Quick Navigation

Report Overview

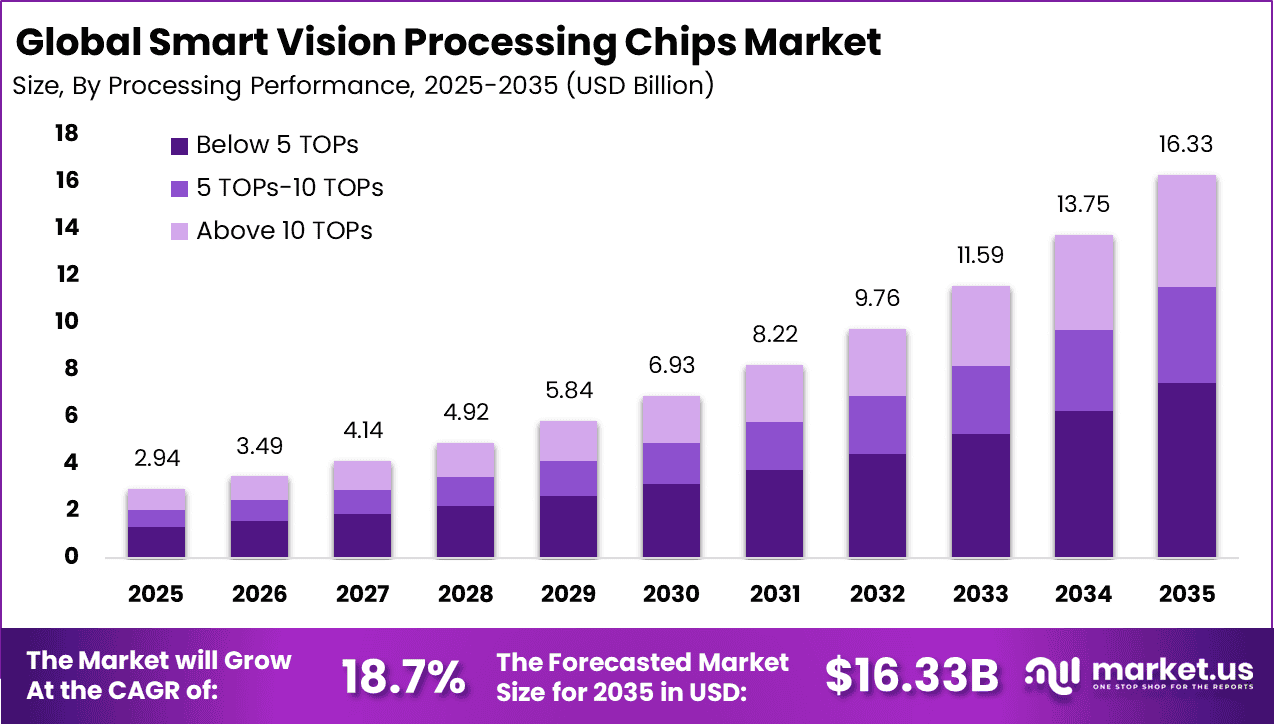

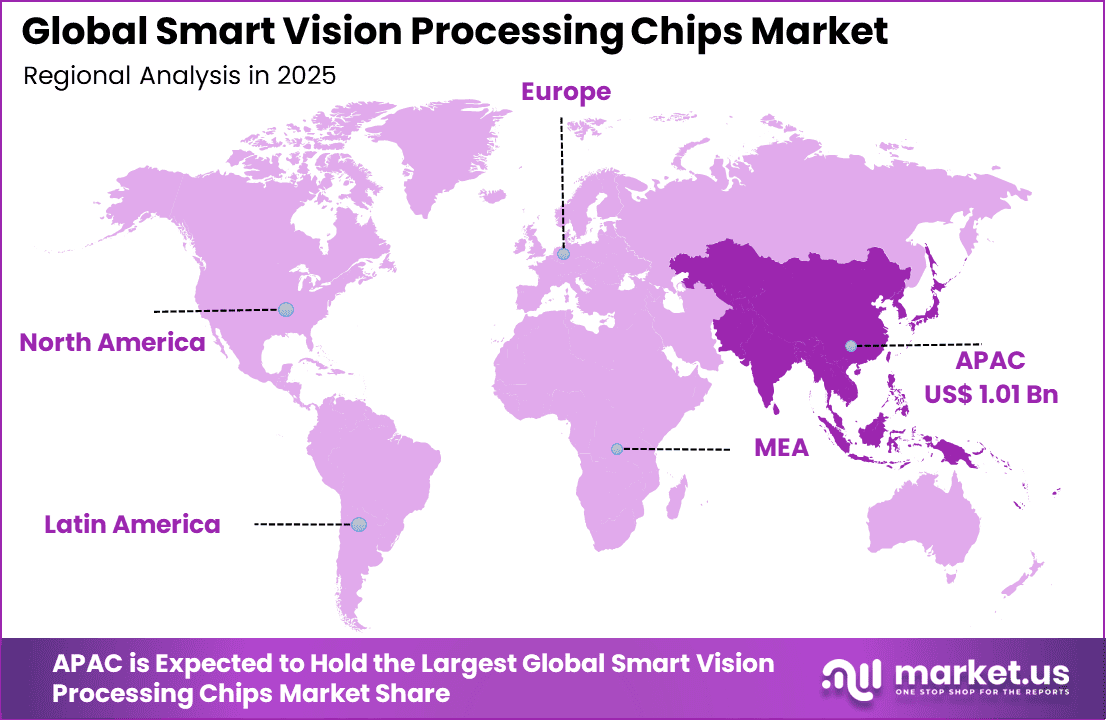

The Global Smart Vision Processing Chips Market size is expected to be worth around USD 16.33 billion by 2035, from USD 2.94 billion in 2025, growing at a CAGR of 18.7% during the forecast period from 2025 to 2035. Asia Pacific held a dominant market position, capturing more than 34.5% share and generating USD 1.01 billion in revenue.

Smart Vision Processing Chips refer to specialized semiconductor components designed to process visual data, such as images and videos, directly on devices. These chips enable real-time analysis, object detection, and pattern recognition with lower latency. They are widely used in cameras, autonomous systems, and smart devices to improve efficiency and reduce reliance on cloud processing.

The push for vision processing chips is shaped by rapid growth in AI applications across automotive, industrial, and healthcare environments. These use cases require instant visual decision-making. Around 80% of new autonomous vehicles integrate multiple vision chips, reflecting strong demand for low power, high speed processing, and advanced neural acceleration capabilities.

The market for Smart Vision Processing Chips is driven by rising demand for fast and efficient visual computing across vehicles, factories, healthcare, and smart devices. Businesses need chips that can process images instantly at the edge with low power use. Growing use of AI, automation, and real-time decision systems is further strengthening demand across many practical applications.

Demand is rising steadily with the expansion of edge computing, where data is processed closer to the source. This reduces latency and improves privacy. Nearly 65% of industrial robots use vision chips for quality inspection tasks, showing a clear shift toward intelligent, self-reliant systems across manufacturing, surveillance, and retail environments.

For instance, in January 2026, Rockchip announced RK3588V2 with enhanced vision ISP supporting 8K60 decoding and 6 TOPS NPU. Targeting smart screens and in-vehicle cameras, it offers 30% better power efficiency than competitors. Rockchip’s versatile platform keeps them competitive across consumer and automotive segments.

Key Takeaway

- In 2025, the Below 5 TOPs segment led the global smart vision processing chips market with a share of 45.7%.

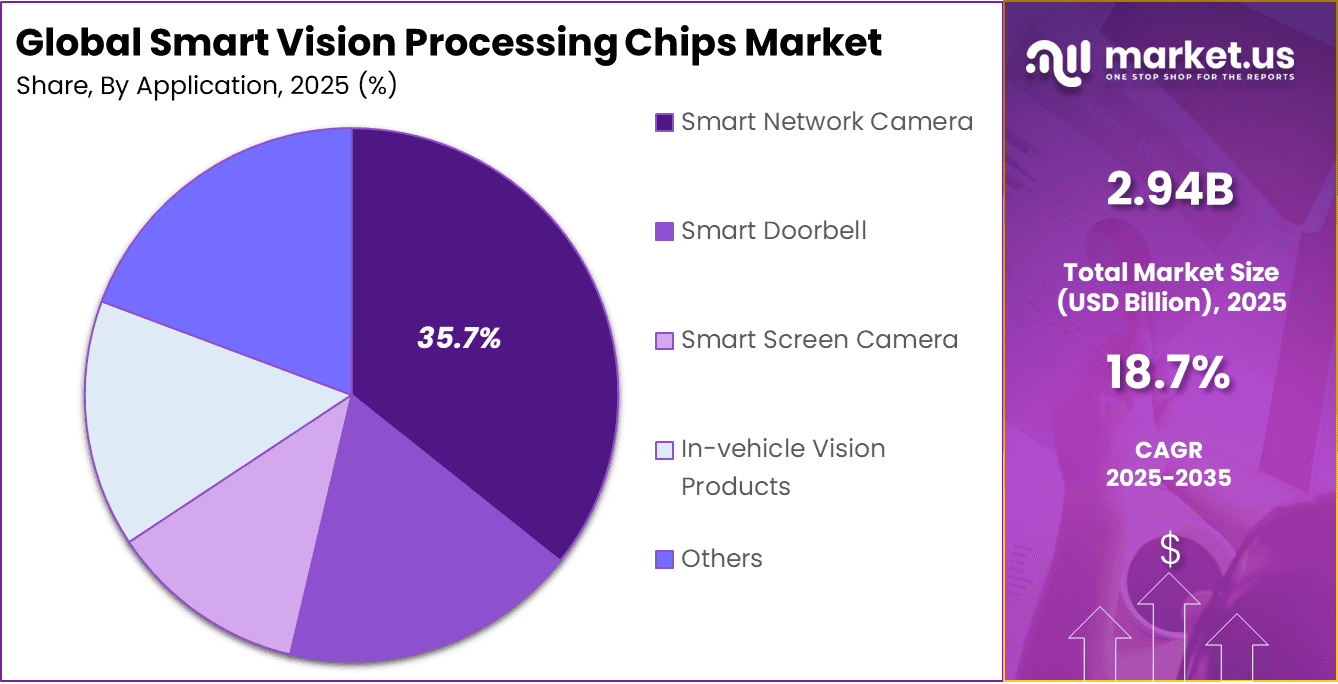

- The smart network camera segment held a dominant share of 35.7%, reflecting strong demand for embedded vision processing in surveillance devices.

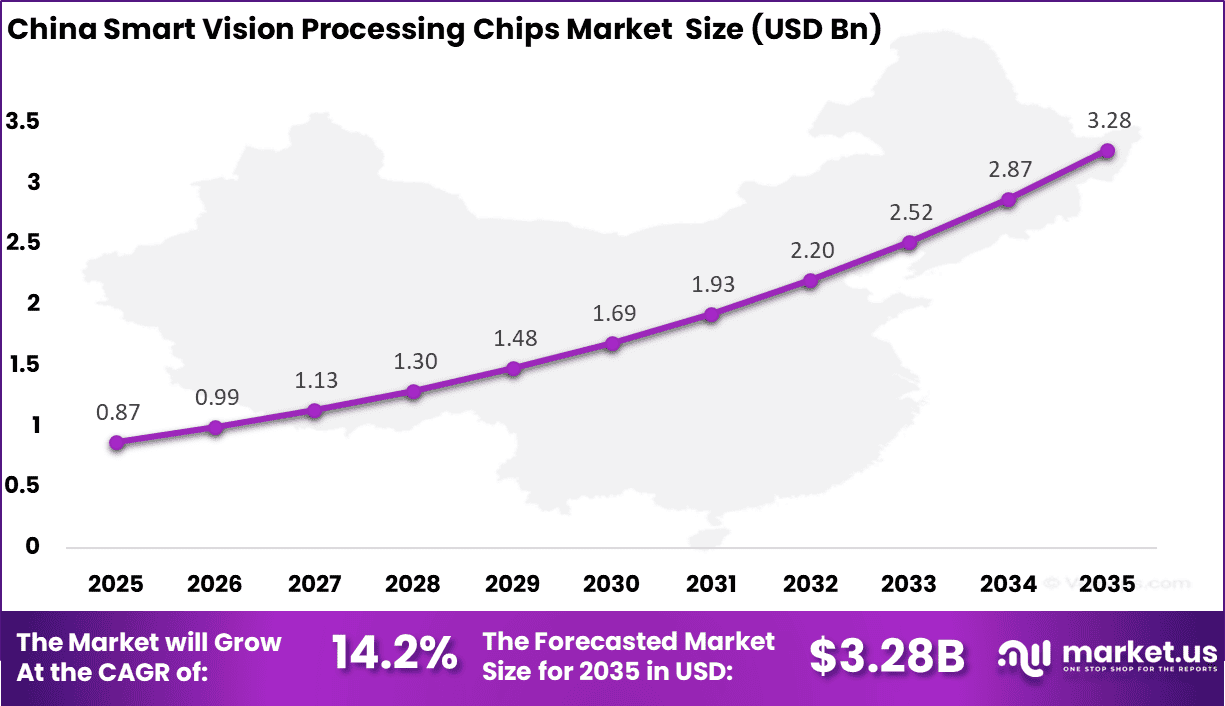

- The China smart vision processing chips market was valued at USD 0.87 billion in 2025 and is projected to grow at a CAGR of 14.2%.

- Asia Pacific accounted for more than 34.5% of the global market in 2025, supported by strong electronics manufacturing and vision technology adoption.

Role of Generative AI

Generative AI is improving how vision chips are trained by creating synthetic images when real datasets are limited. This approach helps models learn faster from well-structured visual data. It cuts training time by 70% in many cases, especially for scenarios involving rare events like defects or safety incidents.

It also supports privacy-focused development in sensitive sectors such as healthcare, where real image usage is restricted. Around 60% of computer vision projects now use synthetic data methods. This improves accuracy and reduces deployment time, making chip performance more reliable across diverse real-world environments.

Investment and Business Benefits

Investment activity is focused on edge AI solutions, particularly in retail analytics and robotics applications, where compact and efficient chips are essential. Roughly 60% of venture interest targets automotive vision technologies. Additional opportunities are emerging in drone-based multi-modal systems and healthcare imaging tools, supporting long-term innovation and adoption.

Vision processing chips provide real-time insights that improve operational efficiency and workplace safety, especially in automated environments like warehouses. These chips support scalable deployments across devices while maintaining cost control. Firms report up to 50% faster processing speeds, enabling quicker decision making, improved service delivery, and stronger customer satisfaction.

Regional Analysis

In 2025, Asia Pacific held a dominant market position in the Global Smart Vision Processing Chips Market, capturing more than 34.5% share and generating USD 1.01 billion in revenue. This dominance is because the region has a strong electronics manufacturing base, large-scale demand for smart devices, and fast adoption of AI-enabled vision systems across industries.

Countries in this region are investing heavily in automation, smart cities, and advanced surveillance infrastructure. Strong semiconductor activity, cost-efficient production, and rising use of edge processing in consumer and industrial applications continue to support regional market leadership.

For instance, in February 2025, Zhejiang Dahua Technology Co., Ltd. unveiled its Xinghan Large-Scale AI Models integrated with self-developed vision processing chips, targeting video surveillance and smart city applications. The chips deliver multimodal intelligence for urban traffic management, as demonstrated in Malaysia’s Penang Bridge project. Dahua’s AIoT focus reinforces China’s commanding market share in Asia Pacific vision processing.

China Smart Vision Processing Chips Market Size

The market for Smart Vision Processing Chips within China is growing tremendously and is currently valued at USD 0.87 billion; the market has a projected CAGR of 14.2%. The market is growing because demand for smart cameras, industrial automation, driver assistance systems, and intelligent consumer devices is rising steadily.

Strong electronics manufacturing capacity, faster adoption of edge AI, and continued investment in smart city projects are also supporting growth. In addition, local demand for real-time image processing with lower latency and better energy efficiency is encouraging wider use of these chips across multiple applications.

For instance, in March 2025, Hangzhou Hikvision Digital Technology Co., Ltd. strengthened China’s dominance in smart vision processing chips by launching advanced AI SoC processors optimized for edge computing in surveillance cameras. These chips enable real-time object detection and facial recognition with minimal latency, powering massive smart city deployments across Asia.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Processing Performance Analysis

In 2025, The Below 5 TOPs segment held a dominant market position, capturing a 45.7% share of the Global Smart Vision Processing Chips Market. This dominance is due to the strong demand for energy-efficient processing in edge devices, where real-time decisions are required. Many applications, such as basic object detection and monitoring tasks, operate well within lower performance limits, making these chips practical for wide deployment across consumer and industrial use cases globally.

These chips also support compact designs and reduce system costs, which makes them suitable for large-scale adoption. Manufacturers prefer them for devices that require stable performance without high power consumption. Their ability to balance efficiency and functionality ensures steady demand across smart devices and embedded vision systems.

For Instance, in March 2026, Sony introduced a new low‑power vision processing platform optimized for below‑5‑TOPs edge cameras, focusing on energy‑efficient AI‑enabled surveillance and home‑security devices. The chip emphasizes compact form factor and reduced thermal load, enabling OEMs to build smaller, battery‑friendly cameras without compromising basic analytics performance for applications such as motion detection and people counting.

Application Analysis

In 2025, the Smart Network Camera segment held a dominant market position, capturing a 35.7% share of the Global Smart Vision Processing Chips Market. This dominance is due to the increasing need for real-time video analytics in surveillance and monitoring environments. Smart network cameras are now expected to process data locally, allowing faster detection of events and reducing dependence on centralized systems. This shift supports efficient operations across security and industrial applications.

These cameras also improve bandwidth management by limiting unnecessary data transfer to cloud systems. Organizations benefit from faster insights and reduced storage requirements. As safety and automation needs grow, demand for intelligent camera systems continues to expand across urban infrastructure and enterprise environments steadily.

For instance, in March 2026, Ambarella launched an advanced smart network camera platform embedding a powerful NPU and multi‑stream encoding, aimed at high‑volume security and infrastructure deployments. The design allows cameras to run complex object detection, people‑counting, and license‑plate recognition directly on‑device, reducing reliance on centralized servers and lowering the total cost of AI‑enabled video analytics.

Key Market Segments

By Processing Performance

- Below 5 TOPs

- 5 TOPs-10 TOPs

- Above 10 TOPs

By Application

- Smart Network Camera

- Smart Doorbell

- Smart Screen Camera

- In-vehicle Vision Products

- Others

Emerging Trends

Edge computing is reshaping how vision tasks are processed, with nearly 70% of workloads now handled directly on chips instead of the cloud. This shift reduces delays and ensures faster response in systems like drones, surveillance cameras, and autonomous devices that require immediate decision-making.

At the same time, neuromorphic chip designs are gaining attention for their efficiency. These systems mimic brain-like processing and reduce power use by 80% for continuous sensing. When combined with event-based sensors, they allow robots and machines to process only relevant visual data, improving speed and energy use.

Growth Factors

The automotive sector continues to be a major growth driver, contributing nearly 35% of chip demand due to the rising use of driver assistance systems. Multi-camera setups in vehicles require real-time image processing, which increases the need for advanced vision chips that can support safer and more responsive driving experiences.

Industrial automation also plays a strong role, adding around 25% demand for vision chips in manufacturing. These chips enable defect detection up to 10x faster than traditional methods. This leads to reduced material waste, improved product quality, and higher adoption of automated inspection systems across factories.

Market Dynamics

Drivers - Rising Need for Real-Time Analytics

Real-time analytics is becoming essential as businesses require instant insights from visual data. Smart vision processing chips enable quick interpretation of images and video streams directly on devices. This supports faster decisions in areas such as surveillance, industrial monitoring, and smart mobility, where delays can reduce effectiveness and operational value.

The growing use of connected devices is further strengthening this need. Organizations prefer systems that can process data immediately without depending on remote servers. This improves response time and reliability. As industries move toward automation and intelligent systems, demand for real-time visual processing continues to increase steadily across applications.

For instance, in March 2026, Rockchip started shipping its upgraded RV1126B AI vision chip after tests cleared, packing a strong NPU for real-time scene analysis. The chip grabs complex images and fuses data on the fly, aiding factory monitors that spot flaws without delay. Builders say it halves response times for live alerts.

Restraint - Complex Supply Chains

The market faces challenges due to complex semiconductor supply chains that involve multiple stages and global dependencies. Delays in component availability and production constraints can impact delivery timelines. This creates uncertainty for manufacturers and buyers, making it harder to maintain a consistent supply and plan long-term deployments effectively.

Managing these supply networks also requires coordination across regions and partners. Any disruption can increase costs and slow innovation cycles. Companies often need to invest more in sourcing strategies and inventory planning. These operational challenges can limit market growth, especially for smaller players with limited access to stable supply channels.

For instance, in February 2026, Huawei HiSilicon faced delays in chip deliveries due to tight component shortages from global disruptions, slowing orders for vision sensors. Teams had to rework designs mid-way, stretching timelines by months and hiking costs for partners. It highlights how tangled supplier links stall fresh releases.

Opportunities - Smarter Automation

Smarter automation is creating strong opportunities for smart vision processing chips across industries. Visual systems are being used for inspection, quality control, and process monitoring. These applications require reliable image processing at the device level, increasing demand for efficient, compact chips designed for continuous operation.

As automation expands, businesses seek solutions that improve accuracy and reduce manual effort. Vision-based systems can identify patterns and detect issues faster than traditional methods. This enhances productivity and consistency. The growing shift toward automated workflows is expected to support wider adoption of smart vision chips in industrial and commercial environments.

For instance, in April 2026, Sony unveiled a new sensor chip series for robotic arms in auto plants, enabling machines to spot parts and adjust their grips instantly. Paired with edge AI, it boosts assembly speed without human checks, tapping into the automation wave. Early tests in plants show smoother workflows ahead.

Challenges - Privacy and Compliance Concerns

Increasing use of vision-based systems raises concerns around data privacy and regulatory compliance. Visual data often includes sensitive information, which requires careful handling and secure processing. Organizations must ensure that systems follow evolving rules and guidelines while maintaining user trust and protecting personal data.

Compliance requirements can add complexity to product development and deployment. Companies need to invest in secure design, data protection measures, and transparent practices. Failure to meet these expectations can limit adoption and create legal risks, making privacy and compliance a key challenge in the growth of this market.

For instance, in December 2025, Nextchip paused a facial recognition chip rollout after regulators flagged data handling gaps in public surveillance tests. Extra audits and code tweaks followed to meet strict rules on user tracking, delaying market entry. It underscores the tightrope of powerful vision tech and privacy laws.

Key Players Analysis

One of the leading players in December 2025, Goke Microelectronics partnered with HiWatch to deploy GK2102 chips across 5 million Chinese surveillance cameras. The chip’s 4 TOPS AI delivers real-time face recognition at the edge. This massive rollout reinforces China’s surveillance infrastructure push.

Top Key Players in the Market

- Sony

- Ambarella

- Huawei HiSilicon

- Nextchip

- Goke Microelectronics

- Rockchip Electronics

- Axera Semiconductor

- Shanghai TaskOrientedAI

- Vimicro Technology Corporation

- Shanghai Visinex Technology

- Shanghai Timesintel

- Shanghai NextVPU

- Other Major Players

Recent Developments

- In March 2026, Sony unveiled its latest IMX990 stacked CMOS sensor chip with integrated AI processing for smart cameras. Delivering 120dB dynamic range, it’s perfect for automotive ADAS and surveillance. Sony’s continued dominance in image sensor tech keeps them ahead, especially as edge AI demands better raw data quality.

- In February 2026, Huawei HiSilicon introduced the Ascend 710B vision processor optimized for smart city surveillance networks. Supporting 16-stream 4K decoding, it integrates with HarmonyOS for seamless deployment. Despite global restrictions, HiSilicon maintains a strong domestic market share through massive Chinese smart city projects.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2.9 Billion |

| Forecast Revenue (2035) | USD 16.3 Billion |

| CAGR(2026-2035) | 18.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics, and Emerging Trends |

| Segments Covered | By Processing Performance (Below 5 TOPs, 5 TOPs-10 TOPs, Above 10 TOPs), By Application (Smart Network Camera, Smart Doorbell, Smart Screen Camera, In-vehicle Vision Products, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Sony, Ambarella, Huawei HiSilicon, Nextchip, Goke Microelectronics, Rockchip Electronics, Axera Semiconductor, Shanghai TaskOrientedAI, Vimicro Technology Corporation, Shanghai Visinex Technology, Shanghai Timesintel, Shanghai NextVPU, Other Major Players |

| Customization Scope | Customization for segments and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |