Global Smart Finance Hardware Market Size, Share and Analysis Report By Type (Smart POS (Point of Sale) Terminals, Smart ATMs (Automated Teller Machines), Kiosks & Self-Service Terminals, Payment Cards & Terminals with Embedded Chips, IoT-Enabled Devices & Sensors, Digital Signage & Display Hardware, Others (Smart Modules & Embedded Components, etc.), By Deployment (On-Premises, Cloud-Based, Field-Based Deployment), By End-User (Banks & Financial Institutions, Independent ATM Deployers, Non-Banking Financial Companies, Corporate & Institutional Bank, Government Institutions, Fintech Companies, Others (Retail, etc.), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: March 2026

- Report ID: 179807

- Number of Pages: 252

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

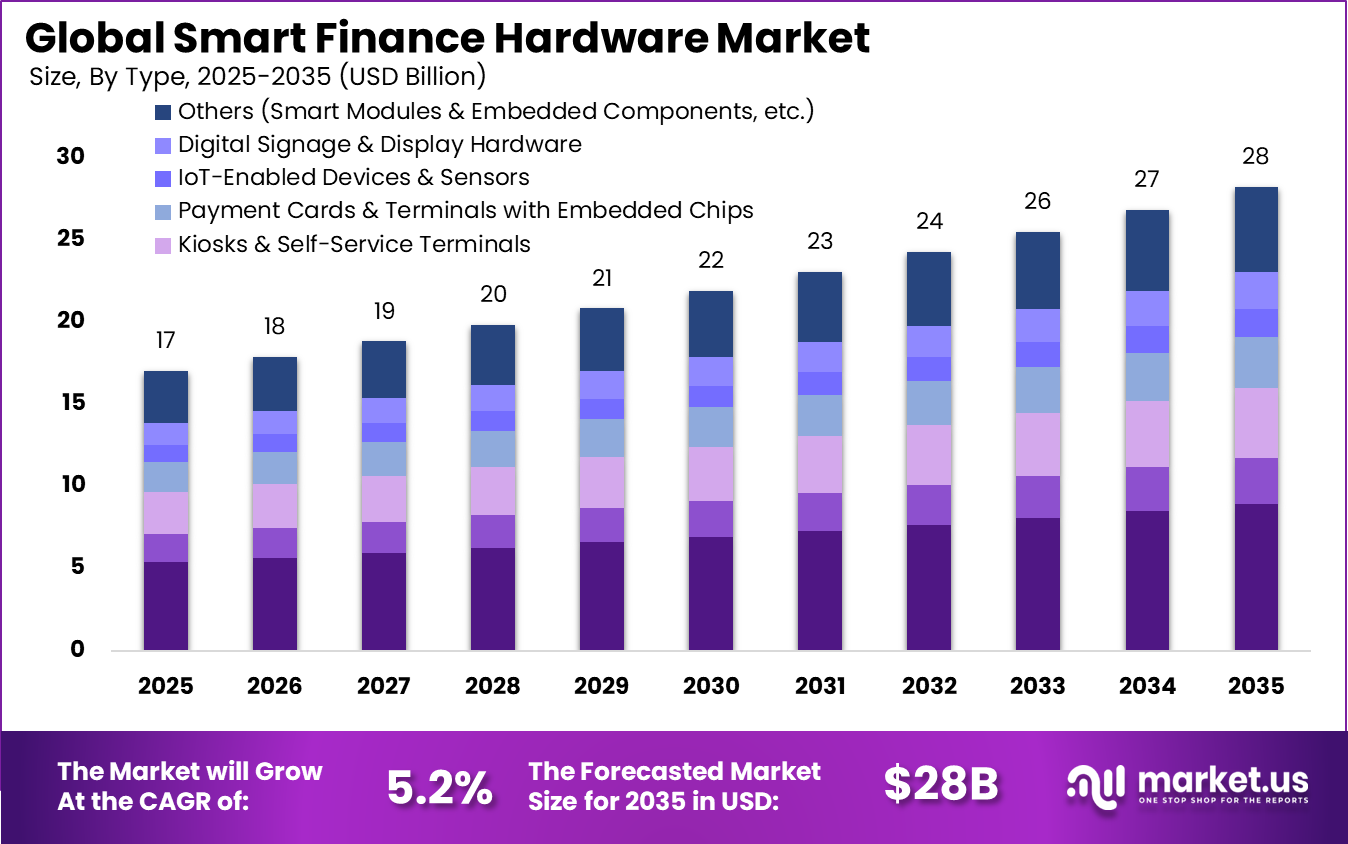

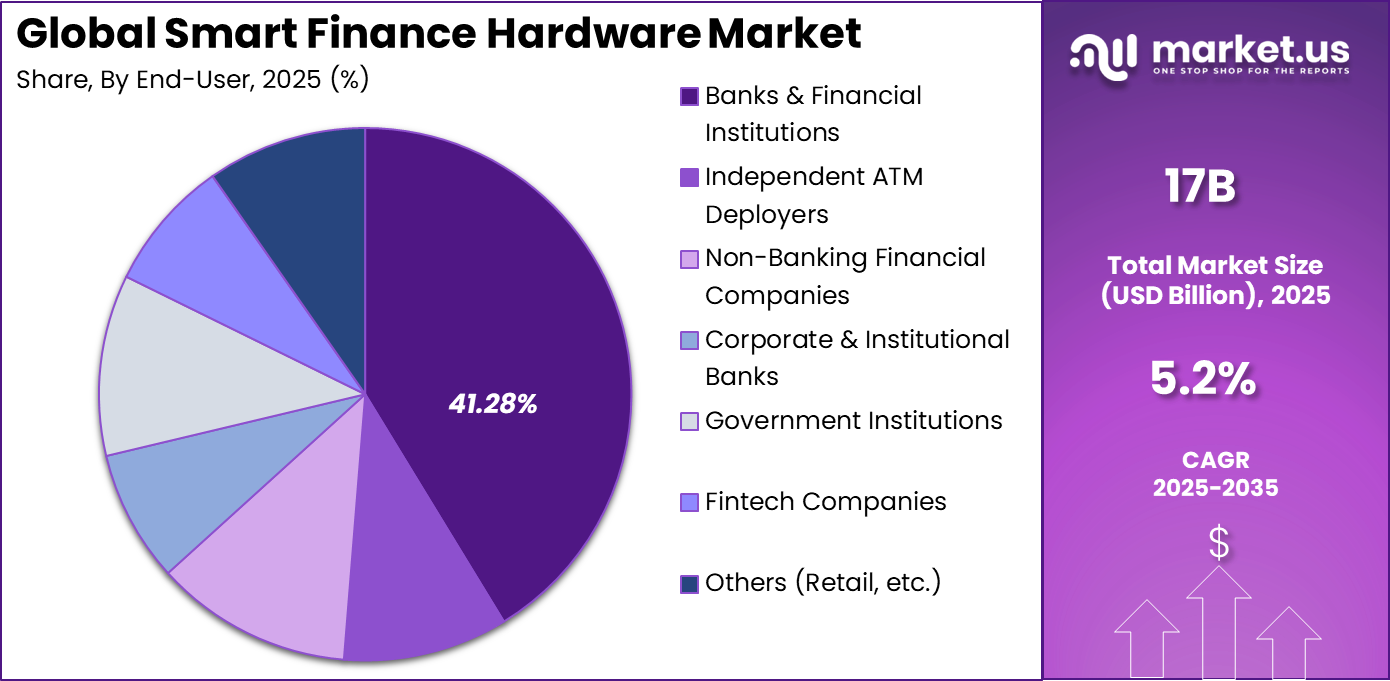

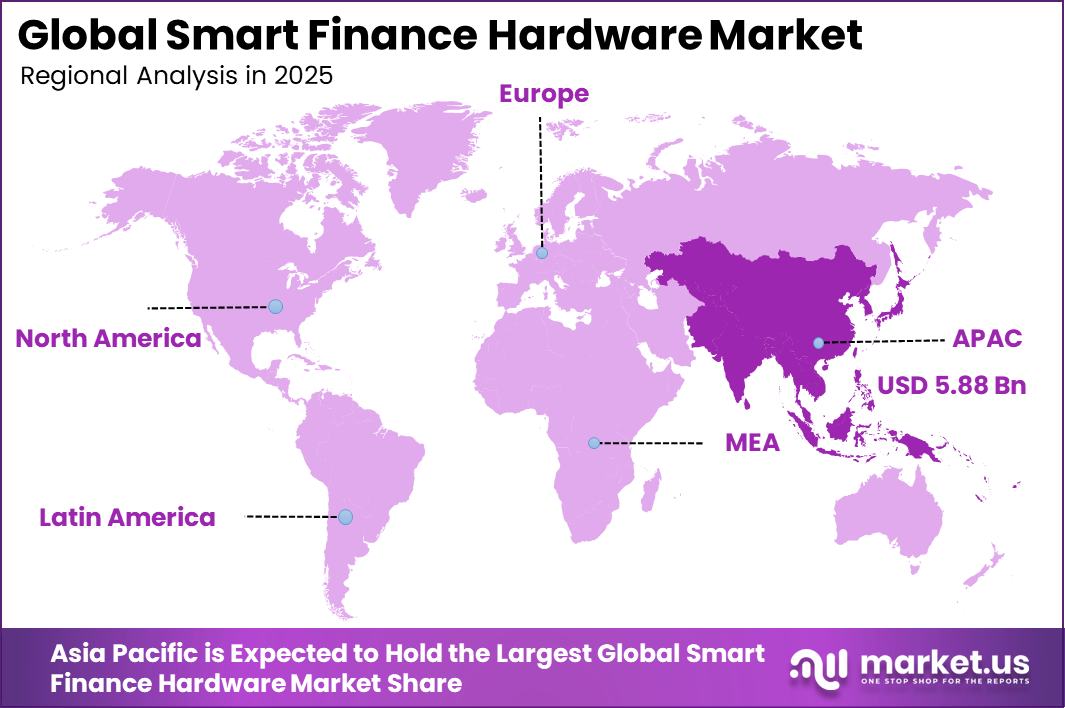

The Global Smart Finance Hardware Market size is expected to be worth around USD 28 billion by 2035, from USD 17 billion in 2025, growing at a CAGR of 5.2% during the forecast period from 2025 to 2035. APAC held a dominant market position, capturing more than a 34.6% share, holding USD 5.88 billion in revenue.

The Smart Finance Hardware Market includes intelligent physical devices used in banking, payments, and financial service environments. These devices combine embedded software, connectivity modules, biometric authentication, and secure transaction processing capabilities. Smart POS terminals, intelligent ATMs, biometric authentication devices, and secure payment kiosks form the core product base. Market demand has been supported by the modernization of financial infrastructure and the transition toward digital payment ecosystems.

Financial institutions are increasingly investing in hardware that integrates with cloud platforms and digital banking systems. Traditional standalone devices are being replaced by connected hardware that enables real time transaction monitoring and fraud detection. As payment volumes increase globally, financial institutions require secure and high performance hardware to manage large transaction loads. The market is therefore shaped by the convergence of secure hardware engineering and financial technology integration.

Contactless payment adoption has reached a high level globally, with more than 75% of face to face transactions now completed through contactless methods. In advanced payment markets such as United Kingdom, Australia, and South Korea, usage levels exceed 90%, reflecting strong infrastructure maturity and consumer acceptance. Worldwide, nearly 140 million active point of sale terminals support this ecosystem, enabling secure and rapid digital transactions across retail, hospitality, and service sectors.

A structural shift is also visible in merchant hardware adoption patterns. Around 25% of micro merchants are bypassing dedicated terminals by using smartphone based acceptance solutions such as Tap to Pay on iPhone developed by Apple Inc., converting mobile devices into payment hardware. At the enterprise level, smart POS systems are typically refreshed every 3 to 4 years to comply with evolving security standards including PCI DSS 6.0, ensuring strong encryption, regulatory alignment, and fraud risk mitigation.

One major driver is the rapid growth of digital payment adoption. Contactless payments, QR based transactions, and mobile wallet usage have increased the need for advanced POS terminals and secure authentication devices. Smart terminals enable multi payment acceptance, including cards, mobile wallets, and biometric verification. As transaction methods diversify, hardware upgrades become necessary to maintain compatibility and security standards.

For instance, in June 2025, Fujitsu shifted strategy by ending its own ATM hardware production by March 2028, partnering with OKI for supply while doubling down on software/services. This frees up focus for digital transformation in finance, like AI and biometrics.

Key Takeaway

- In 2025, Smart POS terminals led the Smart Finance Hardware Market by type, accounting for 31.6% of total share.

- In 2025, On-Premises deployment remained dominant, capturing 58.42% of the market.

- In 2025, Banks and Financial Institutions represented the largest end user segment, contributing 41.28% of overall demand.

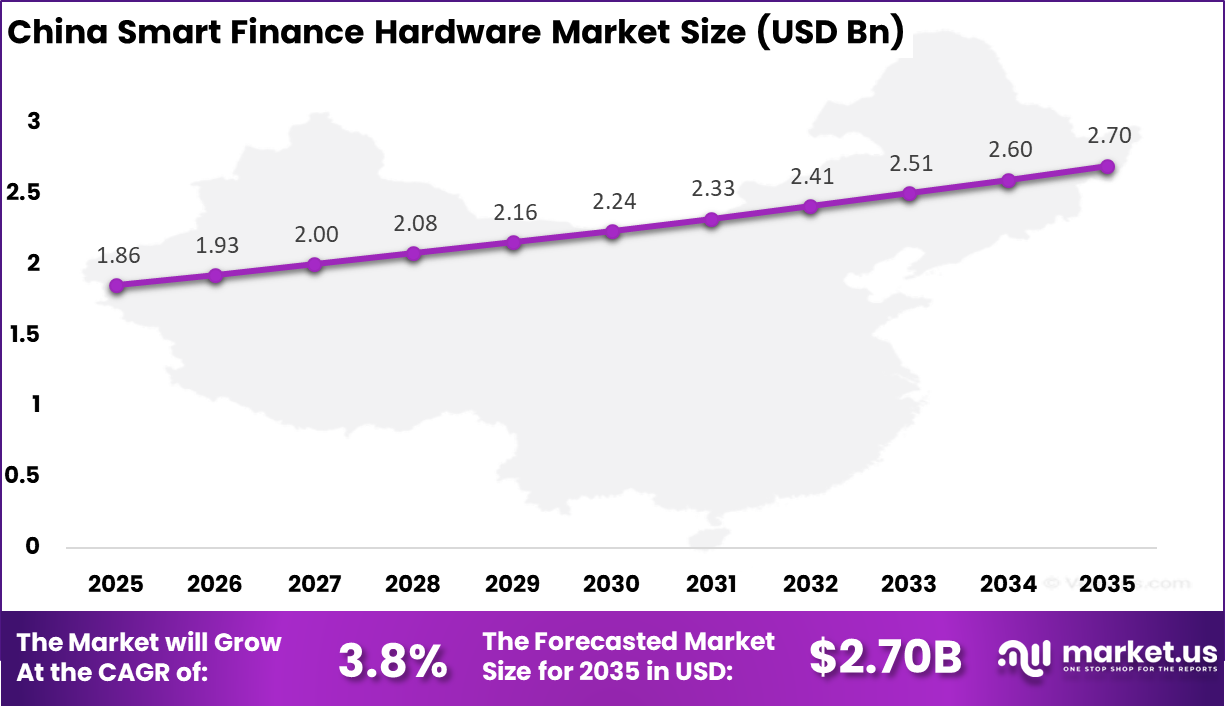

- In 2025, Asia Pacific held a leading regional position with a 34.6% share, while the China market was valued at USD 1.86 billion and recorded a growth rate of 3.8%.

By Type

Smart POS terminals at 31.6% represent the leading hardware category due to widespread merchant deployment. These devices support contactless payments, chip and PIN transactions, and mobile wallet integration. Modern POS systems also include inventory tracking and analytics capabilities. Their multifunctional design makes them essential for retail and service industries.

Adoption is further supported by government initiatives promoting digital payments. As more economies encourage cashless transactions, merchants upgrade traditional terminals to smart connected systems. Continuous innovation in device portability and battery efficiency also enhances adoption across small and medium businesses.

For Instance, in January 2025, Verifone unveiled the Victa series POS portfolio at NRF’25, featuring mobile and countertop models with biometrics. These devices enhance customer interactions and security, helping retailers handle diverse payments seamlessly. The launch targets efficiency in high-volume settings.

By Deployment

On premises deployment at 58.42% reflects strong preference for localized infrastructure control within financial institutions. Banks often require direct oversight of hardware systems due to strict regulatory compliance and data protection standards. On premises systems provide controlled network environments and enhanced security customization.

This deployment model is particularly relevant for high volume banking operations and ATM networks. Institutions managing sensitive financial data prioritize physical and network level control. While cloud connectivity is increasing, on premises architecture remains dominant in critical transaction environments.

For instance, in September 2025, Ingenico rolled out Manage 360, a cloud tool for on-premises device oversight, cutting service costs by up to 75%. It enables real-time updates and diagnostics for payment hardware fleets. Banks gain better control without full cloud shifts.

By End User

Banks and financial institutions at 41.28% lead hardware demand due to their central role in transaction processing. These organizations deploy smart terminals, biometric authentication systems, and secure payment infrastructure across branch networks. Reliability and uptime are critical performance indicators for these buyers.

Digital banking expansion further increases hardware requirements. Even as mobile banking grows, physical transaction points remain necessary for cash services and customer verification. As a result, institutional hardware investments remain stable and strategically important.

For Instance, in December 2025, Diebold Nixdorf launched DN Series 300 and 350 cash dispensers for bank branches. With high-capacity modules, they cut costs and boost availability for self-service banking. The on-site hardware fits secure financial environments perfectly.

Regional Insights

Asia Pacific at 34.6% benefits from rapid digital payment adoption and financial inclusion initiatives. Countries in the region are investing heavily in electronic payment infrastructure to reduce reliance on cash transactions. Retail digitization and fintech expansion further stimulate hardware demand.

For instance, in January 2026, PAX Technology expanded Asia Pacific dominance with its Android-based smart POS terminals featuring 5G connectivity and biometric payments. Deployed across 20+ countries, these terminals drive China’s fintech hardware supremacy in high-volume retail and hospitality sectors.

China’s valuation of USD 1.86 Bn and 3.8% CAGR reflects infrastructure modernization and steady replacement cycles. While growth is moderate compared to software driven markets, stable financial network expansion supports long term hardware demand across the region.

For instance, in February 2026, Nexgo strengthened China’s smart finance hardware lead by introducing compact payment kiosks with QR code scanning and real-time fraud detection. These solutions dominate Asia Pacific merchant adoption, powering seamless digital transactions in emerging markets.

Investment and Business Benefits

Investors focus on manufacturers of energy-efficient devices, with 65% of new hardware using low power for remote locations. Collaborations between banks and technology firms create opportunities for custom solutions in expanding regions. Scalable IoT kits for fintech startups offer high potential, as adoption continues to grow rapidly and hardware demand increases across various markets.

Smart finance devices enhance operational efficiency by automating checks, allowing staff to focus on customer service. Trials show a 30% increase in customer satisfaction, and maintenance costs are reduced by 25% due to self-diagnosing features. Long-term advantages include improved trust and security, as these devices reduce the likelihood of data breaches and ensure safe financial transactions.

Emerging Trends Analysis

One emerging trend is the integration of biometric authentication within smart POS and banking hardware. Fingerprint and facial recognition modules enhance transaction verification security. These technologies reduce dependency on traditional PIN based authentication.

Another trend is modular hardware design. Manufacturers are developing upgradeable devices that allow component replacement without full system overhaul. This approach reduces long term operational costs and extends hardware lifecycle.

Growth Factors Analysis

The global shift toward cashless economies is a major growth factor. As digital payment volumes increase, merchant and banking hardware infrastructure must expand accordingly. Financial inclusion programs also require deployment of secure devices in underserved regions.

Another growth factor is the integration of hardware with fintech ecosystems. Collaboration between banks and fintech companies often requires compatible hardware infrastructure. This interoperability encourages device modernization.

Key Market Segments

By Type

- Smart POS (Point of Sale) Terminals

- Smart ATMs (Automated Teller Machines)

- Kiosks & Self-Service Terminals

- Payment Cards & Terminals with Embedded Chips

- IoT-Enabled Devices & Sensors

- Digital Signage & Display Hardware

- Others (Smart Modules & Embedded Components, etc.)

By Deployment

- On-Premises

- Cloud-Based

- Field-Based Deployment

By End-User

- Banks & Financial Institutions

- Independent ATM Deployers

- Non-Banking Financial Companies

- Corporate & Institutional Banks

- Government Institutions

- Fintech Companies

- Others (Retail, etc.)

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Drivers

Growth of Digital and Contactless Payments

The rise of digital and contactless payments is driving the adoption of smart finance hardware. Customers now prefer tapping cards or using mobile wallets instead of handling cash, and merchants are upgrading to devices that support these payment methods. Smart terminals streamline transactions, making payments faster and more secure for both businesses and consumers.

Financial institutions are also encouraged by initiatives promoting digital payments and financial inclusion. Improved infrastructure and internet connectivity support wider adoption, prompting banks and retailers to invest in modern hardware. These devices help deliver smoother operations and meet the growing expectations of tech-savvy customers.

For instance, in February 2026, Ingenico rolled out the next-generation AXIUM payment device family at Paytech 2026, built for smooth contactless and digital payments across mobile and countertop setups. Running on Android 14 with PCI PTS v7 security, it enables merchants to handle quick taps effortlessly.

Restraint

High Initial Costs and Security Concerns

High upfront costs for purchasing, installing, and integrating smart finance hardware are a significant restraint. Small businesses and some financial institutions may struggle to justify the investment, especially when older systems are still operational. Training staff to manage new devices adds to the overall expense and complexity.

Security and data privacy concerns further limit adoption. Connected devices handling sensitive information can be vulnerable to cyber threats, and organisations must implement strict security measures. Regulatory requirements for safeguarding financial data increase the workload, making some companies cautious about deploying advanced hardware widely.

For instance, in September 2025, PAX Technology highlighted its security edge with 86 PCI-certified models, including top PTS 6.x standards and tamper-proof modules. While strong protection draws users, the heavy focus on certifications and dedicated processors shows upfront costs for top security in Android SmartPOS. It reassures but weighs on smaller setups.

Opportunities

Expansion in Emerging Economies

Emerging markets offer significant opportunities for smart finance hardware as digital banking expands and financial inclusion improves. Banks and fintech providers are deploying smart POS devices and biometric systems to serve communities with limited access to traditional banking, bringing digital transactions to new users.

As smartphone use grows and infrastructure develops, demand for affordable, adaptable hardware is increasing. Manufacturers and service providers can offer solutions tailored to these regions, creating new customer bases while supporting broader financial inclusion goals and enabling secure, convenient payment systems.

For instance, in January 2025, Hitachi partnered with AEON Credit Service in Southeast Asia to drive financial inclusion using digital finance tech like mobile banking and microloans for unbanked groups. Their systems embed services in e-wallets, reaching lower-income users through mini-apps. This expands smart hardware reach in fast-growing economies ready for tech leaps.

Challenges

Integration and Operational Complexity

Integrating smart finance hardware with existing legacy systems is a major challenge. Many financial institutions still rely on older technology platforms that are not easily compatible with advanced devices. This can cause delays in deployment and require extra resources to ensure accurate and secure operation.

Ongoing maintenance and technical support add further complexity. Smart devices need regular updates, security patches, and monitoring to function properly. Organisations without strong technical expertise may struggle to manage these requirements, slowing adoption and increasing the burden on internal IT teams.

For instance, in January 2026, NCR shifted to a cloud-native platform model, facing integration challenges from hardware to service revenue amid legacy system overhauls. Tariff impacts complicate device additions, requiring careful testing to maintain service flow. This tests operational tweaks for unified payments without disrupting daily banking ops.

Key Players Analysis

The Smart Finance Hardware Market is characterized by a mix of established global manufacturers and specialized technology providers. Diebold Nixdorf, NCR Corporation, and Hyosung TNS maintain strong positions in ATM systems and integrated banking terminals. Their portfolios focus on secure cash handling, self service banking, and digital transaction enablement. Continuous product upgrades and software integration capabilities support their long term competitiveness in retail banking and financial institutions.

Payment terminal specialists such as PAX Technology Inc., Ingenico Group, and VeriFone Systems Inc. play a critical role in smart POS infrastructure. These companies emphasize contactless payments, mobile wallet compatibility, and embedded security features. Asian manufacturers including GRG Banking Equipment Co. Ltd. and Hitachi Channel Solutions Corp. are expanding global distribution networks. Their growth is supported by demand for advanced cash recyclers and branch automation solutions.

Technology component and connectivity providers strengthen the broader ecosystem. Intel Corporation, Microchip Technology Inc., and Digi International Inc. supply processors, embedded systems, and secure communication modules. Firms such as Fujitsu, AURES Group, and emerging players including Nexgo, Castles Technology, and InHand Networks focus on compact POS devices and IoT enabled banking hardware.

Top Key Players in the Market

- Diebold Nixdorf

- NCR Corporation

- Hyosung TNS

- GRG Banking Equipment Co. Ltd.

- PAX Technology Inc.

- Ingenico Group

- VeriFone Systems Inc.

- Hitachi Channel Solutions Corp.

- OKI Electric Industry Co., Ltd.

- Castles Technology Co., Ltd.

- Nexgo (SZ Xinguodu Technology)

- AURES Group

- Fujitsu

- Digi International Inc.

- IMS Evolve

- InHand Networks

- Microchip Technology Inc.

- com

- Intel Corporation

- Miles Technologies

- Others

Recent Developments

- In February 2026, Ingenico unveiled the next-gen AXIUM payment device family and the Ingenico 360 cloud platform at Paytech 2026. Live across Europe, the Americas, and APAC, it promises enterprise-grade payments with AI-ready hardware for massive rollouts.

- In January 2026, OKI Electric Industry partnered with OpenSys to launch the Horizon Series self-service banking platform. Featuring cash recycling, biometrics, and anti-skimming, it’s built for efficient branches in digital banking shifts. Denis Koay notes it cuts costs without scrapping existing infrastructure.

Report Scope

Report Features Description Market Value (2025) USD 17.0 Bn Forecast Revenue (2035) USD 28.0 Bn CAGR (2026-2035) 5.2% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Type (Smart POS (Point of Sale) Terminals, Smart ATMs (Automated Teller Machines), Kiosks & Self-Service Terminals, Payment Cards & Terminals with Embedded Chips, IoT-Enabled Devices & Sensors, Digital Signage & Display Hardware, Others (Smart Modules & Embedded Components, etc.), By Deployment (On-Premises, Cloud-Based, Field-Based Deployment), By End-User (Banks & Financial Institutions, Independent ATM Deployers, Non-Banking Financial Companies, Corporate & Institutional Bank, Government Institutions, Fintech Companies, Others (Retail, etc.) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Diebold Nixdorf, NCR Corporation, Hyosung TNS, GRG Banking Equipment Co., Ltd., PAX Technology Inc., Ingenico Group, VeriFone Systems Inc., Hitachi Channel Solutions Corp., OKI Electric Industry Co., Ltd., Castles Technology Co., Ltd., Nexgo (SZ Xinguodu Technology), AURES Group, Fujitsu, Digi International Inc., IMS Evolve, InHand Networks, Microchip Technology Inc., OptConnect.com, Intel Corporation, Miles Technologies, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Smart Finance Hardware MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Smart Finance Hardware MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Diebold Nixdorf

- NCR Corporation

- Hyosung TNS

- GRG Banking Equipment Co. Ltd.

- PAX Technology Inc.

- Ingenico Group

- VeriFone Systems Inc.

- Hitachi Channel Solutions Corp.

- OKI Electric Industry Co., Ltd.

- Castles Technology Co., Ltd.

- Nexgo (SZ Xinguodu Technology)

- AURES Group

- Fujitsu

- Digi International Inc.

- IMS Evolve

- InHand Networks

- Microchip Technology Inc.

- com

- Intel Corporation

- Miles Technologies

- Others

Our Clients

- 179807

- March 2026