Global Seed Binders Market Size, Share Analysis Report By Product Type (Polyvinyl Alcohol, Polyacrylate, Polyvinyl Acetate, Biopolymer-based, Acrylic Latex, Cellulose Derivatives, Guar Gum Binders, Others), By Function (Film Coating, Pelleting, Encrusting, Dust Control Coatings, Controlled-Release Shells, Color Enhancement Layers), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Flowers and Ornamentals, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180799

- Number of Pages: 216

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

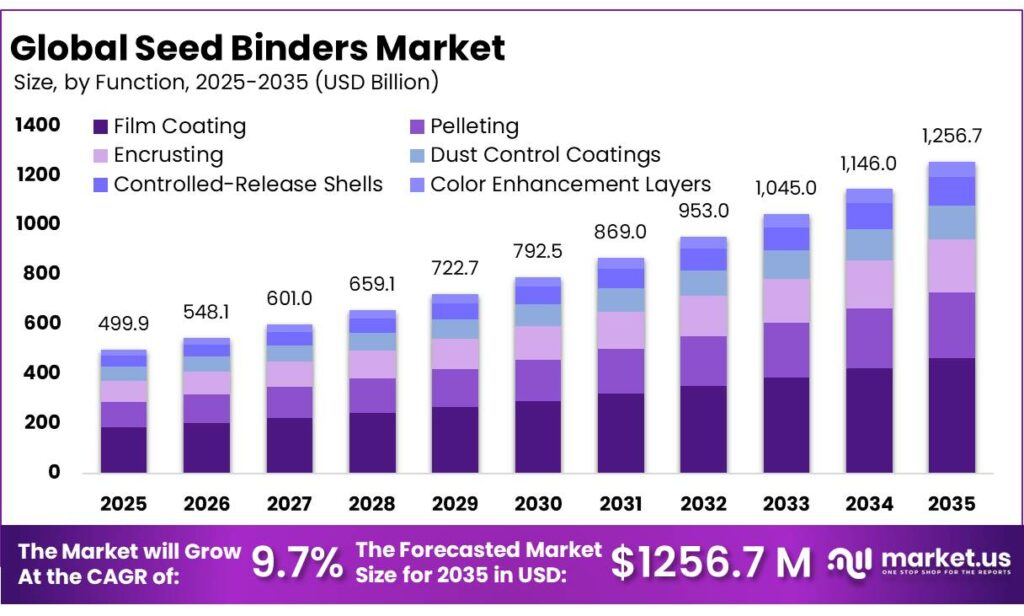

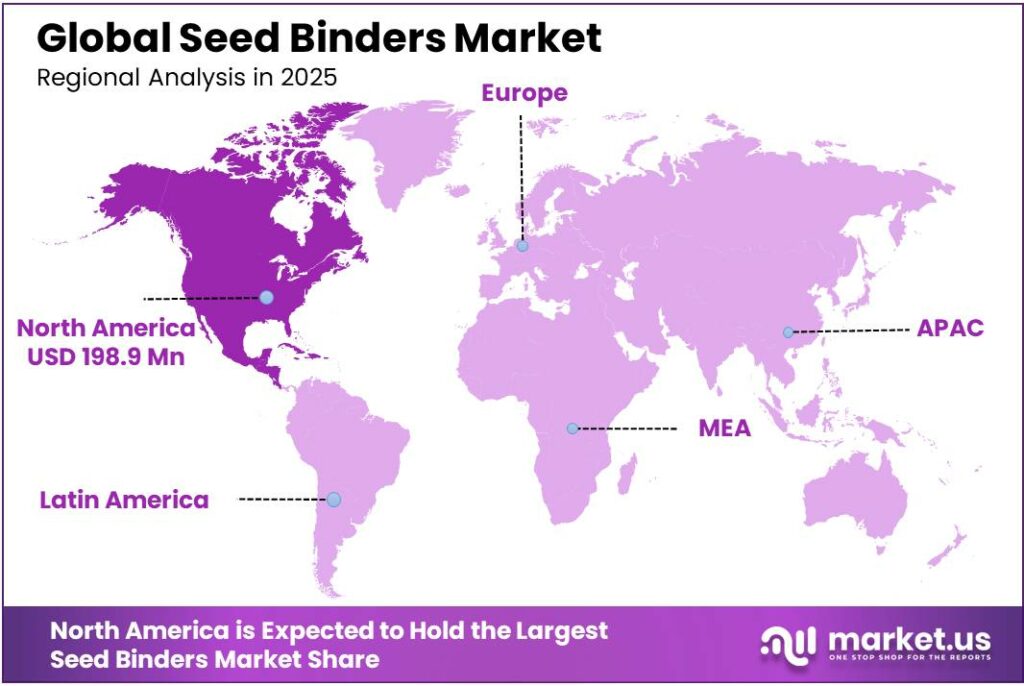

The Global Seed Binders Market size is expected to be worth around USD 1,256.7 Million by 2035, from USD 499.9 Million in 2025, growing at a CAGR of 9.7% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 39.8% share, holding USD 198.9 Million revenue.

The seed binders industry, viewed from a food ingredients perspective, sits at the intersection of functional formulation, nutrition-led product development, and oilseed value-chain expansion. Seed binders are used to provide cohesion, texture stability, sliceability, moisture control, and shelf-life consistency in products such as seed bars, granola clusters, crackers, bakery toppings, confectionery inclusions, and emerging plant-based snacks.

- The OECD-FAO Agricultural Outlook projects world population to reach 8.7 billion by 2033, with total agricultural commodity consumption rising 1.1% annually, while food use is expected to represent 46% of additional global demand over the outlook period. These indicators support steady downstream demand for ingredients that can convert seeds into scalable, consumer-ready formats.

The industrial scenario for seed binders and coatings is shaped by several market forces. Precision agriculture adoption continues to rise, with modern tools such as automated guidance and variable rate technologies improving resource use and crop management efficiency. In the US, for example, automated guidance technologies are used on over 50% of acreage planted to major crops such as corn and soybean, indicating an enabling environment for advanced input solutions like coated seeds.

Driving factors for adoption of seed binders and associated coating technologies include the relentless global demand for increased food production as populations grow, necessitating improvements in germination rates and crop yield outcomes. Research indicates that seed coating — enabled by binders — can increase crop yields by up to 20%, improve seedling emergence by up to 30%, and reduce seed waste by up to 15%, highlighting tangible productivity benefits that drive uptake across commercial agriculture.

- The European Commission states that the EU arable crop sector supplied 64 million tonnes of crude protein in 2023/24, yet the region still imports plant-based products equivalent to 19 million tonnes of crude protein, underscoring the structural importance of plant-protein and oilseed value chains across food, feed, and industrial uses. In parallel, the Commission noted that EU production of protein-rich plants reached 7.2 million tonnes of crude protein in 2023/24, up 28% over 15 years, indicating a gradually strengthening regional base for plant-based ingredient innovation.

Government initiatives in major agricultural economies further shape this industrial context. In India, the Department of Agriculture and Farmers Welfare’s policies under programmes like the National Food Security and Nutrition Mission (NFSNM) include financial assistance mechanisms — such as 50% cost distribution of quality seeds and seed production incentives of ₹1000 per quintal for cereals and millets and ₹2000 per quintal for pulses and oilseeds — to enhance availability and use of quality seeds, which implicitly supports demand for technologies that improve treated seed performance.

Key Takeaways

- Seed Binders Market size is expected to be worth around USD 1,256.7 Million by 2035, from USD 499.9 Million in 2025, growing at a CAGR of 9.7%.

- Polyvinyl Alcohol held a dominant market position, capturing more than a 27.9% share.

- Film Coating held a dominant market position, capturing more than a 37.4% share.

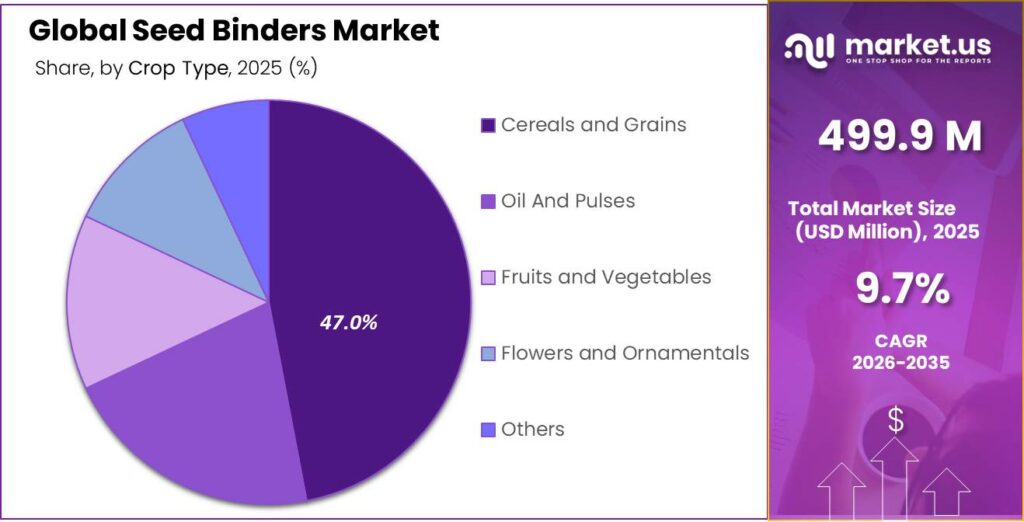

- Cereals and Grains held a dominant market position, capturing more than a 47.5% share.

- North America stands out as the dominant player, capturing a substantial 39.8% share, which equates to approximately 198.9 million.

By Product Type Analysis

Polyvinyl Alcohol leads with 27.9% share driven by strong binding efficiency and wide agricultural use

In 2024, Polyvinyl Alcohol held a dominant market position, capturing more than a 27.9% share in the global seed binders market. Its strong performance was mainly supported by its excellent film-forming properties and reliable adhesion strength, which make it highly suitable for seed coating applications. Farmers and seed processors continue to prefer Polyvinyl Alcohol because it forms a uniform protective layer around seeds, helping nutrients and crop protection ingredients stick firmly to the surface. This improves seed flow during mechanical sowing and reduces dust-off, which is especially important in modern precision planting systems.

By Function Analysis

Film Coating leads with 37.4% share as farmers prefer uniform and protective seed layers

In 2024, Film Coating held a dominant market position, capturing more than a 37.4% share in the seed binders market by function. Its strong share reflects the growing need for thin, uniform, and protective layers applied to seeds before planting. Film coating is widely preferred because it improves seed appearance, enhances flowability during sowing, and ensures that crop protection products and nutrients stay firmly attached to the seed surface. This function plays a key role in modern agriculture where precision planting equipment requires smooth and evenly coated seeds for accurate distribution in the field.

By Crop Type Analysis

Cereals and Grains lead with 47.5% share as staple crops drive seed treatment demand

In 2024, Cereals and Grains held a dominant market position, capturing more than a 47.5% share in the seed binders market by crop type. This strong position reflects the large-scale cultivation of staple crops such as wheat, rice, corn, and barley across major agricultural regions. Since these crops are grown in high volumes and across extensive land areas, the demand for treated and coated seeds remains consistently high. Seed binders play an important role in ensuring that protective and nutritional coatings adhere properly to cereal and grain seeds, improving planting efficiency and early crop establishment.

Key Market Segments

By Product Type

- Polyvinyl Alcohol

- Polyacrylate

- Polyvinyl Acetate

- Biopolymer-based

- Acrylic Latex

- Cellulose Derivatives

- Guar Gum Binders

- Others

By Function

- Film Coating

- Pelleting

- Encrusting

- Dust Control Coatings

- Controlled-Release Shells

- Color Enhancement Layers

By Crop Type

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Flowers and Ornamentals

- Others

Emerging Trends

Sustainable and Next-Generation Seed Coating Technologies

A major trend shaping the seed binders industry today is the shift toward sustainable, high-performance coating technologies that go beyond traditional binders and offer real agronomic value in real farming conditions. In recent years, the way seeds are prepared for planting has begun to change dramatically, driven by a deeper understanding of how coatings interact with seeds and soil, as well as broader pressures on agriculture to be more efficient, more environmentally responsible, and better suited to withstand climate stress.

- Traditionally, seed coatings were used mainly to improve handling and protect seeds from pests during sowing. But now, coatings are being designed with advanced functionalities – such as enhanced nutrient delivery, protection against environmental stresses like drought or heat, and even smart materials that interact with soil moisture levels. Research shows that sophisticated seed coating technologies can improve crop yields by up to 20%, boost seedling emergence by as much as 30%, and reduce seed waste by around 15% compared to untreated seeds.

Government efforts in many countries mirror this focus on sustainable seed technologies. Agricultural extension programmes are increasingly including training on advanced seed treatments and coatings, not just traditional inputs. In India, state-level innovations like seed cooperatives are pairing local farmers with training and access to certified, quality seeds — laying the groundwork for wider adoption of advanced seed coating and treatment options that often include binders.

This trend towards sustainability is also backed by policies and initiatives aimed at strengthening seed systems as a foundation for long-term food security. The Food and Agriculture Organization of the United Nations (FAO) emphasises the importance of improving the quality, diversity and delivery of seeds through sustainable seed systems — including advanced technologies — as critical for achieving food security and nutrition goals around the world.

Drivers

Rising Global Food Demand as a Major Driving Force for Seed Binders

One of the most important reasons seed binders have become so crucial in modern agriculture is the world’s rapidly growing need for more and better food. Farmers and seed producers alike are under pressure to make every seed count, and binders help ensure that seeds not only survive the planting process but also emerge strongly in the field. This driving force connects directly to bigger global challenges like feeding a rising population and increasing crop yields sustainably.

- According to the Food and Agriculture Organization (FAO), global food production must rise sharply to keep up with population growth and consumption patterns. In fact, FAO projections show that food production around the world will need to grow by an estimated 70% by 2050 compared to current levels just to feed an expected larger population of nearly 10 billion people. This figure highlights how urgent the demand challenge is for staple crops like cereals and grains, which form the backbone of food security everywhere.

Another aspect that ties into this demand narrative is food security. Even today, hundreds of millions of people struggle with hunger. According to United Nations estimates under Sustainable Development Goal 2, around 757 million people were facing hunger in 2023, a stark reminder that global food systems are still under strain. Improving crop yields through better seed performance can help close production gaps and contribute to food availability in regions that need it most. Seed binders, in conjunction with coated seeds and other agronomic inputs, help maximise the potential of every planted seed, reducing losses and bolstering food production outcomes.

Government initiatives also reflect this urgency. Many national agricultural policies now emphasise improved seed quality, ensuring that smallholder farmers and large commercial growers alike have access to seeds that stand up to diverse climates and soil conditions. These policies often include support for seed treatment practices, which can involve the use of binders to make coatings more effective and durable.

Restraints

High Cost of Advanced Seed Treatment Materials Limits Adoption

One of the most real and grounding challenges holding back the seed binders market is the high cost of advanced seed treatment materials. This isn’t just about a price tag on a bag of powder or liquid. It reflects deeper constraints in farming economics, especially for small farmers and regions where agriculture is already tight on financial margins. When farmers can’t afford to invest in enhanced seed coatings and binders, the potential benefits—like better germination or stronger early growth—remain out of reach. This restraining factor has a knock-on effect on how widely and how quickly seed binders can be adopted.

- According to the Food and Agriculture Organization (FAO) of the United Nations, nearly 609 million people in the world were undernourished in 2023, highlighting ongoing food insecurity challenges. This number reflects not only food availability but also farmers’ ability to produce enough food affordably. When basic needs for food and livelihood are already stretched thin, spending more on seed technology—even if it offers long-term benefits—can feel out of reach for many producers.

Another trusted source, the World Bank, estimates that operational costs for smallholder farmers often consume a large share of their income. These costs include seeds, fertilisers, equipment, and labour, with limited access to credit or financial buffers. High treatment costs add to this burden, making advanced seed binders a less attractive option. For smallholders with narrow profit margins, choosing cheaper but less effective treatments is often a necessity, not a preference.

This cost barrier also ties into government policies. While many regions have agricultural support programs, the focus often remains on subsidies for basic inputs like fertilisers or staple seeds, rather than advanced coatings and binders. In some countries, seed certification and quality standards still lag behind the technology curve, meaning farmers do not see clear regulatory incentives to adopt higher-cost solutions. Even where governments are trying to strengthen seed systems, budget constraints limit how much support reaches farmers for premium seed treatment products.

Opportunity

Enhanced Seed Quality and Distribution through Government and Global Initiatives

One significant growth opportunity for the seed binders market lies in the increasing global emphasis on improving seed quality and strengthening seed distribution systems, supported by public policies and international food security efforts. As world agriculture faces the twin challenges of rising population and climate change, governments and trusted organisations are placing more focus on ensuring that farmers have access to certified, high-quality seeds that perform well in diverse conditions.

A clear example of how supportive policies open doors for improvement in seed quality can be seen in India. The Indian Department of Agriculture runs the Development and Strengthening of Infrastructure Facilities for Production and Distribution of Quality Seeds scheme, which ensures production and multiplication of high-yielding, certified seeds in sufficient quantities and distributes them at affordable prices, even to remote areas.

Beyond individual countries, international support for seed systems further emphasises this opportunity. Collaborative efforts, such as initiatives to strengthen seed hubs and improve access to high-quality, climate-resilient seeds in developing regions, aim to support small- and medium-scale seed enterprises, particularly in places where agricultural productivity and food security remain under strain.

An increased focus on the formalisation of informal seed systems — which currently provide more than 80% of all seeds used by smallholder farmers in some regions such as sub-Saharan Africa — also highlights growth potential. Turning these informal networks into more robust channels can help spread improved seed technologies faster, bringing benefits like better germination and more resilient crop stands to a wider base of farmers.

Regional Insights

North America leads seed binders adoption with 39.8% share, valued at 198.9 million

In a professional review of the seed binders market by region, North America stands out as the dominant player, capturing a substantial 39.8% share, which equates to approximately 198.9 million in regional value terms. This leading position reflects the region’s advanced agricultural infrastructure, strong emphasis on technology-driven farming practices, and widespread adoption of seed enhancement solutions designed to improve planting efficiency and crop performance.

Across the United States and Canada, farmers increasingly rely on treated and coated seeds to tackle challenges like unpredictable weather, pest pressure, and the need for higher yields from constrained land resources. Seed binders play a crucial role in ensuring that seed coatings — which often contain nutrients, protective agents, and biologicals — remain firmly attached during handling, storage, and sowing. In highly mechanised farming systems common in North America, the smooth flow of treated seeds through planters is essential to achieving planting accuracy and uniform crop stands, which in turn supports yield consistency at scale.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

BASF SE, headquartered in Ludwigshafen, Germany, is a major chemical and seed treatment player globally. It offers a broad portfolio of seed coatings and polymers that enhance flowability and seed performance during planting, supporting protection and early growth across cereals, soybeans, and other crops. BASF’s agricultural solutions unit invests roughly 9–10% of its sales into R&D, with global agriculture sales of about €9.8 billion in 2024. Their innovations aim to improve seed care and help farmers tackle complex field challenges.

Incotec Group BV, headquartered in the Netherlands, specialises in seed enhancement technologies including coating, pelleting, priming, and binder solutions. With a global presence in over 90 countries, Incotec delivers tailored polymer and coating systems designed to support seed protection and handling performance for cereals, vegetables, and specialty crops. Its technologies aim to increase planting efficiency and bolster early plant establishment, serving seed processors and growers who prioritise quality and precision in treated seeds.

Corteva Agriscience is an American agricultural company formed from Dow AgroSciences and DuPont’s agriculture businesses, focused on seed genetics, crop protection, and digital agriculture. In 2025, Corteva’s overall sales were around US $17 billion, with about US $9.6 billion from its seeds business, underscoring its strength in crop innovation and seed technologies. Corteva’s seed treatments and binders support corn, soybean, wheat, and other major crop cultivation, integrating protection with genetic advancements to improve yield and resilience.

Top Key Players Outlook

- BASF SE

- Bayer AG

- Clariant AG

- Incotec Group BV (Croda International plc)

- Corteva Agriscience

- Solvay SA

- Michelman, Inc.

- Germains Seed Technology Inc

- Covestro AG

- Lanxess AG

Recent Industry Developments

In 2024, Bayer Crop Science reported total sales of €22.3 billion, reflecting a 2.0% decline year-on-year, with earnings before interest, taxes, depreciation and amortisation of €4.3 billion as pricing pressures and market conditions shifted demand across crop inputs.

In 2025, Clariant AG posted CHF 1,981 million in sales and maintained solid profitability, indicating stability in demand for its functional chemical solutions that indirectly support agricultural supply chains including seed enhancement technologies.

Report Scope

Report Features Description Market Value (2025) USD 499.9 Mn Forecast Revenue (2035) USD 1,256.7 Mn CAGR (2026-2035) 9.7%% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Product Type (Polyvinyl Alcohol, Polyacrylate, Polyvinyl Acetate, Biopolymer-based, Acrylic Latex, Cellulose Derivatives, Guar Gum Binders, Others), By Function (Film Coating, Pelleting, Encrusting, Dust Control Coatings, Controlled-Release Shells, Color Enhancement Layers), By Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Flowers and Ornamentals, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape BASF SE, Bayer AG, Clariant AG, Incotec Group BV (Croda International plc), Corteva Agriscience, Solvay SA, Michelman, Inc., Germains Seed Technology Inc, Covestro AG, Lanxess AG Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- BASF SE

- Bayer AG

- Clariant AG

- Incotec Group BV (Croda International plc)

- Corteva Agriscience

- Solvay SA

- Michelman, Inc.

- Germains Seed Technology Inc

- Covestro AG

- Lanxess AG

Our Clients

- 180799

- Mar 2026