Global Rubber Process Oil Market By Type (Aromatic, Paraffinic, Naphthenic, and Low PCA oils), By Viscosity (Low Viscosity, Medium Viscosity, and High Viscosity), By Application (Tyre, Footwear, Conveyor Belts And Industrial Rubber, Automotive Rubber Parts, Rubber Flooring And Mats, Wire And Cable Covering, Paints And Coatings, Adhesive And Sealants, and Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180703

- Number of Pages: 323

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

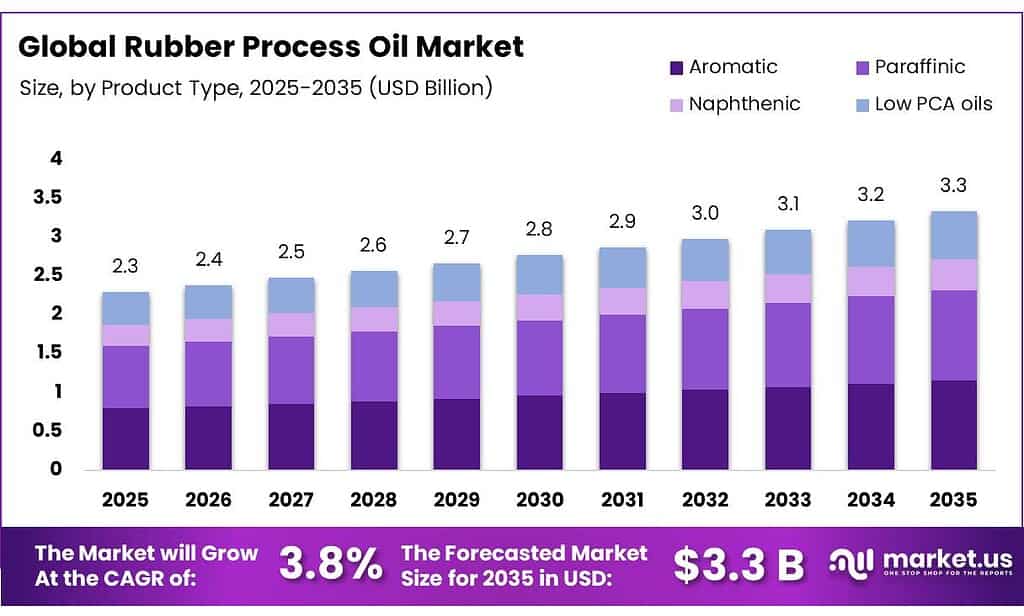

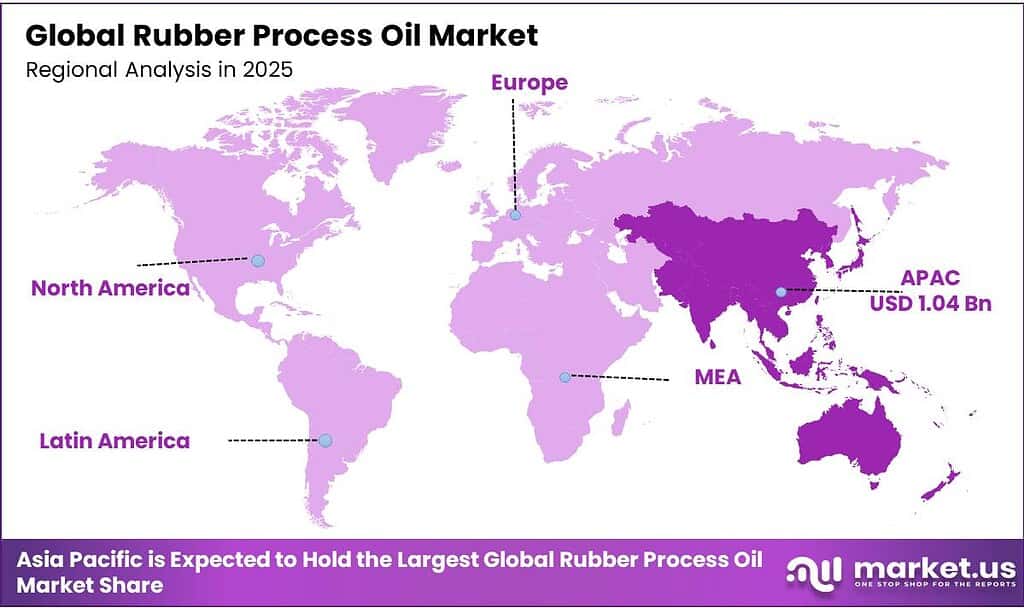

The Global Rubber Process Oil Market size is expected to be worth around USD 3.3 Billion by 2035, from USD 2.3 Billion in 2025, growing at a CAGR of 3.8% during the forecast period from 2026 to 2035. In 2025, Asia Pacific held a dominant market position, capturing more than a 45.3% share, holding USD 1.4 billion revenue.

Rubber process oil (RPO) is a specialized petroleum-derived oil used as an additive in the manufacturing of rubber products to improve the processing of the raw material and the performance of the final goods. It primarily functions as a plasticizer to soften rubber compounds and as an extender to reduce production costs. The market is primarily driven by its essential role as a plasticizer and process aid in rubber compounding, enhancing filler dispersion, elasticity, and processability.

- In the United States alone, the U.S. Tire Manufacturers Association (USTMA) forecasted over 337.4 million tire shipments in 2025, surpassing previous annual totals and indicating sustained tire demand.

Tyre manufacturing constitutes the largest end-use segment, reflecting high rubber volumes, complex multi-component formulations, and continuous production requirements. Additionally, Asia Pacific emerged as the dominant regional market, supported by its leading global position in automotive production and natural and synthetic rubber consumption, particularly in China, India, Thailand, and Indonesia.

- According to the All India Rubber Industries Association, the total rubber exports from India is 1.5% and in value terms are around 43,500 crores, out of which 27,500 crore belongs to the tyre segment and 16,000 crores to the non-tyre segment for the year 2023-24.

RPO formulations vary by aromatic, naphthenic, paraffinic, and low-PAH grades, with aromatic oils historically preferred for their solvency and compatibility with natural and synthetic rubbers. Medium-viscosity oils are most widely used, balancing processability and compound performance. Current trends include a shift toward eco-friendly, low-PAH (poly aromatic hydrocarbons) oils in response to regulatory limits such as EU REACH.

- According to a 2024 study by the Environmental Protection Agency (EPA), more than 800 million tires are discarded each year and are either burned as fuel or processed into recycled products such as artificial turf infill, asphalt, landscaping mulch, and doormats. These disposal and recycling practices may pose potential hazards, including exposure to chemicals and heavy metals through skin contact, inhalation, or ingestion, as well as additional risks associated with polycyclic aromatic hydrocarbons (PAHs).

Key Takeaways:

- The global rubber process oil market was valued at USD 2.3 billion in 2025.

- The global rubber process oil market is projected to grow at a CAGR of 3.8% and is estimated to reach USD 3.3 billion by 2035.

- Based on type, aromatic rubber process oils dominated the market, constituting 34.6% of the total market share.

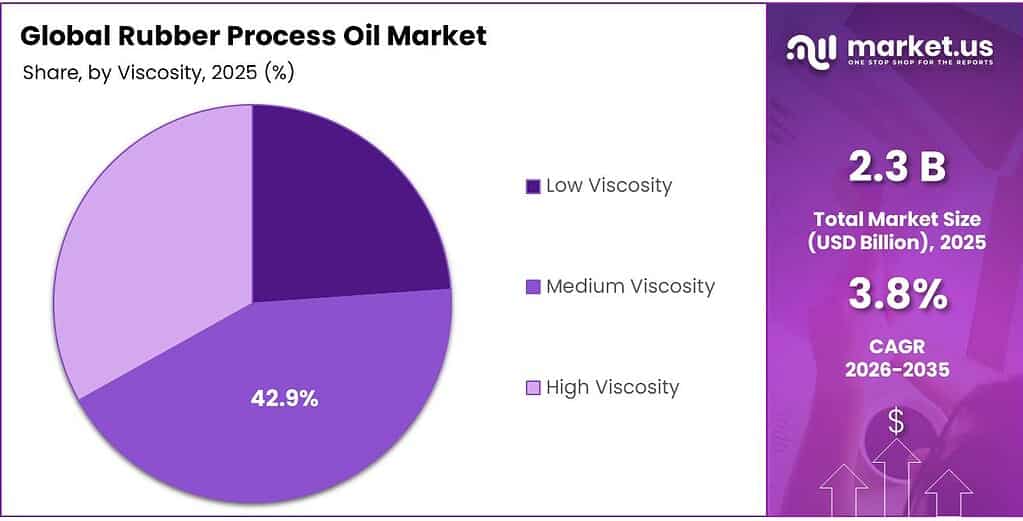

- Based on the viscosity, medium viscosity rubber process oil dominated the market, with a substantial market share of around 42.9%.

- Among the applications of rubber process oil, the tyre industry held a major share in the market, 40.1% of the market share.

- In 2025, the Asia Pacific was the most dominant region in the rubber process oil market, accounting for 45.3% of the total global consumption.

Type Analysis

Aromatic Rubber Process Oils Dominated the Market Due to Their Solvency and Compatibility with Common Rubber Polymers.

On the basis of type, the rubber process oil market is segmented into aromatic, paraffinic, naphthenic, and low PCA oils. The aromatic rubber process oil dominated the market, comprising 34.6% of the market share. Aromatic oils contain a high proportion of aromatic hydrocarbons, which deliver excellent solvating power that improves filler dispersion and reduces compound viscosity, facilitating efficient mixing and enhanced physical properties in vulcanized rubber, particularly in tire compounds where styrene-butadiene rubber (SBR) and natural rubber are predominant. This strong compatibility leads to aromatic oils effectively plasticizing both natural and many synthetic elastomers, improving processing and finished-goods performance. Additionally, their comparatively lower raw petroleum refining cost relative to more refined paraffinic or naphthenic oils has supported widespread use where regulatory limits are less stringent.

By contrast, paraffinic oils offer better oxidation stability and lower PAH content but reduced solvency, and naphthenic grades provide a mid-range balance of properties, making them less universally suitable across diverse rubber formulations than aromatics.

Viscosity Analysis

Medium Viscosity Rubber Process Oil Held the Largest Share in the Market.

Based on the viscosity, the rubber process oil market is divided into low viscosity, medium viscosity, and high viscosity. The medium viscosity rubber process oil dominated the market, with a notable market share of 42.9%, as it provides an optimal balance between processability and compound performance in rubber manufacturing. Practical specifications for many commercial RPOs indicate typical kinematic viscosity at 100°C between about 30-60 cSt for preferred grades, aligning with industry standards that support versatile use across tire and general rubber goods applications.

On the contrary, oils with too low viscosity may not impart sufficient plasticization or solvency, potentially weakening filler dispersion and leading to less robust cured rubber. Conversely, excessively high viscosity can impede mixing and blending with elastomers, reducing operability and efficiency in processing. Medium viscosity oils facilitate smoother mixing, improved flow, and effective filler incorporation while maintaining adequate solvency for both natural and synthetic rubbers, making them suitable for a broad range of formulations without performance trade-offs inherent at the extremes of viscosity.

Applications Analysis

The Tyres Industry Accounted for a Significant Portion of the Rubber Process Oil Market.

The rubber process oil market is categorized by applications into tyre, footwear, conveyor belts & industrial rubber, automotive rubber parts, rubber flooring & mats, wire & cable covering, paints & coatings, adhesive & sealants, and other applications. The tyre industry accounts for 40.1% of the total global usage of rubber process oil market, as tyres require large rubber volumes, complex compound formulations, and consistent plasticization. Additionally, tyre production is highly standardized and continuous, favoring oils that deliver predictable rheology at scale.

In contrast, applications such as footwear, conveyor belts, automotive rubber parts, flooring, wire and cable coverings, paints, coatings, adhesives, and sealants use smaller rubber volumes per unit, fewer compound layers, or alternative plasticizers and resins. Similarly, many of these segments prioritize specific performance traits, including hardness, oil resistance, and adhesion, over bulk processing efficiency. Consequently, tyres dominate rubber process oil usage due to volume intensity, formulation complexity, and continuous high-throughput manufacturing requirements.

Key Market Segments:

By Type

- Aromatic

- Paraffinic

- Naphthenic

- Low PCA Oils

By Viscosity

- Low Viscosity

- Medium Viscosity

- High Viscosity

By Applications

- Tyre

- Footwear

- Conveyor Belts & Industrial Rubber

- Automotive Rubber Parts

- Rubber Flooring & Mats

- Wire & Cable Covering

- Paints & Coatings

- Adhesive & Sealants

- Other Applications

Drivers

Automotive Industry Growth & Tire Demand Drives the Rubber Process Oil Market.

Global motor vehicle production, measured by the International Organization of Motor Vehicle Manufacturers (OICA), has expanded, with nearly 92.5 million vehicles produced worldwide in 2024, with passenger cars accounting for 67.7 million units and commercial vehicles accounting for 20.9 million units of that total, reflecting ongoing automotive industry growth. This uptrend directly correlates with tire manufacturing volumes in the industry, as the production of vehicles grows, it creates demand for a large number of tyres.

According to a study by the Environmental Protection Agency (EPA) in 2024, the production of over 3 billion tires annually takes place. Tire production constitutes the largest single end-use segment for rubber process oils, which are incorporated into rubber compounds to improve processability, elasticity, and filler dispersion in tire treads and sidewalls. Additionally, automotive production increases demand for replacement tyres alike, creating proportional growth in rubber process oil consumption due to its essential functional role in tire compound formulation.

Restraints

Regulatory Constraints and Environmental Impact Might Pose Challenges to the Rubber Process Oil Market.

Regulatory constraints and environmental impacts present measurable challenges for rubber process oil production and use. For instance, the EU REACH regulation (Regulation (EC) No. 1907/2006, Annex XVII, Entry 50) restricts polycyclic aromatic hydrocarbons (PAHs) in extender oils for tires and rubber products, banning tyres with more than 1 mg/kg benzo[a]pyrene and more than 10 mg/kg total PAHs, directly affecting traditional high-aromatic process oils.

PAHs are classified as persistent organic pollutants with carcinogenic, mutagenic, and reproductive toxicity concerns, leading regulators to impose these limits to minimize environmental and human exposure. Similarly, in the United States, the Toxic Substances Control Act (TSCA) authorizes the EPA to regulate the manufacture, processing, use, and disposal of commercial chemicals, requiring testing and limiting harmful substances.

Furthermore, environmental statutes such as the Resource Conservation and Recovery Act (RCRA) govern hazardous waste from industrial oils, mandating disposal controls to prevent soil and water contamination. These regulatory frameworks elevate compliance requirements for refining and handling RPOs, constrain the use of certain grades, and raise recycling and disposal standards, imposing operational and environmental compliance costs on producers and users.

Opportunity

Growth in Non-Tire Rubber Industries Creates Opportunities in the Market.

Expansion in non-tire rubber segments presents a measurable opportunity for rubber process oils through diversified industrial end uses. The rubber compounding chemicals, including plasticizers such as RPOs, are widely applied in industrial belts, hoses, gaskets, seals, and molded mechanical goods used in construction, oil & gas, machinery, and transportation sectors, where elasticity and durability are required.

The U.S. National Institute for Occupational Safety and Health (NIOSH) noted that rubber production involves complex additives to meet performance specifications across diverse products beyond tires. Additionally, nitrile butadiene rubber (NBR), a key synthetic elastomer, underpins product lines such as automotive belts, hoses, O-rings, and gaskets, categories that rely on plasticizers and process aids.

Similarly, in 2024, footwear production and exports increased by 6.9% and 4.6%, respectively, according to data published in the World Footwear Yearbook 2025, recently released by APICCAPS, the Portuguese Footwear Association. The non-tire applications account for substantial proportions of rubber compound production, signaling adjacent demand for process oils as these sectors grow in tandem with global manufacturing and infrastructure activity.

Trends

Shift Towards Eco-Friendly Rubber Process Oils.

Regulatory frameworks aimed at reducing environmental and human health risks are driving a measurable shift toward eco-friendly rubber process oils, notably treated distillate aromatic extracts (TDAE) and mild extraction solvents (MES), which exhibit significantly lower polycyclic aromatic hydrocarbon (PAH) content than traditional high-aromatic extender oils. This trend is codified by global environmental standards, specifically targeting the reduction of PAHs.

The European Union’s REACH Regulation (Entry 50 of Annex XVII) mandates that extender oils must contain less than 3% PCA (polycyclic aromatics) as measured by the IP 346 method. Under the restrictions, vulcanized rubber compounds must comply with PAH limits to meet market access criteria, effectively limiting high-PAH oils in tires and other rubber products.

TDAE grades typically contain lower PAH concentrations, reducing carcinogenic classification and enabling compliance with these environmental restrictions. Experimental observations show no detectable PAH migration from rubber matrices containing TDAE under standardized test conditions, contrasting with conventional oils.

Geopolitical Impact Analysis

The Geopolitical Reality of Supply Chain Disruptions for Rubber Process Oil.

The geopolitical tensions materially affect the rubber process oil market primarily through crude oil price volatility and supply-chain disruptions, given that RPOs are petroleum-derived products. Oil prices remain sensitive to geopolitical developments, including Middle East tensions and conflicts such as ongoing U.S.-Iran and Russia-Ukraine disputes, which have driven short-term price swings. For instance, Brent crude has fluctuated amid conflict-related concerns, with episodic increases of about 10% linked to supply-risk perceptions via chokepoints such as the Strait of Hormuz, a conduit for nearly 20% of global crude exports.

Geopolitical risks correlate with supply-chain fragmentation and trade restrictions, which are key drivers of logistical complexity and delivery delays in global commodity flows. For instance, export controls and sanctions regimes influence international movements of crude and refined feedstocks, complicating sourcing for process oil producers and potentially raising transportation costs.

Furthermore, natural rubber supply disruptions linked to regional tensions, exacerbated by weather and geopolitical pressures in Southeast Asian producing countries, have contributed to price pressures, evidencing how geopolitical factors affect multiple upstream inputs relevant to rubber compound production.

Regional Analysis

Asia Pacific Held the Largest Share of the Global Rubber Process Oil Market.

In 2025, the Asia Pacific dominated the global rubber process oil market, holding about 45.3% of the total global consumption. underpinned by its central role in global rubber and automotive manufacturing, which are primary drivers of process oil consumption. The automotive scale in the region directly correlates with tire manufacturing, which uses significant quantities of rubber compounds containing process oils. The robust regional motor vehicle and rubber production volumes evidence Asia Pacific’s leading position in underlying demand factors for rubber process oils.

- According to the Thai Rubber Association, the Asia Pacific has accounted for approximately 57% of global rubber demand, reflecting large volumes of tire and industrial rubber production concentrated in Thailand, Indonesia, Malaysia, China, and India.

- Additionally, International Organization of Motor Vehicle Manufacturers (OICA) data confirm that Asia Pacific remains the world’s largest automobile production region, producing 54.9 million vehicle units, with major producers such as China, Japan, and India constituting a majority of global output. China alone produced about 31.3 million vehicles in 2024.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of rubber process oil pursue several strategic activities to strengthen competitive positioning and enhance market share. A principal focus is product innovation and formulation development, including low-PAH and bio-based process oils that meet stringent environmental and regulatory standards while preserving technical performance.

Another key focus is geographic and application diversification through tailored product portfolios that address specific regional regulatory requirements and end-use needs. In addition, manufacturers emphasize operational and logistical optimization, maintaining strategic facilities and distribution networks in major production regions to improve supply reliability and reduce lead times.

The following are some of the major players in the industry

- Exxon Mobil Corporation

- TotalEnergies

- Chevron Corporation

- Repsol

- Panama Petrochem Ltd

- Shell Plc

- ORGKHIM Biochemical Holding

- PetroChina Company Limited

- Nynas AB

- APAR Industries Ltd

- Indian Oil Corporation Ltd.

- H&R Group

- Eagle Petrochem

- Gandhar Oil Refinery (India) Limited

- Witmans

- Idemitsu Kosan

- Petro Naft

- Other Key Players

Key Development

- In October 2025, the ethylene project of PetroChina Guangxi Petrochemical was officially completed and put into operation at Qinzhou Port in Guangxi. The project represents the largest ethylene facility with a capacity of one million tons per year in Southwest China. In addition, it includes PetroChina’s first self-developed units for an 80,000-tonne-per-year styrene-butadiene-styrene (SBS) plant and a 120,000-tonne-per-year functionalized solution-polymerized styrene-butadiene rubber (FSSBR) plant.

- In November 2024, TotalEnergies acquired Tecoil, a Finnish company specializing in the production of regenerated base oils (RRBOs), with a production facility in Hamina, Finland, and an annual capacity of 50,000 tons. The company had established a circular economy network for the collection of used lubricants across Europe.

Report Scope

Report Features Description Market Value (2025) US$2.3 Bn Forecast Revenue (2035) US$3.3 Bn CAGR (2026-2035) 3.8% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Aromatic, Paraffinic, Naphthenic, and Low PCA oils), By Viscosity (Low Viscosity, Medium Viscosity, and High Viscosity), By Application (Tyre, Footwear, Conveyor Belts & Industrial Rubber, Automotive Rubber Parts, Rubber Flooring & Mats, Wire & Cable Covering, Paints & Coatings, Adhesive & Sealants, and Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape Exxon Mobil Corporation, TotalEnergies, Chevron Corporation, Repsol, Panama Petrochem Ltd., Shell Plc, ORGKHIM Biochemical Holding, PetroChina Company Limited, Nynas AB, APAR Industries Ltd., Indian Oil Corporation Ltd., H&R Group, Eagle Petrochem, Gandhar Oil Refinery (India) Limited, Witmans, Idemitsu Kosan, Petro Naft, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Exxon Mobil Corporation

- TotalEnergies

- Chevron Corporation

- Repsol

- Panama Petrochem Ltd

- Shell Plc

- ORGKHIM Biochemical Holding

- PetroChina Company Limited

- Nynas AB

- APAR Industries Ltd

- Indian Oil Corporation Ltd.

- H&R Group

- Eagle Petrochem

- Gandhar Oil Refinery (India) Limited

- Witmans

- Idemitsu Kosan

- Petro Naft

- Other Key Players

Our Clients

- 180703

- Mar 2026