Global Robot Vision Guidance Market Size, Share and Analysis Report By Component (Hardware, Software, Services), By Robot Type (Articulated Robots, Collaborative Robots, SCARA Robots, Others), By Type (2D Vision Systems, 3D Vision Systems), By Application (Material Handling, Assembly, Inspection, Packaging, Welding, Others), By Industry (Automotive, Electronics & Semiconductors, Food & Beverages, Metals & Machinery, Healthcare, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

- Published date: Feb. 2026

- Report ID: 178122

- Number of Pages: 333

- Format:

-

keyboard_arrow_up

Quick Navigation

- Robot Vision Guidance Market size

- Top Market Takeaways

- Key Insights Summary

- Report Overview

- Drivers Impact Analysis

- Restraint Impact Analysis

- By Component: Hardware

- By Robot Type: Articulated Robots

- By Type: 2D Vision Systems

- By Application: Material Handling

- By Industry: Automotive

- Regional Overview: Asia-Pacific

- Investor Type Impact Matrix

- Technology Enablement Analysis

- Key Market Segments

- Competitive Analysis

- Recent Developments

- Report Scope

Robot Vision Guidance Market size

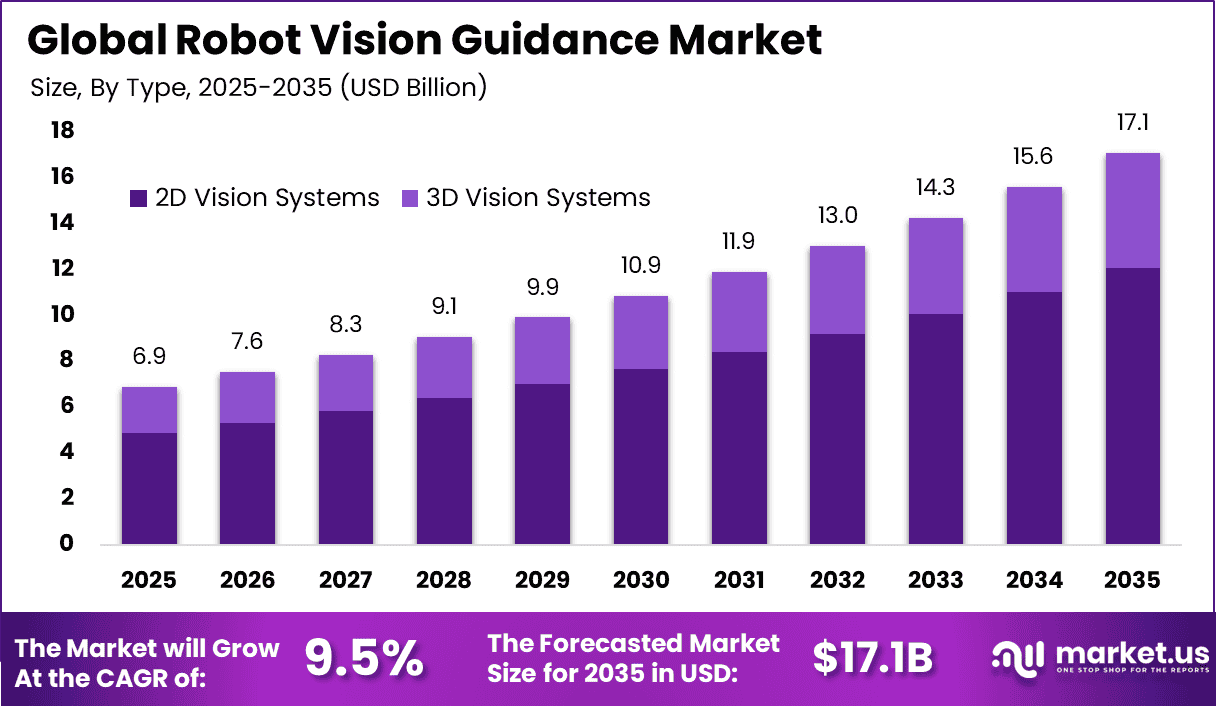

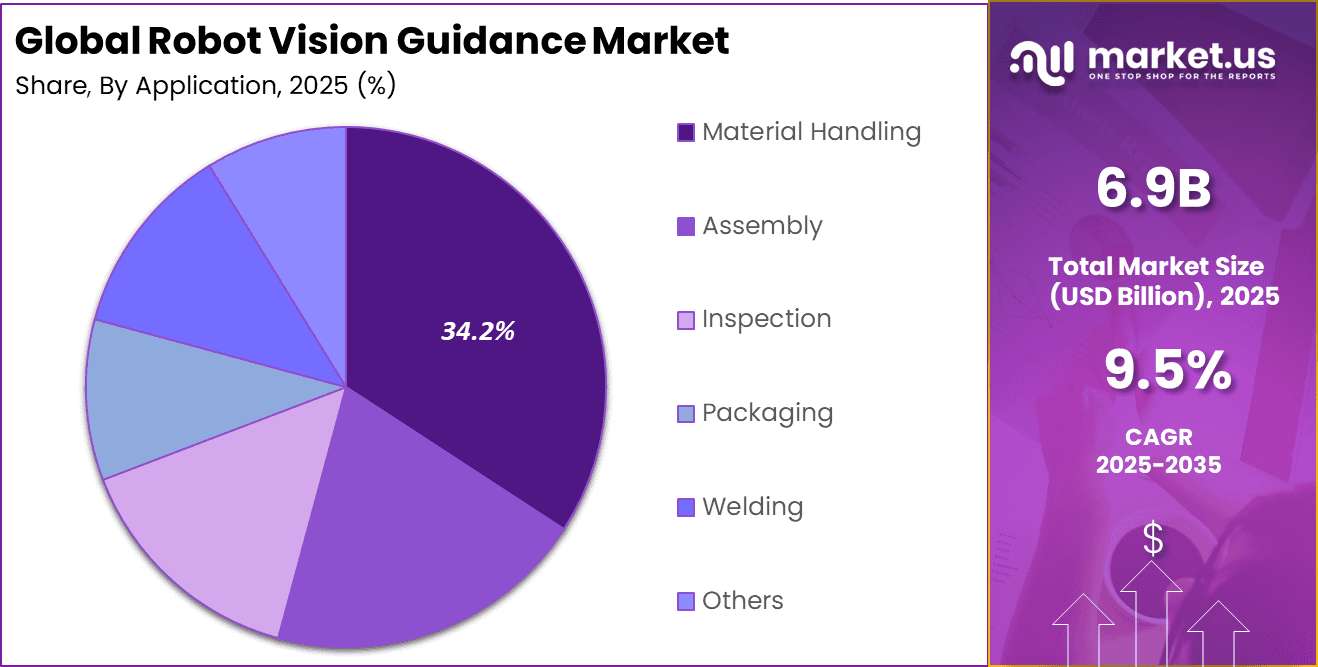

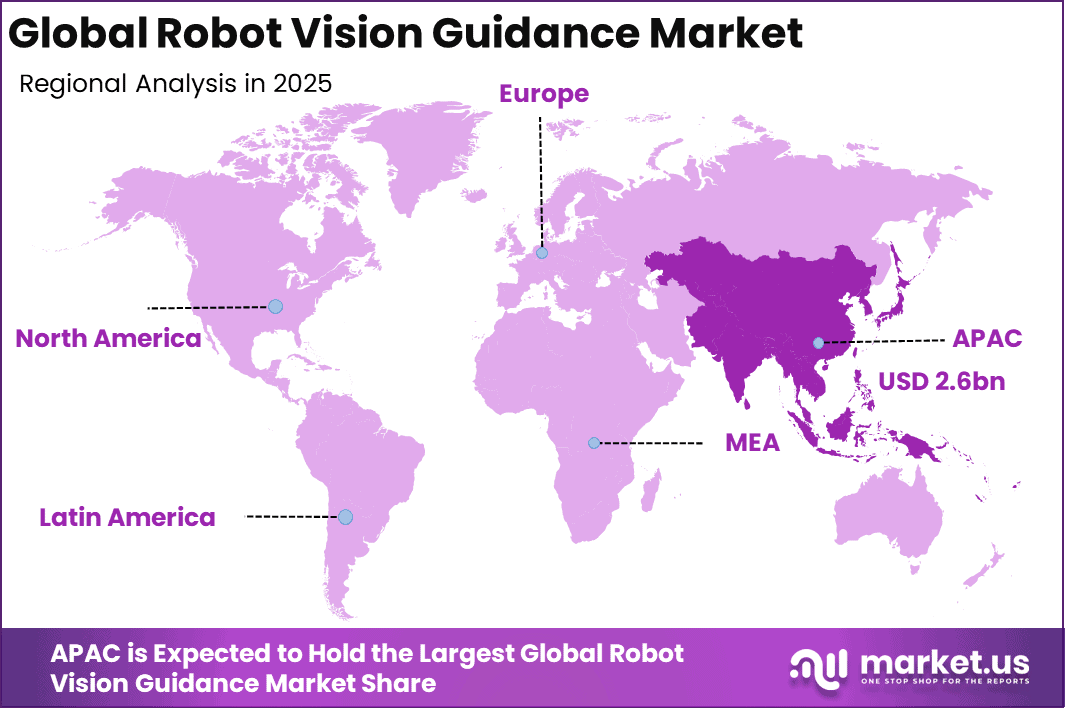

The Global Robot Vision Guidance Market size is expected to be worth around USD 17.1 Billion By 2035, from USD 6.9 billion in 2025, growing at a CAGR of 9.5% during the forecast period from 2026 to 2035. APAC held a dominant Market position, capturing more than a 38.7% share, holding USD 2.6 Billion revenue.

Top Market Takeaways

- Hardware accounted for 66.4% of total market revenue by component. High demand for cameras, sensors, controllers, and embedded vision processors continues to drive capital investment, particularly in high-speed industrial automation environments.

- Articulated Robots held a 45.3% share by robot type. Their flexibility, multi-axis movement, and compatibility with vision-guided operations make them suitable for welding, assembly, and precision inspection tasks.

- 2D Vision Systems dominated the technology landscape with a 70.6% share. Wider adoption is supported by lower implementation cost, ease of integration, and suitability for standardized manufacturing processes.

- Material Handling represented 34.2% of application demand. Increasing warehouse automation, palletizing, sorting, and pick-and-place operations have strengthened the use of vision-enabled robotic systems.

- The Automotive industry contributed 27.5% of total revenue. High automation penetration, quality inspection requirements, and precision assembly processes continue to support steady demand from automotive manufacturers.

- Asia-Pacific led the global market with a 38.7% share. Strong manufacturing output, rapid industrial automation, and supportive government policies have reinforced regional growth.

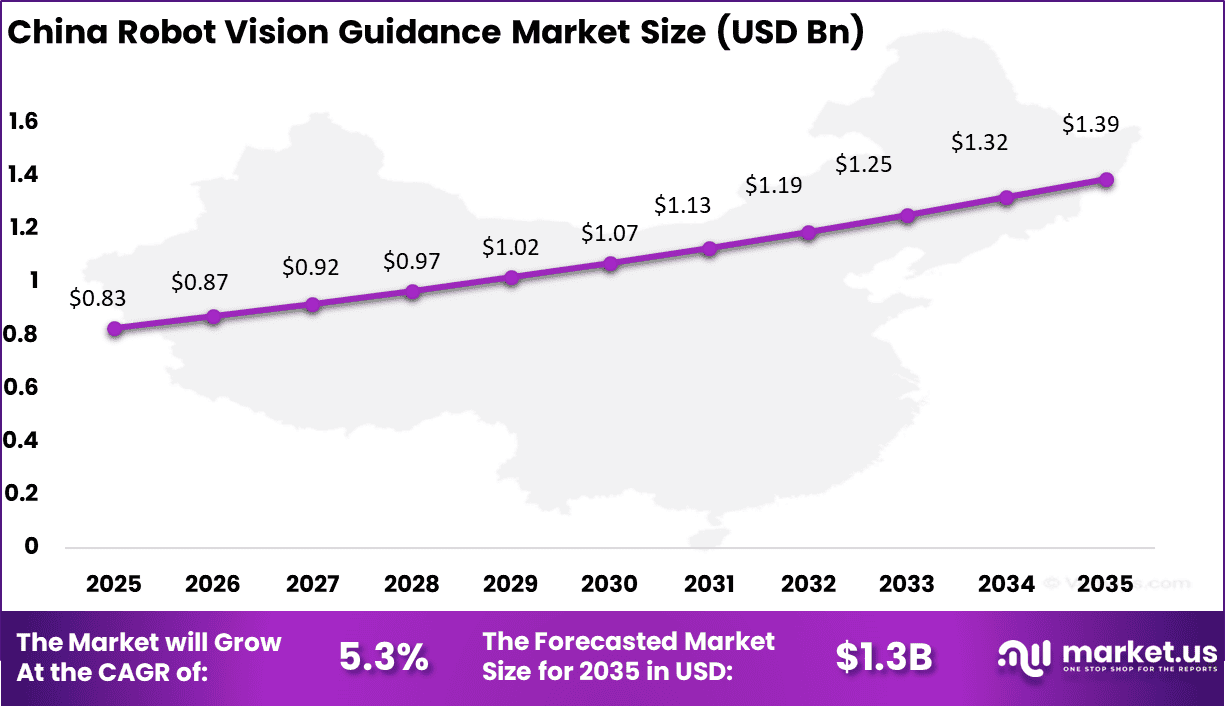

- The China market was valued at USD 0.83 Billion, expanding at a CAGR of 5.3%. Growth is supported by rising factory modernization initiatives and increased deployment of robotic systems across electronics and automotive production lines.

Key Insights Summary

- Automated vision guidance systems reduce human error rates from nearly 25% to below 2% in controlled industrial environments. This improvement enhances production reliability and reduces rework costs.

- Vision-based inspection improves defect detection performance by more than 90% compared to manual inspection methods. Higher detection rates support stronger quality assurance standards across precision manufacturing sectors.

- Advanced 3D vision systems deliver up to 25% higher picking accuracy compared to conventional 2D systems, particularly in unstructured and complex material handling operations.

- AI-enabled vision platforms have increased safety compliance rates from below 25% to above 90% in sensitive assembly environments such as airbag manufacturing. Several implementations report zero safety incidents following deployment.

- In aerospace assembly lines, vision-guided robotic cells have reduced cycle times by up to 26 seconds, while maintaining approximately 97% operational consistency. This supports higher throughput without compromising quality.

- Around 68% of manufacturing firms require a return on investment within 18 months before approving vision-guided automation projects. This reflects a strong focus on measurable financial performance.

- Automotive suppliers report nearly 40% reductions in manual inspection costs after integrating robotic vision guidance solutions. Labor optimization and lower defect rates contribute to these savings.

- Deployment and customization costs typically range between USD 50,000 and USD 200,000 per production line, depending on system complexity and integration requirements.

- The Automotive sector continues to dominate end-user demand, accounting for approximately 35.83% of total market share in 2025, supported by high automation intensity and strict quality control standards.

Report Overview

The robot vision guidance market refers to the set of technologies, hardware, and software that enable machines to interpret visual information from their environment and use this data to guide movement or decision-making. It includes systems such as cameras, sensors, image processing algorithms, and control interfaces that work together to support automated visual perception. The market has grown as industrial automation and robotics applications expand across sectors such as manufacturing, logistics, and automotive.

The integration of vision guidance enhances the ability of robots to perform tasks with higher precision and reliability. Robotic vision guidance systems make it possible for machines to detect, identify, and track objects or features within a workspace. These systems help coordinate motion, align components, and inspect quality throughout operational processes. As organisations pursue higher productivity and consistent output, visual guidance contributes to improved operational performance.

A principal factor driving the robot vision guidance market is the increasing demand for automation in industrial processes. Organisations are under pressure to improve throughput and reduce production cycle times, which encourages the adoption of visual guidance systems. These systems help reduce reliance on manual inspections and adjustments, leading to more consistent outcomes. As automation becomes more pervasive, the need for advanced vision solutions grows in parallel.

Drivers Impact Analysis

Key Driver Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline Rising automation across manufacturing and assembly lines +2.8% Asia Pacific, North America Short to medium term Increasing demand for precision and quality inspection +2.2% Europe, North America Medium term Growth of automotive, electronics, and semiconductor industries +1.9% Asia Pacific Medium term Adoption of collaborative robots in industrial settings +1.5% Global Medium term Expansion of warehouse robotics and logistics automation +1.1% North America, Europe Medium to long term Restraint Impact Analysis

Key Restraint Impact on CAGR Forecast (~%) Geographic Relevance Impact Timeline High capital investment in advanced vision systems -2.1% Emerging Markets Short to medium term Integration complexity with legacy robotic systems -1.8% Global Medium term Shortage of skilled robotics and machine vision engineers -1.6% Global Medium term Sensitivity to lighting and environmental conditions -1.3% Global Medium term Pricing pressure in competitive industrial automation markets -1.0% Asia Pacific Medium to long term By Component: Hardware

Hardware accounts for 66.4% of the robot vision guidance market, reflecting the central role of cameras, sensors, processors, and lighting systems in enabling machine perception. Vision-guided robotics depends heavily on high-resolution imaging devices and robust processing units to detect objects, measure positions, and guide movement with precision.

Industrial environments require durable hardware capable of operating in challenging conditions such as heat, dust, and vibration. As automation expands across manufacturing floors, demand for advanced imaging components continues to increase. Improvements in sensor accuracy and processing speed have strengthened hardware adoption.

High-performance cameras combined with embedded vision controllers enable faster response times and improved reliability. Integration with robotic arms and automated systems ensures accurate positioning and repeatability. Hardware upgrades are often prioritized to enhance operational efficiency and reduce downtime. This strong reliance on physical vision infrastructure explains the leading share of hardware in the market.

By Robot Type: Articulated Robots

Articulated robots represent 45.3% of the robot vision guidance segment. These robots are widely used due to their flexibility, multiple rotational joints, and ability to perform complex movements. When combined with vision guidance systems, articulated robots can precisely identify, pick, place, and assemble components.

Their adaptability makes them suitable for dynamic production lines that require frequent adjustments. This versatility contributes significantly to their market dominance. Articulated robots are commonly deployed in welding, assembly, packaging, and inspection operations. Vision systems enhance their accuracy by providing real-time feedback on object orientation and positioning.

This reduces errors and improves throughput across manufacturing processes. Industries seeking higher automation levels continue to prefer articulated robots with integrated vision capabilities. Their broad range of motion and compatibility with vision technologies support sustained demand.

By Type: 2D Vision Systems

2D vision systems account for 70.6% of the market, highlighting their widespread industrial use. These systems capture flat images to identify object shape, size, orientation, and surface features. They are widely applied in quality inspection, barcode reading, and alignment tasks.

2D systems are generally more cost-effective and easier to implement compared to advanced 3D alternatives. This balance of functionality and affordability drives strong adoption across industries. Despite advancements in 3D imaging, many industrial applications still rely on 2D systems for consistent performance.

These systems offer sufficient precision for repetitive and standardized processes. Integration with robotic controllers enables accurate guidance during pick-and-place or sorting operations. Their simplicity and reliability make them suitable for high-volume manufacturing environments. As a result, 2D vision systems maintain a significant share in the robot vision guidance market.

By Application: Material Handling

Material handling represents 34.2% of total market share. Vision-guided robots are widely used to identify, sort, and transport components within production facilities. Automated material handling improves efficiency, reduces manual labor requirements, and enhances workplace safety.

Vision systems allow robots to recognize varying object shapes and positions without predefined programming. This flexibility supports faster production cycles and improved operational consistency. In warehouses and distribution centers, vision guidance supports palletizing, depalletizing, and order fulfillment tasks.

Real-time object detection reduces errors and improves inventory accuracy. Manufacturing environments also rely on vision systems to streamline assembly line logistics. As industries focus on optimizing supply chain operations, demand for vision-enabled material handling solutions continues to grow steadily.

By Industry: Automotive

The automotive sector accounts for 27.5% of the robot vision guidance market. Automotive manufacturing requires high precision and repeatability across assembly, welding, painting, and inspection processes. Vision-guided robots enhance alignment accuracy and quality control within production lines.

The increasing adoption of electric vehicle production further supports automation investments. Manufacturers rely on vision systems to maintain consistency and reduce defect rates. Automotive facilities operate at high production volumes, where even minor inefficiencies can lead to significant losses.

Vision guidance enables rapid defect detection and component verification. Integration with articulated robots ensures precise part placement and assembly. The sector’s strong focus on automation and operational efficiency continues to drive steady adoption of robot vision technologies.

Regional Overview: Asia-Pacific

Asia-Pacific holds 38.7% of the global robot vision guidance market. The region benefits from strong manufacturing activity and increasing industrial automation initiatives. Countries across the region continue to invest in robotics to improve productivity and maintain global competitiveness.

Vision-guided systems are increasingly integrated into electronics, automotive, and heavy machinery manufacturing. This supports consistent regional demand growth. China plays a significant role within the region, with a market value of 0.83 Billion and a CAGR of 5.3%.

The country’s large-scale manufacturing ecosystem drives strong adoption of robotic systems. Government support for industrial modernization further strengthens automation deployment. Continuous investment in smart manufacturing infrastructure supports steady expansion. Asia-Pacific is expected to remain a leading hub for robot vision guidance implementation.

Investor Type Impact Matrix

Investor Type Growth Sensitivity Risk Exposure Geographic Focus Investment Outlook Industrial automation and robotics manufacturers High Medium Asia Pacific, Europe Stable hardware-driven growth Machine vision technology providers High Medium North America, Europe Value-added system expansion Semiconductor and sensor manufacturers Medium Medium Asia Pacific Component-level growth Private equity firms Medium Medium North America, Europe Consolidation of automation vendors Venture capital investors Medium High North America Innovation in AI-based vision systems Technology Enablement Analysis

Technology Enabler Impact on CAGR Forecast (~%) Primary Function Geographic Relevance Adoption Timeline 3D vision systems and depth sensing cameras +3.1% Precise object recognition Global Short to medium term AI-based image processing and pattern recognition +2.6% Enhanced accuracy North America, Europe Medium term High-speed industrial cameras and sensors +2.2% Real-time inspection Asia Pacific Medium term Edge computing integration for faster processing +1.8% Reduced latency Global Medium to long term Integration with Industry 4.0 and smart factory platforms +1.4% End-to-end automation Global Long term Key Market Segments

By Component

- Hardware

- Cameras

- Optics

- Frame Grabbers

- Processors & Controllers

- LED Lighting

- Others

- Software

- Services

By Robot Type

- Articulated Robots

- Collaborative Robots

- SCARA Robots

- Others

By Type

- 2D Vision Systems

- 3D Vision Systems

By Application

- Material Handling

- Assembly

- Inspection

- Packaging

- Welding

- Others

By Industry

- Automotive

- Electronics & Semiconductors

- Food & Beverages

- Metals & Machinery

- Healthcare

- Others

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

Global industrial robotics manufacturers such as ABB Ltd., Fanuc Corporation, Yaskawa Electric Corporation, Denso Corporation, Nachi-Fujikoshi Corporation, Mitsubishi Electric Corporation, Epson Robots, Staubli Robotics, and Midea Group integrate vision guidance into robotic arms and assembly systems. These players focus on precision, speed, and flexibility in manufacturing lines. Demand is driven by automation in automotive, electronics, and logistics sectors.

Machine vision and sensor technology providers such as Cognex Corporation, Basler AG, Keyence Corporation, SICK AG, Teledyne Technologies, Pleora Technologies Inc., and Hikvision Robotics provide high-resolution cameras and 3D imaging technologies. Their solutions enable object detection, alignment, and quality inspection. Adoption is supported by the need for accurate real-time visual feedback in automated environments.

Automation and system integration specialists such as Omron Corporation, Atlas Copco AB, Teradyne, Festo AG, TKH Technologie Deutschland AG, and Robotiq support end-to-end deployment of vision-guided robotics. These vendors emphasize collaborative robots and flexible manufacturing cells. Other players expand innovation and regional penetration, supporting steady growth in robot vision guidance systems.

Top Key Players in the Market

- ABB Ltd.

- Basler AG

- Nachi-Fujikoshi Corporation

- Denso Corporation

- Cognex Corporation

- Midea Group

- Fanuc Corporation

- Atlas Copco AB

- Omron Corporation

- Pleora Technologies Inc.

- SICK AG

- Teradyne

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Keyence Corporation

- Epson Robots

- Teledyne Technologies

- Staubli Robotics

- Festo AG

- TKH Technologie Deutschland AG

- Robotiq

- Hikvision Robotics

- Others

Recent Developments

- ABB and SICK joined forces in September 2025 on vision-guided robotics, using SICK’s PLOC2D sensor with ABB’s controllers to cut programming time and make cobots easier for everyday use.

- Epson Robots showcased AI-driven spectral vision and a 50kg payload SCARA at the International Robot Exhibition in December 2025, signaling big leaps for EV battery handling heading into 2026.

Report Scope

Report Features Description Market Value (2025) USD 6.9 Bn Forecast Revenue (2035) USD 17.1 Bn CAGR(2026-2035) 9.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Component (Hardware, Software, Services), By Robot Type (Articulated Robots, Collaborative Robots, SCARA Robots, Others), By Type (2D Vision Systems, 3D Vision Systems), By Application (Material Handling, Assembly, Inspection, Packaging, Welding, Others), By Industry (Automotive, Electronics & Semiconductors, Food & Beverages, Metals & Machinery, Healthcare, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape ABB Ltd., Basler AG, Nachi-Fujikoshi Corporation, Denso Corporation, Cognex Corporation, Midea Group, Fanuc Corporation, Atlas Copco AB, Omron Corporation, Pleora Technologies Inc., SICK AG, Teradyne, Yaskawa Electric Corporation, Mitsubishi Electric Corporation, Keyence Corporation, Epson Robots, Teledyne Technologies, Staubli Robotics, Festo AG, TKH Technologie Deutschland AG, Robotiq, Hikvision Robotics, Others Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Robot Vision Guidance MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample

Robot Vision Guidance MarketPublished date: Feb. 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- ABB Ltd.

- Basler AG

- Nachi-Fujikoshi Corporation

- Denso Corporation

- Cognex Corporation

- Midea Group

- Fanuc Corporation

- Atlas Copco AB

- Omron Corporation

- Pleora Technologies Inc.

- SICK AG

- Teradyne

- Yaskawa Electric Corporation

- Mitsubishi Electric Corporation

- Keyence Corporation

- Epson Robots

- Teledyne Technologies

- Staubli Robotics

- Festo AG

- TKH Technologie Deutschland AG

- Robotiq

- Hikvision Robotics

- Others

Our Clients

- 178122

- Feb. 2026