Quick Navigation

- Reports Description

- Key Takeaways

- US Tariff Impact Analysis

- Analysts’ Viewpoint

- APAC Market Size

- Component Analysis

- Product Type Analysis

- Technology Analysis

- Application Analysis

- End-user Industry Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Regions and Countries

- Key Player Analysis

- Recent Developments

- Report Scope

Reports Description

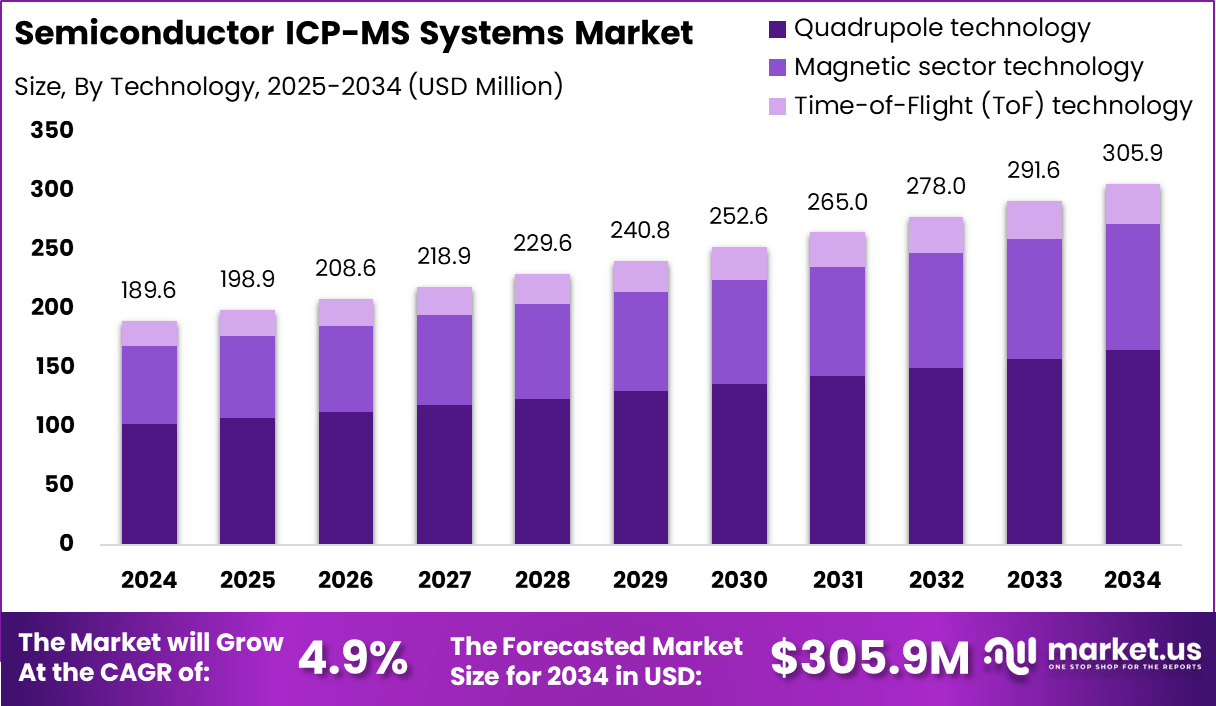

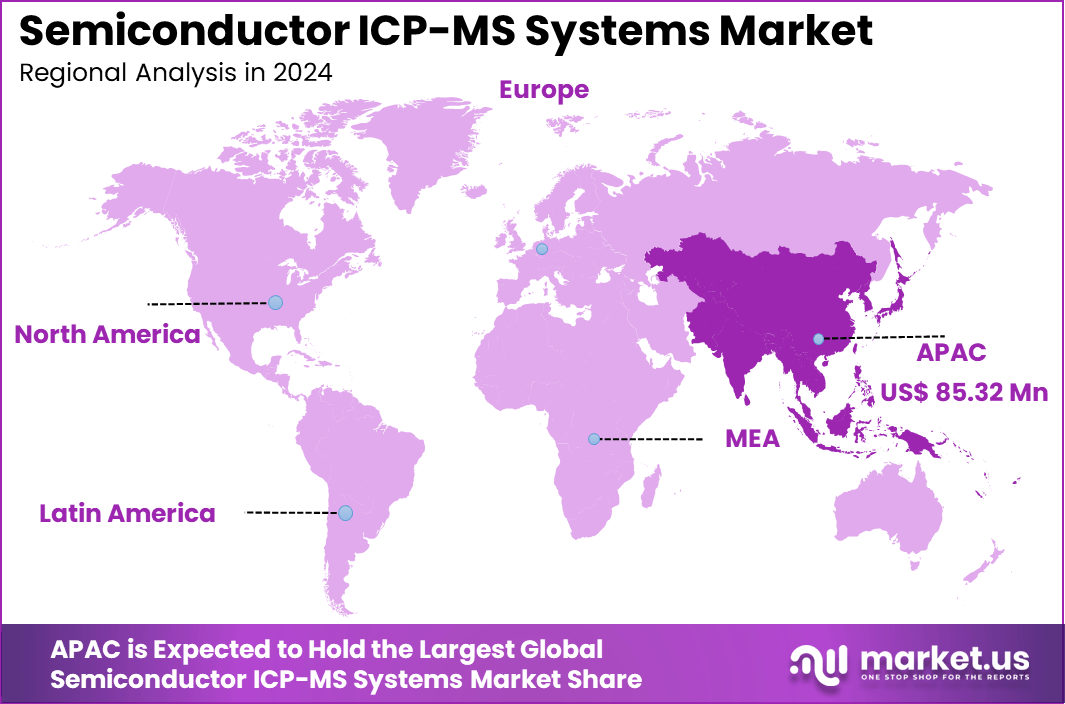

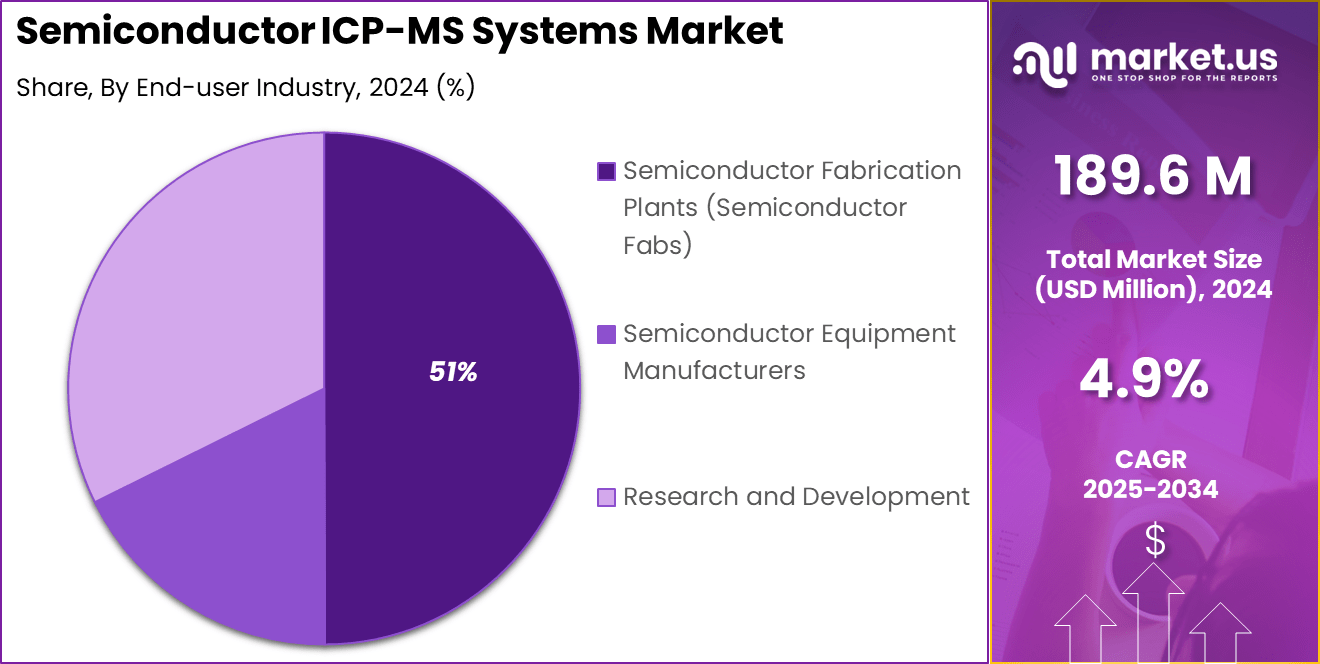

The Global Semiconductor ICP-MS Systems Market size is expected to be worth around USD 305.96 Million By 2034, from USD 189.6 Million in 2024, growing at a CAGR of 4.9% during the forecast period from 2025 to 2034. In 2024, APAC held a dominant market position, capturing more than a 45% share, holding USD 85.32 Million revenue.

Semiconductor Inductively Coupled Plasma Mass Spectrometry (ICP-MS) systems are advanced analytical tools utilized predominantly in the semiconductor industry. These systems play a crucial role in detecting and quantifying ultra-trace levels of metals and elemental contaminants in semiconductor materials.

The high sensitivity and precision of ICP-MS systems make them indispensable for maintaining the purity of materials used in semiconductor manufacturing, ensuring the production of high-performance semiconductor chips.

The global market for semiconductor ICP-MS systems has been experiencing growth, driven by the semiconductor industry’s ongoing need for material purity and contamination analysis. The increasing demand for these systems is attributed to their critical role in improving yield and minimizing defects during semiconductor fabrication.

The increasing integration of technologies such as AI and machine learning in ICP-MS systems enhances their capability to perform more refined analyses, thus broadening their applicability not only in semiconductor manufacturing but also in fields like pharmaceuticals, environmental testing, and food safety. These industries demand high accuracy in detecting trace elements and contaminants, which in turn fuels the demand for advanced ICP-MS systems.

According to Market.us’s analysis, The global semiconductor market is projected to reach approximately USD 996 billion by 2033, rising from USD 530 billion in 2023, at a steady CAGR of 6.5% during the forecast period (2024-2033). This growth is being driven by increasing demand for advanced electronic devices, AI-integrated chips, and expanding applications across automotive, industrial automation, and telecom sectors.

The semiconductor ICP-MS systems market is witnessing a trend towards the adoption of high-resolution and multi-collector ICP-MS systems, known for their enhanced capabilities in isotope discrimination and precise elemental analysis. Technological advancements are continuously being integrated into these systems, improving their efficiency and applicability across various industries.

Innovations such as the development of benchtop models that offer the same precision as larger systems have made ICP-MS technology more accessible and cost-effective for smaller laboratories or on-site analyses. Furthermore, the evolving regulatory landscape that mandates stricter control and reporting of contaminants is another significant trend encouraging the adoption of these advanced systems

Key Takeaways

- The market is projected to reach USD 305.96 Million by 2034, growing at a steady CAGR of 4.9% from its current size of USD 189.6 Million in 2024.

- In 2024, the Asia-Pacific (APAC) region held a commanding lead, accounting for over 45% of global revenue, equivalent to approximately USD 85.32 Million.

- Hardware components made up 78% of the total market share, underlining the capital-intensive nature of ICP-MS systems and the increasing adoption of high-performance instrumentation in quality-sensitive environments such as semiconductor fabs.

- Among product types, Single Quadrupole ICP-MS systems captured 35% of the market. These systems remain a preferred choice due to their cost-efficiency and sufficient sensitivity for routine semiconductor-grade material analysis, especially in mid-tier fabrication environments.

- Quadrupole technology led the market with a 54% share, showcasing its dominance as a mature, stable, and reliable platform for high-throughput elemental detection.

- From an application perspective, Semiconductor Analysis alone contributed 40% of total revenue.

- Semiconductor Fabrication Plants (Fabs) represented 51% of the end-user segment, reinforcing that the primary customer base remains the integrated device manufacturers (IDMs) and foundries.

- Policy-wise, the introduction of a 25% or higher tariff by the U.S. on semiconductor imports is a notable disruptor.

- With around 89% of semiconductors used in the U.S. being imported, this tariff may shift global sourcing strategies and incentivize regional equipment procurement and localization of analytical testing, possibly creating new demand pockets in domestic ICP-MS manufacturing and servicing.

US Tariff Impact Analysis

The introduction of a 25% or higher tariff on semiconductor imports by the United States is anticipated to create far-reaching impacts across the global semiconductor value chain. This policy is likely to raise procurement costs for U.S.-based manufacturers and reduce access to affordable chips, particularly for industries reliant on advanced nodes and overseas production.

The increased tariff burden may disrupt global supply chains, as nearly 89% of semiconductors used in the U.S. are sourced from abroad. This dependence on international suppliers, especially from countries like Taiwan and South Korea, makes the industry more vulnerable to geopolitical tensions and trade restrictions.

The impact of U.S. tariffs on semiconductor ICP-MS systems can be analyzed through various market dynamics and operational challenges faced by the industry:

- Increased Costs: The recent increase in tariffs on semiconductors imported from China to 50% in 2024 has significantly elevated production costs for companies reliant on these components. This escalation is compounded by tariffs targeting specific high-tech components like advanced chips, which are crucial for ICP-MS systems.

- Supply Chain Disruptions: Over 60% of advanced semiconductors are sourced from regions now facing heavy tariffs. This situation forces companies to reevaluate their supply chains, potentially causing delays and increasing the need for manufacturers to find alternative suppliers or increase inventory levels to mitigate risks.

- Strategic Shifts in Manufacturing: The tariffs have incentivized some firms to consider relocating their manufacturing bases or to diversify their production to countries not subject to these heavy tariffs. However, shifting supply chains is a complex and time-consuming process that might not be feasible for all companies in the short term.

- Compliance and Legal Challenges: The implementation of tariffs on semiconductors could potentially violate international trade agreements, such as the Information Technology Agreement (ITA-1), which mandates zero tariffs on semiconductors among participating nations. This could lead to legal disputes and further complicate international relations and business operations.

- Market Dynamics and Competitiveness: Companies like Intel, AMD, and NVIDIA, which rely on global supply chains for semiconductor procurement, could face reduced competitiveness and market share losses to Asian rivals not subjected to these tariffs.

Analysts’ Viewpoint

Investment opportunities in the semiconductor ICP-MS systems market are robust, particularly in developing regions with expanding semiconductor manufacturing capabilities. The business benefits of investing in these systems include enhanced compliance with quality and safety standards, improved product quality, and reduced risk of production downtimes due to contamination.

The regulatory landscape for semiconductor ICP-MS systems is influenced by global standards and regulations that mandate the monitoring and control of environmental and industrial pollutants. Compliance with these regulations promotes the adoption of advanced analytical technologies, including ICP-MS systems.

APAC Market Size

In 2024, APAC held a dominant market position in the Semiconductor ICP-MS Systems market, capturing more than a 45% share and generating revenue of USD 85.32 million. This leadership can be attributed to several key factors.

Firstly, the APAC region benefits from a robust semiconductor manufacturing infrastructure. Countries like Taiwan, South Korea, and China are global leaders in semiconductor production, which naturally extends to specialized equipment such as ICP-MS systems.

This regional dominance in semiconductor fabrication provides a direct boost to the market for associated analytical and measurement equipment, as local manufacturers have easier access to the latest technologies and can integrate new systems more rapidly into their production processes.

Additionally, the region’s commitment to technological innovation and substantial investments in research and development further propel its leadership in this market segment. Governments in APAC countries have prioritized the development of high-tech industries, often providing incentives for semiconductor production and related technologies.

Component Analysis

In 2024, the Hardware segment of the semiconductor ICP-MS systems market held a dominant position, capturing more than a 78% share. This leadership can be attributed primarily to the indispensable role of core hardware components such as the main ICP-MS instrument, plasma generators, and mass spectrometers in conducting detailed elemental analyses.

These components are fundamental to the operation of ICP-MS systems, providing the technological backbone for high-precision measurement and detection capabilities required in semiconductor manufacturing and other high-purity environments. The robust market share is also bolstered by continuous advancements in hardware technology, which enhance system performance and reliability.

For instance, the development of more efficient plasma generators and highly sensitive mass spectrometers has allowed for quicker and more accurate detection of trace elements, meeting the stringent quality control standards of the semiconductor and pharmaceutical industries. The substantial investment in R&D by leading manufacturers ensures ongoing improvements in hardware, further consolidating the market dominance of this segment.

Additionally, the demand for hardware is sustained by the need for regular upgrades and maintenance, ensuring that these systems remain at the cutting edge of technology and comply with evolving industry regulations and standards. This requirement for continuous technological enhancement encourages repeated investments and fosters a cycle of renewal and expansion within the hardware sector of the semiconductor ICP-MS systems market.

Product Type Analysis

In 2024, the Single quadrupole ICP-MS segment held a dominant market position, capturing more than a 35% share. This leading role is primarily due to the segment’s broad applicability and cost-effectiveness, which make it a preferred choice in various industries, including semiconductor manufacturing.

Single quadrupole ICP-MS systems are known for their robustness, ease of use, and excellent performance in routine analysis of high matrix samples where complex and precise isotopic analysis is not required. The prominence of the Single quadrupole ICP-MS segment is further supported by its suitability for a wide range of applications from environmental monitoring to quality control in pharmaceutical production.

These systems meet the industry’s needs for rapid throughput and reliable performance, essential for maintaining stringent quality standards. Additionally, ongoing advancements in technology have enhanced their efficiency, thereby sustaining their popularity and market dominance.

Moreover, the demand for Single quadrupole ICP-MS systems is bolstered by the growing emphasis on regulatory compliance across industries, which requires accurate and traceable measurement of contaminants. The affordability and operational simplicity of these systems allow smaller laboratories and companies with limited budgets to adopt high-quality analytical capabilities, thus expanding the segment’s market reach.

Technology Analysis

In 2024, the Quadrupole technology segment held a dominant market position, capturing more than a 54% share. This leadership is attributed to the technology’s exceptional capability in routine analysis where high throughput and robustness are crucial.

Quadrupole ICP-MS systems are favored for their precision and reliability in quantifying trace elements across a wide range of sample types, from environmental matrices to complex industrial products. The dominance of Quadrupole technology in the market is further reinforced by its versatility and economic efficiency, which make it suitable for both high-end research and routine industrial applications.

These systems offer a balance of performance and cost, appealing to a broad spectrum of users who require fast, accurate results but must also manage operational budgets. Moreover, ongoing technological enhancements in Quadrupole ICP-MS systems, such as increased sensitivity and faster analysis times, continue to solidify their market position.

These advancements meet the evolving demands of industries such as semiconductor manufacturing, where the need for rapid, precise analysis of contaminants at trace levels is critical for maintaining product quality and adherence to stringent regulatory standards.

Application Analysis

In 2024, the Semiconductor Analysis segment within the semiconductor ICP-MS systems market held a dominant market position, capturing more than a 40% share. This substantial market share can be attributed to the critical role of ICP-MS systems in ensuring the purity and quality of semiconductors, which are fundamental to the electronics and technology sectors.

These systems are employed extensively to analyze and quantify trace metals in silicon wafers and other semiconductor materials, which is essential for minimizing defects and improving yield in semiconductor manufacturing. The leadership of the Semiconductor Analysis segment is also supported by the continuous advancements in semiconductor technology, including the development of microelectronics and nanotechnology.

These advancements increase the demand for precise and accurate measurement technologies that can detect contaminants at the atomic level. ICP-MS systems meet these requirements effectively, making them indispensable in the production of high-quality semiconductors.

Furthermore, the ongoing miniaturization of electronic devices necessitates even stricter control over material purity, driving the need for highly sensitive and accurate analytical techniques like those provided by ICP-MS systems. This trend ensures sustained demand for semiconductor analysis applications, reinforcing the segment’s leading position in the market.

End-user Industry Analysis

In 2024, the Semiconductor Fabrication Plants (Semiconductor Fabs) segment held a dominant market position in the semiconductor ICP-MS systems market, capturing more than a 51% share. This substantial market share is primarily due to the critical role of ICP-MS systems in ensuring the purity of materials and components used in semiconductor manufacturing.

Semiconductor fabs require high-precision analytical tools to detect and quantify trace elements and contaminants that can affect the performance and yield of semiconductor devices. The accuracy and sensitivity of ICP-MS systems make them indispensable in these environments.

The dominance of the Semiconductor Fabs segment is also bolstered by the increasing complexity of semiconductor devices and the continuous drive towards miniaturization. As devices become smaller and more complex, the need for stringent contamination control becomes more critical, further driving the demand for sophisticated ICP-MS systems capable of detecting elements at ultra-trace levels.

Furthermore, the ongoing expansion of semiconductor manufacturing capabilities globally, especially in regions like Asia Pacific and North America, continues to fuel the demand for high-quality analytical tools. The strategic deployment of ICP-MS systems in semiconductor fabs ensures adherence to stringent industry standards, maintaining the segment’s leadership in the market.

Key Market Segments

By Component

- Hardware

- Main ICP-MS instrument

- Plasma generator

- Mass spectrometer

- Software

By Product Type

- Single quadrupole ICP-MS

- Triple quadrupole ICP-MS

- Multi-quadrupole ICP-MS

- High resolution ICP-MS

- Multi-collector ICP-MS

- Others

By Technology

- Quadrupole technology

- Magnetic sector technology

- Time-of-Flight (ToF) technology

By Application

- Water Analysis

- Environmental Analysis

- Pharmaceutical and Biomedical Research

- Geological and Mining Research

- Food and Beverage Testing

- Petrochemical Analysis

- Semiconductor Analysis

- Others

By End-user Industry

- Semiconductor Fabrication Plants (Semiconductor Fabs)

- Semiconductor Equipment Manufacturers

- Research and Development

Driver

Increasing Demand for High-Purity Materials in Semiconductor Manufacturing

The semiconductor ICP-MS (Inductively Coupled Plasma Mass Spectrometry) systems market is primarily driven by the escalating need for high-purity materials in semiconductor manufacturing. As the semiconductor industry continues to miniaturize components, the requirement for ultra-pure materials becomes critical to ensure the performance and reliability of the final products.

ICP-MS systems are crucial for detecting and quantifying trace elements and impurities that can affect the semiconductor fabrication process. This capability supports industry demands for higher yields and fewer defects in semiconductor devices.

Restraint

High Cost and Complexity of ICP-MS Systems

One significant restraint in the semiconductor ICP-MS systems market is the high cost associated with these systems, coupled with their complex operation and maintenance requirements. The advanced technology of ICP-MS systems, while providing unparalleled sensitivity and accuracy, requires substantial initial investment and skilled personnel to operate effectively. These factors can be prohibitive for smaller laboratories or institutions, potentially limiting market growth in sectors with constrained budgets

Opportunity

Expansion into New Application Areas

There is a growing opportunity for semiconductor ICP-MS systems in various new application areas beyond traditional semiconductor manufacturing, such as environmental testing, food safety, and pharmaceuticals.

As regulatory standards across these industries tighten, the demand for capable analytical tools like ICP-MS systems that can perform precise trace metal analysis continues to rise. This diversification into multiple sectors presents significant growth opportunities for the ICP-MS market.

Challenge

Need for Continuous Technological Advancements

The semiconductor ICP-MS systems market faces the challenge of continuously needing to innovate and improve. The rapid evolution of semiconductor technology demands parallel advancements in analytical techniques to handle new materials and more stringent purity requirements.

Staying ahead in this competitive market requires ongoing research and development to enhance system capabilities, reduce costs, and increase the ease of use for these complex instruments.

Growth Factors

The growth of the semiconductor ICP-MS (Inductively Coupled Plasma Mass Spectrometry) systems market can primarily be attributed to the increasing demand for precise contaminant measurement in semiconductor manufacturing. This demand is driven by the need for high-purity materials, crucial for advancing microchip technology.

The stringent regulatory requirements across various industries, including pharmaceuticals and environmental monitoring, further necessitate the adoption of high-precision analytical tools such as ICP-MS systems. Technological advancements such as the development of the ICPMS-2030, which integrates functions for analytical method development, are significant in reducing operational costs and enhancing reliability.

Emerging Trends

A major trend observed in the semiconductor ICP-MS systems market is the increasing integration of advanced technologies that offer enhanced detection capabilities for ultra-trace elements. For example, developments in Quadrupole ICP-MS and Multi-Collector ICP-MS have expanded the applications of these systems beyond traditional uses, facilitating their use in more complex and sensitive analyses. The market is also witnessing a shift towards automation and ease of use, making these systems accessible for a broader range of industries and applications.

Business Benefits

The implementation of semiconductor ICP-MS systems provides substantial business advantages, including improved quality control for manufacturing processes, which in turn enhances product reliability and brand reputation.

The ability to conduct thorough material analysis supports compliance with stringent quality and safety standards, reducing the risk of regulatory penalties. Furthermore, the detailed analysis capabilities of ICP-MS systems allow for better process optimization and resource management, leading to cost savings and increased operational efficiency.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Player Analysis

In the Semiconductor ICP-MS (Inductively Coupled Plasma Mass Spectrometry) Systems market, several key players are prominent due to their technological innovations, global reach, and strategic expansions. Here is an analysis of a few major companies that have a strong presence in this industry:

Agilent Technologies is noted for its comprehensive range of ICP-MS systems that cater to various analytical needs in the semiconductor industry. The company focuses on providing instruments that offer high precision and sensitivity, essential for the detection and quantification of trace metal contaminants. Agilent’s ongoing commitment to R&D and its established global distribution network significantly bolster its market position.

Thermo Fisher Scientific stands out with its advanced ICP-MS solutions, which are integral to semiconductor manufacturing for their capability to analyze high-purity materials and chemicals. The company’s systems are designed to meet the stringent requirements of semiconductor manufacturers, aiming at improving yield and reducing defects. Thermo Fisher’s global presence and robust customer service further enhance its competitive edge in the market.

PerkinElmer Inc. Known for its innovative approach to ICP-MS technology, PerkinElmer focuses on systems that support environmental and safety standards in the semiconductor industry. Their instruments are acclaimed for their ability to perform complex analyses with high accuracy, an essential factor for maintaining the purity of semiconductor materials.

Top Key Players in the Market

- Thermo Fisher Scientific Inc.

- Agilent Technologies Inc.

- PerkinElmer Inc.

- Horiba Scientific

- Analytik Jena (A Xylem Brand)

- Shimadzu Corporation

- SPECTRO Analytical Instruments (A part of AMETEK Group)

- E2V Technologies (Teledyne Technologies)

- JEOL Ltd.

- Hitachi High-Technologies Corporation

- Other Key Players

Recent Developments

- In August 2024, PerkinElmer launched the NexION 1100 ICP-MS system, purpose-built for semiconductor applications. This system is engineered to significantly enhance trace element detection, a critical requirement for maintaining material purity in semiconductor production.

- In October 2024, Thermo Fisher Scientific introduced the iCAP MX Series ICP-MS instruments, targeting advanced elemental analysis in semiconductor manufacturing. These instruments are designed to deliver high sensitivity and accuracy, simplifying complex workflows while meeting the sector’s rising expectations for analytical performance and process reliability.

- In April 2024, Agilent introduced the ADS 2 Advanced Dilution System, designed to integrate seamlessly with Agilent’s autosamplers and ICP-MS instruments. This system automates sample preparation, improving laboratory efficiency and reducing operational costs.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 189.6 Mn |

| Forecast Revenue (2034) | USD 305.9 Mn |

| CAGR (2025-2034) | 4.9% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue forecast, AI impact on market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Component (Hardware (Main ICP-MS instrument, Plasma generator, Mass spectrometer), Software), By Product Type (Single quadrupole ICP-MS, Triple quadrupole ICP-MS, Multi-quadrupole ICP-MS, High resolution ICP-MS, Multi-collector ICP-MS, Others), By Technology (Quadrupole technology, Magnetic sector technology, Time-of-Flight (ToF) technology), By Application (Water Analysis, Environmental Analysis, Pharmaceutical and Biomedical Research, Geological and Mining Research, Food and Beverage Testing, Petrochemical Analysis, Semiconductor Analysis, Others), By End-user Industry (Semiconductor Fabrication Plants (Semiconductor Fabs), Semiconductor Equipment Manufacturers, Research and Development) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Thermo Fisher Scientific Inc., Agilent Technologies Inc., PerkinElmer Inc., Horiba Scientific, Analytik Jena (A Xylem Brand), Shimadzu Corporation, SPECTRO Analytical Instruments (A part of AMETEK Group), E2V Technologies (Teledyne Technologies), JEOL Ltd., Hitachi High-Technologies Corporation, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |