Quick Navigation

Report Overview

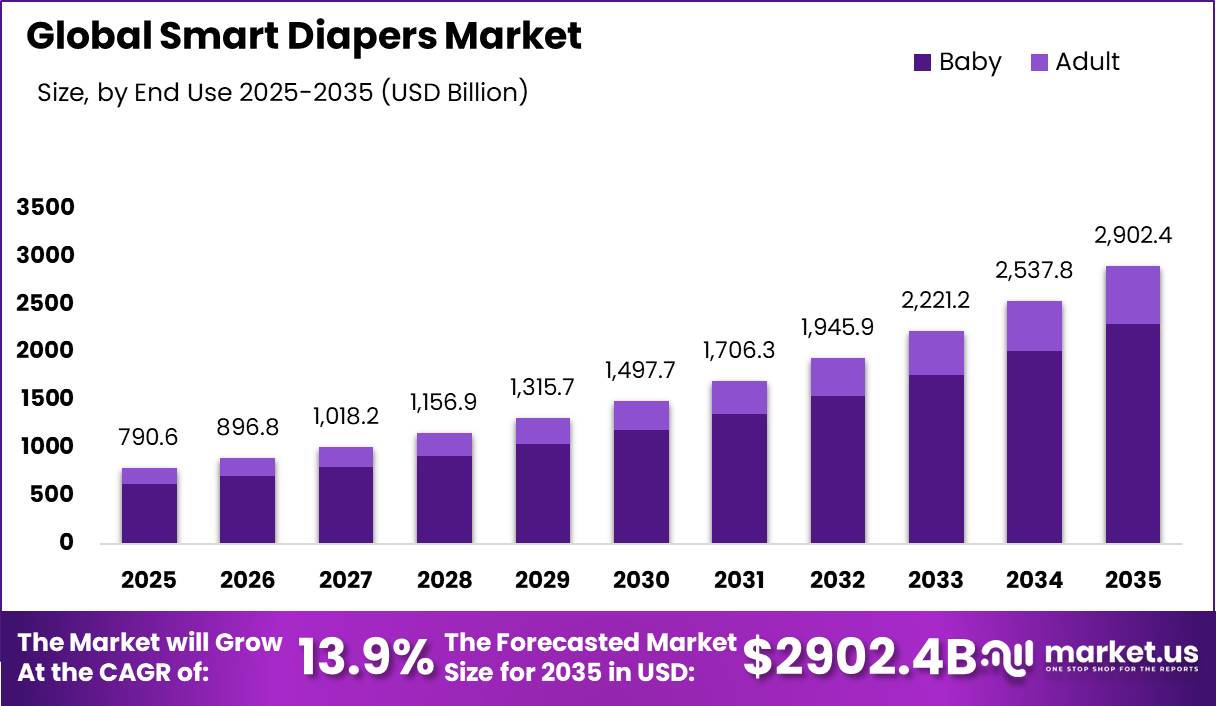

Global Smart Diapers Market size is expected to be worth around USD 2,902.4 Billion by 2035 from USD 790.6 Billion in 2025, growing at a CAGR of 13.9% during the forecast period 2026 to 2035.

Smart diapers are sensor-embedded absorbent products that detect moisture, track urination patterns, and transmit caregiver alerts through wireless protocols. The market spans two primary end uses, baby care and adult continence management, and operates across two core technology platforms, RFID-based monitoring and Bluetooth-connected sensor systems. Distribution runs through both online retail and offline healthcare supply channels.

Key Takeaways

- Smart Diapers Market size in 2025 stands at USD 790.6 Billion, forecast to reach USD 2,902.4 Billion by 2035 at a CAGR of 13.9%.

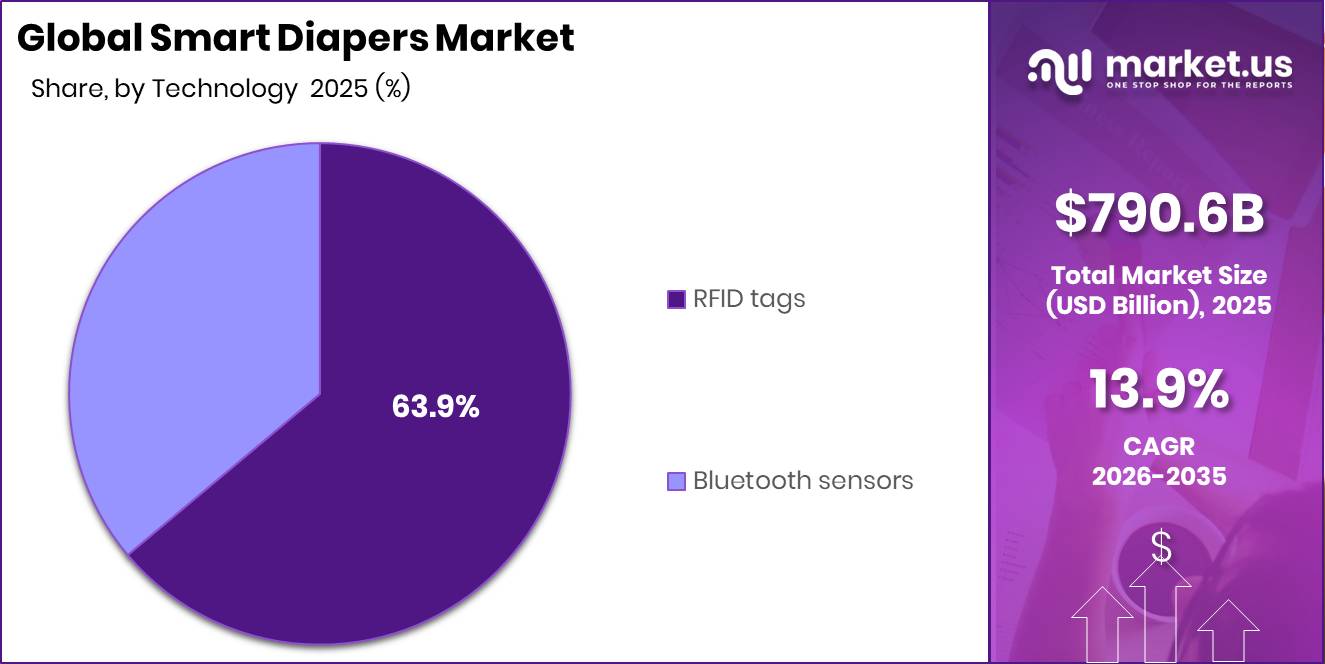

- RFID tags dominate the Technology segment with a 63.9% share in 2025.

- Baby end use leads the End Use segment with a 79.3% share in 2025.

- Online channels hold 59.7% of distribution channel share in 2025.

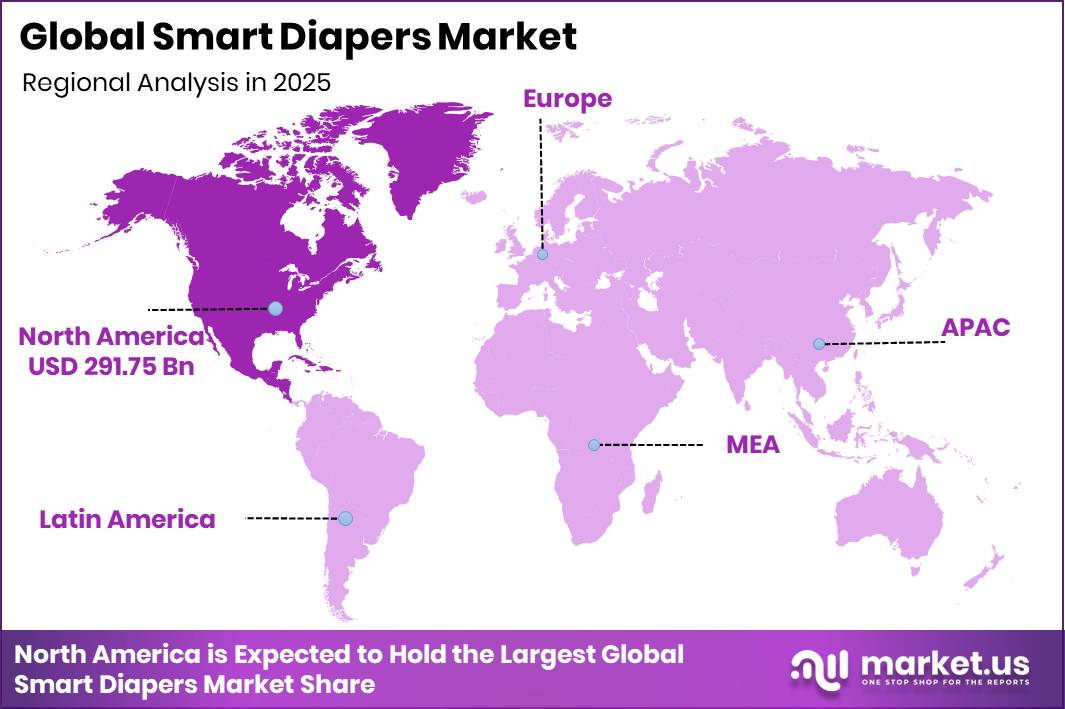

- North America leads all regions with a 36.9% market share, valued at USD 291.75 Billion in 2025.

Connected healthcare infrastructure has become a structural enabler for smart diaper adoption. Nursing homes and long-term care facilities now deploy automated urine-volume monitoring systems at scale, replacing manual rounding with sensor-driven workflows. As reported by JMIR Formative Research, a 2024 smart diaper validation study enrolled 97 older adults across three nursing homes for one month. This trial scale signals that institutional procurement is moving from pilot to deployment-ready.

According to JMIR Formative Research, the study participants had a mean age of 86.5 years, confirming that the primary institutional user profile centers on high-dependency elderly adults. Data from NCBI shows that more than 50% of long-term care facility residents have urinary or fecal incontinence. This prevalence rate positions smart diapers not as a premium add-on but as a direct clinical response to a documented care burden.

Regulatory pressure around data privacy in wireless health monitoring is shaping product development timelines and raising compliance costs. This creates a two-tier market structure, with well-capitalized manufacturers building compliant sensor platforms and smaller entrants facing higher barriers to institutional sales. From January to December 2022, 97 elderly patients with at least one chronic disease were monitored across three nursing homes using a smart diaper system, providing early longitudinal evidence that supports institutional purchasing decisions.

Technology Analysis

RFID Tags dominates with 63.9% due to passive sensing and low per-unit cost.

In 2025, RFID Tags held a dominant market position in the By Technology segment of the Smart Diapers Market, with a 63.9% share. RFID tags require no battery and embed directly into diaper substrate during manufacturing. From January to December 2022, smart diaper systems using sensor monitoring tracked 97 elderly patients across three nursing homes. This real-world deployment evidence strengthens institutional buyer confidence in RFID-based platforms over power-dependent alternatives.

Bluetooth Sensors hold the remaining 36.1% of the Technology segment and serve a different use case from RFID platforms. Bluetooth-connected systems enable two-way data transmission and direct integration with caregiver dashboards and mobile applications. As reported by PMC, a hospital-based study recorded 390 urination episodes from 30 patients using a Bluetooth-connected smart diaper system. This volume of tracked events shows Bluetooth sensors can generate clinically actionable datasets at a per-patient level.

End Use Analysis

Baby dominates with 79.3% due to high diaper usage frequency in infant care.

In 2025, Baby held a dominant market position in the By End Use segment of the Smart Diapers Market, with a 79.3% share. Infant care generates high diaper consumption per household per week, creating strong volume-driven revenue across both premium and standard product tiers. This segment benefits from parental willingness to pay for real-time wetness alerts, particularly among first-time buyers in higher-income brackets.

Adult end use accounts for 20.7% of the End Use segment and concentrates heavily in institutional eldercare settings. JMIR Formative Research data shows 89% of smart diaper study participants had dementia and 89% had two or more comorbidities, defining the clinical complexity that adult-focused smart diapers must address. This co-morbidity profile means adult products require caregiver dashboard integration and alert escalation features that infant products do not.

Distribution Channel Analysis

Online dominates with 59.7% due to subscription convenience and repeat purchase behavior.

In 2025, Online held a dominant market position in the By Distribution Channel segment of the Smart Diapers Market, with a 59.7% share. E-commerce platforms enable direct-to-consumer subscription models that reduce churn and improve unit economics for manufacturers. Caregiver audiences, particularly parents and home eldercare managers, prefer digital procurement for convenience and product comparison access.

Offline distribution retains the remaining share and serves two distinct buyer types, institutional procurement teams and in-store retail consumers. Hospitals, nursing homes, and long-term care facilities often require vendor contracts and bulk supply agreements that bypass online channels entirely. As a result, Ontex and Henkel expanded the European rollout of the Orizon smart incontinence solution in March 2026, targeting institutional offline buyers through care facility partnerships.

Key Market Segments

By Technology

- RFID Tags

- Bluetooth Sensors

By End Use

- Baby

- Adult

By Distribution Channel

- Online

- Offline

Market Dynamics

Market Opportunity Analysis - Underserved eldercare regions and niche sensor licensing channels offer entry points for focused players

The Adult end use segment holds only 20.7% of current market share despite representing the highest-frequency clinical user in institutional settings. This underrepresentation signals a structural misalignment between product portfolio focus and actual care demand. Vendors that redirect product development and sales toward adult continence monitoring in nursing homes and rehabilitation centers can capture share ahead of competitors still anchored to infant-first positioning.

Offline distribution retains a significant share of procurement despite online channels leading at 59.7%. Institutional buyers in hospitals and long-term care facilities operate through contract procurement systems that bypass e-commerce entirely. New entrants that build direct institutional sales capabilities and comply with bulk supply contract requirements can access a buyer segment that online-first competitors structurally cannot serve.

Latin America and the Middle East and Africa remain at early adoption stages, where private care facilities in urban centers represent the lowest-competition entry points available to smart diaper vendors. GCC countries are investing in smart hospital infrastructure, creating selective procurement opportunities for vendors that meet local compliance standards. This geographic gap between current revenue concentration in North America and Europe and the emerging institutional buildout elsewhere defines a medium-term market share capture window.

Bluetooth Sensors account for 36.1% of the Technology segment and remain underutilized relative to their clinical data generation capacity. Vendors that pair Bluetooth-enabled systems with caregiver dashboard analytics and EHR integration can differentiate on workflow value rather than unit price alone. This positions Bluetooth-focused platforms as a premium institutional offering that RFID-only competitors cannot replicate without sensor architecture changes.

Technology and Innovation Landscape - Battery-free sensors, AI analytics, and printed flexible circuits reshape the smart diaper competitive edge

Bluetooth Low Energy and battery-free sensor architectures are redefining design priorities for smart diaper manufacturers. In January 2026, Asahi Kasei Microdevices presented a battery-free smart diaper at CES 2026 that generates power from urine using conductive materials embedded in the diaper substrate. This eliminates battery replacement as a cost and maintenance variable, lowering the total operational cost for institutional buyers and removing a key procurement objection in nursing home settings.

AI-powered predictive analytics for urination pattern tracking and care scheduling represent the next layer of clinical differentiation. Vendors that integrate machine learning models into caregiver dashboard platforms can shift the product value proposition from reactive alert to proactive care scheduling. This capability is particularly valuable in facilities with high patient-to-caregiver ratios, where predictive scheduling directly reduces labor demand per patient-day.

Colorimetric and printed flexible sensors are creating a new cost tier for disposable smart diaper applications. These sensors use printed circuit methods rather than rigid embedded electronics, enabling lower per-unit manufacturing costs without sacrificing moisture detection accuracy. Commercialization of this architecture opens the addressable market beyond premium institutional buyers to mid-tier care facilities and price-sensitive consumer segments that sensor-embedded diapers currently cannot reach.

Smartphone-based caregiver dashboards for multi-patient monitoring are consolidating smart diaper data streams into single-operator interfaces. This technology reduces the per-caregiver cognitive load of monitoring multiple patients simultaneously and improves alert response time at the facility level. Vendors that build multi-patient dashboard capability into their sensor platform can position their product as a facility management tool rather than a single-patient device, supporting higher-value institutional contracts.

Drivers

Aging-led continence demand is the strongest structural driver for smart diapers because the largest long-term user base is increasingly older adults rather than infants. WHO projects the population aged 60 and older to rise from 1.0 billion in 2020 to 1.4 billion by 2030 and 2.1 billion by 2050. The 80-and-above population will reach 426 million by 2050. This demographic shift positions eldercare facilities as the most reliable volume buyers for sensor-embedded continence products over the next decade.

As mobility limitations, dementia, stroke-related disabilities, and urinary incontinence become more prevalent with age, demand for continuous continence monitoring rises accordingly. Older adults require more frequent caregiver intervention than infant users, making sensor-driven monitoring economically justified for care operators. Adoption is most pronounced in Japan, Europe, North America, and South Korea, where population aging and caregiver shortages are pushing facilities toward automated monitoring solutions.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

| Aging-led continence demand | +2.7% | Japan, EU, North America, Korea | Long term (≥ 4 years) |

| Nursing labor productivity push | +2.2% | North America core, EU, Japan, GCC | Short term (≤ 2 years) |

| Low-cost sensor miniaturization | +1.8% | Global OEM hubs, APAC manufacturing corridors | Medium term (2-4 years) |

| Home-based eldercare expansion | +1.9% | U.S., Canada, EU, urban Asia | Medium term (2-4 years) |

| Clinical proof for smart monitoring | +1.6% | Hospitals and LTC facilities globally | Short term (≤ 2 years) |

| Premium infant monitoring demand | +1.1% | North America, EU, affluent APAC | Medium term (2-4 years) |

Restraints

Infant birth decline is a structural challenge for smart diaper producers targeting newborns and young children as their primary user base. In the United States, 3,606,400 births were recorded in 2025, representing a 1% decline from 2024, while the general fertility rate fell to 53.1 births per 1,000 women aged 15 to 44. Similar low-fertility trends across Europe and East Asia reduce the number of potential new users entering the market each year, tightening the infant volume ceiling for manufacturers.

Higher product prices and uncertainty around the necessity of sensor-enabled diapers further constrain adoption among mainstream consumers. Since smart diaper adoption remains concentrated among higher-income households, a shrinking infant population raises customer acquisition costs and limits volume expansion. These demographic pressures are encouraging manufacturers to shift focus toward adult continence care, eldercare facilities, and home-healthcare applications where long-term demand fundamentals are stronger.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing adoption barrier | -2.3% | North America, EU, APAC urban markets | Medium term (2-4 years) |

| Limited reimbursement pathways | -1.9% | U.S., EU, Japan, developed APAC | Long term (≥ 4 years) |

| Care-system integration gap | -1.6% | Hospitals, LTC, home-care markets globally | Medium term (2-4 years) |

| Infant birth decline exposure | -1.4% | North America, EU, East Asia | Long term (≥ 4 years) |

| Disposable sensor cost burden | -1.3% | Global OEM hubs, cost-sensitive markets | Medium term (2-4 years) |

| Clinical validation narrowness | -1.1% | Global regulated healthcare markets | Short term (≤ 2 years) |

Challenges

Medical device data privacy and wireless health monitoring compliance requirements are increasing product development costs for smart diaper manufacturers. Healthcare-grade wireless products must meet jurisdiction-specific data handling standards before institutional buyers can approve procurement. This compliance overhead disproportionately affects smaller sensor-focused entrants who lack dedicated regulatory affairs teams, giving larger incumbents a structural cost advantage in institutional sales cycles.

High unit costs of sensor-embedded disposable diapers continue to limit mass-market consumer adoption outside premium household segments. Data from NCBI shows that more than 50% of long-term care facility residents have urinary or fecal incontinence, confirming that the addressable clinical need far exceeds current product penetration. This gap between clinical need and price-accessible supply represents the central commercial challenge that manufacturers must solve to unlock volume growth beyond high-income early adopters.

Care-system integration gaps create a third layer of friction. Smart diaper data streams must connect with electronic health record platforms to generate clinical value at the point of care. Without seamless EHR connectivity, nursing staff must manually log sensor alerts into separate systems, reducing workflow efficiency and weakening the institutional ROI case that drives procurement decisions in hospitals and long-term care settings.

Opportunities

Eldercare continence platforms are emerging as a major opportunity as aging populations increase pressure on long-term care systems. WHO projects the global population aged 60 and older to grow from 1.0 billion in 2020 to 1.4 billion by 2030, reaching 2.1 billion by 2050. The UN estimates one in six people worldwide will be over 65 by 2050. Smart continence platforms that combine predictive bladder monitoring and caregiver alerts can help facilities reduce manual checks by 20 to 35%.

These efficiency gains can improve caregiver productivity, patient comfort, and resource utilization across nursing homes and assisted living facilities. Adoption potential is particularly strong in Japan, North America, Europe, and South Korea, where aging demographics and healthcare workforce shortages are most pronounced. This creates a commercially viable entry point for vendors who can demonstrate measurable staffing cost reductions within a single facility trial period.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Eldercare continence platforms | +2.8% | Japan, North America, EU, Korea | Short term (≤ 2 years) |

| Hospital workflow automation | +2.1% | North America core, EU, GCC, developed APAC | Medium term (2-4 years) |

| Home-care subscription bundles | +1.9% | U.S., Canada, EU, urban China | Medium term (2-4 years) |

| Reimbursement-led clinical adoption | +1.7% | U.S., Germany, Japan, Nordics | Long term (≥ 4 years) |

| Infant wellness analytics layer | +1.4% | North America, EU, affluent APAC | Medium term (2-4 years) |

| Sensor-IP and OEM licensing | +1.6% | Global OEM hubs, APAC manufacturing corridors | Short term (≤ 2 years) |

Regional Analysis

North America Dominates the Smart Diapers Market with a Market Share of 36.9%, Valued at USD 291.75 Billion

North America leads the Smart Diapers Market because of its advanced connected healthcare infrastructure, high institutional adoption in long-term care facilities, and strong consumer spending on premium infant care products. The United States concentrates the majority of regional revenue, driven by nursing home procurement programs and an established e-commerce supply chain for direct-to-consumer diaper subscriptions.

Europe holds a structurally significant position, supported by aging demographics across Germany, France, Italy, and the Nordics, where eldercare spending is publicly funded and continence care is embedded in care protocols. In March 2026, Ontex and Henkel expanded the European rollout of the Orizon smart incontinence solution using conductive-ink moisture sensors and reusable wearable devices. This deployment signals that institutional procurement in Europe is accelerating beyond pilot-stage activity.

Asia Pacific represents a fast-expanding region driven by Japan’s acute eldercare labor shortage and China’s urban parental market for premium infant products. Japan’s care facility density and caregiver-to-patient ratio constraints make it the strongest near-term institutional buyer in the region. South Korea and Australia show emerging adoption, supported by government investment in digital health infrastructure for aging populations.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Procter and Gamble commands scale advantages in the smart diaper space through its global manufacturing footprint and established retail distribution across more than 180 markets. Its capacity to embed sensor technology into high-volume diaper lines lowers per-unit sensor costs. As reported by JMIR Formative Research, smart diaper systems achieved a Pearson correlation of 0.971 between sensor measurements and actual urine weight, validating the clinical accuracy standard that large-scale producers must meet.

Opro9 positions itself as a specialized smart diaper technology provider focused on institutional eldercare monitoring rather than mass-market retail. This narrower focus allows faster product iteration for nursing home procurement requirements. Figures from JMIR Formative Research show accuracy reaching a Pearson coefficient of 0.990 among male participants and 0.969 among female participants. In March 2026, Orizon data showed smart continence solutions can save up to eight caregiver working hours per resident per month, reinforcing the institutional ROI case that Opro9-style specialists use to justify premium pricing.

Key Players

- Procter and Gamble

- Opro9

- Ontex BV

- SINOPULSAR

- Essity Aktiebolag (publ)

- Pixie Scientific

- Simavita (Smartz AG)

- ElderSens

- Abena Holding A/S

Recent Developments

- September 2025 – Monit Corp. officially launched the MECS PRO AI-IoT smart diaper care system for institutional elderly-care facilities, expanding its smart incontinence monitoring portfolio with a solution purpose-built for nursing home deployment.

- January 2026 – Asahi Kasei Microdevices presented an updated battery-free smart diaper solution at CES 2026 that generates power from urine using conductive materials embedded directly in the diaper substrate.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 790.6 Billion |

| Forecast Revenue (2035) | USD 2,902.4 Billion |

| CAGR (2026-2035) | 13.9% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Technology (RFID Tags, Bluetooth Sensors), By End Use (Baby, Adult), By Distribution Channel (Online, Offline) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Procter and Gamble, Opro9, Ontex BV, SINOPULSAR, Essity Aktiebolag (publ), Pixie Scientific, Simavita (Smartz AG), ElderSens, Abena Holding A/S |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |