Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Product Type Analysis

- By Application Analysis

- By End-User Analysis

- By Distribution Channel Analysis

- Investor Type Impact Analysis

- Technology Enablement Analysis

- Key Challenges

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outlook

- Recent Developments

- Report Scope

Report Overview

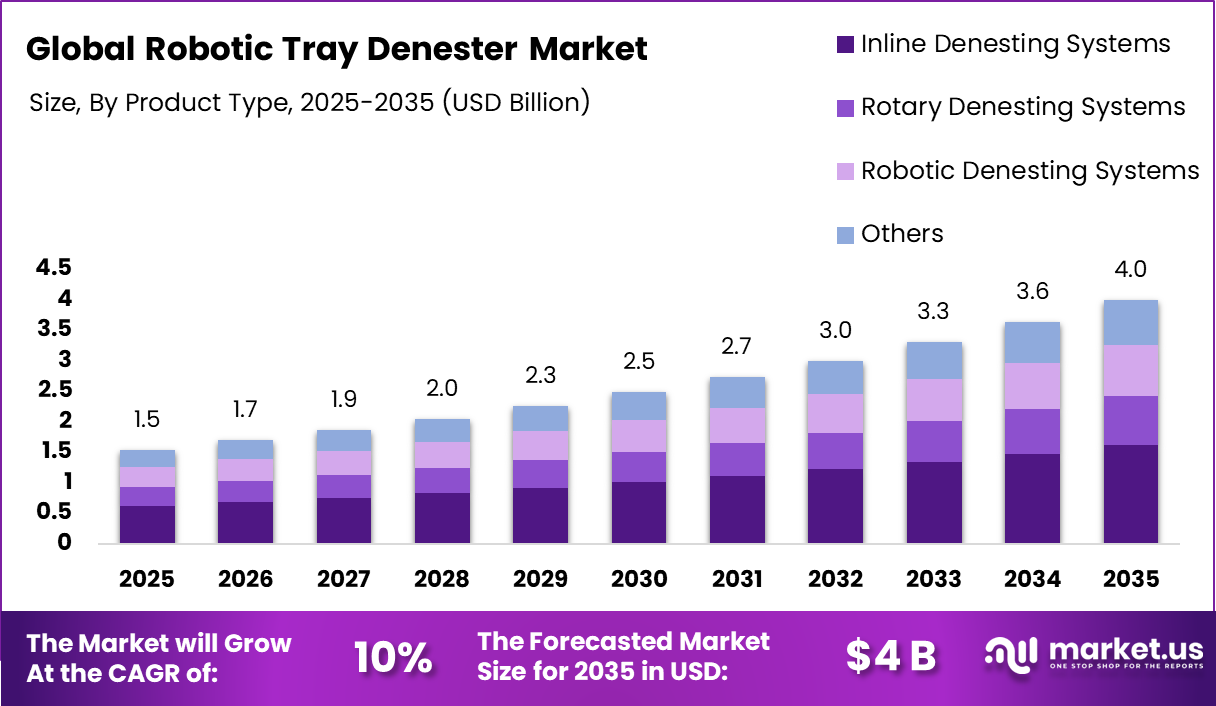

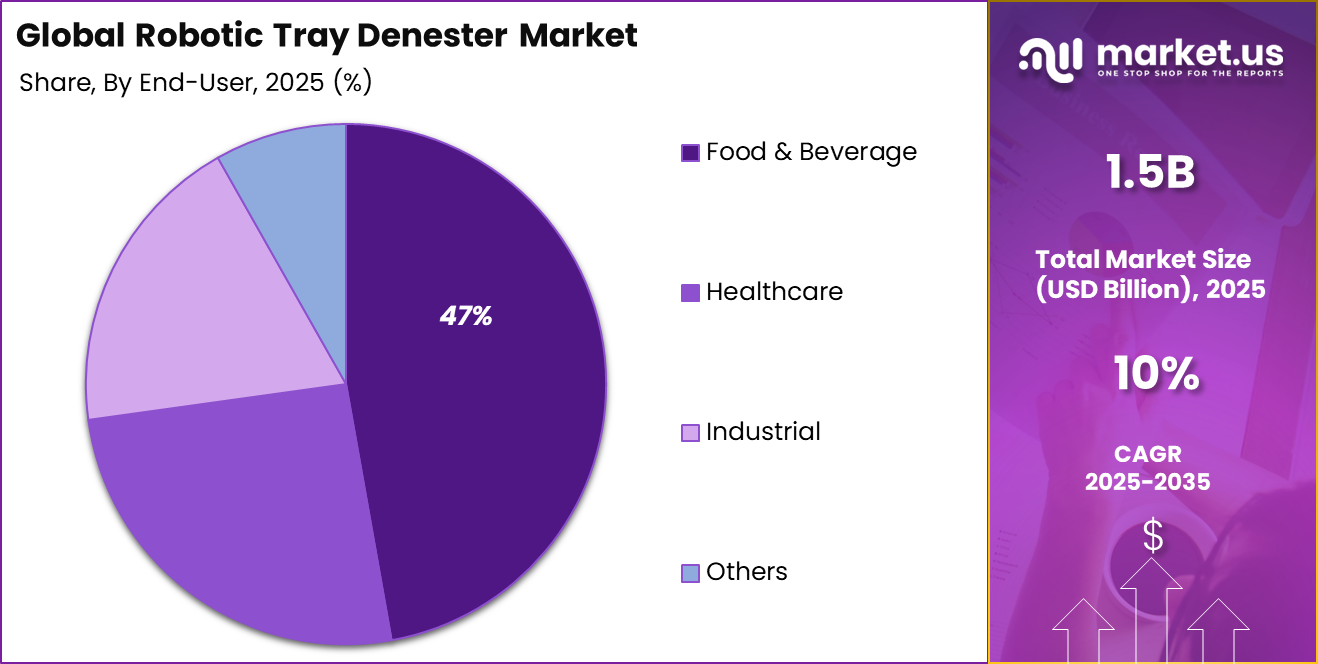

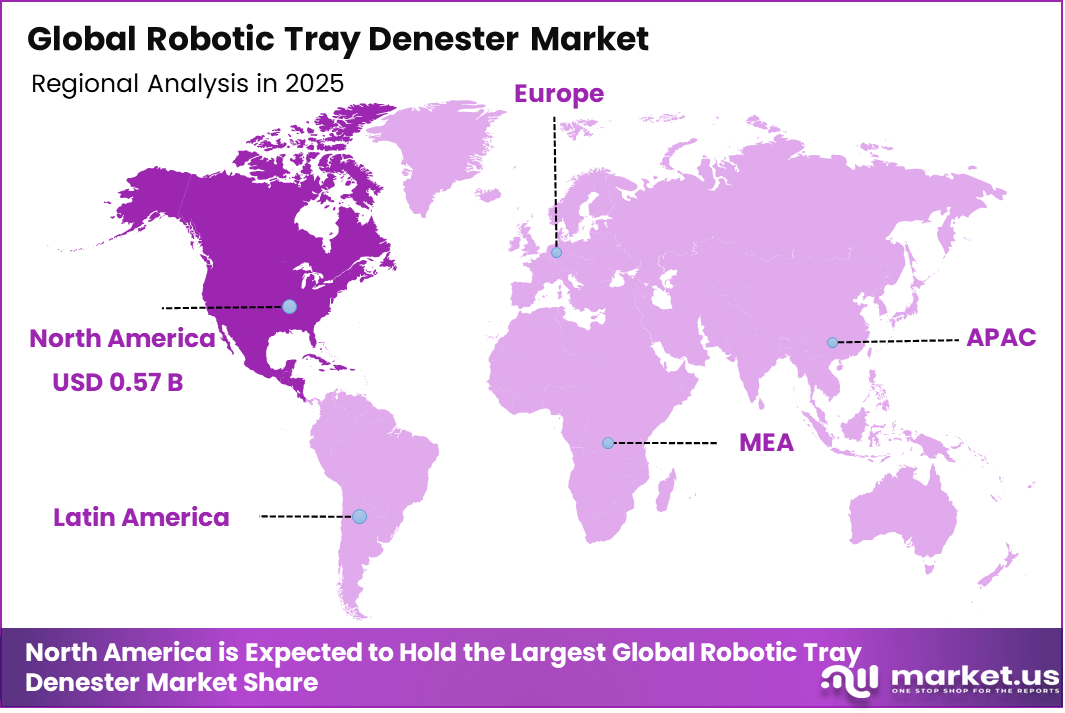

The Global Robotic Tray Denester Market generated USD 1.5 billion in 2025 and is predicted to register growth from USD 1.7 billion in 2026 to about USD 4 billion by 2035, recording a CAGR of 10% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 37.1% share, holding USD 0.57 Billion revenue.

Top Market Takeaways

- Product Type Inline denesting systems account for 40.7% of the Robotic Tray Denester market, as they are widely used to automatically separate and feed trays directly into production lines for higher speed and efficiency.

- Application Food processing represents 42.6% of the market, because tray denesters are heavily used for handling packaging trays in meat, bakery, ready meals, and other food products.

- End-User The food and beverage sector makes up 47.2% of demand, reflecting strong adoption of automated tray handling to improve hygiene, reduce labor, and increase throughput.

- Distribution Channel Direct sales account for 55.2%, as many manufacturers prefer to purchase denesting systems directly from OEMs for customized solutions, service, and integration support.

- Region North America holds 37.1% of the global market, supported by advanced food processing industries and strong adoption of automation.

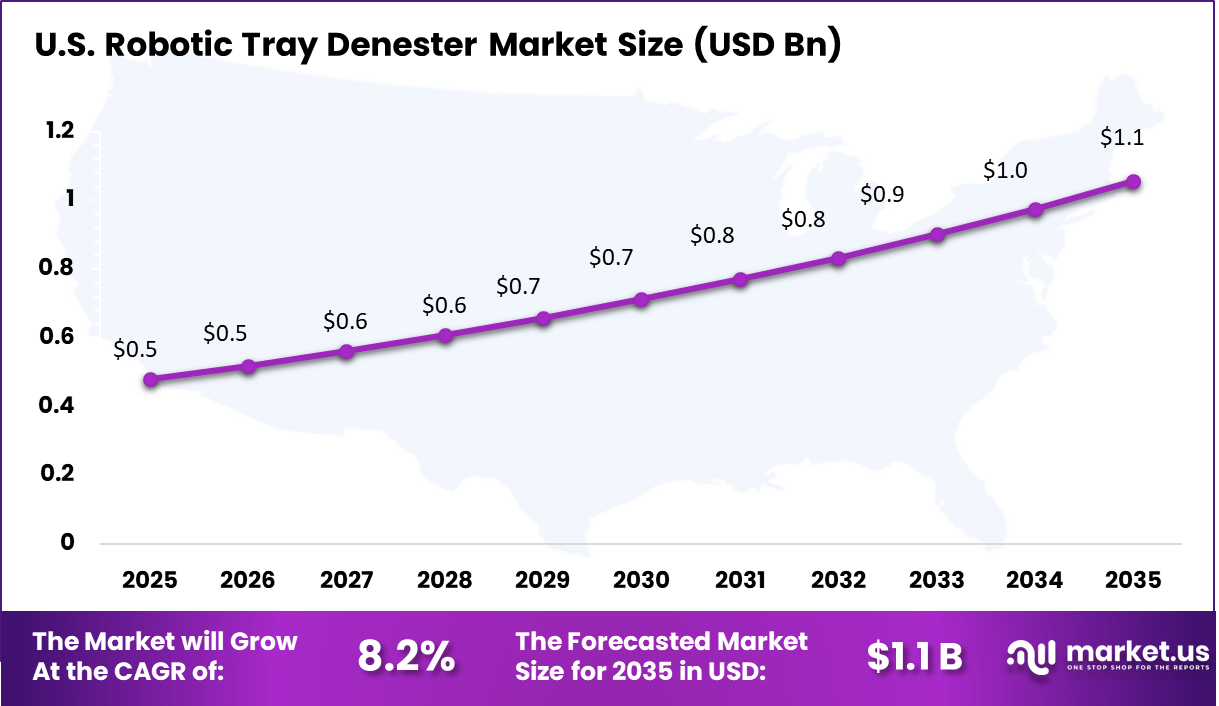

- Country The US market is valued at USD 0.48 billion and is expected to grow at a CAGR of 8.2%, driven by increasing investments in automated packaging lines and food safety compliance.

Robotic tray denesters are automated systems used to separate stacked trays and place them accurately onto production or packaging lines. These machines are widely used in food processing, pharmaceuticals, logistics, and consumer goods industries where trays are needed for filling, sorting, or transport.

By replacing manual tray handling, robotic denesters help improve speed, consistency, and hygiene while reducing labor dependency. As production facilities focus on higher throughput and reliable automation, tray denesting systems are becoming an important part of modern material handling operations.

One of the main driving factors is the increasing demand for automation in high volume manufacturing and packaging environments. Companies are looking for ways to reduce repetitive manual tasks, lower handling errors, and maintain steady production flow.

In addition, stricter hygiene standards in food and healthcare sectors are encouraging the use of touch free automated systems. The rise of flexible manufacturing is also supporting adoption, as robotic denesters can handle multiple tray sizes and formats with faster changeovers. Growing labor shortages in many industrial markets are further pushing investment in automated tray handling solutions.

Demand for robotic tray denesters is rising as manufacturers seek efficient and space saving equipment for production lines. There is a strong preference for systems that offer precise placement, gentle tray handling, and easy integration with conveyors, fillers, and robotic cells. Buyers are also looking for machines with low maintenance needs, quick format adjustments, and user friendly controls.

The demand is particularly strong among food packaging plants, pharmaceutical facilities, warehouses, and contract manufacturing sites where speed and consistency are critical. As factories continue to modernize, the need for dependable and intelligent tray denesting solutions is expected to grow steadily.

Drivers Impact Analysis

| Key Driver | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| Rising automation in food packaging and processing lines | +3.1% | North America, Europe, Asia Pacific | Medium term | Automated lines increase denester demand |

| Growing demand for hygienic and contactless material handling | +2.8% | Global | Short to medium term | Hygiene focus supports robotic systems |

| Expansion of ready-to-eat and packaged food production | +2.6% | North America, Asia Pacific, Europe | Medium to long term | Packaged food growth boosts tray handling needs |

| Need for higher throughput and labor cost reduction | +2.3% | Global | Medium term | Robotics improves speed and efficiency |

| Increasing adoption in pharmaceuticals and consumer goods | +2.0% | Developed markets | Medium to long term | New sectors widen application scope |

Restraints Impact Analysis

| Key Restraint | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| High upfront equipment and integration costs | -2.7% | Emerging markets | Short to medium term | Costs slow adoption |

| Complexity in handling varied tray sizes and materials | -2.3% | Global | Medium term | Customization raises deployment time |

| Limited awareness among small manufacturers | -1.9% | Developing regions | Medium term | Smaller firms adopt slowly |

| Maintenance needs and technical downtime risks | -1.6% | Global | Medium to long term | Downtime impacts productivity |

| Shortage of skilled automation technicians | -1.4% | Global | Long term | Skill gaps affect servicing |

By Product Type Analysis

The inline denesting systems segment accounted for 40.7% of the market share, reflecting its strong role in supporting continuous and high-speed production lines. This dominance is supported by the growing demand for automated systems that can separate and place trays accurately without interrupting workflow. Inline configurations are widely preferred in processing environments where speed, consistency, and smooth integration with conveyors are essential.

Another factor driving this segment is the need to reduce manual handling and improve operational efficiency. Inline denesting systems help lower labor dependency, minimize tray jams, and maintain consistent output quality. Their compatibility with automated packaging lines continues to strengthen adoption across industrial facilities.

By Application Analysis

The food processing segment held 42.6% share, driven by the increasing use of automation in handling, packaging, and product movement operations. Food processors require hygienic and reliable tray denesting systems to maintain production efficiency and meet strict quality standards. Robotic solutions help improve speed while reducing direct human contact with packaged items.

In addition, rising demand for packaged and ready-to-eat food products has increased production volumes across processing plants. Manufacturers are investing in automated tray handling systems to improve throughput, reduce waste, and maintain consistent packaging operations.

By End-User Analysis

The food and beverage segment captured 47% of the market, reflecting its strong need for efficient tray handling across production and packaging facilities. Companies in this sector rely on denesting systems to support large-scale operations involving meals, snacks, beverages, and fresh products. Automation helps improve consistency and operational productivity.

Furthermore, the industry faces increasing pressure to meet high consumer demand while maintaining hygiene and product quality. Robotic tray denesters reduce manual intervention and support faster line speeds, reinforcing strong adoption among food and beverage manufacturers.

By Distribution Channel Analysis

The direct sales segment accounted for 55.2% of the market share, driven by the technical nature of robotic denesting systems and the need for customized purchasing decisions. Buyers often prefer dealing directly with manufacturers to receive tailored solutions, installation planning, and system integration support. This approach improves confidence in capital equipment investments.

Moreover, direct sales channels provide better after-sales service, maintenance support, and training for operators. Businesses value close supplier relationships when purchasing automation systems that require long-term performance and operational reliability. This has strengthened the leading position of direct sales in the market.

Investor Type Impact Analysis

| Investor Type | Growth Sensitivity | Risk Exposure | Geographic Focus | Investment Outlook |

|---|---|---|---|---|

| Venture capital firms | Moderate | High | US, Europe | Investing in packaging automation startups |

| Private equity firms | Moderate to high | Moderate | North America and Europe | Scaling industrial automation suppliers |

| Corporate investors | High | Moderate | Global | Strategic investments in smart packaging lines |

| Institutional investors | Moderate | Low to moderate | Developed markets | Prefer stable industrial equipment firms |

| Government and public funding bodies | Moderate | Low | Global | Supporting manufacturing modernization |

Technology Enablement Analysis

| Technology | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| Vision-guided robotic pick-and-place systems | +3.3% | Global | Medium to long term | Improves tray detection accuracy |

| AI-based motion and cycle optimization | +2.9% | US, Europe, Asia Pacific | Medium term | Enhances throughput efficiency |

| Servo-driven precision handling systems | +2.5% | Developed markets | Medium to long term | Enables smooth tray separation |

| IoT-based predictive maintenance platforms | +2.2% | Global | Medium term | Reduces downtime risks |

| Collaborative robot integration | +1.9% | Global | Long term | Supports flexible production lines |

Key Challenges

- High equipment cost makes adoption difficult for small manufacturers.

- Complex installation and setup require technical expertise.

- Integration challenges with existing production and packaging lines.

- Maintenance needs can increase downtime and operating costs.

- Limited flexibility for handling different tray sizes and materials.

- Risk of jams or misfeeds during high-speed operations.

- Need for skilled operators and service technicians.

- Space constraints in compact production facilities.

- Dependence on stable power and smooth line coordination.

- Slow replacement cycles delay new equipment purchases.

Emerging Trends

The robotic tray denester market is evolving toward smarter and more flexible automation systems designed to improve packaging line efficiency. One of the key emerging trends is the integration of vision systems and intelligent sensors that help robots identify tray position, orientation, and stack conditions with greater accuracy. This reduces jams and improves continuous line performance.

Another important trend is the shift toward multi format denesting systems that can handle different tray sizes and materials with minimal changeover time, which is highly valuable for manufacturers managing varied product lines. There is also growing adoption of hygienic and washdown ready designs, especially in food processing environments where sanitation standards are strict. In addition, collaborative robotic solutions are gaining traction, allowing safer interaction between automation systems and human operators in compact facilities. Remote monitoring and predictive maintenance tools are also becoming more common, helping reduce unexpected downtime.

Growth Factors

The growth of this market is driven by the increasing need for labor efficiency and consistent throughput in packaging operations. Manufacturers are facing pressure to improve productivity while reducing reliance on repetitive manual handling tasks, which is encouraging investment in automated denesting systems. The expansion of ready to eat meals, fresh produce packaging, and convenience food categories is also supporting demand for faster tray handling solutions.

Another major factor is the need to reduce product contamination risks and maintain clean production environments, where robotic systems offer clear operational advantages. Companies are also focusing on minimizing packaging line stoppages and improving output accuracy, further strengthening adoption. Additionally, the broader move toward smart factories and automated material handling is creating long term opportunities for robotic tray denesters across food, healthcare, and industrial packaging applications.

Key Market Segments

By Product Type

- Inline Denesting Systems

- Rotary Denesting Systems

- Robotic Denesting Systems

- Others

By Application

- Food Processing

- Packaging

- Pharmaceuticals

- Bakery & Confectionery

- Others

By End-User

- Food & Beverage

- Healthcare

- Industrial

- Others

By Distribution Channel

- Direct Sales

- Distributors

- Online Sales

Regional Analysis

North America accounted for 37.1% of the Robotic Tray Denester market, supported by strong automation adoption across food processing, packaging, and manufacturing industries. The region has a mature industrial ecosystem where companies are investing in robotic systems to improve production speed, reduce labor dependency, and maintain consistent handling accuracy.

Robotic tray denesters are increasingly used to separate and place trays efficiently in high-volume operations, helping businesses improve workflow efficiency and hygiene standards. In addition, rising demand for automated packaging lines and smart factory solutions is strengthening market growth across the region.

The U.S. market reached USD 0.48 Billion and is projected to grow at a CAGR of 8.2%, driven by increasing need for efficient material handling and automated production systems. Manufacturers are adopting robotic tray denesters to reduce manual intervention, lower operational errors, and enhance throughput in fast-paced environments.

Growth in packaged food production, e-commerce fulfillment, and consumer goods manufacturing is also supporting demand for automated tray handling equipment. In addition, continued investments in robotics and industrial modernization are expected to support steady growth of the market in the US over the coming years.

Key Regions and Countries

-

-

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

- North America

-

Competitive Analysis

The competitive landscape of the Robotic Tray Denester Market is driven by global automation companies and packaging machinery specialists. Companies such as ABB Ltd., Yaskawa Electric Corporation, Fanuc Corporation, KUKA AG, Omron Corporation, and Schneider Electric SE focus on robotic systems, motion control, and factory automation technologies used in tray denesting operations.

These players provide high-speed, accurate, and reliable solutions for food processing, consumer goods, and industrial packaging lines. Their strong engineering capabilities and global service networks help them maintain a leading position in the market.

At the same time, companies such as JLS Automation, BluePrint Automation (BPA), Marel hf., Ishida Co., Ltd., SOMIC Packaging, Inc., Bosch Packaging Technology, Brillopak Ltd., Cama Group, Endoline Automation, Sidel Group, GEA Group AG, FlexLink (Coesia Group), Delkor Systems, Inc., and Fortress Technology Group compete by offering specialized packaging and end-of-line automation systems.

These players focus on flexible machine designs, easy integration, and reduced labor dependency for high-volume production lines. Competition in this market is driven by automation efficiency, hygiene standards, throughput speed, and the ability to handle different tray sizes and packaging formats.

Top Key Players in the Market

- Fortress Technology Group

- JLS Automation

- ABB Ltd.

- BluePrint Automation (BPA)

- Schneider Electric SE

- Marel hf.

- Ishida Co., Ltd.

- SOMIC Packaging, Inc.

- Yaskawa Electric Corporation

- Fanuc Corporation

- KUKA AG

- Bosch Packaging Technology

- Brillopak Ltd.

- Cama Group

- Endoline Automation

- Sidel Group

- GEA Group AG

- Omron Corporation

- FlexLink (Coesia Group)

- Delkor Systems, Inc.

- Others

Future Outlook

The future outlook for the Robotic Tray Denester Market looks positive as food processing, packaging, and manufacturing companies continue to automate production lines. The market is expected to grow with rising demand for faster handling, improved hygiene, and reduced manual labor in tray loading operations. Companies are anticipated to adopt robotic denesters to increase accuracy, lower waste, and improve production efficiency. In the coming years, advancements in robotics, machine vision, and smart factory systems are expected to make these solutions more flexible and reliable, supporting wider adoption across industries.

Recent Developments

March, 2026 – Fortress Technology Group is highlighted in packaging‑automation overviews as a supplier integrating product inspection with upstream and downstream tray‑handling equipment to reduce waste and rework on high‑speed lines. Its systems are increasingly paired with robotic denesters and packers in food plants that want both metal detection/x‑ray and automated tray presentation.

March, 2026 – ABB Ltd. features prominently in global packaging‑robot reports, with IRB delta and articulated robots used to load and pack trays at speeds above 50 cycles per minute. ABB’s latest software and vision options are designed so integrators can add tray‑denesting and loading cells quickly into existing food and pharma lines.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.5 Billion |

| Forecast Revenue (2035) | USD 4 Billion |

| CAGR(2025-2035) | 10% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2024 |

| Forecast Period | 2025-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Product Type (Inline Denesting Systems, Rotary Denesting Systems, Robotic Denesting Systems, Others), By Application (Food Processing, Packaging, Pharmaceuticals, Others), By End-User (Food & Beverage, Others), By Distribution Channel (Direct Sales, Distributors, Online Sales) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | Fortress Technology Group, JLS Automation, ABB Ltd., BluePrint Automation (BPA), Schneider Electric SE, Marel hf., Ishida Co., Ltd., SOMIC Packaging, Inc., Yaskawa Electric Corporation, Fanuc Corporation, KUKA AG, Bosch Packaging Technology, Brillopak Ltd., Cama Group, Endoline Automation, Sidel Group, GEA Group AG, Omron Corporation, FlexLink (Coesia Group), Delkor Systems, Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |