Service Topology Discovery Market By Component (Software, Services), By Deployment Mode (On-Premises, Cloud), By Application (Network Management, IT Operations, Security and Compliance, Others), By Organization Size (Large Enterprises, Small and Medium Enterprises), By End-User (BFSI, Healthcare, IT and Telecommunications, Retail, Manufacturing, Government, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2026-2035

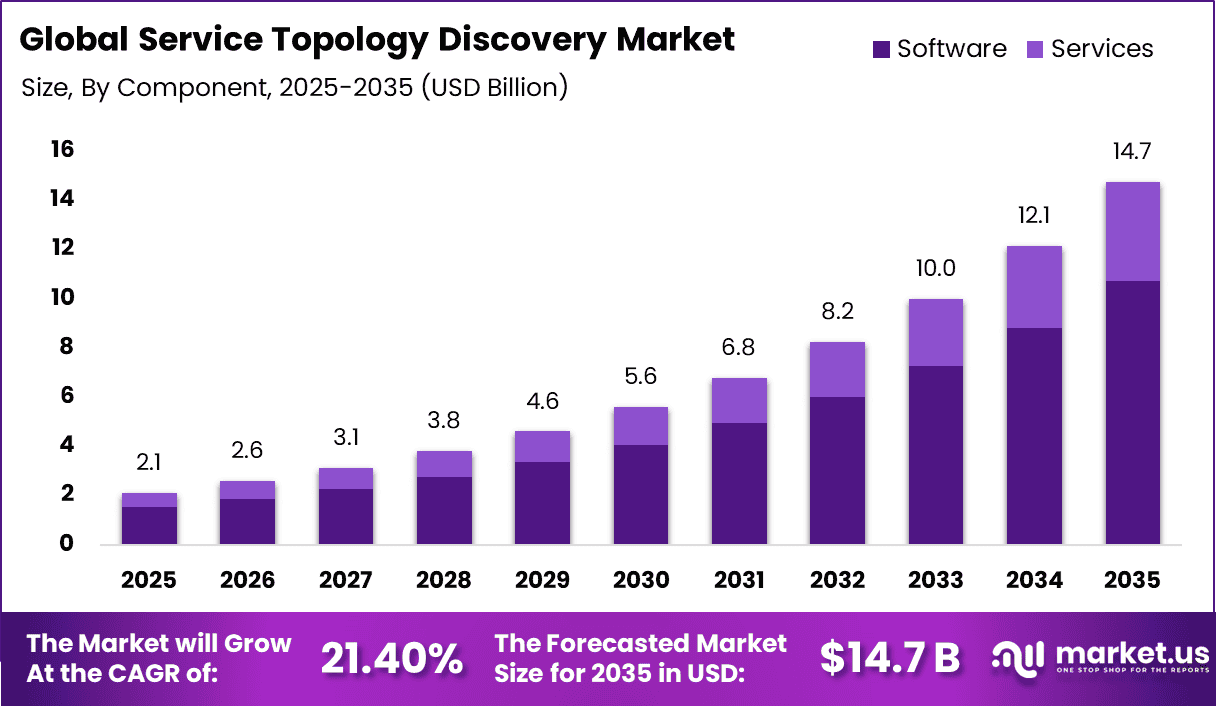

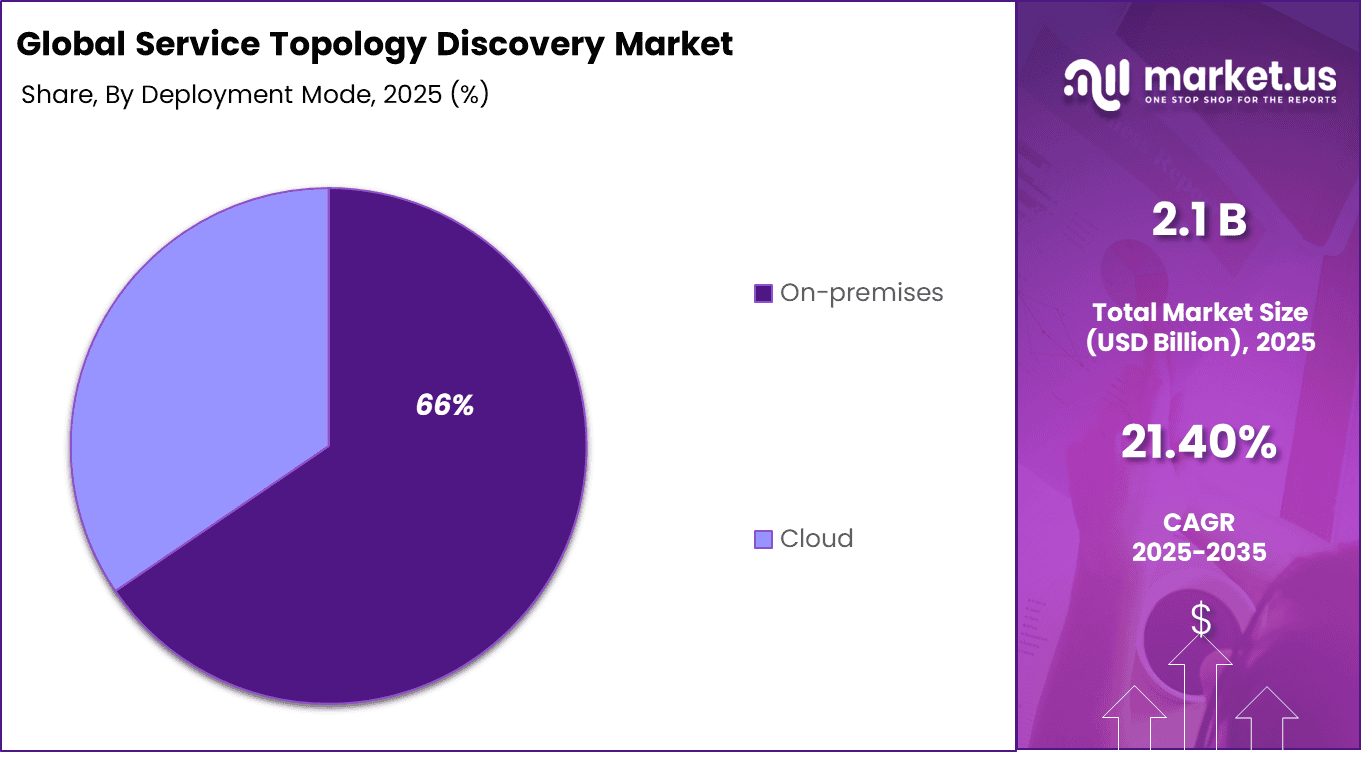

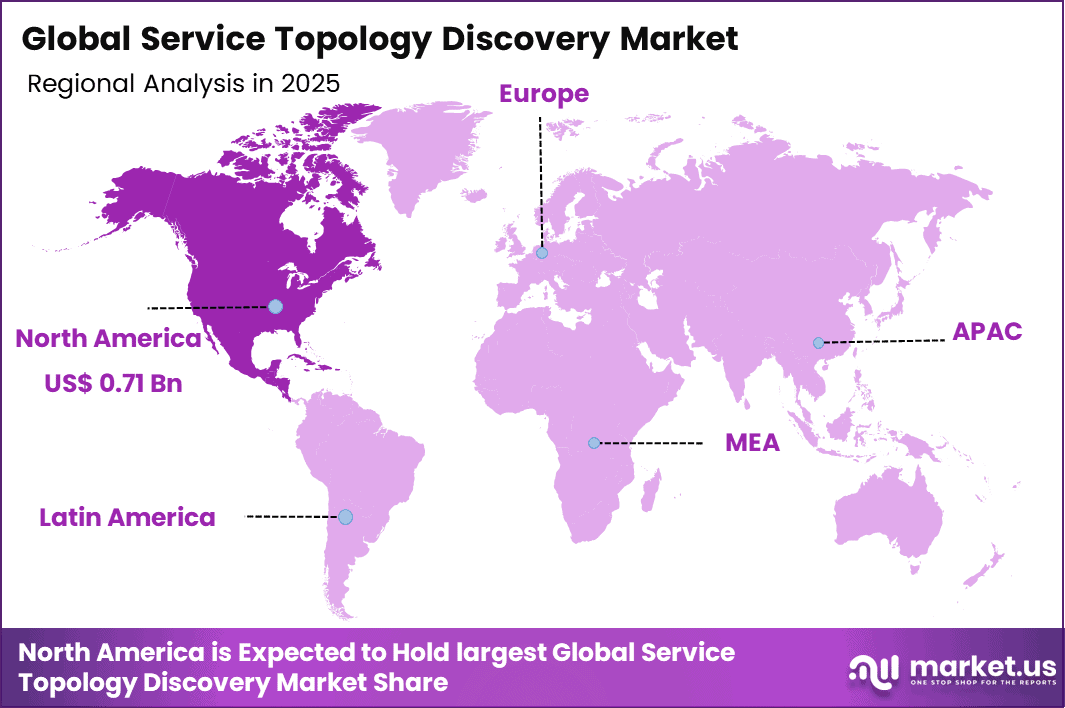

The Global Service Topology Discovery Market generated USD 2.1 billion in 2025 and is predicted to register growth from USD 2.6 billion in 2026 to about USD 14.7 billion by 2035, recording a CAGR of 21.40% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 33.7% share, holding USD 0.71 Billion revenue.

Top Market Takeaways

Software commands 72.7% market share, delivering agentless discovery, dependency mapping, and real-time topology visualization across multi-cloud and legacy environments.

On-premises deployment captures 65.5%, enabling air-gapped scanning, custom protocol support, and integration with enterprise SIEM/CMDB systems.

Network management applications claim 40.8%, powering automated change detection, impact analysis, and troubleshooting workflows for distributed infrastructures.

Large enterprises hold 75.6%, leveraging comprehensive platforms for service dependency mapping, capacity planning, and digital twin creation.

BFSI sector represents 38.9%, utilizing topology discovery for transaction processing resilience, fraud detection correlation, and audit-ready network documentation.

North America drives 33.7% global value, with U.S. market at USD 0.61 billion and 18.5% CAGR, fueled by Dodd-Frank reporting and zero-trust architecture mandates.

Service Topology Discovery market refers to software and monitoring solutions that automatically identify services, applications, infrastructure components, and the relationships between them across an IT environment.

These tools create a live map of how systems connect and depend on each other, which helps operations teams understand service structure more clearly. The market is gaining importance as enterprises run more distributed applications across cloud, on premises, and hybrid environments and need better visibility into service dependencies.

One of the main factors driving this market is the growing complexity of modern IT environments. When applications span multiple services, platforms, and infrastructure layers, manual mapping becomes difficult and often becomes outdated. Service topology discovery helps organizations reduce blind spots, improve incident investigation, and support change management by showing how different services and dependencies interact in real time.

Demand for service topology discovery is increasing among enterprises that rely on cloud applications, digital services, and complex operational systems where downtime and troubleshooting delays can affect business performance.

These buyers want practical tools that can improve observability, speed up root cause analysis, and provide a clearer operational view of service dependencies. Demand is also rising because IT teams increasingly prefer automated mapping instead of manually maintained service diagrams that can quickly become inaccurate.

Drivers Impact Analysis

Key Driver

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Strategic Effect

Increasing complexity of hybrid and multi cloud IT environments

+3.6%

North America, Europe, Asia Pacific

Short to Mid Term (2025–2031)

Enhances visibility across systems

Rising adoption of microservices and containerized architectures

+3.3%

Global

Mid Term (2026–2032)

Improves service mapping accuracy

Growing demand for real time IT infrastructure monitoring

+3.0%

Global

Mid Term (2026–2032)

Supports proactive issue resolution

Expansion of DevOps and continuous delivery practices

+2.7%

Global

Mid to Long Term (2026–2035)

Drives automated topology discovery

Increasing need for application performance management

+2.5%

Global

Mid to Long Term (2026–2035)

Improves service reliability

Restraints Impact Analysis

Key Restraint

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Strategic Effect

Complexity in integrating with legacy IT systems

-2.5%

North America, Europe

Mid Term (2026–2032)

Delays implementation

High cost of advanced monitoring and discovery tools

-2.2%

Global

Mid Term (2026–2032)

Limits adoption among SMEs

Data privacy and security concerns

-2.0%

Europe, North America

Mid to Long Term (2026–2035)

Restricts data visibility

Lack of skilled IT professionals for deployment

-1.8%

Global

Mid Term (2026–2032)

Slows adoption

Challenges in handling dynamic and large scale environments

-1.6%

Global

Mid to Long Term (2026–2035)

Affects accuracy

By Component Analysis

Software accounted for 72.7% of the Service Topology Discovery Market. This segment leads because organizations rely on automated tools to map network assets, applications, and service dependencies in real time. These platforms help create accurate topology views, which improve visibility and support faster issue identification.

The segment is also supported by increasing complexity in IT environments. As systems become more interconnected, software based discovery tools help maintain updated topology data and reduce manual effort, which strengthens their adoption across enterprise networks.

By Deployment Mode Analysis

On premises deployment held 66% of the market. This segment leads because organizations prefer to keep network discovery systems within their internal infrastructure to maintain control over sensitive operational data. It allows direct monitoring and secure handling of network information.

The segment is also driven by the need for stable and reliable performance. Enterprises use on premises solutions to ensure consistent operation and maintain compliance with internal security requirements, especially in critical IT environments.

By Application Analysis

Network management represented 40.8% of the market. This segment dominates because topology discovery plays a key role in monitoring network structure, identifying dependencies, and supporting troubleshooting processes. It helps organizations manage performance and maintain service continuity.

The segment is driven by the need for better visibility and control over network operations. Companies use discovery tools to detect configuration changes, optimize performance, and reduce downtime, which supports strong demand in this application area.

By Organization Size Analysis

Large enterprises accounted for 75.6% of the market. This segment leads because large organizations operate complex IT infrastructures with numerous interconnected systems. They require advanced discovery tools to manage dependencies and maintain operational efficiency.

The segment is supported by higher investment capacity and strong focus on IT governance. Large enterprises adopt topology discovery solutions to improve system visibility, support decision making, and enhance overall infrastructure management.

By End User Analysis

BFSI captured 38.9% of the market. This segment dominates because financial institutions manage highly interconnected systems that require continuous monitoring and strong visibility. Topology discovery helps them understand system relationships and reduce operational risks.

The segment is driven by strict regulatory requirements and the need for system reliability. BFSI organizations invest in discovery tools to maintain service continuity, improve incident response, and ensure efficient management of critical IT infrastructure.

Investor Type Impact Analysis

Investor Type

Growth Sensitivity

Risk Exposure

Geographic Focus

Investment Outlook

Venture Capital Firms

Very High

High

US, Europe, Israel

Strong cloud observability opportunity

Private Equity Firms

High

Medium

North America, Europe

Expansion in IT operations platforms

Strategic Technology Investors

Very High

Medium

US, China, Japan

Strengthens cloud ecosystem

Corporate Venture Arms

High

Medium

Global

Supports DevOps and monitoring tools

Government and Digital Infrastructure Funds

Medium

Low

Asia Pacific, Europe

Supports digital transformation initiatives

Technology Enablement Analysis

Technology Enabler

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Implementation Significance

AI driven topology discovery and dependency mapping

+3.8%

Global

Short to Mid Term (2025–2031)

Improves accuracy and automation

Cloud native monitoring and observability platforms

+3.4%

Global

Short to Mid Term (2025–2030)

Enables scalable deployment

Integration with DevOps and CI CD pipelines

+3.1%

Global

Mid Term (2026–2032)

Supports continuous monitoring

Real time analytics and visualization tools

+2.8%

Global

Mid to Long Term (2026–2035)

Enhances decision making

API based integration across IT ecosystems

+2.5%

Global

Mid to Long Term (2026–2035)

Improves interoperability

Key Challenges

Mapping complex IT environments is a major challenge because service topology discovery tools must identify relationships across applications, servers, cloud services, networks, and databases.

Integration can be difficult because many organizations use old systems, cloud platforms, and third party tools that do not share data in a consistent way.

Data accuracy is a key issue because frequent infrastructure changes, temporary workloads, and incomplete system visibility can lead to wrong service maps.

Real time discovery can be hard because large enterprise environments generate huge volumes of system activity that are difficult to track continuously.

User adoption can be slow because IT teams need training to understand discovered dependencies, validate results, and use the software effectively in daily operations.

Emerging Trends

A key trend in the Service Topology Discovery market is the growing use of automated mapping tools that visualize relationships between applications, services, and infrastructure components in real time. These systems continuously track how services interact across cloud and on premises environments, helping teams understand dependencies without manual documentation.

Organizations are adopting solutions that provide dynamic and accurate topology views, which improves visibility into complex digital ecosystems. This trend reflects a shift toward continuous discovery where system relationships are updated automatically as environments change.

Growth Factors

The increasing complexity of modern IT environments is supporting the growth of service topology discovery solutions. Businesses operate across multiple platforms, which makes it difficult to track how services are connected and how changes impact overall performance.

Discovery tools help teams identify dependencies, reduce troubleshooting time, and improve system reliability. At the same time, the need for better operational visibility encourages organizations to adopt solutions that provide clear insights into service interactions and support more efficient management of digital infrastructure.

Key Market Segments

By Component

Software

Services

By Deployment Mode

On-Premises

Cloud

By Application

Network Management

IT Operations

Security and Compliance

Others

By Organization Size

Large Enterprises

Small and Medium Enterprises

By End-User

BFSI

Healthcare

IT and Telecommunications

Retail

Manufacturing

Government

Others

Regional Analysis

North America accounted for 33.7% of the Service Topology Discovery Market, reflecting strong adoption of advanced IT operations and network visibility solutions across enterprises. Organizations across the region increasingly deploy topology discovery tools to map complex application environments, identify dependencies, and improve system performance monitoring. The growing shift toward hybrid cloud and microservices architectures continues to increase network complexity, which drives demand for automated discovery and visualization solutions across North America.

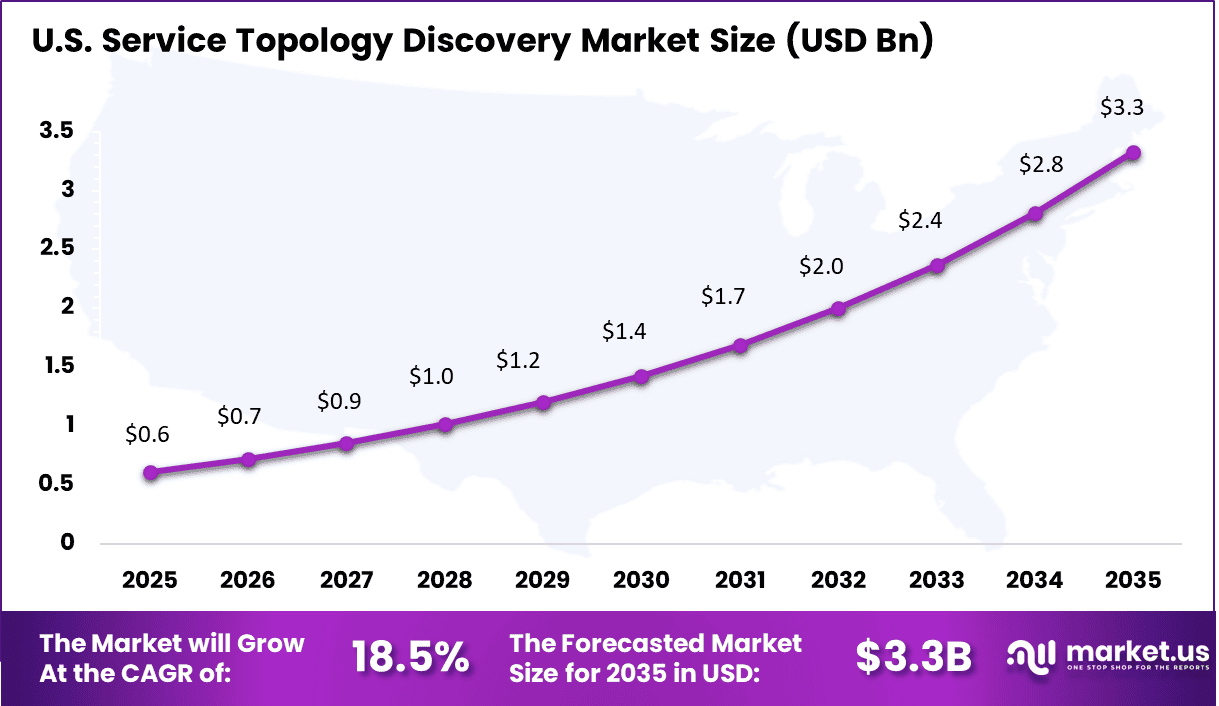

The U.S. generated about USD 0.61 Billion within the regional market and is projected to expand at a CAGR of 18.5%. Enterprises across the country continue to invest in platforms that provide real time visibility into application and infrastructure relationships.

Service topology discovery solutions help IT teams detect issues faster, optimize resource allocation, and support efficient incident management. As organizations manage highly dynamic and distributed IT environments, demand for intelligent topology discovery tools continues to grow rapidly across the US market.

Key Regions and Countries

North America

US

Canada

Europe

Germany

France

The UK

Spain

Italy

Russia

Netherlands

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Singapore

Thailand

Vietnam

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Competitive Analysis

The competitive landscape of the Service Topology Discovery market includes major IT management, network monitoring, and enterprise software providers. IBM Corporation, Cisco Systems, Inc., SolarWinds Worldwide, LLC, Microsoft Corporation, ManageEngine, Broadcom Inc., BMC Software, Inc., and AppDynamics hold strong positions because they offer platforms that help businesses map IT assets, understand service relationships, and improve visibility across complex infrastructure. These companies compete through automation, monitoring depth, and integration with wider IT operations tools.

Other players such as NetBrain Technologies, Inc., Paessler AG, Nagios Enterprises, LLC, ScienceLogic, Inc., Auvik Networks Inc., Micro Focus International plc, Progress Software Corporation, Kentik Inc., LogicMonitor, Inc., Entuity, Inc., HelpSystems, LLC, and FNT GmbH add competition through network discovery, dependency mapping, and performance monitoring solutions. The market is shaped by real time visibility, ease of deployment, scalability, and the ability to support hybrid and multi cloud environments.

The future outlook for the Service Topology Discovery Market looks strong as IT teams need better visibility into how applications, infrastructure, and service dependencies connect across cloud and on premises environments. Current platform guidance shows that service topology discovery helps identify components, map relationships, and build a clearer view of business services, which supports faster troubleshooting and better change planning. As digital systems become more complex and organizations focus more on uptime, automation, and root cause analysis, demand for service topology discovery solutions is expected to grow steadily in the coming years.

Recent Developments

February, 2026 – IBM Instana adds auto-topology for Kubernetes clusters with AI root cause. Maps app-to-infra deps across AWS and Azure. Targets enterprises with Turbonomic links for auto-scale.

March, 2026 – Cisco AppDynamics rolls ThousandEyes integration for full-stack topology. Discovers BGP paths and SaaS deps in real-time. Boosts zero-trust with device health overlays.

Report Scope

Report Features

Description

Market Value (2025)

USD 2.1 Billion

Forecast Revenue (2035)

USD 14.7 Billion

CAGR(2025-2035)

21.40%

Base Year for Estimation

2024

Historic Period

2020-2024

Forecast Period

2026-2035

Report Coverage

Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends

Segments Covered

By Component (Software, Services), By Deployment Mode (On-Premises, Cloud), By Application (Network Management, IT Operations, Security and Compliance, Others), By Organization Size (Large Enterprises, Small and Medium Enterprises), By End-User (BFSI, Healthcare, IT and Telecommunications, Retail, Manufacturing, Government, Others)

Regional Analysis

North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA