Global Space Division Multiplexing Devices Market Size, Share, Growth Analysis By Component (Optical Fiber, Multiplexers, Demultiplexers, Amplifiers, Others), By Application (Telecommunications, Data Centers, Enterprise Networks, Others), By Fiber Type (Multi-Core Fiber, Few-Mode Fiber, Others), By End-User (Telecom Operators, Cloud Service Providers, Enterprises, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 183419

- Number of Pages: 393

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

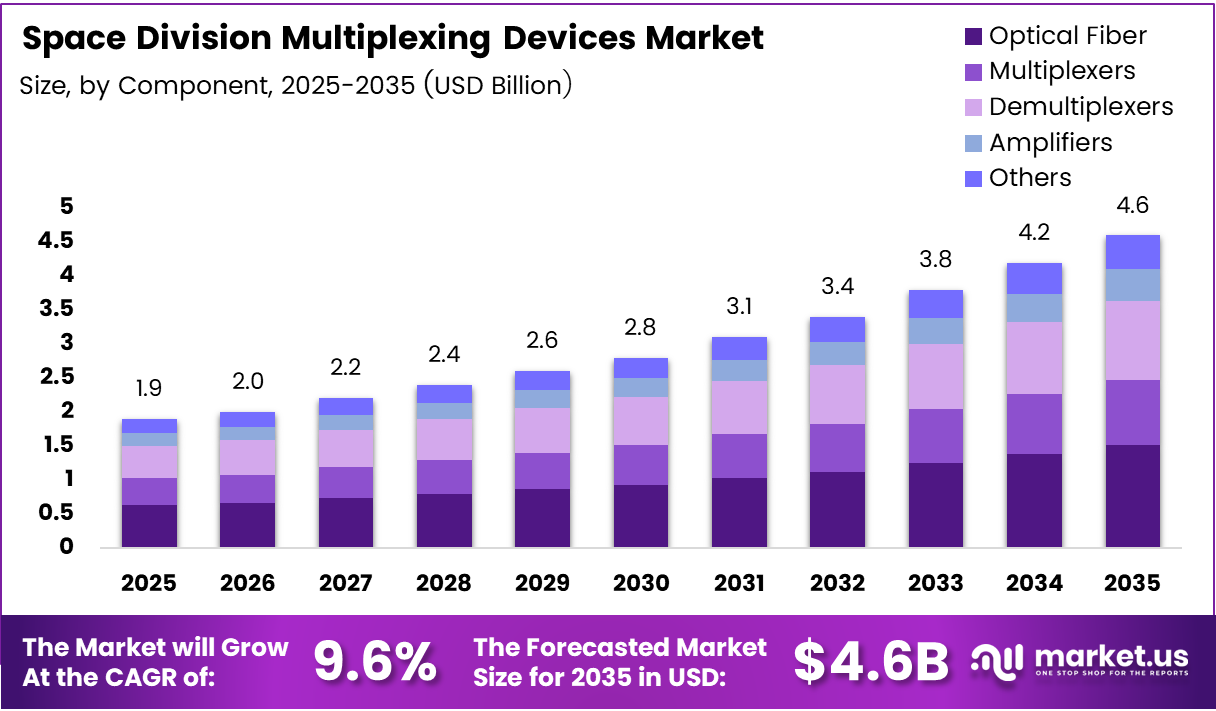

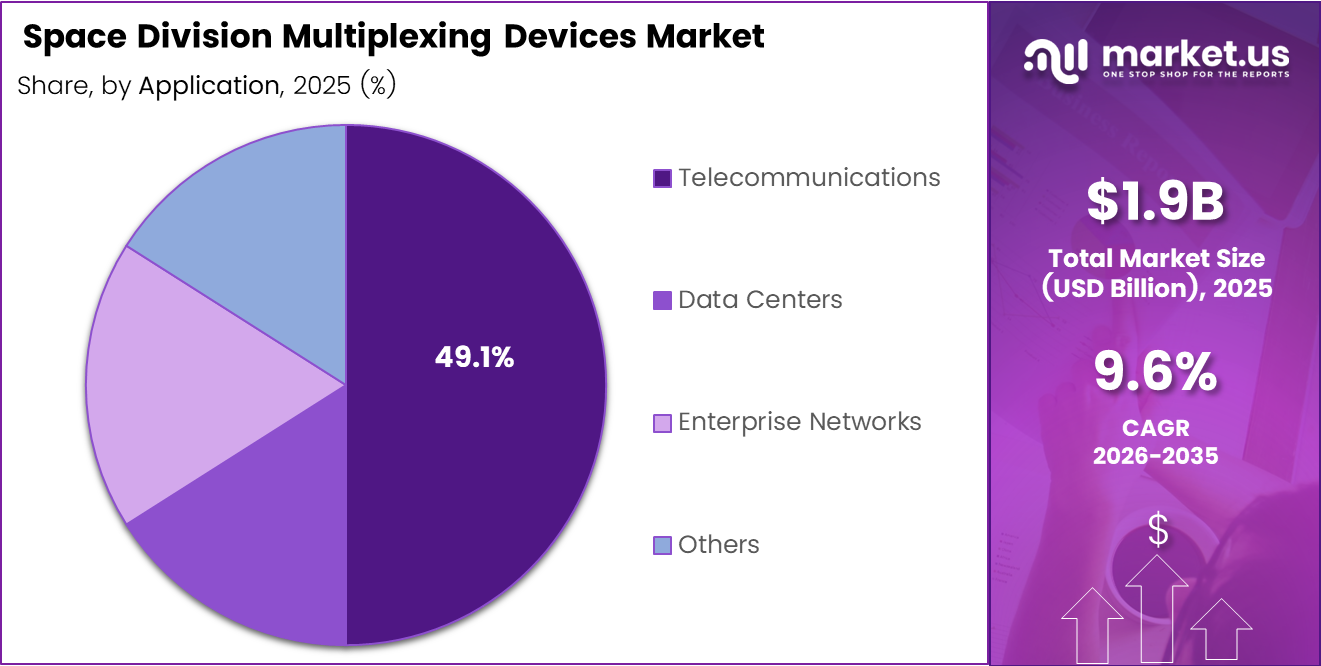

Global Space Division Multiplexing Devices Market size is expected to be worth around USD 4.6 Billion by 2035 from USD 1.9 Billion in 2025, growing at a CAGR of 9.6% during the forecast period 2026 to 2035.

Space division multiplexing (SDM) devices enable multiple data channels to travel simultaneously through a single optical fiber by using spatially separated paths. This architecture directly solves the capacity crunch facing telecom operators and data center operators — allowing more data through existing physical infrastructure without laying new cables.

The core technology relies on specialized optical components including multicore fibers, fan-in/fan-out devices, multiplexers, demultiplexers, and optical amplifiers. Each component plays a distinct role in routing, separating, and amplifying spatial channels. The precision engineering required at each stage creates high barriers to entry and strong pricing power for specialized manufacturers.

Hyperscale data centers from cloud service providers drive a structural shift in bandwidth requirements. Facilities processing AI workloads and real-time video streaming now require transmission architectures that conventional single-mode fiber cannot support. SDM devices fill this gap by multiplying fiber capacity without proportional increases in physical infrastructure cost.

Telecom operators investing in next-generation optical backhaul — especially for 5G densification — represent the largest near-term demand pool. Network planners prioritize spectral efficiency and scalability, two areas where SDM architectures outperform legacy DWDM systems at scale. This positions SDM device vendors as critical infrastructure suppliers rather than peripheral component makers.

Government-backed national broadband programs across North America, Europe, and Asia Pacific accelerate fiber deployment timelines. These programs mandate high-capacity last-mile and backbone infrastructure, which in turn creates procurement pipelines for advanced optical components. SDM vendors with certified product portfolios benefit directly from public tender processes.

In January 2024, HYC Company launched a compact 4-core fan-in/fan-out device achieving less than 0.5 dB average coupling loss with more than 45 dB crosstalk suppression — a performance benchmark that signals the maturation of commercial SDM interconnect hardware. This launch reflects how component-level innovation is shortening the gap between laboratory SDM research and deployable network infrastructure.

According to ScienceDirect, laser direct writing 3D-PIC fan-in/fan-out devices for coupled-core 4-core fiber achieve an average insertion loss of 0.63 dB at 1550 nm after full assembly. This performance level matters because lower insertion loss directly translates to longer transmission reach and fewer regeneration points — reducing total network cost. Additionally, optimized adiabatic taper design has cut insertion loss by 50% compared to prior works, signaling that fabrication advances are compressing cost curves for SDM commercialization.

Key Takeaways

- The Global Space Division Multiplexing Devices Market was valued at USD 1.9 Billion in 2025 and is forecast to reach USD 4.6 Billion by 2035.

- The market grows at a CAGR of 9.6% during the forecast period 2026 to 2035.

- By Component, Optical Fiber leads with a 32.8% market share in 2025.

- By Application, Telecommunications holds the dominant position with a 49.1% share.

- By Fiber Type, Multi-Core Fiber commands the largest share at 62.9%.

- By End-User, Telecom Operators account for 51.2% of total market demand.

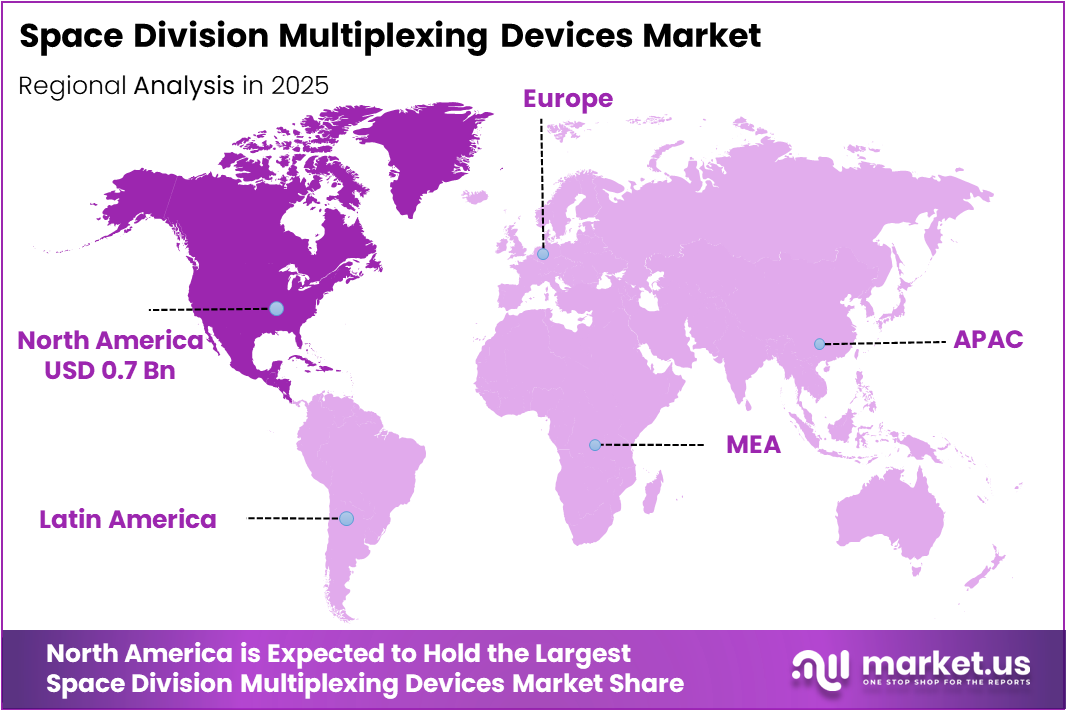

- North America dominates the regional landscape with a 41.80% share, valued at USD 0.7 Billion.

Component Analysis

Optical Fiber dominates with 32.8% due to foundational role in all SDM transmission.

In 2025, Optical Fiber held a dominant market position in the By Component segment of the Space Division Multiplexing Devices Market, with a 32.8% share. Optical fiber is the physical medium through which all spatial channels travel, making it the non-negotiable foundation of every SDM deployment. Without advanced multicore or few-mode fiber, no other SDM component functions — giving fiber the highest procurement priority across all end-user segments.

Multiplexers combine multiple spatial channels onto a single fiber input, acting as the entry point for SDM signal processing. Their performance directly determines system capacity and channel isolation quality. Vendors supplying low-crosstalk multiplexers command premium positioning because channel interference is the primary technical barrier limiting SDM deployment in live networks.

Demultiplexers separate spatially multiplexed channels at the receive end of a transmission link. Their precision determines the integrity of data recovered from each spatial path. As SDM systems scale to higher channel counts in hyperscale data centers, demultiplexer performance requirements tighten — creating a consistent upgrade cycle for this component category.

Amplifiers restore signal strength across long-distance SDM links where insertion losses accumulate. Multicore-compatible erbium-doped fiber amplifiers (MC-EDFAs) represent the critical enabling technology for submarine and long-haul SDM applications. The availability and cost of MC-EDFAs directly control the economic viability of deploying SDM in transoceanic cable systems.

Others in this segment include connectors, couplers, and passive routing components that complete the physical layer of an SDM network. These components carry lower unit value but are purchased in high volumes, making them a reliable revenue base for optical component distributors with broad catalog coverage.

Application Analysis

Telecommunications dominates with 49.1% due to carrier-scale bandwidth expansion requirements.

In 2025, Telecommunications held a dominant market position in the By Application segment of the Space Division Multiplexing Devices Market, with a 49.1% share. Telecom carriers face relentless traffic growth from mobile broadband, 5G backhaul, and enterprise connectivity services. SDM devices allow operators to multiply fiber capacity without replacing conduit infrastructure — a capital efficiency argument that accelerates procurement decisions at the network planning level.

Data Centers represent the fastest-scaling application segment, driven by the rise of AI training clusters and real-time inference workloads that generate massive intra-facility data movement. Hyperscale operators require inter-rack and inter-pod connectivity at terabit speeds, pushing fiber capacity beyond what conventional DWDM architectures can economically deliver. SDM adoption inside data centers signals a structural shift — from networking as support infrastructure to networking as a competitive performance variable.

Enterprise Networks adopt SDM devices primarily through private fiber deployments connecting distributed campuses and high-performance computing environments. Enterprises running real-time analytics, video conferencing at scale, or private cloud workloads encounter fiber capacity ceilings earlier than anticipated. SDM allows these organizations to upgrade transmission capacity through component-level investment rather than full network rebuilds.

Others include research institutions, government defense networks, and financial trading infrastructure where ultra-low latency and high bandwidth coexist as requirements. These segments purchase in lower volumes but specify the highest performance tiers — making them important early adopters for new SDM component generations before commercial-scale rollout.

Fiber Type Analysis

Multi-Core Fiber dominates with 62.9% due to proven capacity multiplication in commercial deployments.

In 2025, Multi-Core Fiber held a dominant market position in the By Fiber Type segment of the Space Division Multiplexing Devices Market, with a 62.9% share. Multi-core fiber carries multiple independent cores within a single cladding, multiplying transmission capacity by the number of cores without increasing cable diameter. This geometric efficiency makes it the preferred choice for submarine cable operators and hyperscale data center builders where physical conduit space is constrained and expensive.

Few-Mode Fiber supports multiple spatial modes within a single core, offering an alternative path to capacity expansion in scenarios where core-count scaling introduces excessive crosstalk. Few-mode fiber is particularly relevant for metro and regional network upgrades where operators need incremental capacity gains without full infrastructure replacement. Its commercial adoption lags multi-core fiber but advances in mode-selective components are narrowing the performance gap.

Others in the fiber type segment include multimode fibers with SDM-compatible profiles and experimental fiber designs under active research. These variants serve specialized applications in short-reach data center interconnects and laboratory testbeds. Their commercial volumes remain limited, but they represent the development pipeline from which the next dominant fiber standard is likely to emerge.

End-User Analysis

Telecom Operators dominate with 51.2% due to national network capacity upgrade mandates.

In 2025, Telecom Operators held a dominant market position in the By End-User segment of the Space Division Multiplexing Devices Market, with a 51.2% share. Operators managing national fiber backbones face capacity constraints that conventional upgrade paths cannot address cost-effectively. SDM adoption allows carriers to serve growing wholesale bandwidth demand and 5G transport requirements using existing fiber routes — a critical advantage when new cable deployment carries prohibitive cost and regulatory timelines.

Cloud Service Providers purchase SDM devices to satisfy the internal network demands of hyperscale data center campuses housing AI compute clusters and global content delivery infrastructure. Their procurement cycles are fast, volume-driven, and technically demanding — making them an influential customer segment that accelerates vendor product roadmaps. A single hyperscale procurement decision can shift annual component demand by hundreds of millions of dollars.

Enterprises deploy SDM-enabled fiber primarily in high-density campus networks, financial trading floors, and private cloud interconnects. Their purchase volumes are smaller than operators or cloud providers, but enterprise deployments often require customized configurations — creating a higher-margin service opportunity for vendors with strong technical support capabilities.

Others include research universities, national laboratories, and government-funded network infrastructure programs. These buyers often operate on the leading edge of SDM technology, specifying experimental fiber types and prototype device configurations. Their procurement volumes are modest, but their published performance data shapes the technical benchmarks that commercial buyers subsequently require.

Key Market Segments

By Component

- Optical Fiber

- Multiplexers

- Demultiplexers

- Amplifiers

- Others

By Application

- Telecommunications

- Data Centers

- Enterprise Networks

- Others

By Fiber Type

- Multi-Core Fiber

- Few-Mode Fiber

- Others

By End-User

- Telecom Operators

- Cloud Service Providers

- Enterprises

- Others

Drivers

Hyperscale Data Center Expansion and AI Workload Growth Force Operators Toward High-Capacity SDM Optical Architectures

Hyperscale data centers now process AI training and inference workloads that generate internal traffic volumes no conventional fiber architecture can sustain economically. Cloud operators and enterprise network planners require spatial multiplexing solutions to multiply transmission capacity without expanding physical conduit footprints. This creates direct procurement pressure for SDM optical components across the data center supply chain.

Global internet traffic growth from video streaming, cloud computing, and AI applications compounds this pressure at the carrier level. Telecom operators managing national backbones face capacity ceilings on their existing fiber assets — and SDM provides the only upgrade path that avoids full cable replacement. In June 2024, Nokia announced the acquisition of Infinera Corporation specifically to strengthen its capabilities in advanced optical components for space division multiplexing, signaling how seriously network equipment vendors treat this demand shift.

According to Nature, the 4-LP-mode ultra-wideband optical diffractive network multiplexer achieves maximum mode crosstalk less than −17 dB across the full O, E, S, C, L, and U bands spanning 1260–1675 nm. This performance level means that advanced mode multiplexers now cover the entire usable optical spectrum in a single device — a development that eliminates the band-by-band hardware complexity that previously made SDM systems prohibitively expensive to deploy at scale.

Restraints

High Development Costs and Integration Complexity With Legacy Fiber Infrastructure Constrain Broad SDM Adoption

Advanced multicore and few-mode fiber technologies carry substantially higher manufacturing and deployment costs than conventional single-mode fiber. This cost gap means that only operators with large-scale capacity requirements can justify the investment — limiting SDM adoption to a narrow tier of hyperscale and carrier-grade buyers in the near term. Smaller network operators remain priced out of first-generation deployments.

Integration with existing optical network infrastructure compounds the financial barrier. Legacy fiber systems use standardized connectors, amplifier spacings, and management software that are incompatible with SDM architectures. Operators face the choice of running parallel networks during transition periods or undertaking complete infrastructure overhauls — both options carry capital and operational costs that delay procurement decisions.

According to Nature, the ultra-wideband mode multiplexer-demultiplexer system achieves insertion loss below 0.53 dB — a technically impressive result that still represents a performance constraint in long-haul applications where losses accumulate across multiple network spans. This illustrates that even best-in-class SDM components introduce penalties that legacy system operators must budget for, reinforcing the economic hesitation around large-scale SDM transitions.

Growth Factors

Submarine Cable Expansion and 5G Backhaul Investment Open Large-Scale Commercial Deployment Channels for SDM Technology

Submarine optical cable systems represent one of the highest-value deployment channels for SDM technology. Long-distance transoceanic links require maximum transmission capacity per physical cable — exactly the performance profile that multicore fiber SDM delivers. New submarine cable projects commissioned by hyperscale cloud providers create multi-year procurement pipelines for SDM-compatible fiber and associated active components.

According to IEEE, commercially available fan-in/fan-out devices with 1 dB insertion loss cause 8–10% degradation in overall transmission performance and reach in multicore fiber SDM submarine cable systems. This quantified performance gap identifies a specific engineering target — reducing FI/FO device insertion loss below 1 dB — that directly unlocks longer cable spans and higher revenue per route for submarine operators. Vendors who solve this problem capture disproportionate value in high-stakes infrastructure projects.

The expansion of 5G network infrastructure and early-stage 6G research creates sustained demand for ultra-high capacity optical backhaul. Mobile network densification requires fiber to every cell site, and the aggregate backhaul capacity requirements of dense urban 5G grids exceed what current metro fiber networks provide. SDM adoption in backhaul infrastructure allows mobile operators to address this capacity gap through optical component upgrades rather than new civil infrastructure — a faster and more cost-effective path to 5G performance targets.

Emerging Trends

Integrated Photonics and Industry Collaboration Accelerate Compact, Energy-Efficient SDM Device Commercialization

Integrated photonics platforms are reducing SDM device form factors while simultaneously improving energy efficiency. Compact photonic integrated circuits consolidate multiple SDM functions — mode multiplexing, channel routing, and amplification — into single chip-scale assemblies. This integration trend lowers per-port cost and physical footprint, making SDM architectures viable in space-constrained environments like high-density data center switch racks.

According to ScienceDirect, optimized adiabatic taper design reduced the device transition length of fused taper-type fan-in/fan-out devices to 1.8 mm — more than 5 times shorter than prior works — while maintaining low insertion loss. This dimensional reduction is significant because it enables SDM interconnect hardware to fit within standard optical module footprints, clearing a major physical integration barrier for data center deployment at scale.

Telecom operators and optical component manufacturers increasingly collaborate on joint development programs to accelerate SDM standardization. These partnerships compress the timeline from laboratory prototype to certified network hardware — a critical step because carrier procurement requires standards compliance before volume purchasing begins. The energy efficiency dimension of this trend also aligns with operator sustainability commitments, making power-efficient SDM devices a dual-purpose procurement argument for large network buyers.

Regional Analysis

North America Dominates the Space Division Multiplexing Devices Market with a Market Share of 41.80%, Valued at USD 0.7 Billion

North America commands a 41.80% share of the global SDM devices market, valued at USD 0.7 Billion in 2025. This leadership reflects the concentration of hyperscale cloud operators and major telecom carriers that require the highest fiber capacity tiers. U.S.-based data center operators drive consistent procurement of advanced optical components, while federal broadband infrastructure programs sustain carrier investment in backbone network upgrades.

Europe Space Division Multiplexing Devices Market Trends

Europe maintains a strong position driven by regulatory mandates for next-generation broadband coverage and active investment in submarine cable infrastructure connecting European hubs to transatlantic routes. National telecom operators in Germany, France, and the UK have committed to fiber-to-the-premises programs that require high-capacity backbone upgrades. European research institutions also contribute to SDM technology development, creating a supportive environment for commercial adoption.

Asia Pacific Space Division Multiplexing Devices Market Trends

Asia Pacific represents the highest-growth regional opportunity for SDM device vendors. China, Japan, and South Korea operate large-scale fiber networks with active upgrade cycles, while India’s expanding digital infrastructure creates new demand for high-capacity optical systems. Major optical fiber manufacturers concentrated in this region benefit from both domestic deployment demand and export opportunities to global network builders requiring multicore fiber and SDM components.

Middle East and Africa Space Division Multiplexing Devices Market Trends

The Middle East and Africa region shows early-stage SDM adoption concentrated in GCC countries investing in smart city infrastructure and data center capacity. National digital transformation programs in Saudi Arabia and the UAE require enterprise-grade optical connectivity between government facilities and commercial cloud infrastructure. Africa’s long-haul terrestrial fiber networks represent a longer-term deployment opportunity as bandwidth demand from mobile broadband growth intensifies.

Latin America Space Division Multiplexing Devices Market Trends

Latin America’s SDM adoption centers on Brazil and Mexico, where domestic telecom operators are upgrading metro and backbone fiber networks to support growing enterprise and consumer broadband demand. Cross-border cable projects connecting South American hubs represent a key infrastructure driver. However, constrained capital expenditure budgets among regional carriers slow the transition from conventional fiber to SDM-enabled architectures.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Ciena Corporation positions itself as a software-driven optical networking vendor, differentiating its SDM-capable hardware through integrated management software that allows operators to automate spatial channel provisioning. This software layer creates switching costs that protect Ciena’s recurring revenue — operators who embed Ciena’s management platform into their network operations face significant migration friction when evaluating alternative hardware suppliers.

Fujitsu Limited leverages its deep integration across both optical component manufacturing and systems integration, giving it the ability to offer end-to-end SDM solutions from fiber components to network management. This vertical capability reduces procurement complexity for telecom operators who prefer single-vendor accountability for performance across the full optical signal chain. Fujitsu’s Japanese domestic market provides a high-volume proving ground for new SDM configurations before global commercial rollout.

Cisco Systems, Inc. approaches the SDM devices market through its dominant position in data center networking, where it can bundle optical transport capabilities with routing and switching infrastructure. Enterprise and cloud customers already running Cisco architectures represent a natural adoption base for Cisco-compatible SDM components. This installed base advantage means Cisco competes on integration simplicity rather than pure optical performance — a durable positioning in cost-sensitive enterprise segments.

In February 2025, Nokia Corporation completed the acquisition of Infinera Corporation, directly expanding its SDM optical component portfolio and engineering talent base. This move positions Nokia to compete at the component level — not just the systems level — in carrier and data center optical procurement. The combined product roadmap signals Nokia’s intent to challenge pure-play optical vendors on both performance and scale economies, reshaping competitive dynamics in the high-capacity optical transport segment.

Key Players

- Ciena Corporation

- Fujitsu Limited

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- NEC Corporation

- Nokia Corporation

- ZTE Corporation

- Corning Incorporated

- Sumitomo Electric Industries, Ltd.

- Furukawa Electric Co., Ltd.

Recent Developments

- August 2024 — HYC presented its expanded multicore fiber subassemblies at ECOC 2024, showcasing 4CH, 7CH, and 8CH optical fiber connectors alongside advanced fan-in/fan-out devices with 43 μm core pitch and hybrid subassemblies for MC-EDFA systems, demonstrating the breadth of HYC’s commercial SDM interconnect product line.

- February 2025 — Nokia completed the acquisition of Infinera Corporation, finalizing a transaction that enhances Nokia’s SDM optical networking product roadmap and creates manufacturing and engineering synergies across Nokia’s combined optical component and systems portfolio.

Report Scope

Report Features Description Market Value (2025) USD 1.9 Billion Forecast Revenue (2035) USD 4.6 Billion CAGR (2026-2035) 9.6% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Component (Optical Fiber, Multiplexers, Demultiplexers, Amplifiers, Others), By Application (Telecommunications, Data Centers, Enterprise Networks, Others), By Fiber Type (Multi-Core Fiber, Few-Mode Fiber, Others), By End-User (Telecom Operators, Cloud Service Providers, Enterprises, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Ciena Corporation, Fujitsu Limited, Cisco Systems, Inc., Huawei Technologies Co., Ltd., NEC Corporation, Nokia Corporation, ZTE Corporation, Corning Incorporated, Sumitomo Electric Industries, Ltd., Furukawa Electric Co., Ltd. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Space Division Multiplexing Devices MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Space Division Multiplexing Devices MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Ciena Corporation

- Fujitsu Limited

- Cisco Systems, Inc.

- Huawei Technologies Co., Ltd.

- NEC Corporation

- Nokia Corporation

- ZTE Corporation

- Corning Incorporated

- Sumitomo Electric Industries, Ltd.

- Furukawa Electric Co., Ltd.

Our Clients

- 183419

- Mar 2026