Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Component Analysis

- By Security Type Analysis

- By Application Analysis

- By Distribution Channel Analysis

- Investor Type Impact Analysis

- Technology Enablement Analysis

- Key Challenges

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

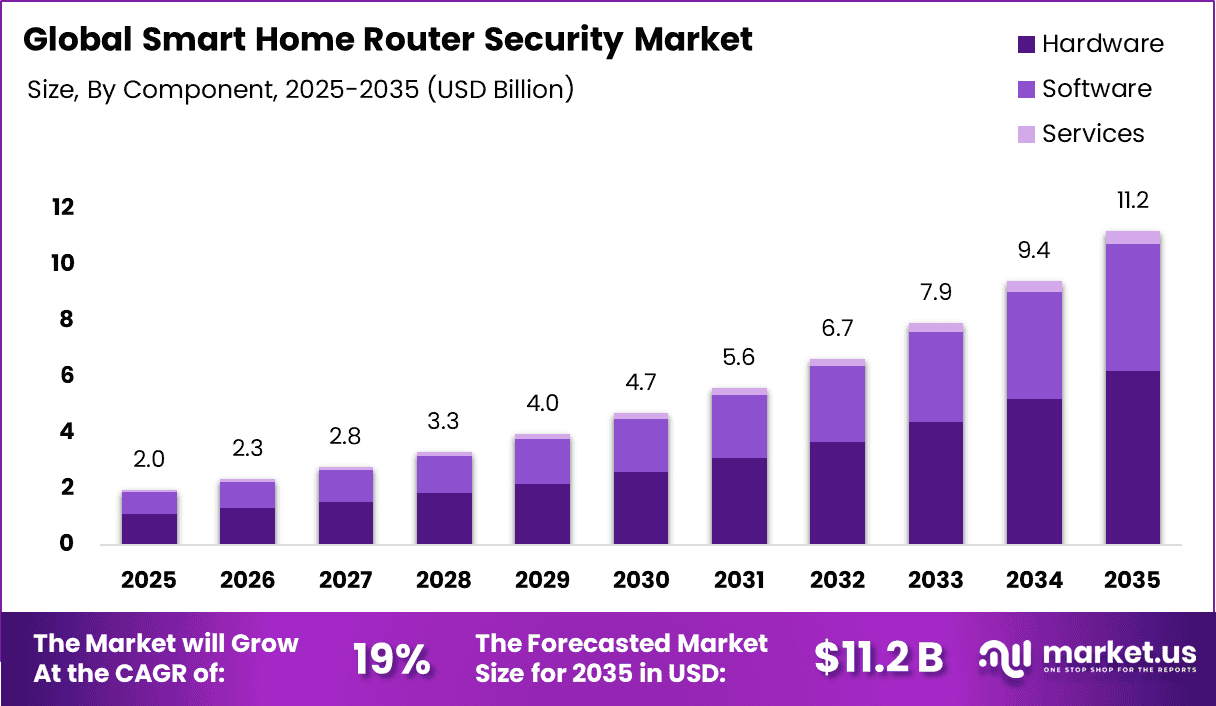

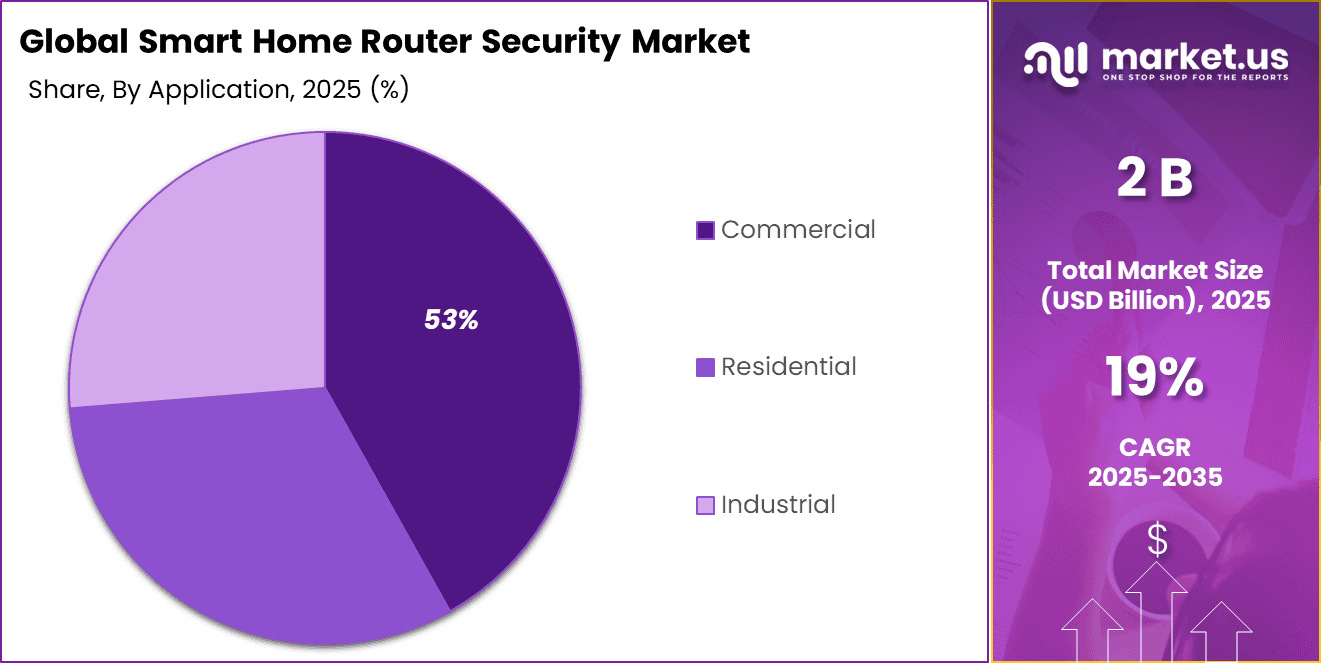

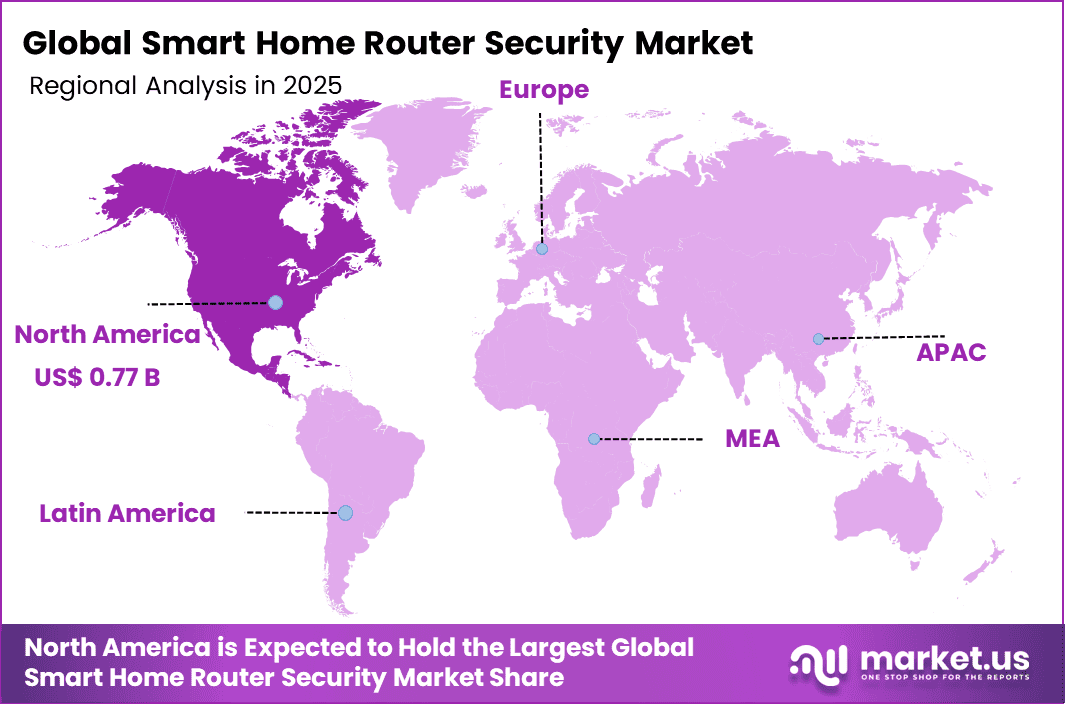

The Global Smart Home Router Security Market generated USD 2 billion in 2025 and is predicted to register growth from USD 2.3 billion in 2026 to about USD 11.2 billion by 2035, recording a CAGR of 19% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 39.2% share, holding USD 0.77 Billion revenue.

Top Market Takeaways

- Hardware commands 55.4% market share, delivering embedded firewalls, intrusion prevention systems, and secure Wi-Fi chipsets optimized for smart home gateway protection.

- Network security captures 44.7%, enabling deep packet inspection, device quarantine, and zero-trust segmentation for multi-device residential ecosystems.

- Commercial applications claim 52.6%, powering hospitality networks, multi-dwelling units, and small business deployments with centralized threat intelligence.

- Offline distribution dominates at 63.7%, facilitating retail partnerships, managed service bundling, and enterprise procurement cycles.

- North America drives 39.2% global value, with U.S. market at USD 0.62 billion and 23.5% CAGR, fueled by smart apartment mandates and consumer privacy regulations.

Smart home router security is becoming an essential part of connected living as households continue to adopt multiple smart devices such as cameras, voice assistants, and connected appliances. The router is no longer just a connectivity tool but acts as the central control point for all digital traffic within a home.

As cyber risks grow more complex, users are paying closer attention to securing their home networks to prevent unauthorized access, data theft, and device manipulation. This shift is pushing the market toward more advanced security-enabled routers that can offer built-in protection, automatic updates, and real-time monitoring. The increasing dependence on uninterrupted and safe internet access is strengthening the role of router security in modern homes.

One of the key driving factors is the rapid expansion of connected devices within households, which is increasing the attack surface for cyber threats. Consumers are becoming more aware of risks such as hacking, identity theft, and privacy breaches, especially with the rise of remote work and online transactions. Government initiatives around digital safety and awareness are also encouraging better security practices at the household level.

In addition, internet service providers are integrating security features into routers to enhance user trust and reduce network vulnerabilities. The growing use of cloud-based services and smart ecosystems is further pushing the need for routers that can detect and respond to threats automatically without requiring technical expertise from users.

Demand for smart home router security solutions is rising steadily as users seek easy to manage and reliable protection systems. There is a clear shift toward plug and play security features that do not require complex setup, making them suitable for non technical users. Households are also looking for solutions that offer parental controls, device-level monitoring, and threat alerts in real time.

The demand is particularly strong in urban areas where smart home adoption is higher and digital lifestyles are more integrated. At the same time, subscription-based security services linked with routers are gaining traction as they provide continuous updates and protection. This evolving demand pattern indicates a move toward more intelligent, automated, and user-friendly security solutions in the home networking space.

Drivers Impact Analysis

| Key Driver | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| Rising cyber threats targeting home networks | +4.7% | Strong in North America and Europe, growing in Asia Pacific | Short to long term | More cyberattacks increase security demand |

| Growth in smart home device adoption | +4.2% | Global, with strong momentum in US, China, and Western Europe | Medium to long term | More devices raise security needs |

| Increasing consumer awareness of data privacy | +3.0% | North America and Europe leading, emerging in Asia | Medium term | Users prefer secure network solutions |

| Expansion of remote work ecosystems | +2.5% | Strong in developed markets such as US and UK | Short to medium term | Home networks handle sensitive work data |

| Integration of AI-based threat detection in routers | +4.3% | Technology-driven markets like US, Japan, South Korea | Medium to long term | AI improves threat detection speed |

Restraints Impact Analysis

| Key Restraint | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| High cost of advanced secure routers | -3.1% | Emerging markets in Asia, Latin America, Africa | Short to medium term | High cost limits adoption |

| Lack of technical awareness among consumers | -2.4% | Developing regions | Medium term | Low awareness reduces upgrades |

| Compatibility issues with legacy devices | -1.6% | Global | Medium term | Older devices face integration issues |

| Data privacy concerns around cloud-based security | -1.2% | Europe and North America | Medium to long term | Trust issues slow adoption |

| Fragmented ecosystem of IoT standards | -2.1% | Global | Long term | Lack of standards creates challenges |

By Component Analysis

The hardware segment accounted for 55.4% of the market share, reflecting its strong role in ensuring built-in security at the device level. This dominance is driven by the growing demand for routers with integrated firewalls, secure chipsets, and advanced encryption capabilities. Consumers and businesses are increasingly prioritizing physical security features that protect networks from unauthorized access. Hardware-based solutions are also preferred for their reliability and long-term performance, especially in environments where continuous protection is critical.

Another factor supporting this segment is the shift toward smart homes with multiple connected devices requiring stable and secure infrastructure. Hardware solutions provide consistent protection without relying heavily on external updates or subscriptions, which makes them attractive for long-term deployment. Manufacturers are also embedding advanced security features directly into routers, which enhances performance and reduces vulnerability risks at the source.

By Security Type Analysis

The network security segment held 44.7% share, supported by the rising need to protect connected devices and data traffic within smart home ecosystems. This segment benefits from increasing awareness about cyber threats such as malware, phishing, and unauthorized intrusions. Network-level protection tools, including intrusion detection systems and traffic monitoring solutions, are widely adopted as they provide a centralized approach to securing multiple devices.

In addition, the growing number of IoT devices in households and workplaces has increased the complexity of network environments. This has led to higher demand for solutions that can monitor and control data flow in real time. Network security systems offer scalable protection and allow users to manage risks more effectively, which is encouraging broader adoption across both residential and commercial settings.

By Application Analysis

The commercial segment captured 53% of the market, driven by the growing adoption of smart routers in offices, retail spaces, and service environments. Businesses are focusing on securing their internal networks to protect sensitive information and ensure uninterrupted operations. The increasing use of IoT devices in commercial settings has also increased the need for reliable router security solutions.

Moreover, organizations are implementing stricter cybersecurity practices to meet regulatory and operational requirements. Commercial users tend to invest in advanced configurations and monitoring tools to manage large networks efficiently. This has strengthened demand for robust router security systems that can support multiple users, ensure data protection, and maintain network stability in high-traffic environments.

By Distribution Channel Analysis

The offline segment dominated with a 63.7% share, reflecting strong consumer preference for purchasing networking equipment through physical stores and authorized dealers. Buyers often rely on expert guidance and product demonstrations before investing in security-focused devices. Offline channels also offer installation support and after-sales services, which are important for customers seeking reliable setup and maintenance.

Additionally, trust plays a key role in purchasing decisions for security-related products. Many users prefer in-person consultations to better understand product features and compatibility with their existing systems. Retail stores and distributors provide hands-on experience and immediate assistance, which enhances customer confidence and contributes to the continued dominance of offline distribution channels.

Investor Type Impact Analysis

| Investor Type | Growth Sensitivity | Risk Exposure | Geographic Focus | Investment Outlook |

|---|---|---|---|---|

| Venture capital firms | Very high | High | US, China, Israel | Focus on early-stage cybersecurity startups with strong innovation potential |

| Private equity firms | High | Moderate | North America and Europe | Investing in scaling established router and security solution providers |

| Corporate investors | Moderate to high | Moderate | Global | Strategic investments to strengthen smart home and network ecosystems |

| Institutional investors | Moderate | Low to moderate | Developed markets | Prefer stable companies with consistent demand in cybersecurity hardware |

| Government and public funding bodies | Moderate | Low | US, EU, Asia Pacific | Supporting cybersecurity infrastructure and digital safety initiatives |

Technology Enablement Analysis

| Technology | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| AI and machine learning-based threat detection | +5.1% | US, China, Japan | Medium to long term | Enables automated protection |

| Cloud-based security management platforms | +3.5% | North America and Europe | Short to medium term | Supports remote control |

| Zero-trust network architecture integration | +4.0% | Developed markets | Medium to long term | Improves access security |

| Edge computing in routers | +2.8% | Global with early adoption in US and Asia | Medium term | Enhances real-time response |

| IoT security protocols and encryption advancements | +4.2% | Global | Long term | Strengthens device security |

Key Challenges

- Increasing cyber threat complexity, as smart home routers face advanced attacks like botnets and ransomware, making continuous protection difficult.

- Low user awareness and weak security practices, as many users do not update firmware or use strong passwords, increasing network vulnerability.

- Fragmented device ecosystem, as multiple connected devices follow different security standards, raising risk levels.

- High cost of advanced security features, which limits adoption, especially in price-sensitive markets.

- Regulatory complexity across regions, making compliance difficult for manufacturers and slowing standardization.

Emerging Trends

The smart home router security market is witnessing a clear shift toward integrated, intelligent protection systems that operate directly at the network edge. One of the key emerging trends is the move from basic firewall protection to AI-driven threat detection embedded within routers. These systems continuously learn from traffic patterns and identify unusual behavior in connected devices such as cameras, smart TVs, and voice assistants.

Another noticeable trend is the rise of zero-trust network models in home environments, where every device is verified before gaining access to the network. Consumers are also showing preference for routers that offer automatic firmware updates and real-time alerts through mobile apps, reflecting a growing demand for convenience alongside security. In addition, the adoption of mesh networking systems is increasing, and security is being built into each node, ensuring consistent protection across larger residential spaces.

Growth Factors

The growth of this market is strongly supported by the rapid expansion of connected devices within households and the increasing awareness of cyber risks among users. As more people rely on remote work, online education, and digital entertainment, home networks are becoming critical infrastructure, which is driving the need for stronger protection. The rise in cyberattacks targeting home networks, including data breaches and unauthorized access, is encouraging users to invest in secure router solutions.

Regulatory attention toward data privacy and consumer protection is also influencing manufacturers to enhance built-in security features. Furthermore, the growing adoption of smart home ecosystems is creating a need for centralized security control at the router level, as it acts as the first line of defense for all connected devices. This combination of increased digital dependency and evolving threat landscape is expected to sustain demand for advanced router security solutions.

Key Market Segments

By Component

- Hardware

- Software

- Services

By Connectivity

- Z-Wave

- Zigbee

- Wi-Fi

- Bluetooth

- Others

By Lock Type

- Deadbolt Controllers

- Mortise Lock Controllers

- Handle Set Controllers

- Others

By Application

- Residential

- Commercial

- Industrial

By Sales Channel

- Direct-to-Consumer (Online/Retail)

- Professional Installers & Security Dealers

- Original Equipment Manufacturers (OEMs)

Regional Analysis

North America accounted for 39.2% of the Smart Home Router Security market, reflecting strong adoption of connected home ecosystems and rising awareness around network-level protection. This dominance is driven by the high penetration of smart devices such as connected cameras, voice assistants, and home automation systems, which has increased the need for secure home networks. Consumers in this region show a clear preference for advanced router security features, including threat detection, parental controls, and device-level monitoring.

The presence of mature broadband infrastructure and early adoption of new networking technologies has further supported the demand for secure routers. In addition, growing concerns around data privacy and cyber threats have encouraged households to invest in security-focused networking solutions, strengthening regional market leadership.

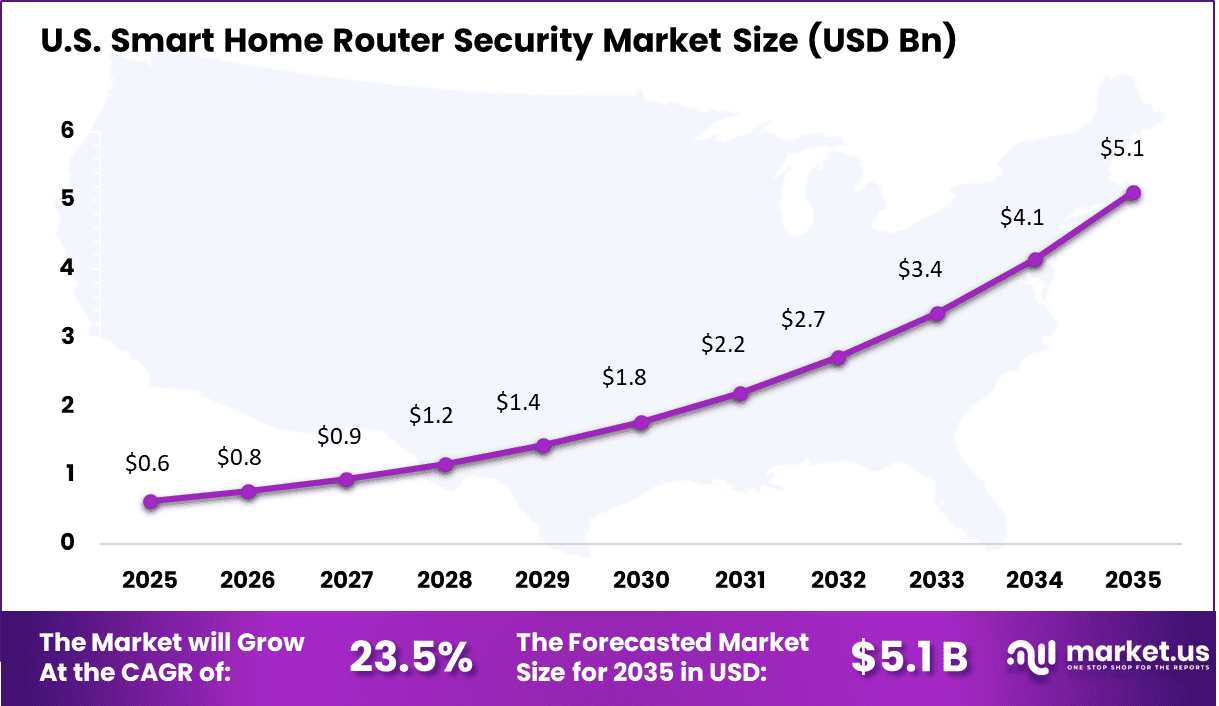

The U.S. market reached USD 0.62 Billion and is projected to grow at a CAGR of 23.5%, highlighting strong momentum in consumer demand and technology upgrades. This growth is supported by increasing remote work trends, where secure home networks have become essential for both personal and professional use.

Households are becoming more aware of risks such as unauthorized access, phishing attacks, and IoT vulnerabilities, which is pushing demand for integrated security solutions within routers. Internet service providers are also playing a role by offering bundled security features, making adoption easier for end users. The expansion of smart homes, along with rising digital dependency, is expected to sustain strong growth in the US market over the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

The competitive landscape of the Smart Home Router Security Market is moderately fragmented, with a combination of global cybersecurity vendors, networking equipment providers, and emerging technology firms competing to strengthen their positions.

Companies such as Cisco Systems, Inc., Symantec Corporation, Trend Micro Incorporated, NortonLifeLock Inc., and Fortinet, Inc. focus on delivering advanced security capabilities including threat intelligence, intrusion detection, and cloud-based protection tailored for home networks. At the same time, networking-focused players like TP-Link Technologies Co., Ltd., NETGEAR, Inc., ASUSTeK Computer Inc., D-Link Corporation, and Zyxel Communications Corp. integrate security features directly into routers, such as secure firmware, parental controls, and network monitoring tools. This blend of cybersecurity expertise and hardware integration highlights the ongoing shift toward built-in, user-friendly security solutions for connected households.

In addition, software-centric security providers such as Bitdefender LLC, Avast Software s.r.o., ESET, spol. s r.o., F-Secure Corporation, McAfee, LLC, and BullGuard Ltd. are expanding their reach through partnerships with router manufacturers and internet service providers, enabling embedded protection at the network level. Emerging players like Cujo AI are introducing AI-driven platforms that monitor device behavior and detect anomalies in real time.

Meanwhile, large technology-driven firms such as Huawei Technologies Co., Ltd., Palo Alto Networks, Inc., and Check Point Software Technologies Ltd. are focusing on cloud-managed security frameworks and zero-trust approaches to strengthen their offerings. Overall, competition in this market is shaped by innovation in artificial intelligence, seamless integration with IoT ecosystems, and the ability to deliver simple yet effective security solutions for end users.

Top Key Players in the Market

- Cisco Systems, Inc.

- Symantec Corporation

- Trend Micro Incorporated

- NortonLifeLock Inc.

- TP-Link Technologies Co., Ltd.

- NETGEAR, Inc.

- ASUSTeK Computer Inc.

- D-Link Corporation

- Huawei Technologies Co., Ltd.

- Zyxel Communications Corp.

- Fortinet, Inc.

- F-Secure Corporation

- Bitdefender LLC

- Avast Software s.r.o.

- ESET, spol. s r.o.

- Palo Alto Networks, Inc.

- Check Point Software Technologies Ltd.

- Cujo AI

- McAfee, LLC

- BullGuard Ltd.

- Others

Future Outlook

The future outlook for the Smart Home Router Security Market remains highly positive, supported by the rapid expansion of connected devices and increasing cybersecurity awareness among consumers. The market is anticipated to witness strong growth momentum, driven by the rising number of IoT-enabled home environments, where routers act as the primary entry point for network security. As smart homes continue to evolve, demand for advanced router-level protection such as AI-based threat detection, real-time monitoring, and automated response systems is expected to accelerate significantly.

Recent Developments

- March, 2026 – Cisco Talos adds AI router threat hunting for Linksys and blocks 99% zero-days. Scans smart bulbs and Home DNA Center pilots live. Adds guest Wi-Fi isolation and firmware auto-updates.

- February, 2026 – Norton Genie scans router firmware with AI and patches 500 vulns monthly. Parental controls block phishing and 50M homes protected. Includes VPN kill switch and dark web alerts.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2 Billion |

| Forecast Revenue (2035) | USD 11.2 Billion |

| CAGR(2025-2035) | 19% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Hardware, Software, Services), By Security Type (Network Security, Endpoint Security, Application Security, Cloud Security), By Application (Residential, Commercial, Industrial), By Distribution Channel (Online, Offline) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Cisco Systems, Inc., Symantec Corporation, Trend Micro Incorporated, NortonLifeLock Inc., TP-Link Technologies Co., Ltd., NETGEAR, Inc., ASUSTeK Computer Inc., D-Link Corporation, Huawei Technologies Co., Ltd., Zyxel Communications Corp., Fortinet, Inc., F-Secure Corporation, Bitdefender LLC, Avast Software s.r.o., ESET, spol. s r.o., Palo Alto Networks, Inc., Check Point Software Technologies Ltd., Cujo AI, McAfee, LLC, BullGuard Ltd., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |