Global Storm Resilience Solutions Market Size, Share, Growth Analysis By Solution Type (Structural Solutions, Non-Structural Solutions, Emergency Response Systems, Risk Assessment & Management, Others), By Application (Residential, Commercial, Industrial, Infrastructure, Others), By Technology (Smart Sensors, Weather Forecasting Systems, Flood Barriers, Backup Power Systems, Others), By End-User (Government & Municipalities, Utilities, Private Sector, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 181701

- Number of Pages: 300

- Format:

-

keyboard_arrow_up

Quick Navigation

- Report Overview

- Core Key Insights

- Future Predictions

- Market Growth

- Key Market Segments

- Research-Based Segments

- By Solution Type

- By Application

- By Technology

- By End-User

- Regional Analysis

- US Market Size

- Driving Factors

- Restraint Factors

- Growth Opportunities

- Trending Factors

- Competitive Analysis

- Recent Developments

- Report Scope

Report Overview

The Storm Resilience Solutions Market is gaining strong traction as governments, utilities, and businesses increasingly focus on protecting infrastructure and communities from extreme weather events. Storm resilience solutions include technologies and systems designed to reduce the impact of hurricanes, floods, heavy rainfall, and windstorms.

These solutions range from advanced forecasting tools and early warning systems to resilient infrastructure design, flood protection systems, and grid hardening technologies. As climate patterns continue to shift and the frequency of severe weather events increases, the need for reliable and scalable resilience solutions has become a priority across both public and private sectors.

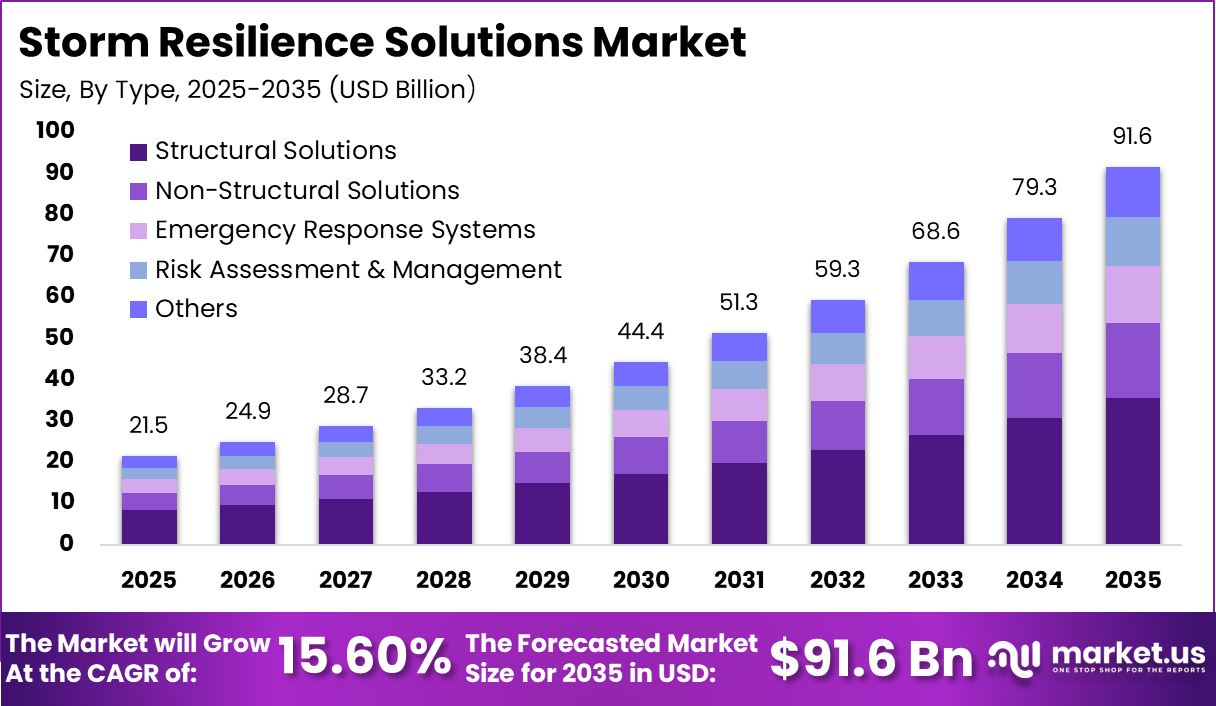

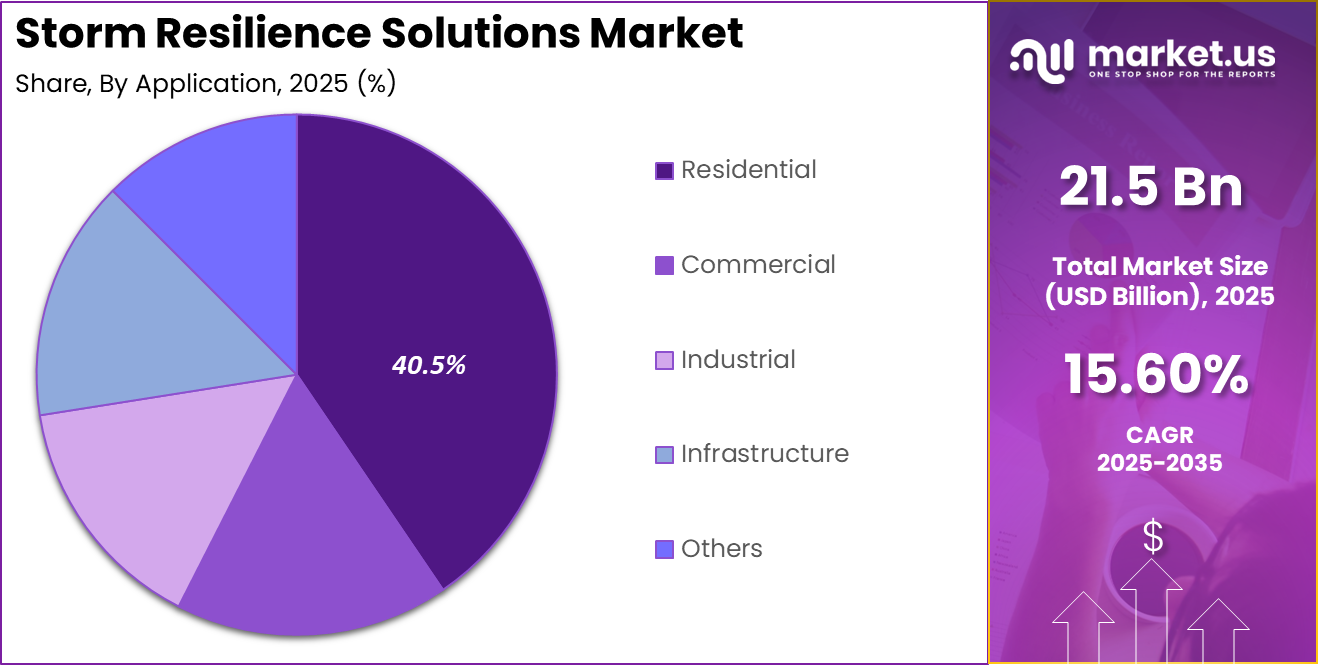

In 2025, the global Storm Resilience Solutions Market is valued at approximately USD 21.5 billion. The market is projected to grow at a compound annual growth rate of 15.60%, reaching an estimated value of around USD 91.6 billion by 2035. This strong growth reflects increasing investments in disaster preparedness, infrastructure protection, and climate adaptation strategies across regions.

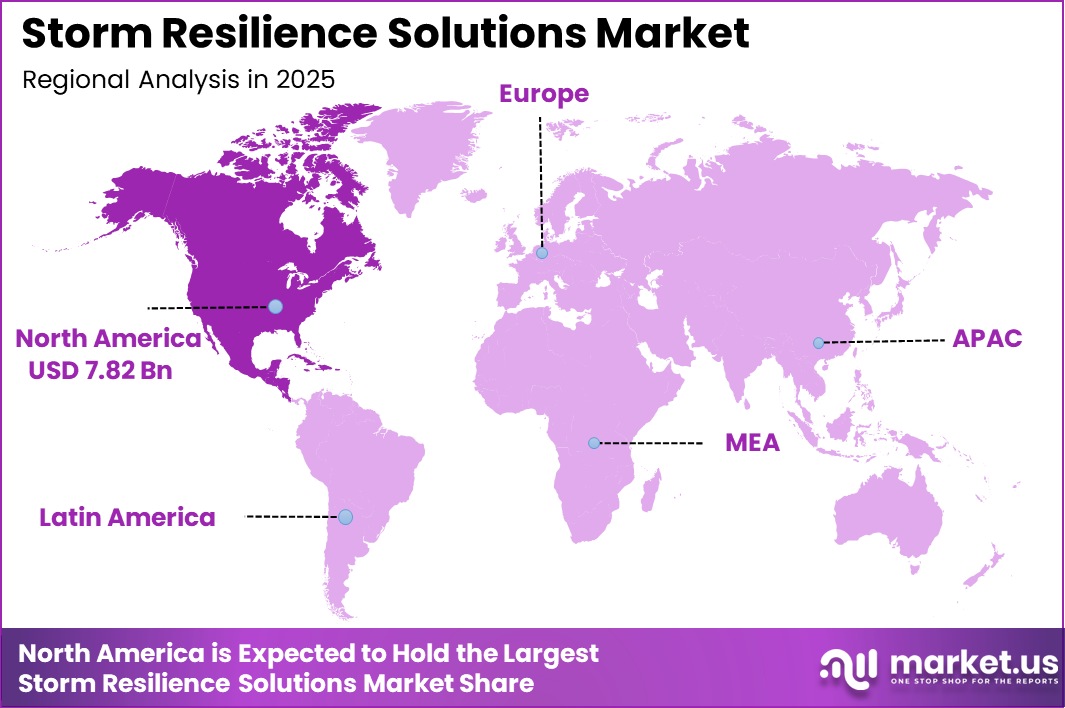

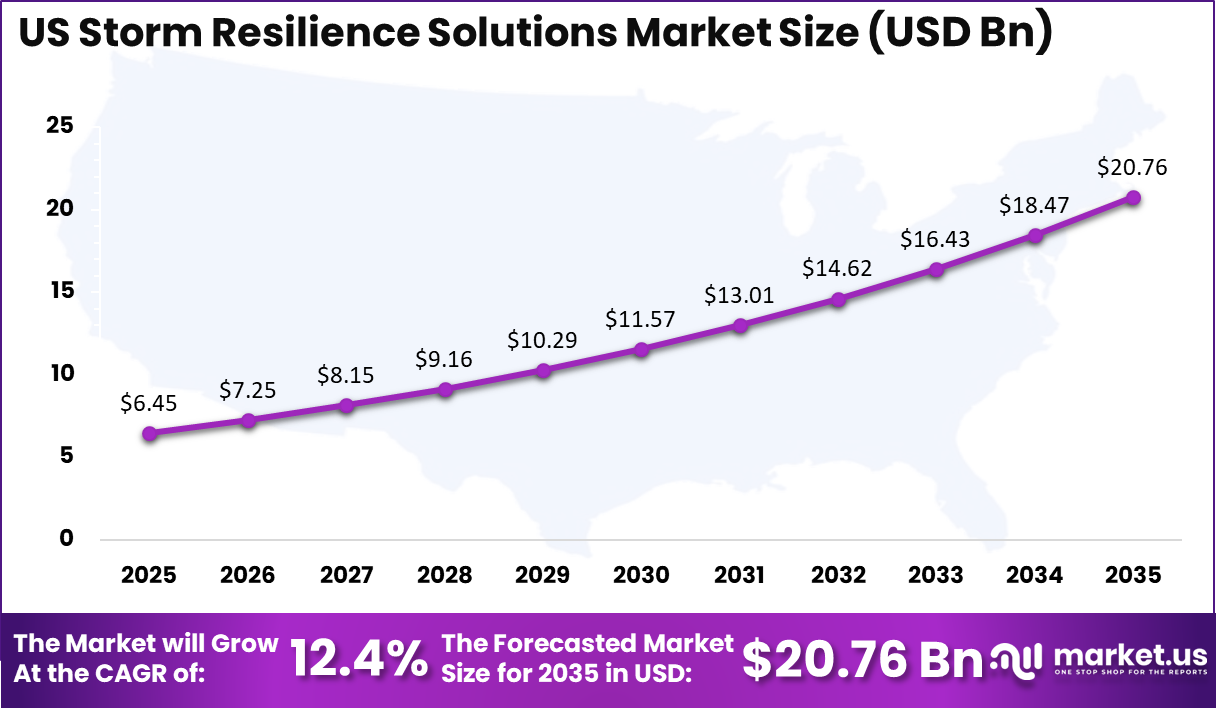

North America leads the market with a 36.4% share, generating about USD 7.82 billion in revenue in 2025. The United States accounts for approximately USD 6.45 billion of this value, driven by high exposure to severe storms and strong investment in resilience planning. The US market is expected to reach nearly USD 20.76 billion by 2035, growing at a CAGR of 12.4%, supported by ongoing infrastructure upgrades and climate resilience initiatives.

The Storm Resilience Solutions Market is gaining strong traction as governments, utilities, and businesses increasingly focus on protecting infrastructure and communities from extreme weather events. Storm resilience solutions include technologies and systems designed to reduce the impact of hurricanes, floods, heavy rainfall, and windstorms.

These solutions range from advanced forecasting tools and early warning systems to resilient infrastructure design, flood protection systems, and grid hardening technologies. As climate patterns continue to shift and the frequency of severe weather events increases, the need for reliable and scalable resilience solutions has become a priority across both public and private sectors.

In 2025, the global Storm Resilience Solutions Market is valued at approximately USD 21.5 billion. The market is projected to grow at a compound annual growth rate of 15.60%, reaching an estimated value of around USD 91.6 billion by 2035. This strong growth reflects increasing investments in disaster preparedness, infrastructure protection, and climate adaptation strategies across regions.

North America leads the market with a 36.4% share, generating about USD 7.82 billion in revenue in 2025. The United States accounts for approximately USD 6.45 billion of this value, driven by high exposure to severe storms and strong investment in resilience planning. The US market is expected to reach nearly USD 20.76 billion by 2035, growing at a CAGR of 12.4%, supported by ongoing infrastructure upgrades and climate resilience initiatives.

Core Key Insights

- The Storm Resilience Solutions Market reached a value of USD 21.5 billion in 2025, reflecting increasing investments in climate adaptation and infrastructure protection.

- The market is projected to grow at a CAGR of 15.60% during the forecast period.

- By 2035, the global market value is expected to reach USD 91.6 billion.

- North America accounted for the largest regional share of 36.4% in 2025.

- The North American market size reached approximately USD 7.82 billion in 2025.

- The United States generated around USD 6.45 billion in revenue in 2025.

- The US market is projected to reach USD 20.76 billion by 2035.

- The United States market is expected to grow at a CAGR of 12.4%.

- By solution type, structural solutions held a leading share of 38.7%.

- By application, commercial use accounted for 40.5% of the market demand.

- By technology, smart sensors represented 36.4% of the market.

- By end user, government and municipalities dominated with a share of 48.8%.

Future Predictions

The future of the Storm Resilience Solutions Market is expected to be strongly influenced by increasing climate risks and rising investments in infrastructure protection. As extreme weather events become more frequent, governments and organizations are likely to allocate a larger portion of their budgets toward resilience planning and disaster mitigation.

It is estimated that global spending on climate adaptation and resilience could exceed hundreds of billions of dollars annually over the next decade, creating significant opportunities for solution providers. Investments in flood protection systems, stormwater management, and resilient urban infrastructure are expected to grow steadily as cities expand and face higher exposure to climate related risks.

Technology will play a key role in shaping future developments in this market. Advanced solutions such as smart sensors, predictive analytics, and early warning systems are expected to see strong adoption. It is anticipated that more than half of urban areas could implement some form of real-time monitoring system to track weather conditions and infrastructure performance.

These technologies can help reduce response time and improve disaster preparedness. In addition, the integration of artificial intelligence in weather forecasting and risk assessment is expected to improve accuracy and decision-making. As awareness of climate resilience continues to rise, demand for comprehensive storm protection solutions is expected to grow across both developed and developing regions.

Market Growth

The Storm Resilience Solutions Market is experiencing strong growth as the frequency and intensity of extreme weather events continue to rise globally. Governments, utilities, and private organizations are increasingly prioritizing investments in infrastructure protection and disaster preparedness to reduce long term economic losses.

Storm-related damages have placed significant pressure on public budgets and insurance systems, encouraging the adoption of solutions such as flood barriers, stormwater management systems, and reinforced infrastructure. These measures help minimize disruption to critical services and protect communities from severe weather impacts.

Urbanization is another key factor supporting market growth. As cities expand, especially in coastal and flood-prone regions, the demand for resilient infrastructure continues to increase. Urban areas require advanced drainage systems, smart monitoring tools, and adaptive construction techniques to manage storm risks effectively. Businesses operating in sectors such as energy, transportation, and real estate are also investing in resilience solutions to safeguard assets and maintain operational continuity during extreme weather conditions.

In addition, technological advancements are accelerating market expansion. The use of smart sensors, data analytics, and real-time monitoring systems allows organizations to predict and respond to storms more effectively. As awareness of climate risks grows and investments in resilience increase, the market is expected to maintain steady growth in the coming years.

Key Market Segments

The Storm Resilience Solutions Market is segmented by solution type, application, technology, and end user, each reflecting how different sectors address the growing impact of extreme weather events. These segments highlight the increasing focus on infrastructure protection, real-time monitoring, and disaster preparedness across regions.

By solution type, structural solutions hold the largest share at 38.7%. This segment includes physical infrastructure such as flood barriers, storm surge protection systems, reinforced buildings, and drainage systems. These solutions are widely adopted because they provide direct protection against storm damage and help reduce long-term repair costs. Governments and organizations invest heavily in structural resilience to safeguard critical infrastructure and urban areas.

By application, commercial use accounts for 40.5% of the market. Businesses across sectors such as real estate, energy, transportation, and retail are investing in resilience solutions to protect assets and ensure business continuity during extreme weather events.

In terms of technology, smart sensors lead with 36.4%, as they enable real-time monitoring of weather conditions, water levels, and infrastructure performance. By end user, government and municipalities dominate with 48.8%, as public sector entities are primarily responsible for disaster management, infrastructure planning, and community protection initiatives.

Research-Based Segments

By Solution Type

- Structural Solutions

- Non-Structural Solutions

- Emergency Response Systems

- Risk Assessment & Management

- Others

By Application

- Residential

- Commercial

- Industrial

- Infrastructure

- Others

By Technology

- Smart Sensors

- Weather Forecasting Systems

- Flood Barriers

- Backup Power Systems

- Others

By End-User

- Government & Municipalities

- Utilities

- Private Sector

- Others

By Solution Type

The solution type segment of the Storm Resilience Solutions Market includes structural solutions, non-structural solutions, emergency response systems, risk assessment and management, and other supporting tools. Structural solutions hold the leading share at 38.7%. These solutions involve physical infrastructure designed to withstand or reduce the impact of storms, such as flood barriers, levees, reinforced buildings, drainage systems, and coastal protection structures.

Governments and urban planners prioritize these investments because they provide long-term protection against storm damage and help reduce recovery costs. Structural measures are especially critical in coastal cities and flood-prone regions where infrastructure is exposed to repeated weather events.

Non-structural solutions also play an important role in resilience planning. These include policies, zoning regulations, early warning systems, and disaster preparedness strategies that help reduce risk without requiring physical construction. Emergency response systems are essential for managing real-time situations, enabling faster evacuation, communication, and coordination during storms.

Risk assessment and management solutions focus on analyzing potential threats, forecasting storm impact, and planning mitigation strategies. Other solutions include integrated platforms that combine data monitoring, planning tools, and infrastructure management. Together, these approaches support a comprehensive resilience strategy that helps communities and organizations better prepare for and respond to extreme weather conditions.

By Application

The application segment of the Storm Resilience Solutions Market includes residential, commercial, industrial, infrastructure, and other sectors, with commercial applications holding the largest share at 40.5%. Businesses are increasingly investing in storm resilience solutions to protect physical assets, reduce operational disruptions, and ensure business continuity during extreme weather events.

Commercial facilities such as office buildings, shopping centers, data centers, and logistics hubs are highly exposed to storm-related risks. Implementing solutions like flood protection systems, backup power infrastructure, and real-time monitoring helps businesses minimize damage and maintain operations.

Residential applications also represent a significant portion of the market, particularly in regions prone to hurricanes, floods, and heavy rainfall. Homeowners are adopting solutions such as storm-resistant construction, drainage improvements, and protective barriers to safeguard properties. Industrial applications focus on protecting manufacturing plants, warehouses, and energy facilities, where disruptions can lead to significant financial losses.

Infrastructure applications include transportation networks, utilities, and public systems that require large-scale resilience planning to ensure continuous operation during storms. Other applications include specialized sectors that require customized resilience strategies. As climate risks increase, adoption across all application segments is expected to grow steadily.

By Technology

The technology segment of the Storm Resilience Solutions Market includes smart sensors, weather forecasting systems, flood barriers, backup power systems, and other supporting technologies. Among these, smart sensors hold the leading share at 36.4%.

These sensors are widely used for real-time monitoring of environmental conditions such as rainfall levels, wind speed, water flow, and infrastructure stress. Smart sensors provide continuous data that helps authorities and organizations detect potential risks early and take timely action. This makes them highly valuable in disaster preparedness and response planning.

Weather forecasting systems also play a critical role by providing accurate predictions of storm paths, intensity, and timing. These systems support early warning mechanisms and help communities prepare in advance. Flood barriers are important physical solutions that prevent water intrusion in flood-prone areas, protecting urban infrastructure and residential zones.

Backup power systems ensure continuity of critical operations during storms by maintaining an electricity supply when primary power sources fail. Other technologies include integrated monitoring platforms and communication systems that support coordinated disaster response. Together, these technologies form a comprehensive ecosystem that enhances storm resilience and helps reduce the impact of extreme weather events.

By End-User

The end user segment of the Storm Resilience Solutions Market includes government and municipalities, utilities, the private sector, and other users. Government and municipalities hold the largest share at 48.8%. Public sector bodies play a central role in planning, funding, and implementing storm resilience strategies.

They are responsible for protecting communities, managing public infrastructure, and coordinating disaster response. Investments in flood control systems, stormwater management, early warning systems, and resilient urban planning are largely driven by government initiatives. Municipal authorities also focus on improving emergency preparedness and reducing long-term economic losses caused by extreme weather events.

Utilities represent another important segment, as they are responsible for maintaining essential services such as electricity, water supply, and gas distribution. These organizations invest in grid hardening, backup systems, and monitoring technologies to ensure service continuity during storms.

The private sector is also increasingly adopting resilience solutions to protect business assets and maintain operations during adverse weather conditions. Industries such as real estate, transportation, and energy invest in protective infrastructure and risk management systems. Other users include non-profit organizations and research institutions that support disaster management efforts and resilience planning.

Regional Analysis

North America holds a dominant position in the Storm Resilience Solutions Market, accounting for approximately 36.4% of the global share. The regional market reached around USD 7.82 billion in 2025, reflecting strong investments in infrastructure protection and disaster preparedness.

The region is highly exposed to extreme weather events such as hurricanes, floods, and severe storms, which has increased the need for advanced resilience solutions. Governments and local authorities across North America are prioritizing long-term strategies to reduce the impact of climate-related risks on communities and critical infrastructure.

The presence of advanced technology providers and well-established infrastructure systems supports market growth in the region. Organizations are adopting solutions such as smart monitoring systems, flood protection infrastructure, and early warning technologies to improve response times and reduce damage. Sectors such as energy, transportation, and urban development are investing heavily in resilience measures to ensure continuity of operations during extreme weather conditions.

In addition, strong regulatory frameworks and funding programs for climate adaptation are encouraging the adoption of storm resilience solutions. Public and private sector collaboration is also increasing, helping accelerate the implementation of large-scale projects. As climate risks continue to rise, North America is expected to remain a key market for storm resilience solutions.

US Market Size

The United States Storm Resilience Solutions Market generated approximately USD 6.45 billion in revenue and continues to show strong growth as the country faces increasing exposure to extreme weather events. Hurricanes, floods, and severe storms frequently impact coastal and inland regions, creating significant economic and infrastructure risks.

As a result, federal, state, and local governments are investing in resilience solutions such as flood control systems, stormwater management infrastructure, and early warning technologies. These investments aim to reduce long term damage, protect communities, and ensure continuity of critical services.

The market is projected to reach around USD 20.76 billion by 2035, growing at a compound annual growth rate of 12.4%. This growth is supported by ongoing infrastructure modernization programs and increased focus on climate adaptation strategies. Utilities and private sector organizations are also investing in resilience solutions to protect energy systems, transportation networks, and commercial assets from storm-related disruptions.

In addition, advancements in technology are playing a key role in market expansion. The use of smart sensors, data analytics, and predictive modeling helps improve disaster preparedness and response efficiency. As awareness of climate risks continues to rise, the adoption of storm resilience solutions across the United States is expected to increase steadily over the forecast period.

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driving Factors

The Storm Resilience Solutions Market is driven by the increasing frequency and severity of extreme weather events across the globe. Hurricanes, floods, and heavy rainfall are causing significant damage to infrastructure, homes, and businesses, which is encouraging governments and organizations to invest in long-term resilience strategies.

Protecting critical infrastructure such as transportation networks, power systems, and urban facilities has become a priority to reduce economic losses and ensure public safety. As climate risks continue to rise, there is a growing need for solutions that can prevent or minimize damage before disasters occur.

Another important driver is the increasing focus on climate adaptation and disaster preparedness. Governments are allocating higher budgets toward flood control systems, early warning technologies, and resilient infrastructure projects.

Urbanization is also contributing to market growth, as expanding cities require stronger protection against storm-related risks. Businesses are adopting resilience solutions to maintain operational continuity and protect assets. The integration of advanced technologies such as smart sensors and predictive analytics further supports adoption by enabling real-time monitoring and faster response to potential threats.

Restraint Factors

One of the key restraints in the Storm Resilience Solutions Market is the high cost associated with implementing large-scale resilience infrastructure. Structural solutions such as flood barriers, stormwater systems, and reinforced construction require significant capital investment.

Many developing regions and smaller municipalities may face budget limitations, which can delay or restrict the adoption of these solutions. In some cases, funding challenges lead to prioritization of immediate recovery efforts rather than long-term resilience planning.

Another restraint is the complexity involved in planning and executing resilience projects. These solutions often require coordination between multiple stakeholders, including government agencies, private contractors, and local communities.

Regulatory approvals, environmental assessments, and land use considerations can extend project timelines. In addition, there is often uncertainty in predicting the exact impact of future climate events, which makes it difficult to design solutions that fully address long term risks. These challenges can slow decision-making and limit the pace of market adoption in certain regions.

Growth Opportunities

The Storm Resilience Solutions Market offers strong growth opportunities as global awareness of climate risks continues to increase. Governments and international organizations are expanding investments in disaster risk reduction and infrastructure protection.

Many countries are developing national resilience strategies that include upgrading urban drainage systems, strengthening coastal defenses, and implementing early warning systems. These initiatives create significant opportunities for solution providers offering advanced technologies and infrastructure solutions.

Another major opportunity lies in the integration of digital technologies with traditional resilience systems. Smart sensors, data analytics, and real-time monitoring platforms allow organizations to detect risks early and respond more effectively. The use of predictive modeling can help authorities plan mitigation strategies based on weather patterns and historical data.

In addition, public-private partnerships are becoming more common, enabling collaboration between governments and private companies to develop large-scale resilience projects. As cities continue to expand and climate challenges intensify, demand for innovative and scalable resilience solutions is expected to grow across both developed and emerging markets.

Trending Factors

Several trends are shaping the Storm Resilience Solutions Market as technology and environmental awareness continue to evolve. One major trend is the increasing use of smart and connected systems for monitoring weather conditions and infrastructure performance.

Real-time data collection through sensors and digital platforms helps authorities make informed decisions and respond quickly to potential threats. These technologies are becoming an essential part of modern resilience strategies.

Another important trend is the shift toward integrated and sustainable resilience solutions. Instead of relying only on physical infrastructure, many projects now combine structural measures with environmental approaches such as green infrastructure and natural flood management systems. This approach helps reduce environmental impact while improving long-term resilience.

There is also growing interest in decentralized solutions such as localized energy backup systems and community-level preparedness programs. As organizations focus on building adaptive and sustainable systems, the market is expected to see continued innovation and adoption of advanced resilience technologies.

Competitive Analysis

The competitive landscape of the Storm Resilience Solutions Market is diverse, with a mix of engineering firms, technology providers, insurance risk analytics companies, and infrastructure consultants competing to deliver comprehensive resilience solutions.

Companies such as Siemens, Schneider Electric, IBM, AECOM, and Arup focus on integrating digital technologies like smart sensors, data analytics, and infrastructure monitoring into resilience planning. These firms provide end-to-end solutions that combine physical infrastructure with digital intelligence to improve disaster preparedness and response.

Engineering and consulting firms such as Jacobs and Arcadis are actively involved in large-scale resilience projects. Jacobs alone is working on more than 1,000 global resilience projects focused on infrastructure protection and climate adaptation. These firms support governments and cities in designing flood control systems, coastal protection, and resilient urban infrastructure.

Technology-driven players are also gaining importance. Companies like ZestyAI use machine learning models approved in over 35 US states to assess property-level storm risks and improve insurance decision-making. New entrants such as Resilitix AI are introducing real-time digital twin solutions that support emergency response for events affecting more than 2 million people.

Competition is driven by innovation, data accuracy, and the ability to combine infrastructure, analytics, and real-time monitoring into scalable resilience solutions.

Top Key Players in the Market

- Schneider Electric

- Siemens AG

- ABB Ltd.

- Eaton Corporation

- Honeywell International Inc.

- Johnson Controls International plc

- General Electric Company

- IBM Corporation

- AECOM

- Black & Veatch

- WSP Global Inc.

- Tetra Tech, Inc.

- Jacobs Engineering Group Inc.

- Leidos Holdings, Inc.

- S&C Electric Company

- Xylem Inc.

- Trimble Inc.

- ResilientGrid, Inc.

- Mott MacDonald

- Veolia Environnement S.A.

- Others

Recent Developments

- In 2025, advanced flood management systems such as AI-driven decision support platforms were introduced, enabling real-time forecasting and automated flood control operations to improve response efficiency.

- In 2025, cities began adopting integrated resilience platforms combining smart sensors, digital twins, and deep learning models to monitor flood risks and support urban planning decisions.

- In 2024, AI-powered digital twin solutions were deployed during hurricane events, helping emergency teams manage disruptions affecting over 2 million people through real-time situational awareness.

Report Scope

Report Features Description Market Value (2025) USD 21.5 Billion Forecast Revenue (2035) USD 91.6 Billion CAGR(2025-2035) 15.60% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics, and Emerging Trends Segments Covered By Solution Type (Structural Solutions, Non-Structural Solutions, Emergency Response Systems, Risk Assessment & Management, Others), By Application (Residential, Commercial, Industrial, Infrastructure, Others), By Technology (Smart Sensors, Weather Forecasting Systems, Flood Barriers, Backup Power Systems, Others), By End-User (Government & Municipalities, Utilities, Private Sector, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Schneider Electric, Siemens AG, ABB Ltd., Eaton Corporation, Honeywell International Inc., Johnson Controls International plc, General Electric Company, IBM Corporation, AECOM, Black & Veatch, WSP Global Inc., Tetra Tech, Inc., Jacobs Engineering Group Inc., Leidos Holdings, Inc., S&C Electric Company, Xylem Inc., Trimble Inc., ResilientGrid, Inc., Mott MacDonald, Veolia Environnement S.A., Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Storm Resilience Solutions MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Storm Resilience Solutions MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Schneider Electric

- Siemens AG

- ABB Ltd.

- Eaton Corporation

- Honeywell International Inc.

- Johnson Controls International plc

- General Electric Company

- IBM Corporation

- AECOM

- Black & Veatch

- WSP Global Inc.

- Tetra Tech, Inc.

- Jacobs Engineering Group Inc.

- Leidos Holdings, Inc.

- S&C Electric Company

- Xylem Inc.

- Trimble Inc.

- ResilientGrid, Inc.

- Mott MacDonald

- Veolia Environnement S.A.

- Others

Our Clients

- 181701

- Mar 2026