Global Renewable Diesel Market By Type (Pure Renewable Diesel (HVO100), Renewable Diesel Blends, Co-processed Renewable Diesel, and Others), By Feedstock (Vegetable Oils, Animal Fats, Used Cooking Oil, Algae, Tall Oil and Waste Residues, and Others), By Application (Transportation Fuel, Aviation (SAF), Marine, Industrial Use, Power Generation, and Others), By End-Use (Oil And Gas, Commercial Fleet Operators, Airlines and Aviation Authorities, Government and Defense, Marine Transport Operators, Industrial and Utility Sector, and Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2024-2034

- Published date: Mar 2026

- Report ID: 182011

- Number of Pages: 346

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

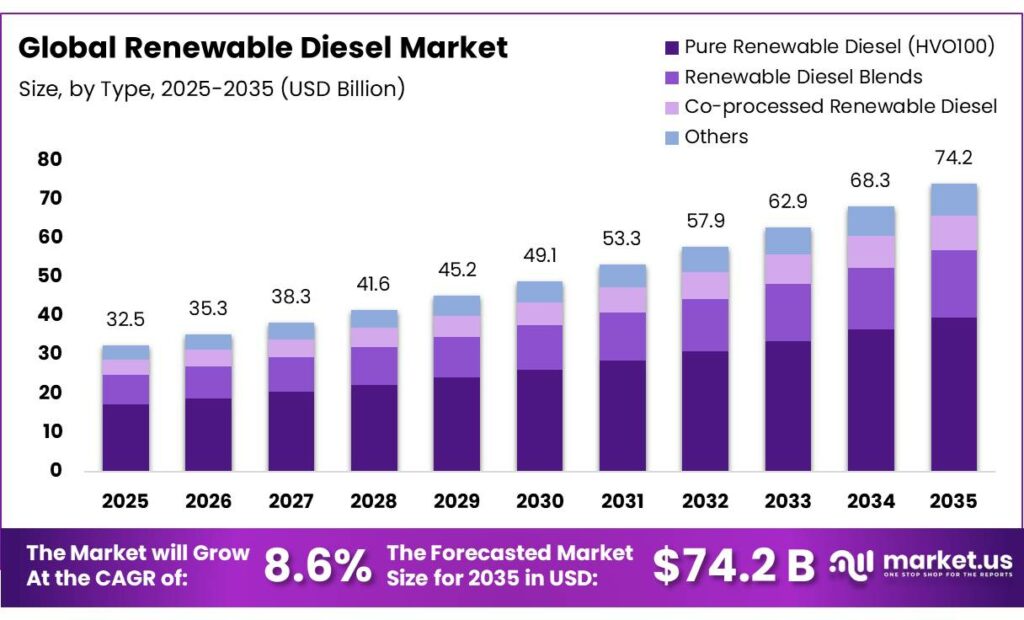

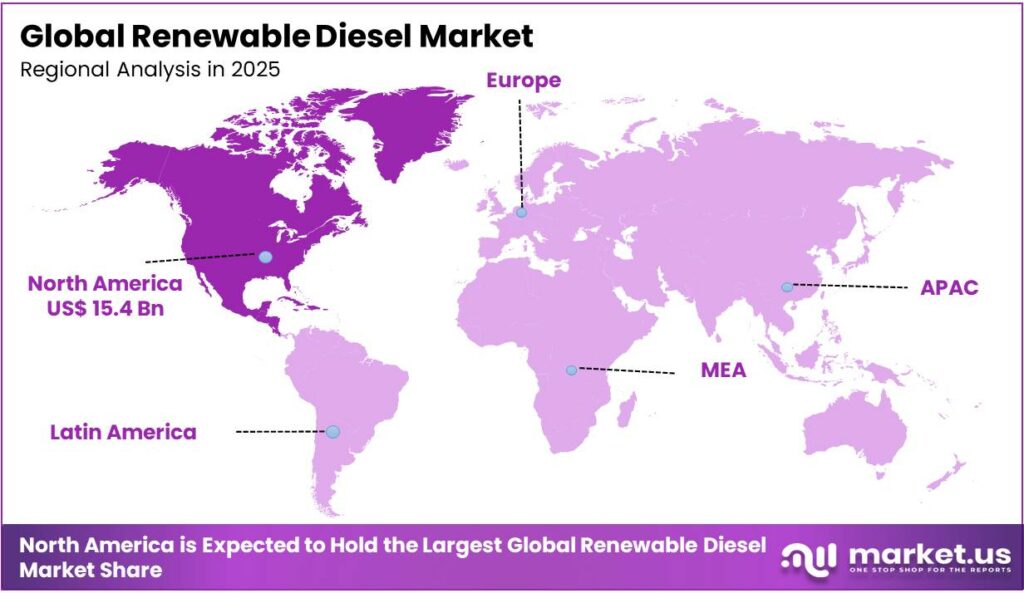

The Global Renewable Diesel Market size is expected to be worth around USD 72.4 Billion by 2035, from USD 32.5 Billion in 2025, growing at a CAGR of 8.6% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 37.9% share, holding USD 1.2 Billion revenue.

Renewable diesel, known as hydrotreated vegetable oil (HVO) or green diesel, is a non-petroleum fuel made from renewable biological resources such as vegetable oils, animal fats, and used cooking oil. The market is shaped by a combination of regulatory mandates, technological characteristics, and feedstock dynamics. North America, led by the United States, is the largest market due to extensive production capacity, federal blending mandates under the renewable fuel standard, and refinery retrofits enabling hydroprocessing of vegetable oils and waste fats.

Pure renewable diesel (HVO100) dominates usage as it is fully compatible with existing diesel engines and infrastructure, offering high cetane numbers, low sulfur content, and improved cold-weather performance. Among feedstocks, vegetable oils are preferred for their availability, consistent quality, and established supply chains, whereas animal fats, used cooking oils, and algae face logistical and processing challenges.

- According to the U.S. Energy Information Administration (EIA), U.S. renewable diesel and associated biofuel production capacity reached about 3 billion gallons per year by January 2023, surpassing biodiesel capacity of about 2.1 billion gallons per year for the first time.

Strategic adoption is concentrated in the oil and gas sector, which integrates production, processing, and distribution efficiently. Regulatory incentives and low-carbon fuel standards provide opportunities, while environmental hurdles, land-use change, energy-intensive processing, and lifecycle emissions pose constraints. Geopolitical tensions, such as supply disruptions in vegetable oils, further influence feedstock sourcing and operational costs. The market is driven by a combination of policy, infrastructure compatibility, and feedstock accessibility.

- According to the U.S. Energy Information Administration (EIA), the United States had 19 renewable diesel and associated biofuel plants with a combined production capacity of 4.72 billion gallons per year, about 308,000 barrels per day, as of January 2025.

Key Takeaways

- The global renewable diesel market was valued at USD 32.5 billion in 2024.

- The global renewable diesel market is projected to grow at a CAGR of 8.6% and is estimated to reach USD 72.4 billion by 2034.

- On the basis of types of renewable diesel, pure renewable diesel (HVO100) dominated the market, constituting 53.5% of the total market share.

- Based on the feedstock, vegetable oils dominated the renewable diesel market, with a substantial market share of around 36.5%.

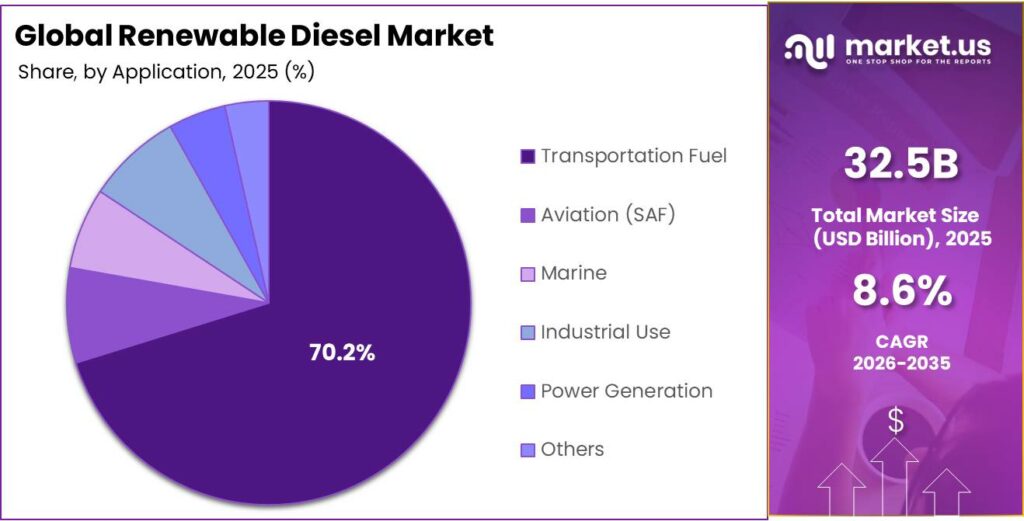

- Based on the applications, the transportation fuel led the market, comprising 70.2% of the total market.

- Among the end-uses, the oil & gas industry held a major share in the renewable diesel market, 52.8% of the market share.

- In 2024, North America was the most dominant region in the renewable diesel market, accounting for 47.4% of the total global consumption.

Type Analysis

Pure Renewable Diesel (HVO100) is a Prominent Segment in the Renewable Diesel Market.

The Renewable Diesel market is segmented based on types of renewable diesel into pure renewable diesel (HVO100), renewable diesel blends, co-processed renewable diesel, and others. The pure renewable diesel (HVO100) led the market, comprising 53.5% of the market share, as its chemical composition closely matches that of petroleum diesel, enabling direct substitution without blending constraints or engine modifications.

Unlike conventional biodiesel (fatty acid methyl esters), which is often limited to blends such as B5 or B20 due to material compatibility and cold-flow properties, HVO100 meets the same fuel specifications as petroleum diesel under standards such as ASTM D975 diesel fuel specification and EN 15940 paraffinic diesel fuel standard. This allows it to be used at 100% concentration in existing diesel engines and transported through conventional fuel pipelines and storage systems.

In addition, HVO100 offers operational advantages, including higher cetane numbers, lower sulfur and aromatic content, and improved cold-weather performance, which support engine efficiency and emissions reduction. These properties make it suitable for heavy-duty transport, aviation ground fleets, and public transport systems without requiring infrastructure or vehicle modifications.

Feedstock Analysis

Renewable Diesel Made from Vegetable Oils Dominated the Market.

On the basis of the feedstock, the renewable diesel market is segmented into vegetable oils, animal fats, used cooking oil, algae, tall oil, waste residues, and others. The renewable diesel made from vegetable oils dominated the market, comprising 36.5% of the market share, primarily due to feedstock availability, consistent quality, and established agricultural supply chains.

Oils such as soybean, rapeseed, and palm oil are produced at large commercial scales, providing a reliable and standardized input for hydroprocessing units that convert oils into renewable diesel. Their relatively uniform fatty-acid composition allows stable catalytic processing and predictable fuel yields, which simplifies refinery operations.

In contrast, feedstocks such as animal fats, used cooking oil, tall oil, or other waste residues often contain higher levels of impurities, free fatty acids, metals, or contaminants, requiring additional pretreatment before refining. These materials are logistically fragmented, as they must be collected from dispersed sources such as restaurants or food-processing facilities. Emerging feedstocks such as algae remain technologically complex and require specialized cultivation and harvesting systems. Consequently, vegetable oils provide the most consistent and scalable feedstock base for current renewable diesel production systems.

Application Analysis

Renewable Diesel Products Are Mostly Used as a Transportation Fuel.

Based on the applications of the renewable diesel, the market is divided into transportation fuel, aviation (SAF), marine, industrial use, power generation, and others. The transportation fuel dominated the renewable diesel market, with a notable market share of 70.2%, particularly in road freight and heavy-duty vehicles, as it is chemically similar to petroleum diesel and can be used directly in existing compression-ignition engines and fuel distribution systems.

Renewable diesel meets established diesel specifications such as ASTM D975 diesel fuel specification and EN 15940 paraffinic diesel fuel standard, allowing it to function as a drop-in fuel without modifications to vehicles, storage infrastructure, or refueling networks. This compatibility supports immediate deployment across large diesel-powered transport fleets.

By contrast, aviation fuels must comply with specialized certification requirements such as ASTM D7566 aviation turbine fuel specification, and sustainable aviation fuel (SAF) is typically blended with conventional jet fuel rather than used at 100% concentration. Marine, industrial, and power-generation sectors often use alternative fuels such as heavy fuel oil, liquefied natural gas, or natural gas–based systems, which limit direct substitution. Consequently, road transportation offers the most straightforward and scalable application for renewable diesel use.

End-Use Analysis

The Oil & Gas Industry Held a Major Share of the Renewable Diesel Market.

Among the end-uses, 52.8% of the total global consumption of renewable diesel is in the oil and gas industry, as this sector controls both production infrastructure and fuel distribution networks, enabling seamless integration of renewable diesel into existing refinery and pipeline systems. Refineries can co-process or upgrade renewable feedstocks within conventional units, and the resulting diesel can be directly blended or sold through established wholesale and commercial channels. In contrast, commercial fleets, aviation, marine transport, government and defense, and industrial or utility sectors often rely on externally procured fuels and may face logistical constraints, regulatory approvals, or blending limitations.

The oil and gas industry benefits from direct access to feedstocks, production facilities, and compliance mechanisms under renewable fuel standards, allowing renewable diesel to be deployed at scale efficiently. This combination of control over the supply chain and technical compatibility with existing infrastructure explains the sectoral concentration of renewable diesel usage.

Key Market Segments

By Type

- Pure Renewable Diesel (HVO100)

- Renewable Diesel Blends

- Co-processed Renewable Diesel

- Others

By Feedstock

- Vegetable Oils

- Soybean Oil

- Palm Oil

- Canola Oil

- Others

- Animal Fats

- Used Cooking Oil

- Algae

- Tall Oil and Waste Residues

- Others

By Application

- Transportation Fuel

- Aviation (SAF)

- Marine

- Industrial Use

- Power Generation

- Others

By End-Use

- Oil & Gas

- Commercial Fleet Operators

- Airlines and Aviation Authorities

- Government & Defense

- Marine Transport Operators

- Industrial & Utility Sector

- Others

Drivers

Decarbonization Goals Drive the Renewable Diesel Market.

Decarbonization mandates and the technical compatibility of renewable diesel as a drop-in fuel are key structural drivers of the renewable diesel market. Renewable diesel is a hydrocarbon fuel produced from biological feedstocks such as vegetable oils, animal fats, and recycled greases, and it meets the same ASTM D975 fuel specification as petroleum diesel. As its molecular structure is similar to fossil diesel, it can be used in existing diesel engines and distribution infrastructure without modification. Similarly, the decarbonization policies have expanded demand for low-carbon fuels.

Under the U.S. renewable fuel standard (RFS), biomass-based diesel fuels, including renewable diesel, must achieve at least a 50% lifecycle greenhouse-gas reduction relative to petroleum diesel. The renewable diesel can deliver lower greenhouse gas emissions compared with conventional diesel. These emission reductions enable transport-sector compliance with climate policies targeting lower carbon intensity fuels.

- The U.S. biomass-based diesel production averaged 3.1 billion gallons in 2022, 4.0 billion gallons in 2023, and 4.8 billion gallons in 2024. Meanwhile, U.S. renewable diesel and related biofuel plant capacity reached 4.7 billion gallons per year across 19 plants as of January 2025.

Moreover, the drop-in property reinforces adoption as it avoids capital-intensive infrastructure retrofits typically required for alternative fuels. Renewable diesel can be blended in any proportion with petroleum diesel and transported through existing logistics systems. This compatibility reduces transition barriers for freight, heavy-duty transport, and existing fuel networks, enabling incremental decarbonization within current diesel-based mobility systems.

Restraints

Infrastructure Bottlenecks and Feedstock Scarcity Might Pose a Challenge to the Renewable Diesel Market.

The environmental constraints associated with feedstock production, processing energy demand, and waste-management trade-offs present structural challenges for the renewable diesel market. Renewable diesel is commonly produced through hydroprocessed esters and fatty acids (HEFA) using vegetable oils, animal fats, or used cooking oil. However, scaling these feedstocks can generate environmental externalities across the supply chain.

According to the U.S. Environmental Protection Agency’s lifecycle framework for biofuels, emissions accounting must include feedstock cultivation, transportation, fuel production, distribution, and combustion, as well as indirect effects such as land-use change when additional cropland is brought into production.

Feedstock sourcing remains a key environmental constraint. Renewable diesel relies on agricultural oils such as soybean or palm oil, whose cultivation can expand agricultural land use and associated emissions. Lifecycle studies indicate that HEFA-based fuels derived from oil crops can generate 40-58g CO₂-equivalent per megajoule across the lifecycle, reflecting emissions from crop cultivation, transport, and processing energy inputs. These emissions vary widely depending on feedstock pathways and processing inputs, highlighting the environmental sensitivity of the supply chain.

Production processes themselves are energy-intensive. For instance, hydrothermal liquefaction and upgrading stages in waste-to-fuel pathways require electricity and natural gas inputs, contributing about 37.3 g CO₂-equivalent per MJ during fuel production in certain process models. In addition, lifecycle analyses show that some renewable diesel pathways can increase impacts such as smog formation, acidification, and eutrophication relative to conventional diesel due to agricultural inputs and fertilizer use.

Opportunities

Government Policies and Incentives Create Opportunities in the Renewable Diesel Market.

Government mandates, blending requirements, and fiscal incentives constitute a major structural opportunity for renewable diesel deployment by creating regulatory demand and lowering compliance costs for low-carbon fuels. These policies operate primarily through mandatory blending quotas, renewable fuel credits, and tax incentives linked to lifecycle emissions reductions. For instance, in the United States, the Renewable Fuel Standard (RFS) requires obligated parties to blend specified volumes of renewable fuels into the national fuel supply.

The U.S. Environmental Protection Agency set biomass-based diesel mandates at 2.82 billion gallons for 2023, 3.04 billion gallons for 2024, and 3.35 billion gallons for 2025, alongside a total renewable fuel requirement of 22.33 billion gallons in 2025. These quotas create guaranteed compliance demand for fuels such as renewable diesel that qualify as biomass-based diesel or advanced biofuel under lifecycle greenhouse-gas criteria.

Similarly, in the European Union, regulatory targets under the Renewable Energy Directive (RED II) require a minimum 14% share of renewable energy in transport by 2030, with policy revisions allowing member states to alternatively achieve at least a 14.5% reduction in transport fuel greenhouse-gas intensity or 29% renewable energy in transport energy consumption. Such targets explicitly support the deployment of low-carbon liquid fuels, including hydroprocessed renewable diesel.

Trends

Shift from Biodiesel.

A structural trend in the renewable diesel market is the gradual substitution of conventional biodiesel with hydroprocessed renewable diesel due to technical compatibility and expanding production capacity. Biodiesel, which is fatty acid methyl esters, differs chemically from petroleum diesel and is commonly blended at 20% concentrations (B20) in diesel engines, whereas renewable diesel is a hydrocarbon fuel chemically equivalent to petroleum diesel and can be used in 100% concentration (R100) without engine modifications. This functional difference has influenced refinery conversion strategies and infrastructure investment.

- The renewable diesel capacity has more than tripled, while biodiesel capacity declined by 169 million gallons per year between 2022 and 2023, equivalent to a 13% reduction.

Similarly, in Q1 2025, the U.S. renewable diesel production averaged about 170,000 barrels per day, while biodiesel output fell to roughly 70,000 barrels per day, representing a more than 30% year-on-year decline for biodiesel and a smaller 12% decline for renewable diesel. Furthermore, renewable diesel can be produced from waste oils, animal fats, and vegetable oils using hydrotreating processes similar to petroleum refining, allowing existing refinery infrastructure to be repurposed.

Geopolitical Impact Analysis

Supply Chain Disruptions in the Renewable Diesel Market Amid Geopolitical Tensions.

The geopolitical tensions, particularly the Russia-Ukraine conflict and related energy sanctions, are influencing the renewable diesel market through feedstock supply disruptions, energy-security policies, and volatility in agricultural commodity markets. The conflict has affected global vegetable-oil supply chains, which are key feedstocks for renewable diesel. Ukraine is a major exporter of sunflower oil, and attacks on its processing and port infrastructure have constrained production and exports.

The sunflower oil prices reached multi-year highs in early 2026 following supply disruptions linked to strikes on Ukraine’s vegetable oil sector and Black Sea logistics. Such price increases directly influence renewable diesel production costs, as hydroprocessed renewable diesel commonly uses vegetable oils and waste fats as primary inputs.

The geopolitical tensions have reshaped fuel trade flows and policy priorities. In response to the Russia-Ukraine war, the European Union implemented a ban on Russian diesel and other refined petroleum products in February 2023, targeting energy revenues associated with the conflict. Before the ban, Russia supplied about 10% of Europe’s diesel imports, creating an immediate need for alternative fuel sources and suppliers. Concurrently, the EU’s REPowerEU strategy aims to reduce dependence on Russian fossil fuels and accelerate renewable energy deployment, reinforcing policy support for low-carbon transport fuels, including renewable diesel.

Furthermore, geopolitical disruptions have triggered volatility in agricultural and energy commodities. Such commodity shocks propagate through biofuel supply chains by raising input costs for energy-intensive processing and agricultural feedstocks. Collectively, sanctions, feedstock supply disruptions, and commodity-market volatility link geopolitical tensions to operational conditions in the renewable diesel value chain.

Regional Analysis

North America Held the Largest Share of the Global Renewable Diesel Market.

In 2024, North America dominated the global renewable diesel market, holding about 47.4% of the total global consumption, supported by extensive production capacity, regulatory mandates, and refinery conversion projects. The United States accounts for the majority of regional activity due to federal biofuel policies and large-scale infrastructure integration. These facilities are distributed across multiple states, with major production clusters in Louisiana, 1.45 billion gallons per year, and California, 1.68 billion gallons per year, reflecting integration with existing refining infrastructure and low-carbon fuel policies.

The EIA projections indicate U.S. renewable diesel production averaging about 230,000 barrels per day in 2025, compared with 210,000 barrels per day in 2024, while consumption has been estimated at approximately 240,000 barrels per day in 2024. Federal blending mandates under the Renewable Fuel Standard require billions of gallons of biomass-based diesel annually, creating a compliance-driven market for renewable diesel fuels. Combined with refinery retrofits and feedstock availability, including soybean oil and waste fats, these regulatory and infrastructure conditions position North America, particularly the United States, as the dominant geographic hub for renewable diesel production and deployment.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of renewable diesel focus on refinery conversion and capacity expansion, where conventional petroleum refineries are retrofitted with hydrotreating units to process renewable feedstocks such as vegetable oils, animal fats, and used cooking oil. Additionally, companies prioritize feedstock diversification and long-term supply agreements to secure inputs and reduce exposure to commodity price volatility. Another key activity is vertical integration across the value chain, including feedstock collection, processing, and fuel distribution, which improves operational control and logistics efficiency.

Producers further invest in process optimization and catalyst technologies to improve conversion efficiency and reduce lifecycle emissions intensity. Strategic partnerships with logistics providers, fuel distributors, and transportation fleets support downstream adoption. Moreover, firms actively pursue regulatory certification and compliance with low-carbon fuel standards and renewable fuel programs, enabling participation in credit-based incentive mechanisms that support renewable diesel deployment in transportation fuel systems.

The Major Players in The Industry

- BP plc

- Chevron Renewable Energy Group

- Diamond Green Diesel

- ENI S.p.A.

- Neste

- Phillips 66

- Shell plc

- TotalEnergies SE

- Valero Energy Corporation

- Wilmar International

- Other Key Players

Key Development

- In January 2026, BP plc and Corteva Inc. launched a joint venture, Etlas, to produce oil from crops (canola, mustard, sunflower) for renewable diesel (RD) and sustainable aviation fuel (SAF).

- In February 2026, Eni approved another major biorefining investment. Alongside the Priolo Gargallo project, it will convert units at the Sannazzaro de’ Burgondi refinery in Pavia, Lombardy. By 2028, both biorefineries will boost Enilive’s capacity to produce HVO diesel and sustainable aviation fuel.

Report Scope

Report Features Description Market Value (2024) US$32.5 Bn Forecast Revenue (2034) US$72.4 Bn CAGR (2025-2034) 8.6% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Pure Renewable Diesel (HVO100), Renewable Diesel Blends, Co-processed Renewable Diesel, and Others), By Feedstock (Vegetable Oils, Animal Fats, Used Cooking Oil, Algae, Tall Oil and Waste Residues, and Others), By Application (Transportation Fuel, Aviation (SAF), Marine, Industrial Use, Power Generation, and Others), By End-Use (Oil & Gas, Commercial Fleet Operators, Airlines and Aviation Authorities, Government and Defense, Marine Transport Operators, Industrial and Utility Sector, and Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape BP plc, Chevron Renewable Energy Group, Diamond Green Diesel, ENI S.p.A., Neste, Phillips 66, Shell plc, TotalEnergies SE, Valero Energy Corporation, Wilmar International, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- BP plc

- Chevron Renewable Energy Group

- Diamond Green Diesel

- ENI S.p.A.

- Neste

- Phillips 66

- Shell plc

- TotalEnergies SE

- Valero Energy Corporation

- Wilmar International

- Other Key Players

Our Clients

- 182011

- Mar 2026