Quick Navigation

Report Overview

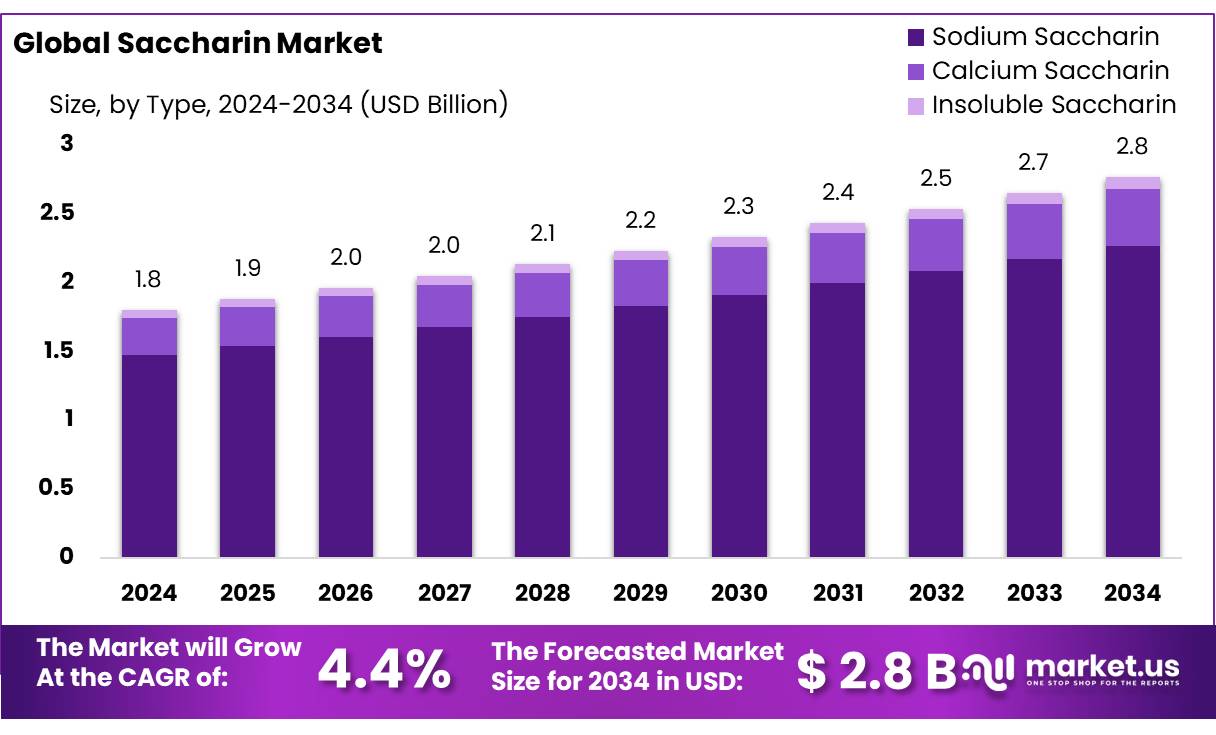

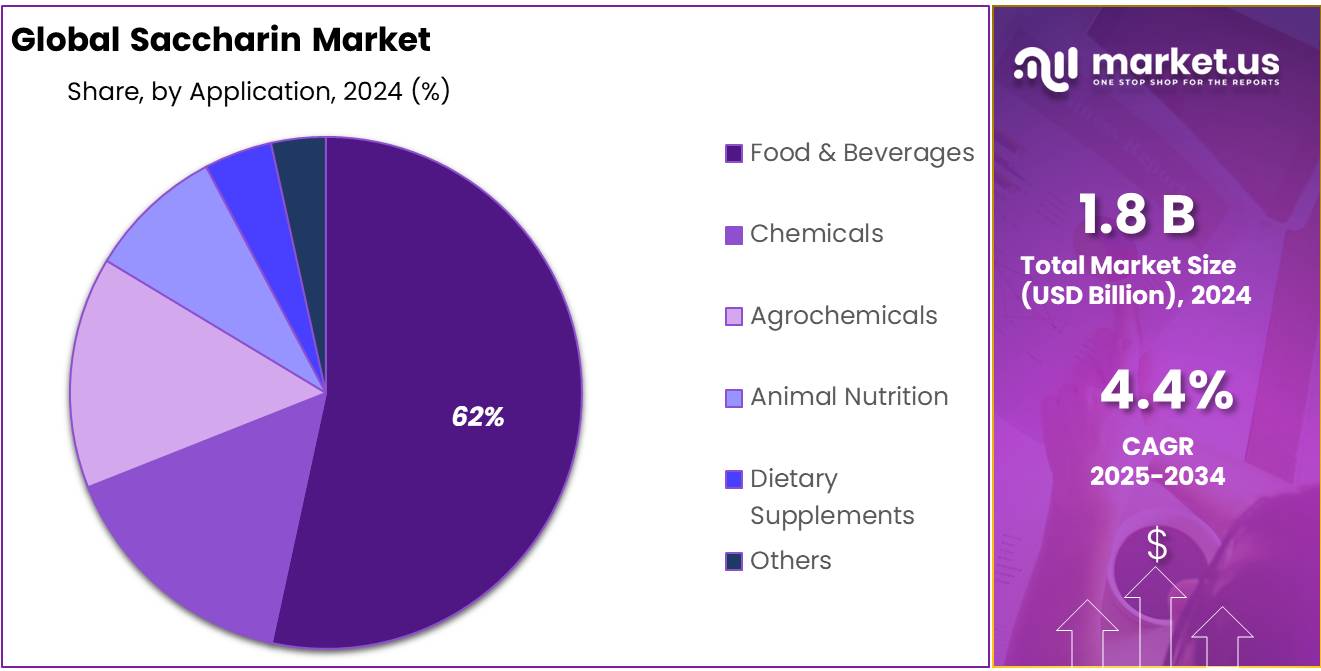

The Global Saccharin Market size is expected to be worth around USD 2.8 Billion by 2034, from USD 1.8 Billion in 2024, growing at a CAGR of 4.4% during the forecast period from 2025 to 2034.

Saccharin concentrates, primarily in the form of sodium saccharin, are synthetic sweeteners extensively utilized across various industries due to their high sweetness intensity—approximately 200 to 700 times that of sucrose—and zero-calorie content. Their stability under heat and acidic conditions makes them suitable for applications in food and beverages, pharmaceuticals, personal care products, and industrial processes such as electroplating. In India, the Food Safety and Standards Authority of India (FSSAI) has approved the use of saccharin sodium in food products, permitting its inclusion up to 100 ppm in carbonated water.

The industrial landscape for saccharin concentrates has evolved significantly over the decades. In the United States, saccharin consumption rose from 21,000 pounds (approximately 9.5 metric tons) in 1953 to 4 million pounds (about 1,800 metric tons) by 1969, following the ban on cyclamates. This surge underscores the industry’s adaptability and the compound’s acceptance as a viable sugar alternative.

Several factors drive the current demand for saccharin. The increasing prevalence of lifestyle-related diseases, such as obesity and diabetes, has heightened the demand for low-calorie sweeteners. For instance, the International Food Information Council reported that nearly 73% of Americans are attempting to reduce or eliminate sugar intake, with 31% of Gen Z and 30% of millennials opting for low or no-calorie sugars. Additionally, saccharin’s cost-effectiveness and stability make it an attractive option for manufacturers aiming to produce sugar-free products without compromising taste.

Government initiatives and regulatory frameworks play a crucial role in shaping the saccharin market. In India, the Directorate General of Trade Remedies (DGTR) recommended a countervailing duty of 20% on imports of saccharin from China in 2019, effective until July 2024, to protect domestic manufacturers from subsidized imports . Such measures aim to promote local production and ensure fair competition in the market.

Key Takeaways

- Saccharin Market size is expected to be worth around USD 2.8 Billion by 2034, from USD 1.8 Billion in 2024, growing at a CAGR of 4.4%.

- Sodium Saccharin held a dominant market position, capturing more than an 82.1% share in the Saccharin market.

- Granular held a dominant market position, capturing more than a 54.3% share in the Saccharin market.

- Food & Beverages held a dominant market position, capturing more than a 62.7% share in the Saccharin market.

- Offline held a dominant market position, capturing more than a 73.9% share in the Saccharin market.

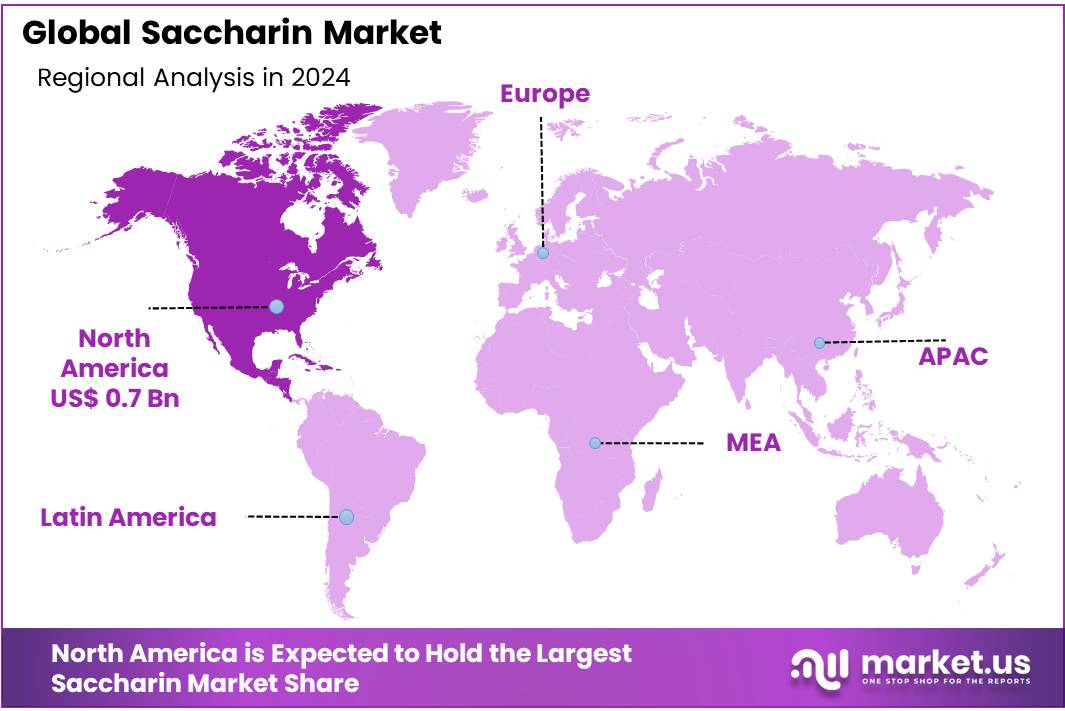

- North America emerged as the leading region in the global saccharin market, capturing 44.3% of the market share, equivalent to approximately USD 0.7 billion.

By Type

Sodium Saccharin Leads the Market with 82.1% Share in 2024

In 2024, Sodium Saccharin held a dominant market position, capturing more than an 82.1% share in the Saccharin market. Its widespread usage in food and beverage applications, coupled with its cost-effective sweetening capabilities, propelled its demand throughout the year. The segment’s extensive application in low-calorie products and pharmaceuticals further contributed to its substantial market share. As consumer inclination toward sugar substitutes grew, Sodium Saccharin maintained its leading position, driven by its superior stability and affordability. Moving into 2025, the demand for Sodium Saccharin is anticipated to remain robust, supported by ongoing product innovations and increased adoption in processed foods and beverages.

By Form

Granular Saccharin Leads the Market with 54.3% Share in 2024

In 2024, Granular held a dominant market position, capturing more than a 54.3% share in the Saccharin market. Its versatility in food processing, pharmaceutical formulations, and beverage production drove its substantial market presence. The segment’s ease of handling and consistent texture made it a preferred choice for manufacturers, contributing to its widespread adoption. The granular form’s stability in high-temperature applications further solidified its position in the market. Moving into 2025, Granular Saccharin is expected to maintain its prominence, with increased utilization in sugar-free and low-calorie products boosting its demand across multiple sectors.

By Application

Food & Beverages Lead the Market with 62.7% Share in 2024

In 2024, Food & Beverages held a dominant market position, capturing more than a 62.7% share in the Saccharin market. The rising demand for low-calorie and sugar-free products significantly propelled the segment’s growth throughout the year. Saccharin’s extensive use as a sweetening agent in soft drinks, confectioneries, and baked goods reinforced its prominence in the food and beverage sector. Additionally, increased consumer awareness regarding calorie reduction and sugar substitutes further supported the segment’s strong market share. Heading into 2025, Food & Beverages are anticipated to retain their leading position, driven by the continued shift towards healthier food and beverage options globally.

By Distribution

Offline Channels Dominate the Market with 73.9% Share in 2024

In 2024, Offline held a dominant market position, capturing more than a 73.9% share in the Saccharin market. Traditional retail outlets, supermarkets, and specialty stores remained the preferred distribution channels, driving significant sales throughout the year. The widespread availability of saccharin products in brick-and-mortar stores allowed consumers easy access, reinforcing Offline’s substantial market presence. Additionally, strong customer preference for in-store purchases, particularly in emerging economies, further contributed to the segment’s leading share. As 2025 progresses, Offline channels are expected to sustain their market dominance, driven by ongoing consumer reliance on physical retail for purchasing food additives and sweeteners.

Key Market Segments

By Type

- Sodium Saccharin

- Calcium Saccharin

- Insoluble Saccharin

By Form

- Granular

- Dry/ Powder

- Liquid

By Application

- Food & Beverages

- Chemicals

- Agrochemicals

- Animal Nutrition

- Dietary Supplements

- Others

By Distribution

- Online

- Offline

Drivers

Rising Health Awareness and Regulatory Support Fuel Saccharin Market Growth

One of the primary drivers of the saccharin market is the increasing health consciousness among consumers, particularly in urban areas. A survey conducted by Local Circles in 2023 revealed that 38% of urban Indians consume artificial sweeteners monthly, indicating a significant shift towards low-calorie alternatives in daily diets .

This growing preference is further supported by regulatory frameworks. The Food Safety and Standards Authority of India (FSSAI) has established safety limits for non-caloric sweeteners, including saccharin, ensuring their safe incorporation into various food products . Such regulations not only safeguard public health but also instill confidence among manufacturers and consumers, promoting the use of saccharin in the food industry.

Government initiatives also play a crucial role in this growth trajectory. FSSAI’s continuous efforts to update and amend food additive regulations reflect a proactive approach to accommodate emerging health trends and scientific findings . These measures ensure that the use of saccharin and other artificial sweeteners aligns with global standards, thereby facilitating their wider acceptance and usage.

Restraints

Health Concerns and Regulatory Warnings Restrain Saccharin Market Growth

A significant factor restraining the growth of the saccharin market is the mounting health concerns associated with artificial sweeteners. In May 2023, the World Health Organization (WHO) released a guideline advising against the use of non-sugar sweeteners (NSS), including saccharin, for weight control or reducing the risk of noncommunicable diseases. The guideline highlighted that NSS do not provide any long-term benefit in reducing body fat in adults or children and may have potential undesirable effects, such as an increased risk of type 2 diabetes, cardiovascular diseases, and mortality.

In India, the Food Safety and Standards Authority of India (FSSAI) has established safety limits for non-caloric sweeteners, including saccharin, to ensure their safe use in various food products. These limits are based on risk assessments and acceptable daily intake levels established by the Joint Expert Committee on Food Additives (JECFA) and are harmonized with Codex standards. However, the presence of such regulations also underscores the need for caution and monitoring, which can impact consumer perception and market growth.

Furthermore, studies have raised concerns about the potential health risks of artificial sweeteners. For instance, a study published in the journal Cell Metabolism found that consumption of certain artificial sweeteners could lead to glucose intolerance by altering gut microbiota. While this study focused on other sweeteners, it contributes to the overall skepticism surrounding artificial sweeteners, including saccharin.

Opportunity

Expanding Sugar-Free Confectionery Market Presents Growth Opportunity for Saccharin

The growing demand for sugar-free confectionery products in India presents a significant growth opportunity for the saccharin market. As consumers become more health-conscious, there’s an increasing preference for low-calorie and sugar-free alternatives in sweets and snacks. This shift is evident in the rising popularity of sugar-free candies, gums, and chocolates, which often utilize artificial sweeteners like saccharin to maintain taste without the added calories.

According to industry reports, the Indian sugar-free confectionery market has been experiencing steady growth, driven by urbanization, rising disposable incomes, and greater awareness of health and wellness. This trend is further supported by the increasing prevalence of lifestyle-related health issues such as obesity and diabetes, prompting consumers to seek healthier alternatives to traditional sugary treats.

Manufacturers are responding to this demand by expanding their product lines to include a variety of sugar-free options. For instance, companies are introducing sugar-free versions of popular confectionery items, leveraging saccharin’s stability and cost-effectiveness as a sweetening agent. This not only caters to health-conscious consumers but also opens up new market segments, including those with dietary restrictions.

Government initiatives aimed at promoting healthier eating habits also play a role in this market expansion. Campaigns and regulations encouraging reduced sugar intake are influencing both consumer behavior and manufacturing practices. As a result, the incorporation of artificial sweeteners like saccharin in confectionery products is becoming more commonplace, aligning with public health objectives.

Trends

Digital Retail Expansion Boosts Saccharin Market in India

In recent years, the saccharin market in India has witnessed a significant shift due to the rapid expansion of digital retail platforms. The increasing penetration of smartphones and the internet has enabled consumers across urban and rural areas to access a wide range of products, including artificial sweeteners like saccharin, through online marketplaces.

This digital transformation has been further accelerated by the COVID-19 pandemic, which prompted a surge in online shopping as consumers sought safe and convenient purchasing options. As a result, e-commerce platforms have become vital channels for the distribution of saccharin, allowing manufacturers to reach a broader customer base without the limitations of traditional brick-and-mortar stores.

Moreover, the Indian government’s initiatives to promote digital literacy and e-commerce have played a crucial role in this trend. Programs aimed at enhancing digital infrastructure and encouraging online transactions have made it easier for consumers to explore and purchase products like saccharin online. This supportive environment has not only benefited consumers but also provided manufacturers with new avenues for growth and market penetration.

The convenience of online shopping, coupled with the availability of detailed product information and customer reviews, has empowered consumers to make informed choices about their purchases. This transparency has built trust in online platforms, further driving the adoption of saccharin through digital retail channels.

Regional Analysis

In 2024, North America emerged as the leading region in the global saccharin market, capturing 44.3% of the market share, equivalent to approximately USD 0.7 billion. This dominance is primarily driven by the region’s heightened health consciousness, leading to increased demand for low-calorie and sugar-free products. The prevalence of lifestyle-related health issues, such as obesity and diabetes, has prompted consumers to seek healthier alternatives, thereby boosting the adoption of artificial sweeteners like saccharin.

The United States, in particular, plays a pivotal role in this market, being the largest importer of saccharin globally. The country’s well-established food and beverage industry has been instrumental in integrating saccharin into various products, ranging from diet sodas to sugar-free confections. Additionally, the pharmaceutical sector utilizes saccharin in formulations like chewable tablets and syrups, further expanding its application scope.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Kaifeng Xinghua Fine Chemical Ltd. is a prominent player in the global saccharin market, specializing in the production and supply of high-quality saccharin for food, pharmaceutical, and industrial applications. The company leverages advanced manufacturing facilities to ensure consistent product quality, positioning itself as a reliable supplier to major clients worldwide. In 2024, it focused on expanding its distribution network to increase its market share, targeting key regions like North America and Europe for strategic growth.

PMC Specialties Group, Inc. is a leading manufacturer of saccharin, catering to the food, beverage, and pharmaceutical sectors. The company emphasizes stringent quality control and adherence to regulatory standards, ensuring its saccharin products meet global safety guidelines. In 2024, PMC Specialties enhanced its production capabilities to accommodate rising demand for low-calorie sweeteners, particularly in the U.S. market. It continues to explore opportunities in emerging markets to strengthen its global footprint.

Productos Aditivos SA, based in Spain, is a key manufacturer of saccharin, supplying both granular and powder forms for various industrial applications. The company leverages its extensive distribution network to serve clients across Europe, Latin America, and Asia. In 2024, it focused on product diversification to meet the growing demand for low-calorie sweeteners in the food processing industry. Its commitment to quality assurance and regulatory compliance further solidifies its market position.

Top Key Players in the Market

- Kaifeng Xinghua Fine Chemical Ltd.

- PMC Specialties Group, Inc.

- Productos Aditivos SA

- JMC Saccharin

- Tianjin Changjie Chemical Co.

- Merck KGaA

- HYET Sweet

- Shree Ganesh Chemicals

- Salvi Chemical Industries Ltd.

- Kyung-In Synthetic Corporation

Recent Developments

In 2024 PMC Specialties Group, Inc., the company continued to lead with its SYNCAL® brand, offering a diverse range of saccharin types, including sodium, calcium, and acid forms, in both granular and powder formats.

In 2024 Kaifeng Xinghua Fine Chemical Ltd., the company reported an annual output of approximately 3,000 metric tons of sodium saccharin, catering to diverse industries including food and beverage, pharmaceuticals, and personal care.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 1.8 Bn |

| Forecast Revenue (2034) | USD 2.8 Bn |

| CAGR (2025-2034) | 4.4% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Sodium Saccharin, Calcium Saccharin, Insoluble Saccharin), By Form (Granular, Dry/ Powder, Liquid), By Application (Food and Beverages, Chemicals, Agrochemicals, Animal Nutrition, Dietary Supplements, Others), By Distribution (Online, Offline) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA |

| Competitive Landscape | Kaifeng Xinghua Fine Chemical Ltd., PMC Specialties Group, Inc., Productos Aditivos SA, JMC Saccharin, Tianjin Changjie Chemical Co., Merck KGaA, HYET Sweet, Shree Ganesh Chemicals, Salvi Chemical Industries Ltd., Kyung-In Synthetic Corporation |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |