Global Specialty Coatings Market Size, Share, And Industry Analysis Report By Coating Type (Anti-Corrosion Coatings, Fire-Resistant Coatings, Waterproof Coatings, Abrasion-Resistant Coatings, Others), By Technology (Solvent-Based Coatings, Water-Based Coatings, High-Solid Coatings, Nano Coatings), By End User (Automotive, Industrial, Marine, Construction, Electronics), By Distribution Channel (Direct Sales, Retail Sales, Online Sales), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 179995

- Number of Pages: 257

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

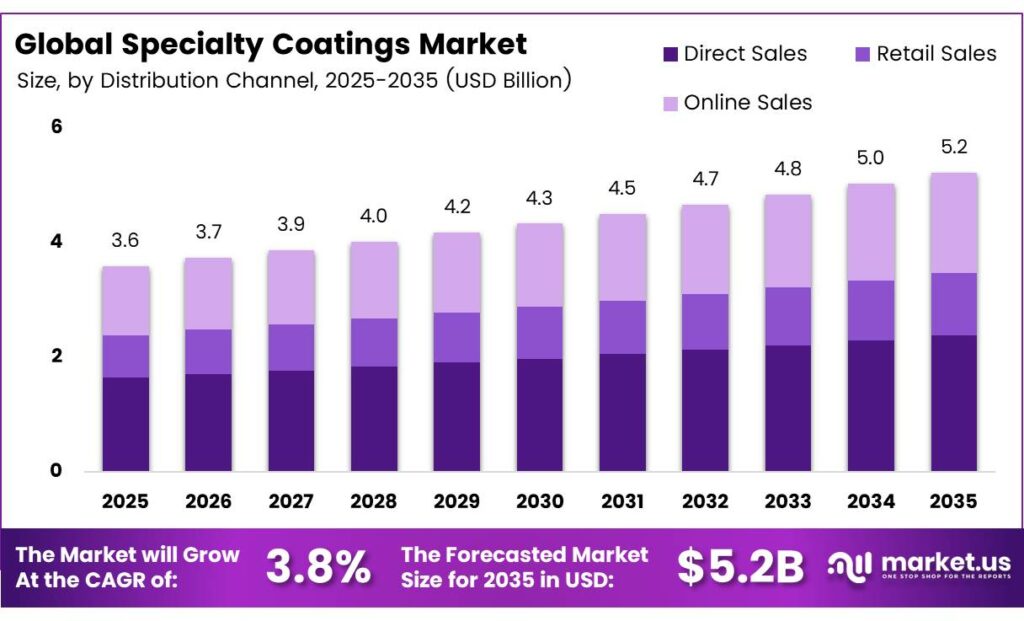

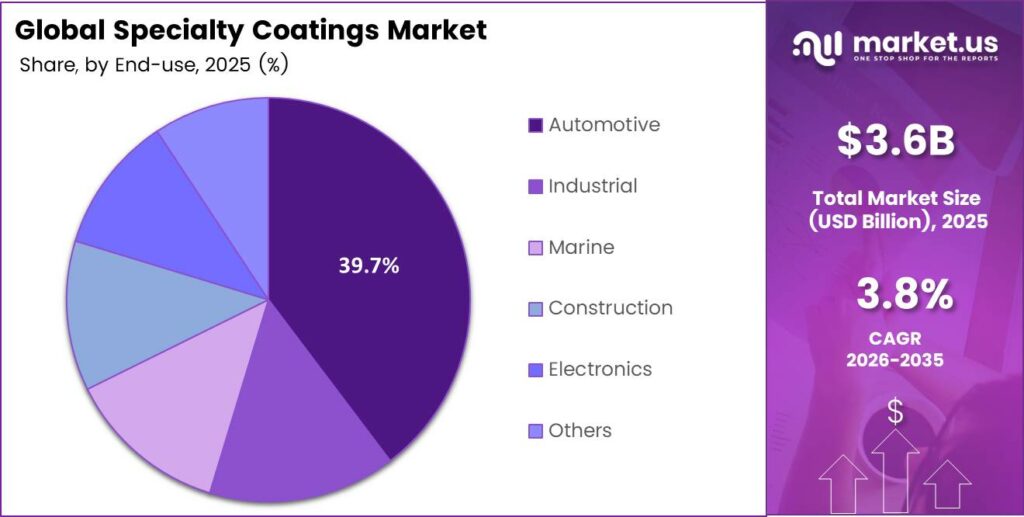

The Global Specialty Coatings Market size is expected to be worth around USD 5.2 billion by 2035 from USD 3.6 billion in 2025, growing at a CAGR of 3.8% during the forecast period 2026 to 2035.

Specialty coatings refer to advanced surface treatment solutions engineered for specific performance needs. These coatings deliver properties such as corrosion resistance, thermal protection, fire retardancy, and UV shielding. Industries including automotive, construction, electronics, and marine rely on these solutions to extend the service life of critical assets.

The specialty coatings sector covers a broad range of technologies, from solvent-based and water-based systems to powder and nano coatings. Manufacturers develop these formulations to meet stringent international standards for chemical resistance, adhesion, and environmental compliance. Consequently, demand continues to rise across both developed and emerging economies.

- PPG Industries recorded coatings sales of $18.17 billion in 2023, supported by over 35,800 employees operating across more than 70 countries, making it one of the largest specialty and performance coatings producers by revenue globally. This scale reflects the significant commercial opportunity that specialty coatings represent for leading players.

Government infrastructure programs worldwide accelerate the consumption of high-performance anti-corrosion and fire-resistant coatings. Investments in bridges, pipelines, and public buildings create sustained order flows for specialty coating producers. Moreover, regulations on volatile organic compound emissions push formulators toward cleaner, higher-value coating technologies.

- Sherwin-Williams generated $23.1 billion in net sales over the trailing year ending 31 December 2024. Axalta Coating Systems reported Adjusted EBITDA of $1,116 million in 2024, a 17% increase from $951 million in 2023, underscoring strong profitability in specialty refinish and industrial coatings portfolios.

Electric vehicle production represents a key growth catalyst for the specialty coatings industry. Automakers require specialized thermal management and battery insulation coatings to meet safety and efficiency targets. Additionally, the rise of renewable energy infrastructure, including wind turbines and solar panels, opens new application segments for protective and thermal-barrier coatings.

Key Takeaways

- The Global Specialty Coatings Market is valued at USD 3.6 billion in 2025 and is projected to reach USD 5.2 billion by 2035, at a CAGR of 3.8% during the forecast period 2026 to 2035.

- Anti-Corrosion Coatings dominate with a 37.4% market share in 2025.

- Solvent-Based Coatings lead with a 45.3% share among all technology segments.

- The Automotive segment holds the largest share at 39.7% of the total market.

- The Direct Sales account for 49.6% of total market revenue.

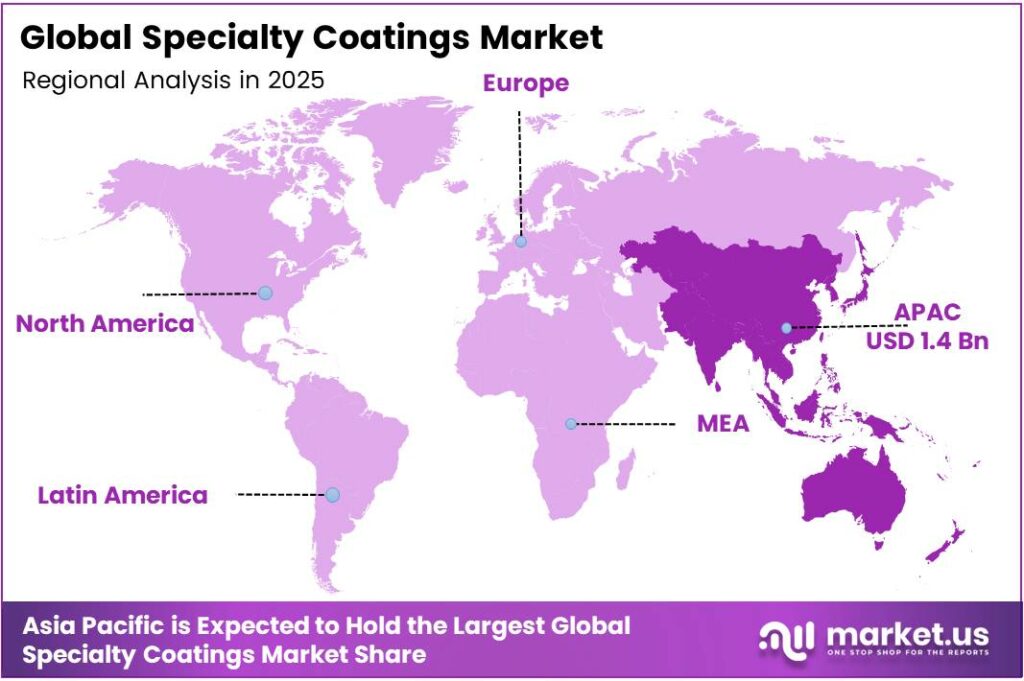

- Asia Pacific dominates the regional landscape with a 39.1% share, valued at USD 1.4 billion.

By Coating Type Analysis

Anti-Corrosion Coatings dominate with 37.4% due to extensive use in infrastructure and industrial asset protection.

In 2025, Anti-Corrosion Coatings held a dominant market position in the By Coating Type segment of the Specialty Coatings Market, with a 37.4% share. These coatings protect bridges, pipelines, and industrial structures from oxidation and chemical attack. Moreover, rising infrastructure investment globally continues to drive steady volume demand in this coating category.

Fire-Resistant Coatings serve construction, offshore, and public safety applications where passive fire protection is mandatory. Building codes in major economies require intumescent and cementitious fire-resistant systems for structural steel. Consequently, new commercial construction and retrofit programs generate consistent procurement activity for fire-resistant coating suppliers.

Waterproof Coatings protect rooftops, basements, tunnels, and marine surfaces from moisture ingress and water damage. Growing urbanization and aging infrastructure push municipalities to invest in waterproofing solutions for bridges and underground facilities. Additionally, Heat Resistant Coatings find application in exhaust systems, furnaces, and power generation equipment where temperatures exceed standard coating thresholds.

Anti-Graffiti Coatings enable rapid cleaning of public surfaces, reducing maintenance costs for transit authorities and municipalities. UV-Resistant Coatings prevent fading and degradation of outdoor surfaces exposed to prolonged solar radiation. Furthermore, Abrasion-Resistant Coatings extend the life of industrial floors, conveyor systems, and mining equipment operating under high mechanical stress.

By Technology Analysis

Solvent-Based Coatings dominate with 45.3% due to superior adhesion and performance in demanding industrial environments.

In 2025, Solvent-Based Coatings held a dominant market position in the By Technology segment of the Specialty Coatings Market, with a 45.3% share. These formulations deliver excellent substrate adhesion, fast drying, and chemical resistance in harsh conditions. However, regulatory pressure on VOC emissions increasingly prompts manufacturers to reformulate or transition to cleaner alternatives.

Water-Based Coatings gain traction across architectural, automotive, and consumer product applications as environmental regulations tighten globally. These systems offer lower toxicity and reduced VOC content compared to traditional solvent-based counterparts. Moreover, advancements in resin technology now allow water-based coatings to match solvent-based performance in many applications.

Powder Coatings deliver near-zero VOC emissions and high transfer efficiency in automated production environments. Industrial manufacturers favor this technology for furniture, appliances, and automotive parts. Additionally, High-Solid Coatings and Nano Coatings represent premium technology segments, with nano coatings offering self-cleaning and super-hydrophobic properties for electronics, aerospace, and marine substrates.

By End User Analysis

Automotive dominates with 39.7% due to high volume demand for protective, decorative, and functional coatings.

In 2025, the Automotive segment held a dominant market position in the By End User segment of the Specialty Coatings Market, with a 39.7% share. Vehicle manufacturers apply multiple coating layers for corrosion protection, scratch resistance, and thermal management. Furthermore, the rapid growth of electric vehicles drives demand for specialized battery insulation and thermal barrier coatings.

The Industrial end-user segment covers manufacturing plants, heavy machinery, and processing equipment requiring durable protective coatings. Industrial buyers prioritize chemical resistance, abrasion performance, and extended maintenance intervals. Consequently, industrial coatings producers invest in epoxy, polyurethane, and fluoropolymer formulations to meet diverse end-market specifications.

The Marine segment demands coatings that withstand saltwater immersion, biofouling, and UV exposure on hulls and offshore structures. Construction applications span commercial buildings, infrastructure, and residential projects requiring fire-resistant and waterproofing systems. Additionally, Electronics manufacturers adopt conformal, conductive, and antimicrobial coatings to protect circuit boards and components in demanding operating environments.

By Distribution Channel Analysis

Direct Sales dominate with 49.6% due to strong relationships between manufacturers and large industrial buyers.

In 2025, Direct Sales held a dominant market position in the By Distribution Channel segment of the Specialty Coatings Market, with a 49.6% share. Coating manufacturers sell directly to large original equipment manufacturers, construction contractors, and industrial operators through dedicated account management teams. This channel enables customized technical support, bulk pricing, and long-term supply agreements.

Retail Sales serve smaller contractors, maintenance teams, and professional applicators who purchase through distributor networks and specialty paint stores. Distributors add value through technical guidance, local inventory, and credit facilities. Moreover, retail channels allow manufacturers to reach fragmented customer bases that direct sales teams cannot efficiently serve.

Online Sales represent the fastest-growing distribution channel for specialty coatings, driven by digital procurement adoption among maintenance and facilities management buyers. E-commerce platforms offer product comparison, technical data sheets, and streamlined reordering for standard coating products. Additionally, manufacturers increasingly invest in digital storefronts and online configurators to capture smaller volume but high-margin specialty coating orders.

Key Market Segments

By Coating Type

- Anti-Corrosion Coatings

- Fire-Resistant Coatings

- Waterproof Coatings

- Heat-Resistant Coatings

- Anti-Graffiti Coatings

- UV-Resistant Coatings

- Abrasion-Resistant Coatings

- Others

By Technology

- Solvent-Based Coatings

- Water-Based Coatings

- Powder Coatings

- High-Solid Coatings

- Nano Coatings

- Others

By End User

- Automotive

- Industrial

- Marine

- Construction

- Electronics

- Others

By Distribution Channel

- Direct Sales

- Retail Sales

- Online Sales

Emerging Trends

Advanced Technologies and Sustainability Drive the Next Wave of Specialty Coatings Innovation

Powder and high-solids coating technologies accelerate adoption across industrial and automotive production lines as manufacturers pursue zero-VOC compliance. These systems deliver superior edge coverage and transfer efficiency compared to conventional liquid coatings. Moreover, regulatory mandates in North America and Europe increasingly make low-emission technologies the standard rather than the exception.

- Automated electrostatic and robotic deposition methods transform high-volume coating operations by improving uniformity and reducing material waste. Manufacturers that deploy robotic application systems achieve consistent film thickness and faster cycle times. The company reported net sales of $5,276 million in 2024, a 2% increase year-over-year, supported in part by investment in precision application technology and specialty refinish demand.

UV-curable coatings gain momentum in wood and plastic substrate applications due to instant cure times and energy savings. Multi-functional fire-resistant and thermal-barrier coatings emerge as a priority segment for renewable energy infrastructure and EV battery systems. Additionally, the development of self-healing and super-hydrophobic nano coatings signals the next frontier of performance differentiation in specialty surface protection.

Drivers

Electric Vehicle Growth and Infrastructure Investment Drive Strong Specialty Coatings Demand

Electric vehicle production surges globally, creating strong demand for specialized thermal management and battery insulation coatings. Automakers require coatings that withstand high operating temperatures while protecting battery modules from moisture and chemical exposure. Consequently, coating manufacturers invest in new formulations to serve this rapidly expanding automotive application segment.

- Global infrastructure mega-projects accelerate procurement of high-performance anti-corrosion coatings for bridges, pipelines, and marine structures. Governments in Asia, the Middle East, and North America commit substantial capital to infrastructure renewal and greenfield construction. RPM International’s Performance Coatings Group generated net sales of $2,397.3 million in fiscal 2024, with EBIT rising to $444.6 million, as industrial epoxy and corrosion-control coatings gained market share.

Nanotechnology integration reshapes specialty coating performance by enabling self-healing, super-hydrophobic, and enhanced barrier properties. Research laboratories and coating companies collaborate to translate nano-material discoveries into commercially viable product lines. Moreover, strict international standards for chemical resistance and durability prompt R&D investment, pushing manufacturers to develop advanced coating formulations that meet evolving industrial certifications.

Restraints

Raw Material Volatility and High Capital Costs Constrain Specialty Coatings Market Growth

Titanium dioxide and polyurethane resin prices experience persistent volatility due to supply chain disruptions, energy cost fluctuations, and geopolitical factors. Mid-sized specialty coating manufacturers absorb margin pressure when raw material costs spike unexpectedly. Consequently, smaller producers struggle to maintain competitive pricing without either reducing quality or accepting lower profitability.

Robotic application systems and industrial curing infrastructure require substantial upfront capital investment that many small and medium enterprises cannot afford. The cost of automated spray booths, UV curing chambers, and electrostatic deposition equipment creates high barriers to entry. Moreover, ongoing maintenance, calibration, and skilled operator training add to the total cost of ownership for advanced coating application systems.

Environmental compliance requirements generate additional cost burdens for specialty coating formulators operating across multiple regulatory jurisdictions. Companies must reformulate products to meet varying VOC limits in different markets, requiring parallel R&D and production investments. Therefore, regulatory complexity increases time-to-market for new coating products and diverts resources from core innovation activities.

Growth Factors

Smart Coatings, Bio-Based Solutions, and Aftermarket Programs Unlock New Market Opportunities

Smart responsive coatings enable real-time adaptation to temperature, humidity, and environmental stimuli, creating new value propositions for industrial and infrastructure buyers. Nippon Paint Group recorded consolidated revenue of 1,774,231 million yen in fiscal 2025, an 8.3% increase, supported by strong automotive and protective coatings performance across Asia, illustrating the commercial scale achievable through specialty segment expansion.

- Bio-based and recycled feedstock coatings align with circular economy mandates, gaining regulatory momentum in packaging, marine, and consumer goods sectors. Sherwin-Williams reported total net sales of $6.35 billion in Q3 2025, with protective and marine coatings achieving double-digit percentage sales growth, demonstrating the market strength of high-performance specialty segments.

Conductive and antimicrobial coatings attract growing investment from electronics and healthcare facility operators seeking functional surface performance. The boom in aerospace and heavy machinery aftermarket refurbishment programs creates additional volume for specialty repair and maintenance coatings. Consequently, coating manufacturers that target aftermarket channels unlock recurring revenue streams less sensitive to new equipment production cycles.

Regional Analysis

Asia Pacific Dominates the Specialty Coatings Market with a Market Share of 39.1%, Valued at USD 1.4 Billion

Asia Pacific leads the global Specialty Coatings Market, holding a 39.1% share valued at USD 1.4 billion in 2025. Rapid industrialization, massive automotive production, and aggressive infrastructure spending in China, India, Japan, and South Korea drive this regional dominance. Moreover, expanding electronics manufacturing hubs in the region generates consistent demand for conformal, thermal, and protective coating solutions.

North America maintains a strong position in the global specialty coatings landscape, supported by large-scale automotive, aerospace, and industrial manufacturing sectors. The United States drives significant demand for anti-corrosion, fire-resistant, and performance coatings across infrastructure and energy applications. Additionally, stringent environmental standards accelerate the adoption of water-based and powder coating technologies across the region.

Europe sustains steady specialty coatings consumption through its mature automotive, construction, and marine industries. Germany, France, and the United Kingdom represent the largest consuming markets within the region. Furthermore, the European Union’s circular economy and Green Deal policies push manufacturers and end-users toward sustainable, low-VOC coating formulations at an accelerating pace.

The Middle East and Africa region offers attractive growth potential driven by large-scale construction, oil and gas, and desalination infrastructure projects. GCC nations invest heavily in diversification mega-projects that require high-performance anti-corrosion and fire-resistant coatings. Additionally, expanding manufacturing sectors in South Africa and Saudi Arabia create new end-user bases for specialty surface protection solutions.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

PPG Industries ranks among the world’s foremost specialty and performance coatings producers, operating across more than 70 countries with a comprehensive portfolio spanning automotive, aerospace, marine, and industrial coatings. Asia Pacific, reflecting its broad global specialty coatings footprint.

AkzoNobel operates as a leading global paints and coatings company with a strategic emphasis on high-value performance coatings. Demonstrating deliberate portfolio concentration toward industrial, protective, and marine specialty segments. AkzoNobel agreed to sell its India decorative paint unit, signaling a continued pivot toward higher-margin specialty coatings businesses globally.

Sherwin-Williams delivers one of the most comprehensive specialty and architectural coatings portfolios in the world, supported by an extensive direct-to-consumer and professional applicator distribution network. The company generated consolidated results for the North America region. Its Performance Coatings Group continues to expand in packaging, auto-refinish, and protective marine coating niches.

Axalta Coating Systems specializes in liquid and powder coatings for the transportation and industrial sectors, serving collision repair shops, OEM vehicle manufacturers, and industrial equipment producers worldwide. The company reported 2024, driven by specialty refinish and mobility coatings demand alongside lower variable input costs.

Top Key Players in the Market

- PPG Industries

- AkzoNobel

- Sherwin-Williams

- Axalta Coating Systems

- RPM International Inc.

- BASF SE

Recent Developments

- In 2025, PPG unveiled its 2026 global automotive color trends in Shanghai under the theme Parallels, featuring three palettes (Authentic, Visionary, Expressive) and the Color of the Year Secret Safari (a mid-tone yellow-green with chameleon-like properties for body panels, wheels, and trim in automotive OEM coatings).

- In 2025, Sherwin-Williams completed the acquisition of BASF’s Brazilian architectural paints business (Suvinil). Suvinil integrates into the Consumer Brands Group; the deal is expected to add a low single-digit percentage to Q4 2025 consolidated sales. Suvinil is a business we have admired for decades… and immediately accelerates our ability to provide industry-leading solutions.

Report Scope

Report Features Description Market Value (2025) USD 3.6 Billion Forecast Revenue (2035) USD 5.2 Billion CAGR (2026-2035) 3.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Coating Type (Anti-Corrosion Coatings, Fire-Resistant Coatings, Waterproof Coatings, Heat Resistant Coatings, Anti-Graffiti Coatings, UV-Resistant Coatings, Abrasion-Resistant Coatings, Others), By Technology (Solvent-Based Coatings, Water-Based Coatings, Powder Coatings, High-Solid Coatings, Nano Coatings, Others), By End User (Automotive, Industrial, Marine, Construction, Electronics, Others), By Distribution Channel (Direct Sales, Retail Sales, Online Sales) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape PPG Industries, AkzoNobel, Sherwin-Williams, Axalta Coating Systems, RPM International Inc., BASF SE Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)  Specialty Coatings MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Specialty Coatings MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- PPG Industries

- AkzoNobel

- Sherwin-Williams

- Axalta Coating Systems

- RPM International Inc.

- BASF SE

Our Clients

- 179995

- March 2026