Global Refillable Deodorants Market Size, Share, Growth Analysis By Type (Refillable Spray Deodorant, Refillable Stick Deodorant), By Packaging (Metal, Glass, Plastic, Paper, Others), By Distribution Channel (Supermarket/Hypermarket, Online, Specialty Store, Drugstores/Pharmacies, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 183139

- Number of Pages: 313

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

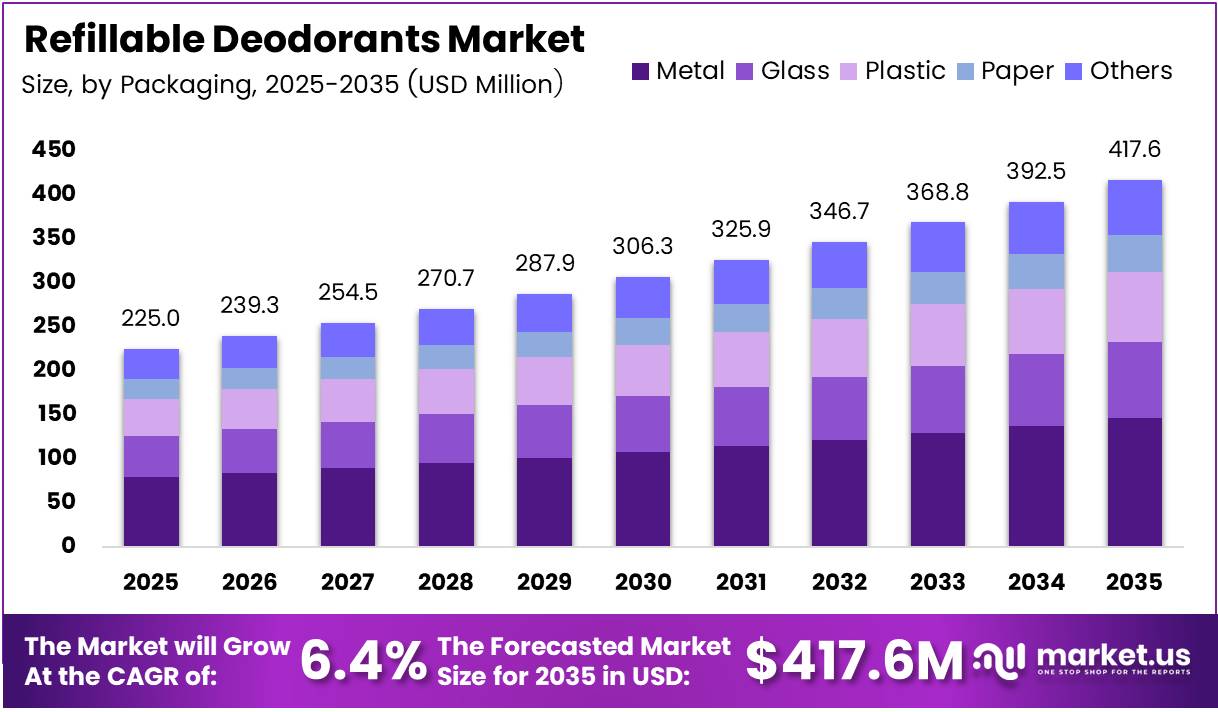

Global Refillable Deodorants Market size is expected to be worth around USD 417.6 Million by 2035 from USD 225.0 Million in 2025, growing at a CAGR of 6.4% during the forecast period 2026 to 2035.

The refillable deodorants market covers personal care products that separate a durable outer casing from replaceable inner refill units. Consumers purchase the case once, then replace only the product core — reducing packaging waste with each use cycle. This format spans spray and stick formats across metal, glass, plastic, and paper packaging.

This market sits at the intersection of personal care and sustainable packaging. Unlike conventional disposable formats, refillable systems require a deliberate purchase decision — buyers invest upfront in a reusable case. That behavioral shift separates this segment from mass-market deodorant and creates a structurally distinct buyer profile.

Consumer preference for zero-waste personal care is reshaping the competitive landscape. Eco-conscious buyers now treat packaging disposal as a product feature, not an afterthought. This shift gives refillable formats a structural advantage that disposable competitors cannot easily replicate without redesigning their entire product architecture.

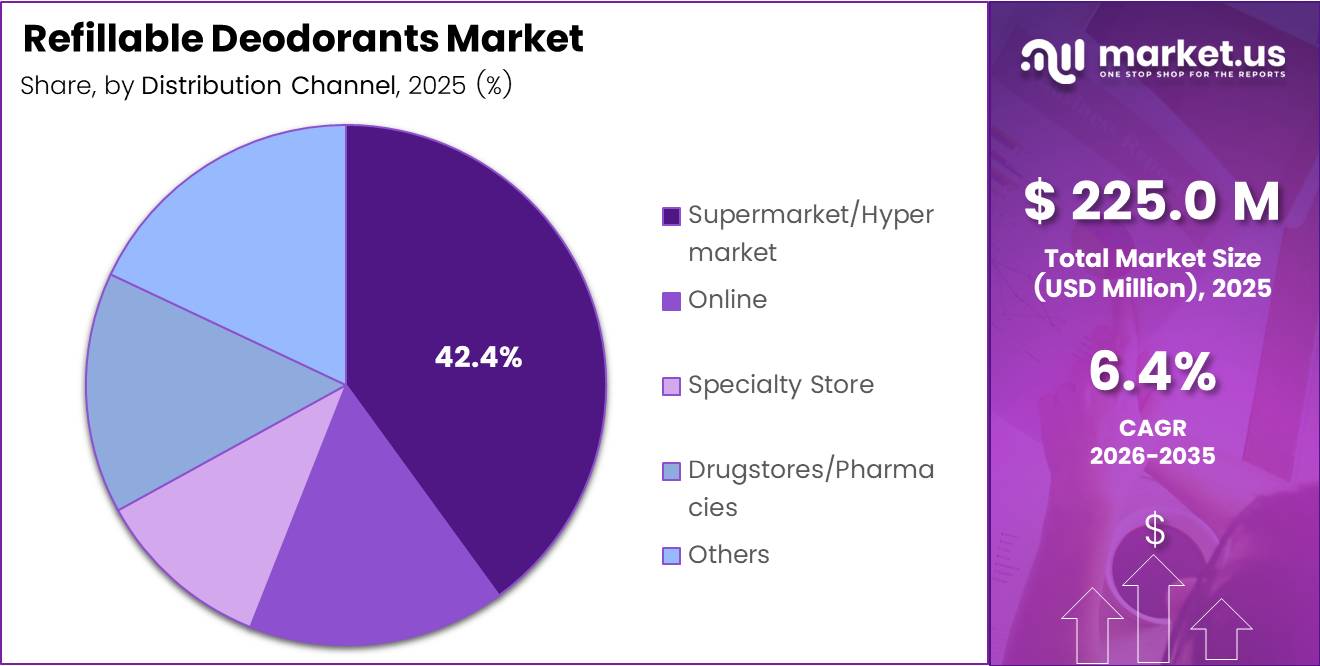

Distribution through supermarkets and hypermarkets holds a 39.2% share, confirming that refillable deodorants have moved beyond niche specialty channels. Mainstream shelf placement signals category maturity — and puts these products in direct competition with conventional deodorant SKUs for the first time at scale.

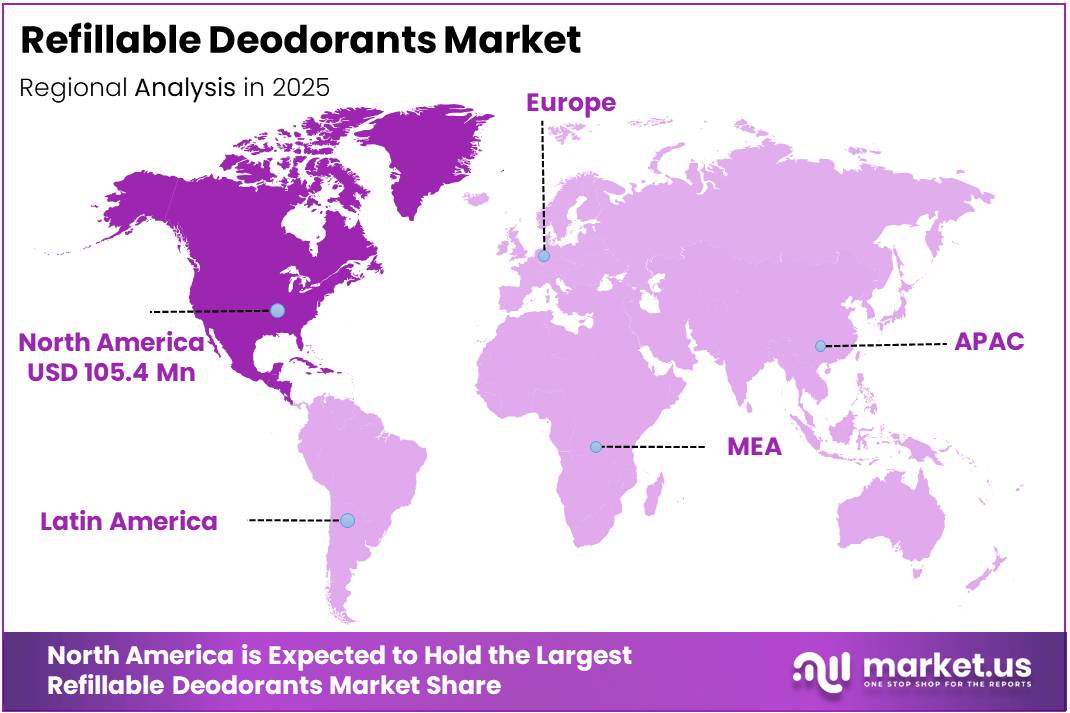

North America leads with a 46.90% share, valued at USD 105.4 million. This reflects early retailer adoption and strong consumer receptivity to premium eco-personal care formats. The region’s infrastructure for sustainability-positioned consumer goods gives refillable brands a faster path to volume compared to developing markets.

In April 2025, Unilever acquired Wild — the UK’s leading natural refillable deodorant brand — for a reported €275 million. This signals that major consumer goods companies now view the refillable format as a strategic asset rather than a niche experiment, accelerating category investment and retail negotiation power.

According to devera.ai packaging trends analysis, Dove’s stainless-steel refillable deodorant uses 54% less plastic per stick. Additionally, according to rebel.care, a typical deodorant refill uses approximately 80% less packaging material than a single-use product. Together, these metrics confirm that the sustainability case for refillable formats is quantifiable — giving brands a defensible, data-backed marketing position.

Key Takeaways

- The Global Refillable Deodorants Market was valued at USD 225.0 Million in 2025 and is forecast to reach USD 417.6 Million by 2035.

- The market grows at a CAGR of 6.4% during the forecast period 2026 to 2035.

- By Type, Refillable Spray Deodorant dominates with a 59.2% market share in 2025.

- By Packaging, Metal holds the leading position with a 34.6% share in 2025.

- By Distribution Channel, Supermarket/Hypermarket leads with a 39.2% share in 2025.

- North America dominates regional markets with a 46.90% share, valued at USD 105.4 Million in 2025.

Type Analysis

Refillable Spray Deodorant dominates with 59.2% due to familiar aerosol application format.

In 2025, Refillable Spray Deodorant held a dominant market position in the By Type segment of the Refillable Deodorants Market, with a 59.2% share. Consumers favor the spray format because it mirrors the sensory experience of conventional aerosol deodorants. This familiarity removes a key adoption barrier — buyers switch to refillable formats without changing their application behavior.

Refillable Stick Deodorant attracts buyers seeking aluminum-free and natural deodorant formulations. Stick formats align closely with clean-beauty positioning, as they typically house solid or cream-based natural formulas. However, this segment serves a narrower buyer group, limiting its volume ceiling compared to spray formats currently.

Packaging Analysis

Metal dominates with 34.6% due to premium durability and sustainability signaling.

In 2025, Metal held a dominant market position in the By Packaging segment of the Refillable Deodorants Market, with a 34.6% share. Metal cases — particularly aluminum — offer the durability required for indefinite reuse cycles. Their tactile quality also reinforces the premium positioning that refillable brands use to justify higher upfront price points against disposable alternatives.

Glass packaging targets the luxury and premium tier of the refillable deodorants category. Its higher cost and fragility limit mass-market application, but glass carries strong sustainability signals and supports brand differentiation. Consequently, glass formats serve as entry points into premium retail channels where aesthetic value drives purchase decisions.

Plastic packaging retains relevance through its lower production cost and lightweight properties. However, plastic’s association with single-use culture creates a perception conflict for sustainability-positioned brands. Therefore, brands using plastic in refillable systems typically emphasize recycled-content credentials — such as certified ocean-bound recycled plastic — to address consumer concerns.

Paper packaging represents the emerging zero-plastic frontier within refillable deodorant formats. Paper-based cases appeal to the most environmentally committed consumer segment. However, structural limitations for liquid-adjacent formulations keep paper formats confined to solid and stick product types currently.

Others in this segment include composite and bio-based materials under active development. Brands and packaging innovators explore these formats to push sustainability performance beyond conventional material options. This sub-segment is small today, but material innovation investment signals future growth in non-conventional packaging formats.

Distribution Channel Analysis

Supermarket/Hypermarket dominates with 39.2% due to mass-market shelf access and footfall.

In 2025, Supermarket/Hypermarket held a dominant market position in the By Distribution Channel segment of the Refillable Deodorants Market, with a 39.2% share. Mainstream retail placement confirms that refillable deodorants have cleared the specialty-only phase of category development. Shelf presence alongside conventional deodorant brands exposes refillable formats to a much broader, less eco-motivated consumer base — widening the addressable market.

Online channels serve as the primary acquisition and repeat-refill path for direct-to-consumer refillable brands. E-commerce enables subscription-based refill delivery models, which improve customer retention and reduce acquisition costs per repeat purchase. Additionally, online platforms support detailed sustainability storytelling that shelf packaging alone cannot communicate.

Specialty Store channels anchor the early-adopter and premium buyer segment for refillable deodorants. These retail environments attract consumers who actively research eco-personal care products. Specialty placement supports higher average selling prices and provides brands with a curated context that reinforces their sustainability credentials.

Drugstores/Pharmacies extend refillable deodorant availability to health-focused consumers. Pharmacy placement positions refillable formats alongside natural health and wellness products, creating a logical adjacency for buyers seeking aluminum-free or skin-sensitive formulations. This channel also builds category credibility through association with personal care expertise.

Others include direct brand boutiques, zero-waste refill shops, and subscription box services. These alternative channels capture the most committed eco-consumer segment. While their volume contribution remains limited, they serve as high-visibility brand-building environments that reinforce refillable deodorant credentials to influential sustainability-focused consumer communities.

Key Market Segments

By Type

- Refillable Spray Deodorant

- Refillable Stick Deodorant

By Packaging

- Metal

- Glass

- Plastic

- Paper

- Others

By Distribution Channel

- Supermarket/Hypermarket

- Online

- Specialty Store

- Drugstores/Pharmacies

- Others

Drivers

Consumer Demand for Zero-Waste Personal Care Pushes Refillable Deodorant Adoption

Consumers now treat packaging waste as a decisive purchase factor in personal care. Eco-conscious buyers actively seek formats that eliminate single-use plastic from their daily routines. Refillable deodorant systems address this directly by separating the durable case from the replaceable refill — converting a repeat-disposal habit into a circular purchase behavior.

The shift toward natural and aluminum-free deodorant formulations strengthens the refillable format’s position. Natural formulas require product containers that reflect their clean-ingredient positioning — and reusable metal or glass cases communicate that credibility visually and tactically. According to Dove’s lifecycle analysis, the aluminum-based refillable system cuts primary plastic use by 75% per 12-month cycle — a measurable claim that accelerates retailer and consumer adoption simultaneously.

In July 2025, Wild launched its new refillable roll-on deodorant with plastic-free compostable refills made from Vivomer material — demonstrating that material innovation actively extends the product pipeline for refillable brands. Expansion of eco-friendly personal care brands offering refillable packaging creates competitive pressure on legacy players to respond, pulling conventional deodorant manufacturers toward sustainable format investment.

Restraints

Higher Upfront Cost and Low Refill System Awareness Slow Market Penetration

Refillable deodorant systems require consumers to pay more at the point of first purchase — covering both the durable case and the initial product fill. This price premium creates a hard barrier for price-sensitive shoppers who compare shelf price rather than total cost of ownership. Conventional disposable deodorants win on upfront cost in nearly every retail context.

Limited consumer awareness about refill-based personal care systems compounds the price barrier. Many buyers do not yet understand how refill systems work — how to purchase refills, where to find them, or how frequently to replace them. This knowledge gap raises the perceived effort of switching, reducing conversion rates even among environmentally motivated consumers.

Together, these two restraints create a dual adoption barrier: high entry cost and high perceived complexity. Brands must invest simultaneously in price education and system literacy — a more expensive go-to-market challenge than conventional personal care launches. Until refill availability reaches mass-market scale, these barriers will continue to cap penetration rates among mainstream shoppers.

Growth Factors

Packaging Innovation and Subscription Models Create Durable Revenue Streams for Refillable Brands

Innovation in durable and aesthetic packaging design directly reduces the price-sensitivity barrier in refillable deodorants. When consumers perceive the reusable case as a premium object worth owning long-term, the upfront cost reframes as an investment rather than a premium. According to Morrama’s design case study, the Wild V2 redesign achieved a 17% reduction in material usage while simultaneously improving usability and performance — proving that sustainability and design quality reinforce each other.

Subscription-based refill delivery models improve unit economics for brands by locking in repeat purchase cycles. Rather than relying on consumers to restock independently, subscription models automate refill cadence and reduce churn. This shifts refillable deodorant brands from a single-transaction model toward a recurring-revenue structure — a significant business model advantage over conventional disposable competitors.

In August 2025, French beauty company Hyléance launched a refillable roll-on deodorant in collaboration with 900.care, emphasizing durable low-plastic packaging — signaling that expansion into the premium and luxury personal care segment is active. Eco-conscious consumer groups represent a high-lifetime-value buyer cohort that supports both premium pricing and subscription retention, creating a favorable revenue profile for brands targeting this audience.

Emerging Trends

Circular Logistics and Plastic-Free Refill Systems Redefine the Refillable Deodorant Category

Metal case packaging — particularly aluminum — consolidates its position as the preferred format for refillable deodorant brands. Metal communicates durability, recyclability, and premium quality simultaneously. This triple signal aligns with the purchase logic of eco-motivated buyers and supports brand positioning at higher price tiers, pulling the category away from commodity personal care pricing.

Vegan, cruelty-free, and organic deodorant formulations increasingly pair with refillable delivery formats. This combination creates a powerful value proposition for clean-beauty buyers — the product inside and the container it comes in both meet their values. Cartridge and stick-based refill systems further simplify the repurchase process, lowering the behavioral effort that currently limits repeat purchase rates.

According to The Interline, Again’s CleanCells can sanitise refillable packaging for as little as 12p per unit. This unit economics breakthrough makes reuse cost-competitive with single-use alternatives in circular beauty logistics — which means the operational cost argument against refillable systems weakens significantly. Collaborations between sustainable packaging startups and established cosmetic brands accelerate this shift, bringing industrial-scale cleaning infrastructure into the refillable personal care supply chain.

Regional Analysis

North America Dominates the Refillable Deodorants Market with a Market Share of 46.90%, Valued at USD 105.4 Million

North America holds a 46.90% share of the global refillable deodorants market, valued at USD 105.4 million in 2025. Early retailer adoption and a mature sustainability-positioned consumer goods infrastructure give this region a structural advantage. Strong eco-consumer demand in the US drives refillable deodorant shelf placement in mainstream grocery and drugstore channels, accelerating category volume beyond specialty retail.

Europe Refillable Deodorants Market Trends

Europe represents the second most significant regional market, anchored by the UK where several prominent refillable deodorant brands originated. EU packaging regulations and plastic reduction mandates create regulatory tailwinds that favor refillable formats structurally. Consumer willingness to pay a premium for sustainable personal care products runs higher in Western Europe than in most other regions globally.

Asia Pacific Refillable Deodorants Market Trends

Asia Pacific holds growth potential driven by urbanizing, premium-aspiring consumer segments in China, Japan, South Korea, and India. However, the refillable deodorant concept requires behavior change from a predominantly disposable personal care culture. Market development in this region depends on brand education investment and the expansion of refill infrastructure through modern retail channels.

Middle East and Africa Refillable Deodorants Market Trends

The Middle East and Africa market remains at an early stage for refillable deodorant adoption. Premium consumer segments in GCC countries show receptivity to luxury personal care formats, creating an entry point for high-end refillable deodorant brands. However, limited refill logistics infrastructure and lower consumer awareness keep overall penetration rates below global averages for now.

Latin America Refillable Deodorants Market Trends

Latin America offers a developing opportunity, with Brazil and Mexico representing the most accessible entry markets. Rising middle-class consumer spending in urban centers supports premium personal care adoption. However, price sensitivity across the broader population and limited retail infrastructure for specialty personal care formats constrain near-term refillable deodorant penetration in the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Unilever Plc. repositioned itself at the center of the refillable deodorant category through its April 2025 acquisition of Wild for a reported €275 million. This move gives Unilever ownership of an established refillable brand with proven consumer loyalty rather than building from scratch. The acquisition signals that major FMCG players now treat refillable personal care formats as strategic assets with long-term volume potential.

The Procter & Gamble Company enters the refillable deodorant space through its Dove brand’s stainless-steel refillable system, which uses 54% less plastic per stick. P&G’s strategic advantage lies in its retail distribution infrastructure — it can place refillable formats on mainstream shelves at a scale that independent eco-brands cannot match. This breadth of reach accelerates consumer exposure to refillable formats beyond the eco-committed buyer segment.

by Humankind positions itself as a direct-to-consumer zero-waste personal care brand built around subscription-based refill delivery. Its model captures recurring revenue through automated refill cadence, reducing dependence on retail distribution margins. This subscription architecture creates a fundamentally different unit economics structure compared to legacy personal care players — and a stickier customer relationship over time.

Grove Collaborative, Inc. differentiates through its platform model — offering a curated marketplace of sustainable personal care products including refillable deodorant options. Rather than competing as a single-brand player, Grove aggregates eco-personal care SKUs across multiple brands, giving it breadth across formulations and formats. This multi-brand model insulates Grove from single-product dependency while building platform loyalty among sustainability-focused households.

Key Players

- Unilever Plc.

- The Procter & Gamble Company

- by Humankind

- Grove Collaborative, Inc.

- Noniko

- Asuvi

- The Lekker Company

- Fussy Ltd

- Proverb Skincare

Recent Developments

- December 2024 — Rollr launched as the first experience-led luxury refillable deodorant brand, featuring powder formulas in refillable glass flacons topped with gemstone rollerballs. The brand debuted exclusively at John Bell & Croyden, targeting the premium personal care segment.

- May 2025 — Purefill launched its refillable deodorant system with the Bod Pod Starter Pack, combining a durable reusable case with compostable deodorant pods. This format advances the zero-waste personal care model by eliminating both outer and inner packaging waste at end of use.

- October 2025 — Lifelong launched Deo 2.0, its second-generation infinitely refillable deodorant applicator made from certified ocean-bound recycled plastic, via a Kickstarter campaign. The use of certified ocean-bound material strengthens the brand’s sustainability credentials beyond standard recycled-content claims.

Report Scope

Report Features Description Market Value (2025) USD 225.0 Million Forecast Revenue (2035) USD 417.6 Million CAGR (2026-2035) 6.4% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Refillable Spray Deodorant, Refillable Stick Deodorant), By Packaging (Metal, Glass, Plastic, Paper, Others), By Distribution Channel (Supermarket/Hypermarket, Online, Specialty Store, Drugstores/Pharmacies, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Unilever Plc., The Procter & Gamble Company, by Humankind, Grove Collaborative Inc., Noniko, Asuvi, The Lekker Company, Fussy Ltd, Proverb Skincare Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Refillable Deodorants MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Refillable Deodorants MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Unilever Plc.

- The Procter & Gamble Company

- by Humankind

- Grove Collaborative, Inc.

- Noniko

- Asuvi

- The Lekker Company

- Fussy Ltd

- Proverb Skincare

Our Clients

- 183139

- Mar 2026