Additionally, the technological complexity associated with designing and fabricating structural electronics poses a barrier to entry for new players in the market.

For instance, In March 2025, Simcona highlighted the ongoing shortage of electronic components as a major challenge for supply chains, particularly in structural electronics. Lead times for key parts like semiconductors have remained unpredictable, ranging from 12 to 40 weeks.

This shortage stems from lingering effects of COVID-19 factory shutdowns, rising geopolitical tensions affecting raw material supplies, and growing demand from sectors like automotive, consumer electronics, and AI.

Opportunities

Integration with Electric Vehicles (EVs)

The expand electric vehicle (EV) market presents a significant opportunity for the adoption of structural electronics. EVs demand lightweight and energy-efficient components to maximize battery life and driving range.

Structural electronics offer a solution by embedding electronic functionalities directly into the vehicle’s structure, thereby reducing weight and improving energy efficiency. This integration is particularly beneficial for applications such as battery enclosures, sensor systems, and lighting components.

Furthermore, advancements in materials and manufacturing processes are making it increasingly feasible to produce structural electronic components at scale. Collaborations between automotive manufacturers and electronics companies are also accelerating the development and integration of these technologies.

Challenges

Maintenance and Repair Complexity

One of the primary challenges associated with structural electronics is the complexity of maintenance and repair. Unlike traditional electronic systems, where components can be easily accessed and replaced, structural electronics involve embedded components within the structural elements of a product.

This integration complicates the repair process, as accessing and replacing faulty components may require disassembling or even destroying parts of the structure. Such complexities can lead to increased maintenance costs and downtime, particularly in critical applications like aerospace and automotive industries.

For instance, In November 2024, STMicroelectronics encountered major setbacks affecting its structural electronics efforts, particularly within the automotive and aerospace sectors. By early 2025, the company projected a 27.6% drop in first-quarter revenue, primarily due to weakened demand in industrial and automotive markets.

This downturn has pushed back STMicroelectronics’ goal of achieving $20 billion in annual revenue and a 30%+ operating margin from its original 2027 target to 2030. CEO Jean-Marc Chery attributed the delay to government interventions that have disrupted market balance, leading to overcapacity and ongoing supply chain challenges.

Latest Trends

Structural electronics is undergoing a significant transformation, driven by advancements in materials science and manufacturing technologies. One notable trend is the integration of electronic functionalities directly into structural components, enabling the creation of “smart” structures that can monitor their own health and performance.

This approach not only reduces weight and complexity but also enhances the durability and functionality of the final product. For instance, the use of 3D printing in structural electronics allows for the fabrication of complex geometries with embedded sensors and circuits, leading to more efficient and responsive systems.

Another emerging trend is the development of flexible and stretchable electronics, which can conform to various shapes and surfaces. This flexibility opens up new applications in wearable technology, biomedical devices, and soft robotics.

The integration of these electronics into structural components enables the creation of devices that are not only functional but also comfortable and adaptable to different environments. As research progresses, the combination of structural integrity with electronic functionality is expected to lead to innovative products that were previously unattainable.

Business Benefits

The adoption of structural electronics offers several business advantages, particularly in industries where weight reduction and space optimization are critical. By embedding electronic components directly into structural elements, manufacturers can eliminate the need for separate housings and connectors, leading to lighter and more compact products.

Moreover, structural electronics enhance product reliability by reducing the number of interconnections and potential points of failure. This increased reliability translates to longer product lifespans and reduced maintenance costs, providing a competitive edge in markets where durability is paramount.

Additionally, the design flexibility afforded by structural electronics allows for greater innovation in product aesthetics and functionality, enabling companies to differentiate their offerings and meet evolving consumer demands.

Regional Analysis

Asia Pacific is emerging as a pivotal region in the structural electronics landscape, driven by its robust electronics manufacturing ecosystem and rapid technological advancements. Countries like China, Japan, and South Korea are at the forefront, leveraging their established semiconductor industries to integrate structural electronics into various applications, including automotive and consumer electronics.

Europe’s structural electronics market is characterized by a strong emphasis on sustainability and innovation. The European Union’s commitment to green technologies and energy efficiency is propelling the integration of structural electronics in sectors such as automotive, aerospace, and renewable energy.

Latin America’s structural electronics market is gaining momentum, supported by the region’s growing consumer electronics sector and increasing digitalization. Countries like Brazil and Mexico are witnessing a surge in demand for smart devices, wearables, and IoT applications, creating opportunities for structural electronics integration.

The Middle East and Africa region is gradually embracing structural electronics, driven by investments in infrastructure, smart city projects, and renewable energy. Countries like the United Arab Emirates and Saudi Arabia are focusing on technological innovation and diversification of their economies, leading to increased adoption of advanced electronics in construction, transportation, and energy sectors.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

TactoTek Oy continues to lead the structural electronics market with its In-Mold Structural Electronics (IMSE®) technology. In November 2024, the company raised $60 million to expand its reach in the automotive and consumer electronics sectors. By December 2024, TactoTek entered a strategic partnership with Sundberg-Ferar to enhance design innovation.

Canatu Oy has strengthened its competitive edge through its Carbon Age initiative and CNT sensor production. In March 2025, Canatu launched the Carbon Age program to innovate semiconductor technologies using carbon nanotubes.

By May 2025, the company began mass production of sensors for defense applications, focusing on reliability in extreme environments. These efforts not only push material science boundaries but also highlight Canatu’s strategy to offer tailored, high-performance solutions for automotive, industrial, and defense electronics.

Neotech AMT GmbH is expanding its global influence in 3D printed electronics. In early 2025, the company announced a strategic partnership with Advanced Printed Electronic Solutions (APES) to enter the North American market. This move enhances Neotech’s presence in smart manufacturing.

Top Key Players in the Market

- TactoTek Oy

- Canatu Oy

- Neotech AMT GmbH

- Pulse Electronics (a Yageo Company)

- T-ink Inc.

- Molex LLC

- Panasonic Corporation

- Odyssian Technology LLC

- Optomec Inc.

- Aconity3D GmbH

- Others

Recent Developments

- In November 2024, TactoTek secured $60 million in funding led by Nidoco AB. This investment aims to accelerate the adoption of its In-Mold Structural Electronics (IMSE®) technology across automotive and consumer electronics sectors.

- In early 2025, Neotech AMT expanded its presence in North America through a partnership with Advanced Printed Electronic Solutions (APES). This collaboration aims to support the growth of 3D printed electronics by combining Neotech’s 3D printing technologies with APES’s market reach.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 98.5 Bn |

| Forecast Revenue (2034) | USD 267.3 Bn |

| CAGR (2025-2034) | 10.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Embedded Sensors, Conductive Inks, Flexible Displays, Energy Harvesting, Others), By Material (Polymers, Composites, Metals), By Application (Automotive, Aerospace & Defense, Consumer Electronics, Healthcare, Building & Architecture, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | TactoTek Oy, Canatu Oy, Neotech AMT GmbH, Pulse Electronics (a Yageo Company), T-ink Inc., Molex LLC, Panasonic Corporation, Odyssian Technology LLC, Optomec Inc., Aconity3D GmbH, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |