Global Robotic Welding Market Size, Share, Growth Analysis By Robot Type (Arc Welding Robots, Spot Welding Robots, Laser Welding Robots, Ultrasonic Welding Robots, Friction Stir Welding Robots, Others), By Payload Capacity (Low Payload Robots, Medium Payload Robots, High Payload Robots), By End-Use Industry (Automotive, Heavy Machinery & Construction Equipment, Shipbuilding & Offshore, Aerospace & Defense, Metal Fabrication & Job Shops, Electronics & Electrical Equipment, Oil & Gas Equipment Manufacturing, Rail & Transportation Equipment, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 180406

- Number of Pages: 206

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

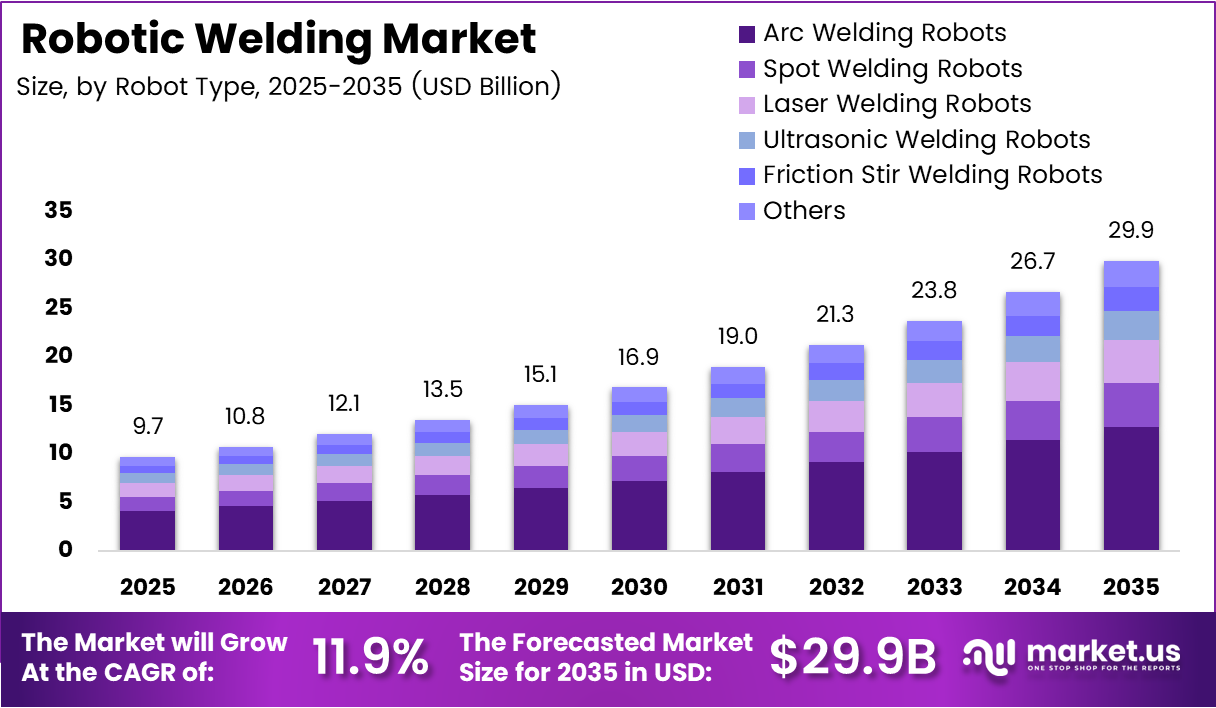

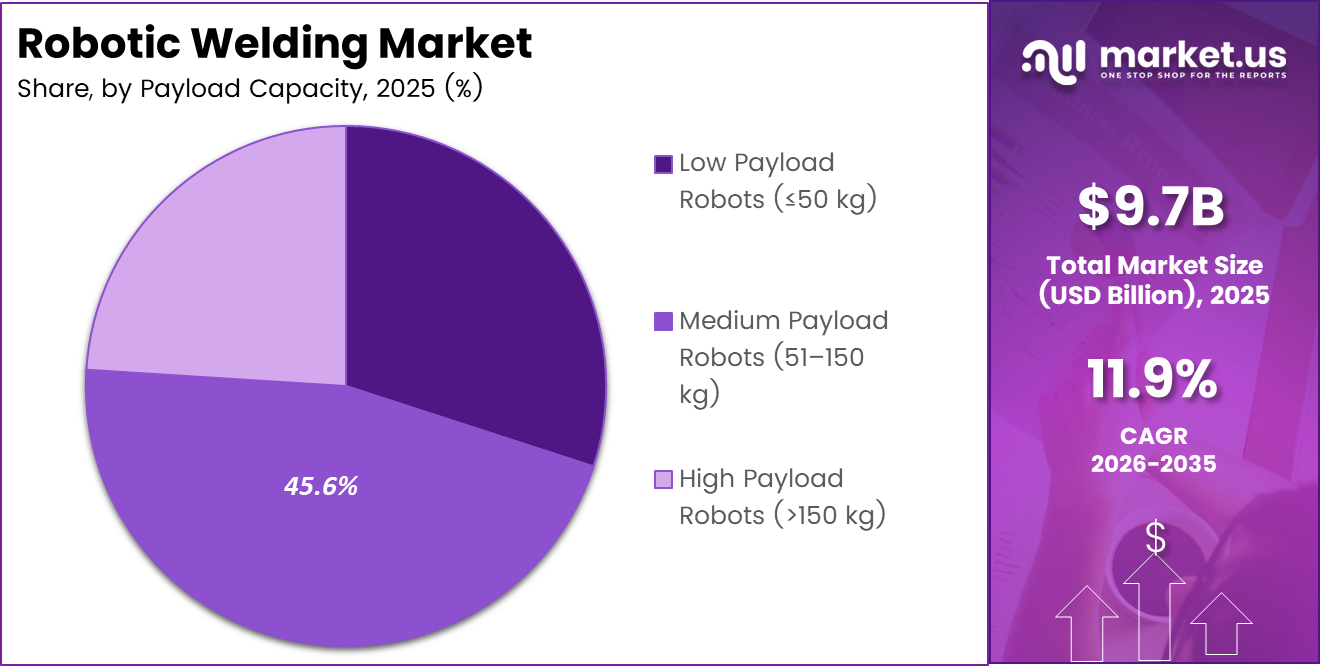

Global Robotic Welding Market size is expected to be worth around USD 29.9 Billion by 2035 from USD 9.7 Billion in 2025, growing at a CAGR of 11.9% during the forecast period 2026 to 2035.

Robotic welding refers to automated systems that use industrial robots to perform welding operations with minimal human intervention. These systems integrate robot arms, welding power sources, wire feeders, and control software to deliver repeatable, high-precision welds across arc, spot, laser, and other welding processes. Manufacturers across automotive, aerospace, shipbuilding, and heavy machinery sectors deploy these systems to meet tighter quality tolerances.

The market spans a broad set of robot types, payload capacities, and end-use industries. Arc welding robots lead adoption due to their versatility in structural and fabrication applications. Spot welding robots remain central to automotive body assembly. Laser and ultrasonic variants serve precision manufacturing where heat input control matters. This diversity allows vendors to address distinct production environments with tailored automation solutions.

Automotive manufacturing underpins the largest share of robotic welding deployments. Vehicle body assembly requires thousands of welds per unit, and the shift to electric vehicle platforms introduces new structural joining requirements. These platforms use more aluminum and advanced high-strength steel, which demand precise welding parameters that robotic systems deliver more reliably than manual labor at scale.

Government-backed industrial policies directly accelerate investment in welding automation. China’s Manufacturing 2025 initiative, Germany’s Industry 4.0 framework, and the U.S. CHIPS and Science Act all allocate capital toward smart factory infrastructure. These programs reduce financial risk for manufacturers upgrading to robotic welding cells, compressing adoption timelines in regions with active policy support.

Labor economics reinforce the capital case for robotic welding. Certified welders command premium wages globally, and the skilled welder shortage has widened in North America, Europe, and parts of Asia. Robotic systems that replace or augment manual welders generate measurable labor cost savings within two to three years, making the investment justifiable even for mid-size fabricators.

According to a 2025 industry guide, robotic welding systems in fabrication environments achieve arc-on time of nearly 90–100%, compared to approximately 30% for manual welding. This gap translates directly into throughput advantage — a single robotic cell running overnight without breaks produces output equivalent to multiple manual shifts, fundamentally changing the unit economics of fabrication.

According to a doctoral dissertation published in 2025 by the University of North Dakota, cobotic welding in high-mix, low-volume manufacturing reduced cycle time by 39% compared to manual processes. This signals that robotic welding is no longer limited to high-volume production runs — it now creates measurable efficiency gains in complex, variable manufacturing environments where automation was previously considered impractical.

Key Takeaways

- The Global Robotic Welding Market was valued at USD 9.7 Billion in 2025 and is forecast to reach USD 29.9 Billion by 2035.

- The market advances at a CAGR of 11.9% during the forecast period 2026 to 2035.

- By Robot Type, Arc Welding Robots lead with a 42.5% market share in 2025.

- By Payload Capacity, Medium Payload Robots (51–150 kg) dominate with a 45.6% share.

- By End-Use Industry, Automotive holds the largest share at 48.7%.

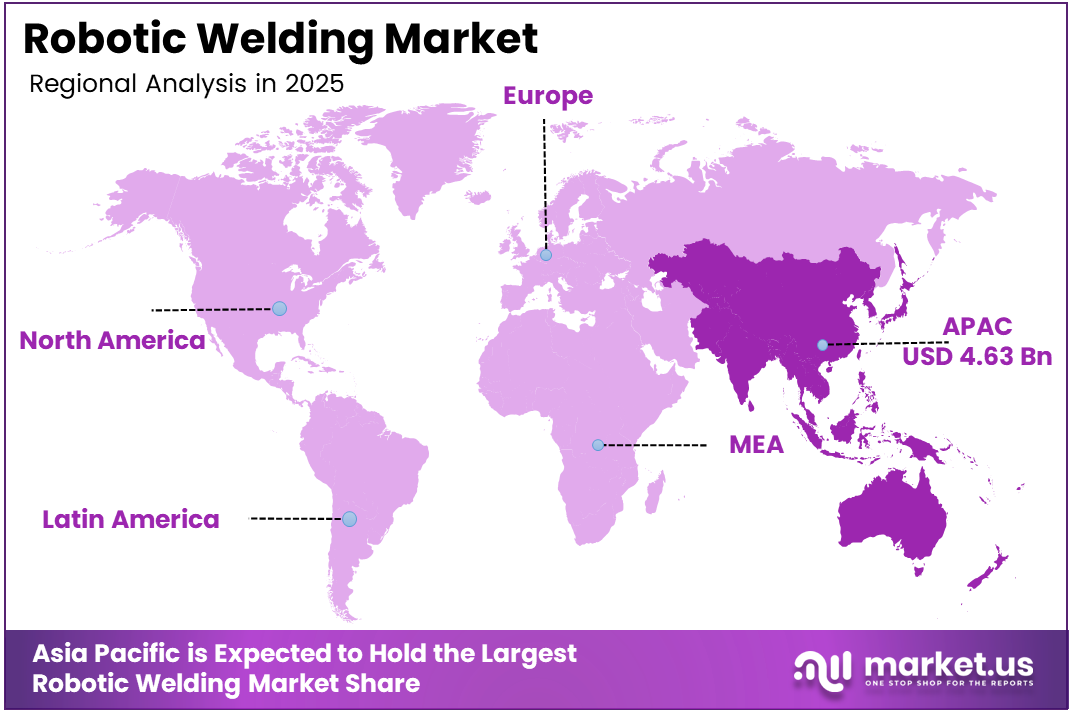

- Asia Pacific dominates regionally with a 47.8% share, valued at USD 4.63 Billion.

Product Analysis

Arc Welding Robots dominate with 42.5% due to broad fabrication versatility and high process adaptability.

In 2025, Arc Welding Robots held a dominant market position in the By Robot Type segment of the Robotic Welding Market, with a 42.5% share. Their ability to handle MIG, TIG, and flux-cored processes across steel, aluminum, and stainless steel makes them the default choice across metal fabrication, automotive, and construction equipment manufacturing. No other robot type matches this process range.

Spot Welding Robots serve as the primary automation tool for automotive body-in-white assembly. Their high-speed, high-cycle operation suits the repetitive joining demands of vehicle production. Automotive manufacturers depend on spot welding robots to maintain line speed and weld consistency across thousands of joint points per vehicle body, making throughput and uptime their critical performance parameters.

Laser Welding Robots carry the highest precision credentials within the robot type segment. They deliver narrow heat-affected zones and deep penetration, enabling joins on thin-gauge metals and dissimilar materials where arc or spot processes would distort the workpiece. Aerospace and electronics manufacturers increasingly specify laser welding robots where tolerances are measured in fractions of a millimeter.

Ultrasonic Welding Robots differentiate through non-thermal bonding, making them the preferred solution for thermoplastic and electronic component assembly. Their absence of heat protects sensitive materials and reduces cycle time for small-part joining. Growth in EV battery module assembly, which involves plastics and thin films, positions ultrasonic welding robots as a structurally relevant sub-segment.

Friction Stir Welding Robots address the specific challenge of joining aluminum and dissimilar metals without melting the base material. Aerospace, rail, and EV battery enclosure manufacturers use this process where material integrity cannot be compromised. The high force requirements of friction stir welding demand purpose-built robotic systems, limiting vendor options but creating defensible niche positions.

Others in the robot type category include plasma, electron beam, and hybrid welding variants. These occupy specialized roles where standard processes cannot meet application requirements. While their combined volume remains small, they represent the technology frontier — early deployment in defense and precision manufacturing signals where next-generation robotic welding demand will concentrate.

Payload Capacity Analysis

Medium Payload Robots dominate with 45.6% due to cross-industry fit and balanced cost-to-capability ratio.

In 2025, Medium Payload Robots (51–150 kg) held a dominant market position in the By Payload Capacity segment of the Robotic Welding Market, with a 45.6% share. This range covers the majority of structural and fabrication welding tasks across automotive, heavy machinery, and metal fabrication. Their versatility eliminates the need for separate low and high-payload systems in mixed-production environments, which improves capital efficiency for buyers.

Low Payload Robots (≤50 kg) serve the entry point for automation in light fabrication and electronics welding. Their compact footprint and lower price point make them accessible to smaller manufacturers transitioning from manual processes. The rise of collaborative robots within this payload class further broadens deployment options, particularly in job shops where flexible redeployment between tasks is a purchasing priority.

High Payload Robots (>150 kg) address the heavy-end welding requirements of shipbuilding, offshore structures, heavy machinery, and large-format construction equipment. Their ability to manipulate oversized workpieces and maintain weld quality under high torch loads makes them irreplaceable in these industries. Capital intensity limits their buyer base, but average transaction values are substantially higher than lower payload classes.

End-Use Industry Analysis

Automotive dominates with 48.7% due to high-volume, repetitive welding demands across vehicle body assembly.

In 2025, Automotive held a dominant market position in the By End-Use Industry segment of the Robotic Welding Market, with a 48.7% share. Vehicle assembly requires thousands of welds per unit across body panels, frames, and subassemblies. The shift to EV platforms intensifies this further — battery enclosures and aluminum-intensive structures demand welding precision that only robotic systems deliver at production speed and quality consistency.

Heavy Machinery and Construction Equipment manufacturers use robotic welding to handle large structural components and thick-gauge steel. Their production volumes are lower than automotive but weld quality requirements are equally stringent. Robotic adoption in this segment accelerates as equipment makers face pressure to cut labor costs and improve structural weld certification compliance.

Shipbuilding and Offshore represent one of the most capital-intensive deployments for robotic welding. Ship hull sections, pressure vessels, and offshore platform components require long continuous welds with full-penetration quality standards. According to a 2025 industry case study, collaborative robotic systems in pipe welding achieve up to a 12-fold productivity increase in stainless steel applications, illustrating the efficiency gap automation closes in this sector.

Aerospace and Defense buyers prioritize weld integrity and traceability above throughput. Robotic welding systems in this segment integrate real-time quality monitoring to meet strict certification requirements. The consequence of weld failure in aerospace structures justifies premium system pricing, making this segment higher-margin for vendors with certified automation expertise.

Metal Fabrication and Job Shops represent the broadest opportunity for mid-market robotic welding adoption. These environments handle diverse parts across short runs, which historically made automation difficult. The emergence of offline programming tools and AI-guided systems now makes robotic welding viable for high-mix, low-volume job shops without requiring dedicated programmers for each new part.

Electronics and Electrical Equipment manufacturing uses precision robotic welding for circuit board components, connectors, and enclosures. The miniaturization trend in electronics pushes welding tolerances beyond manual capability. Laser and ultrasonic welding robots address these requirements, and growth in semiconductor equipment and EV power electronics expands the addressable volume for this sub-segment.

Oil and Gas Equipment Manufacturing deploys robotic welding for pressure-rated pipelines, valves, and subsea structures. Regulatory requirements mandate documented weld quality standards that robotic systems support through data logging and process consistency. Capital project cycles in oil and gas create procurement volatility, but infrastructure renewal programs in the Middle East and Asia sustain baseline demand.

Rail and Transportation Equipment manufacturers weld structural frames, bogies, and car bodies to demanding fatigue-life specifications. Robotic systems in this segment must handle large workpieces and long bead lengths. Expansion of urban rail and high-speed rail networks in Asia and Europe drives fleet procurement, which flows through to robotic welding demand at rolling stock manufacturers.

Others in the end-use category include agricultural equipment, defense vehicles, and white goods manufacturing. These segments adopt robotic welding as cost reduction pressures intensify and skilled labor availability narrows. Their collective share remains secondary, but they offer volume growth for integrators targeting diversification beyond automotive concentration.

Key Market Segments

By Robot Type

- Arc Welding Robots

- Spot Welding Robots

- Laser Welding Robots

- Ultrasonic Welding Robots

- Friction Stir Welding Robots

- Others

By Payload Capacity

- Low Payload Robots (≤50 kg)

- Medium Payload Robots (51–150 kg)

- High Payload Robots (>150 kg)

By End-Use Industry

- Automotive

- Heavy Machinery & Construction Equipment

- Shipbuilding & Offshore

- Aerospace & Defense

- Metal Fabrication & Job Shops

- Electronics & Electrical Equipment

- Oil & Gas Equipment Manufacturing

- Rail & Transportation Equipment

- Others

Drivers

Industrial Automation Mandates, EV Production Expansion, and Skilled Welder Shortages Force Manufacturers to Replace Manual Welding at Scale

Automotive and EV manufacturers now require robotic welding systems to meet production targets that manual labor cannot sustain. EV platforms use more aluminum and advanced high-strength steel than conventional vehicles, requiring precise, repeatable welding parameters at high volume. This structural shift compresses the timeline for welding automation adoption at both OEM and tier-1 supplier levels.

The skilled welder shortage accelerates capital decisions for manufacturers who previously deferred automation. Certified welders command premium wages in North America, Europe, and Australia, and pipeline programs have not kept pace with industry attrition. According to a 2026 academic paper published in ScienceDirect, robotic welding with predictive maintenance achieved 95% sensitivity in anomaly detection — this level of quality monitoring reduces rework and downtime costs that previously justified retaining manual welding specialists.

In January 2026, Path Robotics highlighted its record year — Obsidian AI launch, multi-arm welding advances, and surpassing $100 million in bookings for autonomous robotic welding. This commercial performance confirms that manufacturer demand for fully autonomous welding systems has moved beyond pilot programs. Vendors offering AI-adaptive systems now operate in a market where procurement cycles are shortening and order volumes are scaling.

Restraints

High Capital Requirements and Technical Complexity Lock Small and Mid-Size Manufacturers Out of Robotic Welding Adoption

A complete robotic welding cell — including the robot arm, welding power source, fixturing, safety enclosures, and programming infrastructure — requires substantial upfront capital. For small fabricators operating on tight margins, this entry cost often exceeds annual equipment budgets. Integration costs compound the challenge, as retrofitting robotic systems into existing production layouts frequently requires facility modifications that add six to twelve months to payback calculations.

Technical complexity creates a secondary barrier beyond capital. Robotic welding systems require skilled programmers to create and maintain weld paths, troubleshoot sensor errors, and adapt programs when part geometry changes. Small job shops rarely carry this expertise in-house. According to a 2025 academic paper published in Frontiers in Robotics and AI, maintenance-related issues accounted for 79% of total downtime in robotic welding machines at an automotive tier-1 supplier, with financial losses of R2,281,508.82 over three years. This data signals that even well-resourced manufacturers struggle to manage robotic welding reliability without structured maintenance programs.

Together, capital intensity and technical complexity create a bifurcated market. Large manufacturers with dedicated automation teams and capital access adopt robotic welding at scale. Smaller manufacturers either delay adoption or rely on integrators, increasing total system cost. This dynamic concentrates market benefits among large enterprises while limiting the addressable base for vendors targeting the lower end of the manufacturing segment.

Growth Factors

AI Integration, Cobot Deployment, and Industry 4.0 Infrastructure Unlock Robotic Welding Beyond High-Volume Automotive Applications

Artificial intelligence, machine vision, and smart sensors now enable robotic welding systems to adapt weld parameters in real time based on joint geometry and material variation. This adaptive capability removes the longstanding limitation that robotic welding required precise part fixturing and consistent inputs. Manufacturers with high part-mix production lines can now justify robotic investment without redesigning their entire production setup.

Collaborative welding robots — cobots — open the mid-market to automation by eliminating the need for safety enclosures and reducing floor space requirements. According to a doctoral dissertation published in 2025 by the University of North Dakota, cobotic weldments proved 13.5%–37% stronger across tested parts compared to manual welds. This quality advantage, combined with cobot flexibility, creates a compelling case for fabricators that previously viewed robotic welding as financially or operationally out of reach.

In October 2025, Path Robotics achieved over $100 million in bookings for AI welding automation, alongside advances in multi-arm technology and shipbuilding applications. This commercial milestone demonstrates that smart factory and Industry 4.0 investments are converting into concrete procurement decisions across diverse industries. Vendors that embed connectivity, data analytics, and remote monitoring into welding systems gain preferred positioning in smart factory procurement cycles.

Emerging Trends

Laser and Hybrid Welding Technologies, Digital Twin Simulation, and Real-Time Quality Analytics Redefine Robotic Welding System Expectations

Laser and hybrid robotic welding technologies gain specification priority in aerospace, electronics, and EV manufacturing where heat-affected zone control is non-negotiable. Laser systems deliver weld speeds two to five times faster than conventional arc processes on thin materials, improving throughput without sacrificing joint integrity. Manufacturers investing in next-generation product lines increasingly specify laser-capable robotic systems as a baseline requirement.

Offline programming and digital twin technologies reduce the cost and complexity of deploying robotic welding across new part families. Manufacturers simulate and validate weld paths in a virtual environment before any physical programming occurs, cutting changeover time significantly. In September 2025, Universal Robots showcased next-generation cobot capabilities at FABTECH 2025, including advanced laser welding and a new UR robot model engineered for enhanced reach and stability — demonstrating that digital-physical integration is now a product development priority, not just a research concept.

According to a doctoral dissertation published in 2025 by the University of North Dakota, cobotic welding reduced energy consumption by 41%–71% in single-sided applications compared to manual welding. Real-time weld quality monitoring and data analytics compound this advantage by enabling predictive maintenance, reducing unplanned downtime, and generating weld traceability records required by aerospace and defense customers. Together, these capabilities shift robotic welding from a cost-reduction tool to a quality and compliance asset.

Regional Analysis

Asia Pacific Dominates the Robotic Welding Market with a Market Share of 47.8%, Valued at USD 4.63 Billion

Asia Pacific commands the largest share of the robotic welding market at 47.8%, valued at USD 4.63 Billion. China drives this position through its dense concentration of automotive OEMs, electronics manufacturers, and shipbuilders deploying robotic welding at scale. State-backed industrial automation policies accelerate capital allocation to robotic welding infrastructure, while Japan and South Korea contribute through their established robotics manufacturing ecosystems and export-oriented heavy industry.

North America Robotic Welding Market Trends

North America holds the second-largest position in the robotic welding market, anchored by a mature automotive manufacturing base in the U.S. and Canada. Reshoring of semiconductor and defense manufacturing creates new demand for precision welding automation beyond traditional auto assembly. The skilled welder shortage is acute in this region, making the labor substitution argument for robotic welding more financially compelling than in any other major market.

Europe Robotic Welding Market Trends

Europe sustains strong robotic welding adoption through its high-precision automotive, aerospace, and heavy machinery sectors. Germany leads regional deployment through its Industry 4.0 framework, which directly funds factory automation upgrades. European manufacturers face strict carbon reduction mandates that incentivize energy-efficient robotic welding systems over manual processes, adding a compliance dimension to purchasing decisions beyond pure productivity rationale.

Middle East and Africa Robotic Welding Market Trends

The Middle East advances robotic welding adoption through oil and gas equipment manufacturing and infrastructure construction projects. GCC-based fabricators invest in automated welding to meet pressure vessel and pipeline certification standards required for export and domestic use. Africa’s adoption remains nascent, concentrated in South Africa’s automotive assembly sector, where export vehicle production mandates quality consistency that robotic systems deliver.

Latin America Robotic Welding Market Trends

Latin America’s robotic welding market centers on Brazil and Mexico, where automotive and heavy equipment manufacturing form the industrial base. Mexico’s proximity to U.S. automotive supply chains drives adoption as OEMs transfer production south with automation standards intact. Brazil’s industrial machinery sector and agricultural equipment manufacturers represent secondary demand centers as domestic industrialization investment increases.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

ABB Ltd. positions itself as a full-stack automation provider for welding, integrating its robotic arms with proprietary welding software and digital services. Its strategic advantage lies in combining robot hardware with factory-wide automation platforms, allowing manufacturers to connect welding cells to broader production management systems. In October 2025, SoftBank Group announced an agreement to acquire ABB’s robotics division, a deal expected to close in 2026 that signals major capital backing for accelerated development.

FANUC Corporation leverages its dominant position in CNC systems and factory automation to cross-sell robotic welding solutions to existing customers. This installed base advantage reduces sales cycle length and increases switching costs for manufacturers already running FANUC-controlled machine tools. FANUC’s arc welding robot line emphasizes high-speed, high-duty-cycle performance optimized for continuous automotive production environments where uptime directly determines line output.

KUKA AG competes on integration depth and software capability, offering robotic welding systems that connect directly to MES and ERP platforms. Its position as a preferred supplier to European automotive OEMs gives it reference accounts that validate system performance for prospective buyers. KUKA’s acquisition by Midea Group provides manufacturing scale and China market access that western competitors cannot easily replicate, strengthening its cost and distribution position.

Yaskawa Electric Corporation builds competitive advantage through its Motoman arc welding robots, which are optimized for high-mix, low-volume fabrication environments increasingly targeted by AI-assisted programming tools. Yaskawa’s strategy of combining high-performance hardware with accessible programming interfaces positions it to capture mid-market fabricators that previously could not justify robotic welding investment. Its global service network reduces the perceived technical risk of adoption for first-time automation buyers.

Key Players

- ABB Ltd.

- Carl Cloos Schweisstechnik GmbH

- DAIHEN Corporation

- FANUC Corporation

- Fronius International GmbH

- Kawasaki Heavy Industries, Ltd.

- KUKA AG

- Yaskawa Electric Corporation

- Panasonic Holdings Corporation

- Universal Robots A/S

- Lincoln Electric Holdings, Inc.

- Amada Holdings Co., Ltd.

- Hyundai Robotics

- Comau S.p.A.

- Geometrix Automation And Robotics Pvt. Ltd.

- Other Key Players

Recent Developments

- March 2025 – Novarc Technologies raised $50 million in Series B funding led by Export Development Canada, with participation from Graham Partners, Seaspan, and InBC Investment Corp. The capital targets acceleration of NovAI™ machine vision for intelligent adaptive welding applicable to cobots and articulated robots.

- June 2025 – Comau introduced its MyCo collaborative robot family at Automatica 2025, featuring six cobot models with 3–15 kg payloads. These models are designed for high-precision applications including welding, expanding Comau’s cobot footprint in flexible manufacturing environments.

- August 2025 – LE Robotics, an industrial embodied AI welding specialist, secured Series A funding from Shenzhen Capital Group. This investment supports development and commercialization of AI-native welding systems targeting large-scale industrial deployments across China and global markets.

- September 2025 – Path Robotics launched Obsidian™, its foundational AI model for welding trained on tens of millions of welded inches. Obsidian enables autonomous, adaptive welding for high-mix, low-volume manufacturing without requiring precise part programming for each new component.

- February 2026 – LE Robotics completed a Series A+ round of tens of millions RMB led by Shandong Luhua Investment, following its 2025 Series A. The capital accelerates standardization and large-scale commercialization of embodied AI welding solutions for industrial customers.

Report Scope

Report Features Description Market Value (2025) USD 9.7 Billion Forecast Revenue (2035) USD 29.9 Billion CAGR (2026-2035) 11.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Robot Type (Arc Welding Robots, Spot Welding Robots, Laser Welding Robots, Ultrasonic Welding Robots, Friction Stir Welding Robots, Others), By Payload Capacity (Low Payload Robots ≤50 kg, Medium Payload Robots 51–150 kg, High Payload Robots >150 kg), By End-Use Industry (Automotive, Heavy Machinery & Construction Equipment, Shipbuilding & Offshore, Aerospace & Defense, Metal Fabrication & Job Shops, Electronics & Electrical Equipment, Oil & Gas Equipment Manufacturing, Rail & Transportation Equipment, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape ABB Ltd., Carl Cloos Schweisstechnik GmbH, DAIHEN Corporation, FANUC Corporation, Fronius International GmbH, Kawasaki Heavy Industries Ltd., KUKA AG, Yaskawa Electric Corporation, Panasonic Holdings Corporation, Universal Robots A/S, Lincoln Electric Holdings Inc., Amada Holdings Co. Ltd., Hyundai Robotics, Comau S.p.A., Geometrix Automation And Robotics Pvt. Ltd., Other Key Players Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- ABB Ltd.

- Carl Cloos Schweisstechnik GmbH

- DAIHEN Corporation

- FANUC Corporation

- Fronius International GmbH

- Kawasaki Heavy Industries, Ltd.

- KUKA AG

- Yaskawa Electric Corporation

- Panasonic Holdings Corporation

- Universal Robots A/S

- Lincoln Electric Holdings, Inc.

- Amada Holdings Co., Ltd.

- Hyundai Robotics

- Comau S.p.A.

- Geometrix Automation And Robotics Pvt. Ltd.

- Other Key Players

Our Clients

- 180406

- Mar 2026