Global Remotely Piloted Aircraft System Market Size, Share, Growth Analysis By Component (Airframe, Payload, Avionics, Ground Control Station, Data Link, Software, Others), By Type (Rotary-Wing, Fixed-Wing, Hybrid), By Application (Military and Defense, Commercial, Civil, Homeland Security, Others), By End-User (Government, Commercial, Consumer), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Apr 2026

- Report ID: 184097

- Number of Pages: 287

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

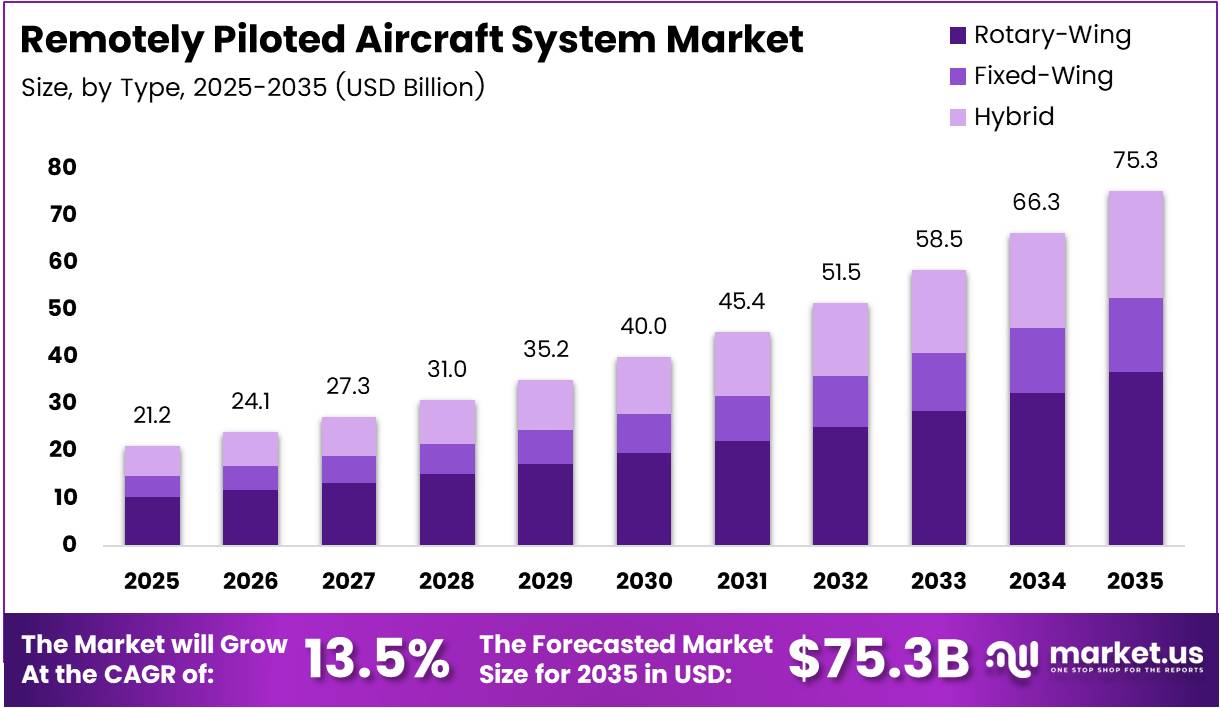

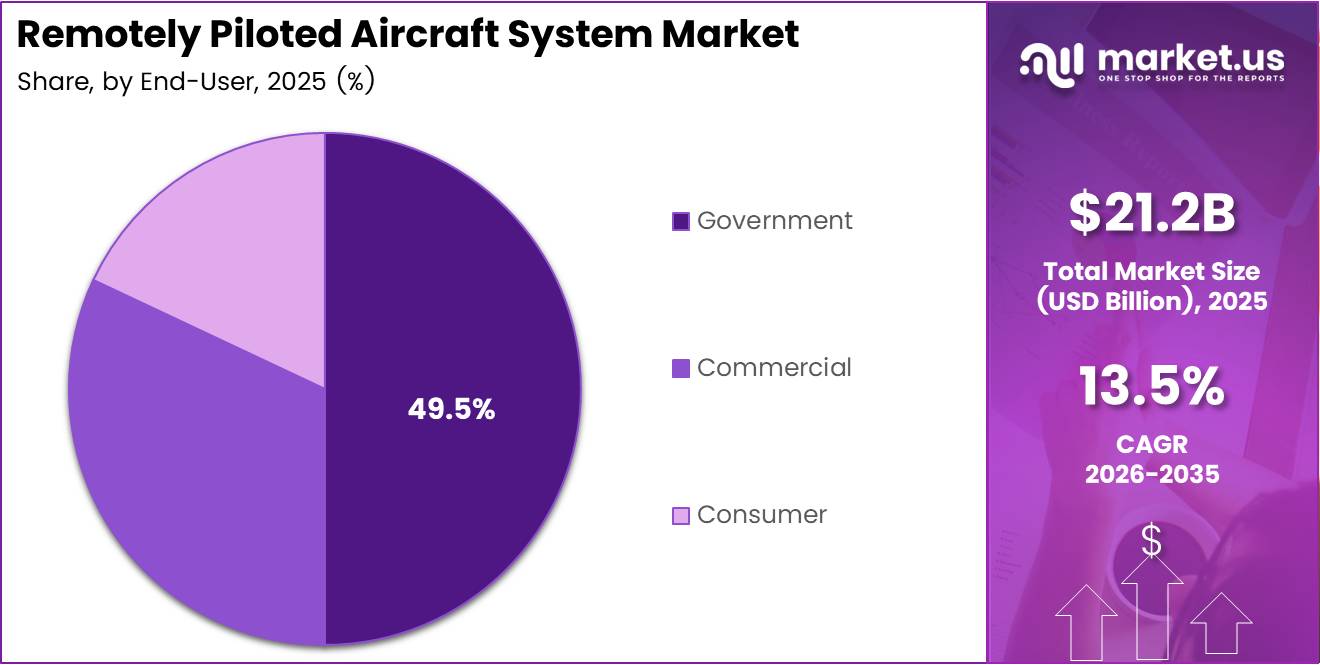

Global Remotely Piloted Aircraft System Market size is expected to be worth around USD 75.3 Billion by 2035 from USD 21.2 Billion in 2025, growing at a CAGR of 13.5% during the forecast period 2026 to 2035.

The remotely piloted aircraft system market spans unmanned aerial vehicles operated from ground control stations across military, commercial, and civil applications. RPAS platforms range from fixed-wing surveillance drones to rotary-wing delivery systems. Defense procurement, agricultural monitoring, and last-mile logistics are reshaping how governments and enterprises deploy airborne intelligence.

Defense budgets continue to redirect capital toward autonomous platforms as traditional manned aircraft costs outpace operational needs. Military RPAS procurement offers persistent surveillance, strike capability, and force multiplication at a fraction of crewed aircraft costs. This cost-performance shift makes unmanned systems a structural priority — not a discretionary upgrade — across NATO and Indo-Pacific defense postures.

Commercial RPAS adoption is accelerating beyond experimental use. Agriculture, infrastructure inspection, and delivery logistics now operate regular drone programs. BVLOS regulatory approvals from the FAA have become the clearest commercial unlock, removing the geographic ceiling that previously capped route economics for enterprise drone operators.

Government investment in RPAS infrastructure spans both procurement and regulatory reform. The FAA’s proposed Part 108 rule, published in August 2025, creates the first scalable framework for routine BVLOS operations without individual waivers — a structural shift that removes the single largest barrier to commercial drone economics at scale.

According to the DOT Office of Inspector General, the FAA had registered more than 361,000 commercial drones in the United States as of December 2023 and forecasts this number will increase to over 1 million by 2027. This near-tripling of the registered fleet signals that enterprise buyers are committing capital — not just running pilots — which compresses vendor timelines for hardware, software, and service offerings.

According to DroneLife, FAA BVLOS drone operation approvals increased from 1,229 in 2020 to 26,870 in 2023 — a 2,085% increase across waivers, air carrier certificates, and regulatory exemptions. This volume of approvals tells a clear story: commercial operators are no longer waiting for perfect regulation — they are building operational scale within current frameworks, creating first-mover advantages that latecomers will find difficult to displace.

Key Takeaways

- The Global RPAS Market is valued at USD 21.2 Billion in 2025 and is projected to reach USD 75.3 Billion by 2035, at a CAGR of 13.5%.

- By Component, Airframe leads with 32.7% market share in 2025.

- By Type, Rotary-Wing dominates with 48.6% share due to versatility in hover, takeoff, and confined-space deployment.

- By Application, Military and Defense holds the largest share at 48.3% driven by sustained defense procurement programs globally.

- By End-User, Government leads with 49.5% share across defense, border security, and public safety deployments.

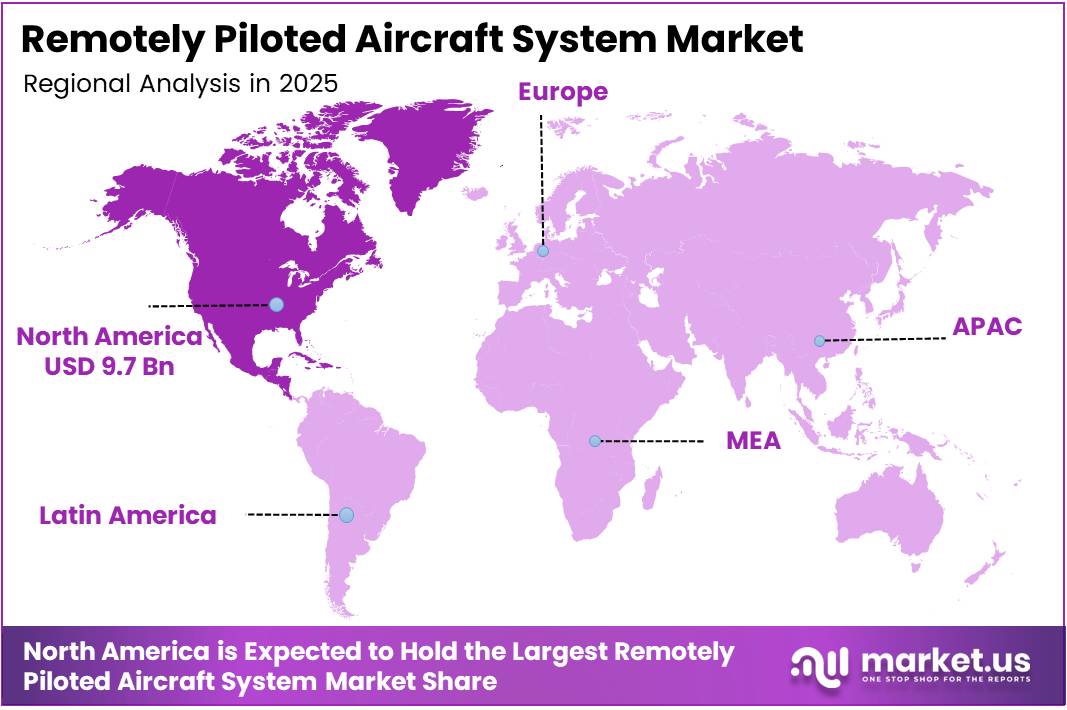

- North America dominates the global RPAS market with a 45.80% share, valued at USD 9.7 Billion.

Component Analysis

Airframe dominates with 32.7% due to structural necessity across all platform types.

In 2025, Airframe held a dominant market position in the By Component segment of the Remotely Piloted Aircraft System Market, with a 32.7% share. Every RPAS platform — military, commercial, or civil — requires an airframe as its physical foundation, making this the highest-volume component category. Structural differentiation between fixed-wing and rotary designs also drives consistent R&D investment and replacement demand.

Payload carries the highest margin within the RPAS component stack. Sensors, cameras, radar, and delivery mechanisms are application-specific — operators upgrade payloads frequently while retaining the same airframe. This creates a recurring revenue model that hardware vendors are increasingly exploiting through modular payload attachment systems and software-managed sensor switching.

Avionics serve as the intelligence layer that separates basic drones from mission-capable systems. Flight controllers, GPS modules, and inertial measurement units determine navigation accuracy and autonomous capability. As BVLOS operations scale under new FAA frameworks, avionics complexity and cost per unit will rise, rewarding suppliers with certified, interference-resistant designs.

Ground Control Station investments define operator scalability. A single GCS that manages multiple aircraft simultaneously reduces cost per flight hour and enables fleet-level operations. Defense customers in particular require ruggedized, encrypted GCS platforms — specifications that create high barriers and long procurement cycles for certified suppliers.

Data Link components determine operational range and security. Military applications require jam-resistant, encrypted waveforms; commercial operators prioritize bandwidth for real-time video transmission. As swarm operations and BVLOS routing expand, data link architecture becomes a competitive differentiator that affects mission success rates directly.

Software increasingly drives platform value beyond hardware. Flight planning, fleet management, analytics, and AI-assisted mission execution software now command premium pricing and subscription revenue. Vendors that transition from one-time hardware sales to software-enabled service models build more defensible, recurring revenue positions.

Others within the component segment include propulsion systems, batteries, and landing gear — categories where innovation is accelerating. Battery energy density improvements, such as the 410 Wh/kg cells developed by BEI, directly extend flight endurance and expand mission profiles, making this a strategically significant sub-category despite its smaller current share.

Type Analysis

Rotary-Wing dominates with 48.6% due to vertical takeoff and hover capability in constrained environments.

In 2025, Rotary-Wing held a dominant market position in the By Type segment of the Remotely Piloted Aircraft System Market, with a 48.6% share. Rotary platforms operate without runways, hover over targets, and deploy in urban, maritime, and combat environments where fixed-wing aircraft cannot function. This operational flexibility makes rotary-wing the default choice across delivery, inspection, and tactical ISR missions.

Fixed-Wing platforms differentiate through endurance and range efficiency. Fixed-wing RPAS consume significantly less power per kilometer than rotary equivalents, enabling long-duration surveillance, border patrol, and agricultural mapping missions. Military programs that require persistent area coverage — such as maritime patrol or wide-area reconnaissance — consistently favor fixed-wing designs for their superior loiter economics.

Hybrid systems bridge the capability gap between rotary and fixed-wing designs. Vertical takeoff followed by forward-flight transition delivers both deployment flexibility and endurance — a combination that suits last-mile delivery, infrastructure inspection, and search and rescue operations. Though currently the smallest type segment, hybrid platforms represent the highest R&D investment concentration as operators demand both flexibility and range.

Application Analysis

Military and Defense dominates with 48.3% due to sustained global defense procurement and ISR demand.

In 2025, Military and Defense held a dominant market position in the By Application segment of the Remotely Piloted Aircraft System Market, with a 48.3% share. Defense ministries across NATO, the Indo-Pacific, and the Middle East are replacing crewed platforms with RPAS for intelligence, surveillance, reconnaissance, and strike missions.

Poland’s Ministry of National Defence signed a $310 million contract with General Atomics Aeronautical Systems in December 2024 for three MQ-9B SkyGuardian systems — a deal that illustrates the scale of individual defense procurement events driving this segment. According to the DOT Office of Inspector General, FAA Part 135 air carrier certificate processing times for drone operators dropped from an average of 2.5 years to 6–8 months, a reduction of approximately 64–76% — a structural improvement that accelerates commercial parity with defense procurement timelines.

Commercial applications span agriculture, infrastructure inspection, media, and logistics. Commercial operators now build systematic drone programs rather than ad hoc deployments. The sector’s growth is directly tied to BVLOS regulatory progress — as approval frameworks mature, commercial route economics improve and the business case for fleet-scale investment strengthens.

Civil applications include surveying, environmental monitoring, urban planning, and law enforcement support. Civil operators often operate under different regulatory standards than commercial users, enabling faster deployment in controlled zones. This segment benefits from government budget allocations for smart city and climate monitoring programs.

Homeland Security deployments cover border surveillance, disaster response, and critical infrastructure protection. Government homeland security agencies treat RPAS as a force multiplier — one drone operator can monitor perimeters that would otherwise require dozens of ground personnel. Budget certainty and long contract cycles in this segment reduce revenue volatility for suppliers.

Others in the application segment include scientific research, telecommunications relay, and emergency communications. These use cases are growing as drone endurance improves and payload miniaturization enables multi-function platforms in a single deployment.

End-User Analysis

Government dominates with 49.5% due to defense, border security, and public safety budget commitments.

In 2025, Government held a dominant market position in the By End-User segment of the Remotely Piloted Aircraft System Market, with a 49.5% share. Defense ministries, border agencies, and law enforcement departments operate under multi-year procurement programs with predictable funding cycles. This budget certainty makes government the most stable revenue base for RPAS manufacturers and service providers, supporting premium contract pricing and long-term support agreements.

Commercial end-users include enterprises in agriculture, energy, construction, logistics, and media. Commercial adoption is volume-driven — a single agricultural operator may deploy dozens of units seasonally, while an energy company runs continuous infrastructure inspection programs. This segment offers the highest unit volume growth potential as BVLOS frameworks reduce per-flight operational costs.

Consumer end-users purchase RPAS platforms for recreational, photography, and hobbyist purposes. Consumer demand established early market volume that funded platform R&D now benefiting commercial and government users. However, regulatory tightening around consumer airspace access has moderated growth in this segment, shifting value toward professional-grade platforms even at lower price points.

Key Market Segments

By Component

- Airframe

- Payload

- Avionics

- Ground Control Station

- Data Link

- Software

- Others

By Type

- Rotary-Wing

- Fixed-Wing

- Hybrid

By Application

- Military and Defense

- Commercial

- Civil

- Homeland Security

- Others

By End-User

- Government

- Commercial

- Consumer

Drivers

Rising Defense Budgets and Commercial BVLOS Approvals Accelerate RPAS Procurement Across Military and Enterprise Markets

Defense ministries are increasing drone procurement as RPAS platforms replace crewed aircraft for ISR and strike missions at lower lifecycle cost. Agricultural and infrastructure operators are simultaneously building systematic drone programs. These two demand pools — defense and commercial — reinforce each other, creating a broad procurement base that reduces market concentration risk for manufacturers.

BVLOS regulatory approvals represent the most consequential commercial demand unlock. According to DroneLife, BVLOS construction drone operations deliver 40–60% reductions in surveying costs and a 70% decrease in data collection time, with ROI payback typically achieved within 6–8 months. These numbers shift the RPAS investment case from a long-horizon bet to a near-term capital efficiency decision — precisely the argument that converts enterprise procurement committees.

Last-mile delivery programs are translating pilot success into capital commitment. Logistics operators that demonstrated RPAS delivery economics in controlled trials are now funding permanent fleet infrastructure. This transition from trial to deployment is the key demand inflection — it signals that delivery drone operators have crossed the internal business case threshold, making RPAS investment a line-item budget decision rather than an innovation experiment.

Restraints

Airspace Regulation Gaps and Cybersecurity Vulnerabilities Constrain Commercial RPAS Scaling

Strict airspace regulations continue to cap commercial drone route density in controlled and urban environments. Operators must navigate fragmented national frameworks, temporary flight restrictions, and airspace class limitations that vary by jurisdiction. This regulatory patchwork forces enterprises to invest heavily in compliance infrastructure rather than operational expansion, compressing margin on commercial drone programs.

According to the DOT Office of Inspector General, of more than 44,000 BVLOS flights under the FAA’s BEYOND program, operators flew fewer than 763 flights — approximately 2% — without a visual observer. Furthermore, only 12.5% of lead participants achieved scalable BVLOS operations without visual observers. This data reveals that regulatory approval and operational scalability remain disconnected — having a waiver does not translate to economically viable autonomous operations at the volume commercial models require.

Cybersecurity vulnerabilities compound the regulatory challenge. Signal jamming and GPS spoofing create safety and operational risk for both commercial and military RPAS platforms. Operators must invest in encrypted data links and anti-jamming avionics to meet mission assurance standards — costs that disproportionately burden smaller commercial operators and consumer-grade platform manufacturers, tilting competitive advantage toward well-capitalized defense suppliers.

Growth Factors

AI-Enabled Autonomy, Disaster Response Deployment, and Medical Delivery Expansion Create New Revenue Streams for RPAS Manufacturers

AI-powered autonomous navigation enables multi-mission drone fleets that execute complex routes without continuous operator input. This capability shift reduces per-flight labor cost and enables simultaneous multi-aircraft operations from a single ground station. Manufacturers that embed certified autonomous flight software gain a structural cost advantage over platform-only vendors as enterprise buyers consolidate on fewer, more capable systems.

Disaster response and humanitarian logistics represent a growing addressable market with direct government funding. RPAS platforms deliver supplies, conduct damage assessment, and maintain communications in environments inaccessible to ground vehicles. The Drone Delivery Canada and Volatus Aerospace merger in August 2024 — creating Volatus Aerospace Inc. with $3.77 million in annualized cost synergies — demonstrates that operators are scaling to meet this demand through consolidation rather than organic growth alone.

Medical delivery into Africa and Southeast Asia is opening new geographic revenue pools. According to peer-reviewed research published in Cities (2025), drone delivery generates revenues 7–8 times greater than e-bike delivery, with cost recovery expected within two years. In healthcare logistics — where cold chain requirements, road infrastructure gaps, and delivery time criticality align — RPAS economics are compelling enough to attract both government health ministry contracts and private healthcare operator investment.

Emerging Trends

Hydrogen Fuel Cells, Swarm Technology, and RPAS-as-a-Service Models Are Redefining Platform Economics and Operational Architectures

Hydrogen fuel cell drones address the single largest operational constraint in current RPAS systems: flight endurance. Conventional lithium-ion batteries limit mission duration, particularly in cold environments. According to DroneLife, BEI’s next-generation battery achieves an energy density of 410 Wh/kg — enabling double the flight time and up to 70% longer distance coverage — while powering a drone for 40 minutes at −20°C, where standard lithium-ion cells failed after 10 seconds. Extended endurance directly expands viable mission profiles for military ISR, agricultural monitoring, and long-range delivery.

Swarm drone technology shifts RPAS from single-platform to networked system operations. Multiple coordinated drones executing simultaneous surveillance grids or precision agricultural spraying multiplies per-mission output without proportional cost increases. AeroVironment’s $4.1 billion acquisition of BlueHalo — a leader in counter-UAS and drone swarm technology — signals that swarm capability is now a strategic asset, not an experimental feature, with defense buyers already funding procurement.

RPAS-as-a-Service models are reducing the capital barrier for enterprise adoption. Operators accessing drone fleets on subscription or per-mission pricing avoid upfront hardware investment while retaining access to current-generation platforms. This model is particularly attractive for low-frequency commercial users — infrastructure inspectors, insurers, and event operators — who cannot justify owned fleet economics but have defined, recurring demand that service providers can profitably serve.

Regional Analysis

North America Dominates the Remotely Piloted Aircraft System Market with a Market Share of 45.80%, Valued at USD 9.7 Billion

North America holds 45.80% of the global RPAS market, valued at USD 9.7 Billion, driven by the world’s largest defense procurement programs, an established commercial drone regulatory infrastructure, and the FAA’s active BVLOS approval pipeline. The U.S. Department of Defense remains the single largest RPAS buyer globally, and domestic manufacturers benefit from proximity to both procurement decision-makers and the world’s most active commercial drone testing environments.

Europe Remotely Piloted Aircraft System Market Trends

Europe is building RPAS capacity through both defense modernization and civil drone integration programs. NATO member states are accelerating unmanned platform procurement, while the European Union Aviation Safety Agency advances a unified drone regulatory framework. Poland’s $310 million MQ-9B procurement in December 2024 illustrates the scale of individual European defense commitments now funding manufacturers across the supply chain.

Asia Pacific Remotely Piloted Aircraft System Market Trends

Asia Pacific is the fastest-expanding regional market for commercial RPAS, driven by large agricultural land areas, precision farming adoption, and government-backed smart logistics initiatives. China’s domestic manufacturers maintain a dominant share of the consumer and commercial platform market. India and Australia are expanding defense drone procurement programs, diversifying the regional demand base beyond agricultural and commercial use cases.

Middle East and Africa Remotely Piloted Aircraft System Market Trends

The Middle East drives RPAS demand through active defense procurement and border security programs in a region where persistent aerial surveillance addresses specific security geography. Africa represents an emerging humanitarian and medical delivery market, where poor road infrastructure makes RPAS the lowest-cost logistics option for reaching remote populations — a structural advantage that multilateral health programs are beginning to fund systematically.

Latin America Remotely Piloted Aircraft System Market Trends

Latin America deploys RPAS primarily for agricultural monitoring, deforestation detection, and law enforcement surveillance across large, low-density territories. Brazil and Mexico are the lead markets, with agricultural operators driving commercial adoption and federal security agencies investing in border and narcotics surveillance platforms. Infrastructure constraints and budget cycles make SaaS and RPAS-as-a-Service models particularly relevant in this region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Northrop Grumman Corporation positions itself at the intersection of advanced RPAS platforms and integrated systems. The company’s Global Hawk and Triton unmanned systems serve the long-endurance ISR segment — a category where contract values are large, switching costs are high, and buyer relationships are measured in decades. This positioning insulates Northrop from mid-market price competition while keeping it tied to defense budget cycles.

General Atomics Aeronautical Systems, Inc. owns the most commercially successful military RPAS franchise globally through the Predator and Reaper family. The December 2024 contract with Poland for three MQ-9B SkyGuardian systems — valued at $310 million — demonstrates sustained allied nation demand for proven, support-backed platforms. GA-ASI’s advantage lies in an unmatched operational track record that new entrants cannot replicate without years of deployed performance data.

DJI controls the commercial and consumer RPAS market through cost leadership and manufacturing scale that defense-focused competitors cannot match on price per unit. DJI’s strategic risk is geopolitical — U.S. and European procurement restrictions create market access constraints that domestic manufacturers are actively filling. However, in agricultural, industrial inspection, and developing market segments outside restricted procurement zones, DJI’s platform ecosystem remains the default commercial choice.

Boeing Company competes in the large military RPAS segment where integration with crewed aircraft systems and multi-domain operations architectures creates high barriers. Boeing’s MQ-25 Stingray — the first operational carrier-based unmanned tanker aircraft — extends the company’s unmanned systems position into carrier aviation, a segment with a limited number of buyers but extremely high contract values and long platform lifecycles.

Key Players

- Northrop Grumman Corporation

- General Atomics Aeronautical Systems, Inc.

- DJI (Da-Jiang Innovations Science and Technology Co., Ltd.)

- Boeing Company

- Lockheed Martin Corporation

- AeroVironment, Inc.

- Elbit Systems Ltd.

- BAE Systems plc

- Thales Group

- Leonardo S.p.A.

Recent Developments

- August 2025 — The FAA published its landmark proposed rule for BVLOS drone operations under Part 108 — the first comprehensive regulatory framework enabling routine, scalable beyond-visual-line-of-sight UAS operations in the National Airspace System without requiring individual waivers. This rule removes the most significant structural barrier to commercial RPAS economics at scale and is expected to catalyze fleet investment across logistics, agriculture, and inspection operators.

- December 2024 — Poland’s Ministry of National Defence signed a $310 million contract with General Atomics Aeronautical Systems to acquire three MQ-9B SkyGuardian remotely piloted aircraft systems, two Certifiable Ground Control Stations, and three years of global support services for the Polish Armed Forces — one of the largest single-nation RPAS procurement contracts in European defense history.

- May 2024 / October 2024 — Axon announced a definitive agreement to acquire Dedrone, the global leader in smart airspace security and counter-UAS technology, with the deal closing in October 2024. Dedrone’s AI-powered drone detection and mitigation capabilities were integrated into Axon’s public safety platform, extending counter-UAS functionality to law enforcement and critical infrastructure operators worldwide.

Report Scope

Report Features Description Market Value (2025) USD 21.2 Billion Forecast Revenue (2035) USD 75.3 Billion CAGR (2026-2035) 13.5% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Component (Airframe, Payload, Avionics, Ground Control Station, Data Link, Software, Others), By Type (Rotary-Wing, Fixed-Wing, Hybrid), By Application (Military and Defense, Commercial, Civil, Homeland Security, Others), By End-User (Government, Commercial, Consumer) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Northrop Grumman Corporation, General Atomics Aeronautical Systems, Inc., DJI (Da-Jiang Innovations Science and Technology Co., Ltd.), Boeing Company, Lockheed Martin Corporation, AeroVironment, Inc., Elbit Systems Ltd., BAE Systems plc, Thales Group, Leonardo S.p.A. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Remotely Piloted Aircraft System MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample

Remotely Piloted Aircraft System MarketPublished date: Apr 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Northrop Grumman Corporation

- General Atomics Aeronautical Systems, Inc.

- DJI (Da-Jiang Innovations Science and Technology Co., Ltd.)

- Boeing Company

- Lockheed Martin Corporation

- AeroVironment, Inc.

- Elbit Systems Ltd.

- BAE Systems plc

- Thales Group

- Leonardo S.p.A.

Our Clients

- 184097

- Apr 2026