Quick Navigation

- Report Overview

- Key Takeaways

- By Form Analysis

- By Product Type Analysis

- By Fat Content Analysis

- By Application Analysis

- By End-Use Analysis

- By Sales Channel Analysis

- Key Market Segments

- Driving factors

- Restraining Factors

- Growth Opportunity

- Challenge

- Emerging Trends

- Business Benefits

- Regional Analysis

- Key Players Analysis

- Recent Development

- Report Scope

Report Overview

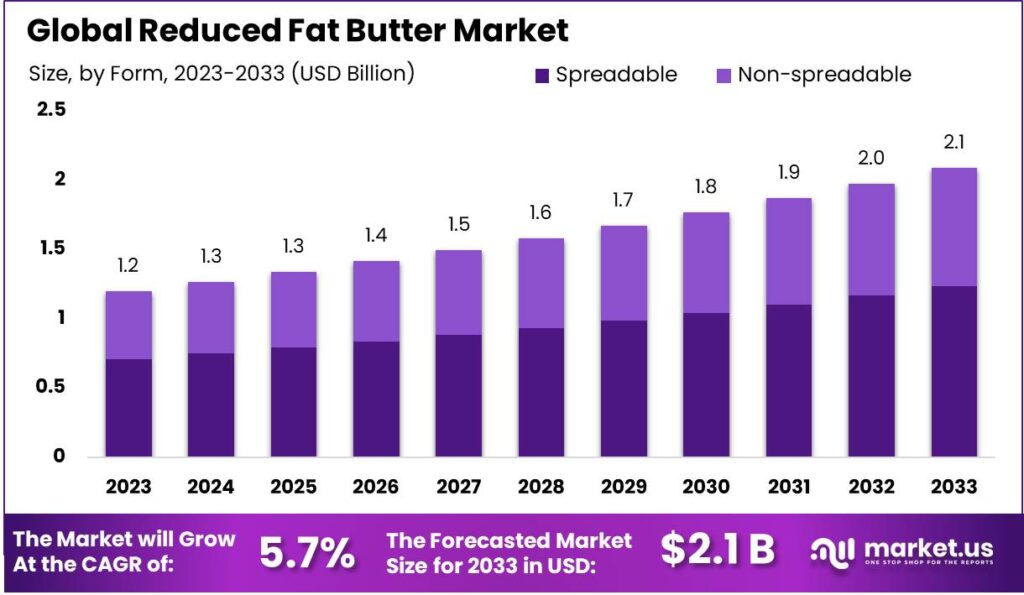

The Global Reduced Fat Butter Market size is expected to be worth around USD 2.1 Billion by 2033, from USD 1.2 Billion in 2023, growing at a CAGR of 5.7% during the forecast period from 2024 to 2033.

The Reduced Fat Butter Market is experiencing significant growth as consumers become more health-conscious and seek alternatives to traditional butter. This shift in consumer behavior is largely driven by a rising awareness of the importance of managing fat intake, particularly about cardiovascular health and weight management.

In recent years, reduced-fat butter has become a popular choice for individuals looking to enjoy the taste and functionality of butter while reducing calorie and fat consumption. This trend is particularly strong among those with dietary restrictions or those striving to maintain a healthier lifestyle.

The demand for reduced-fat butter has surged, with consumers increasingly prioritizing healthier food options. According to market trends, the demand for products that offer both taste and health benefits is expected to continue growing.

The popularity of reduced-fat butter extends beyond health-conscious individuals, as it is now being embraced by families, people on specialized diets, and even those looking to cook healthier meals. Additionally, the availability of reduced-fat butter in various flavors and forms has made it versatile for different culinary applications, further contributing to its widespread appeal.

The market for reduced-fat butter offers several opportunities, particularly in product innovation and catering to specific dietary needs. For example, there is a growing demand for plant-based and dairy-free alternatives, creating potential for brands to target niche segments.

Companies that offer reduced-fat butter with added functional benefits, such as vitamins or probiotics, could expand their consumer base and enhance brand loyalty. Collaboration with other health-focused industries, such as wellness platforms or health-conscious snack brands, also presents a significant growth opportunity.

Market expansion is expected to play a key role in the future growth of the reduced fat butter market. As global awareness of healthy eating rises, new regions such as Asia and Latin America are showing increasing demand for healthier food products.

Additionally, the rise of e-commerce platforms has made reduced-fat butter more accessible to consumers worldwide. The global market for reduced-fat butter is projected to continue growing, driven by both new product innovations and the increasing prioritization of health and wellness in consumer food choices.

The fish peptone market, which is used in various industries, including food production, is also expanding. Regulatory standards for fish peptones are governed by organizations such as the FDA in the U.S. and EFSA in Europe. These standards ensure the safety and traceability of fish-derived products, especially for human consumption. With global fish production increasing by 3.1% annually, the availability of raw materials for fish peptones is on the rise, supporting the growth of the market.

The sector has also seen innovation, with companies like Omega Protein investing over USD 50 million in R&D to improve product quality. Furthermore, significant investments from governments, such as India’s USD 100 million boost to aquaculture, support the expansion of fish peptone production.

Both private and government investments, along with mergers and acquisitions in the industry, indicate strong market consolidation. For example, DSM’s acquisition of Givaudan’s fish protein division for USD 25 million annually reinforces the growing importance of fish-based ingredients. These factors suggest a promising future for both the reduced-fat butter and fish peptone markets.

Key Takeaways

- The Global Reduced Fat Butter Market size is expected to be worth around USD 2.1 Billion by 2033, from USD 1.2 Billion in 2023, growing at a CAGR of 5.7% during the forecast period from 2024 to 2033.

- Spreadable dominated the Reduced Fat Butter market with a 59.1% share by form.

- Salted dominated the Reduced Fat Butter market with a 36.3% share by product type.

- The 40-60% fat content segment dominated the Reduced Fat Butter market with 39.4%.

- Spreading remains the dominant application, driven by its widespread appeal and convenience.

- Households dominated the Reduced Fat Butter market with a 55.7% share.

- Supermarkets/Hypermarkets led the Reduced Fat Butter market with a 44.3% share by Sales Channel.

- APAC dominated the reduced fat butter market with a 37.6% share, USD 0.4 billion.

By Form Analysis

In 2023, Spreadable held a dominant market position in the Reduced Fat Butter market, capturing more than a 59.1% share in the By Form segment. This significant market presence is attributed to the growing consumer preference for convenient, easy-to-spread butter products that combine the health benefits of reduced fat with improved spreadability, making them ideal for daily use. Spreadable reduced-fat butter has gained traction among health-conscious consumers seeking lower-fat alternatives without compromising on texture or taste.

Non-spreadable reduced-fat butter products, while still holding a notable portion of the market, represented a smaller share compared to their spreadable counterparts. These products are typically preferred by consumers who prioritize the traditional butter experience and may use them in cooking or baking applications where spreadability is less of a concern.

However, with the rise of healthier eating trends, non-spreadable reduced-fat butter has seen slower growth in comparison to the more popular spreadable variety. Overall, the Spreadable segment continues to lead the market, driven by demand for convenience, healthier options, and the ability to maintain the richness and texture of traditional butter.

By Product Type Analysis

In 2023, Salted held a dominant market position in the Reduced Fat Butter market, capturing more than a 36.3% share in the By Product Type segment. This strong performance can be attributed to consumer preference for salted butter, which is widely used for enhancing flavor in both cooking and as a spread. Salted reduced-fat butter offers the benefits of lower fat content without compromising on taste, making it a popular choice for consumers who want to maintain the classic buttery flavor while making healthier choices.

The Unsalted variety, while still significant, held a smaller share compared to its salted counterpart. Unsalted reduced-fat butter is favored by consumers who are mindful of their sodium intake or prefer more control over the salt content in their food. It also caters to specific culinary applications where the addition of salt can be managed separately, such as in baking or cooking.

The Spreadable segment, although not directly related to product type but rather to form, also plays a crucial role in the market. Spreadable reduced fat butter combines the benefits of reduced fat with improved spreadability, further boosting its appeal among health-conscious consumers.

By Fat Content Analysis

In 2023, the 40-60% fat content category held a dominant market position in the By Fat Content segment of the Reduced Fat Butter market, capturing more than a 39.4% share. This segment’s growth can be attributed to its balanced approach, offering a moderate reduction in fat while maintaining the rich, creamy texture and flavor that consumers expect from traditional butter. Many health-conscious buyers find the 40-60% range ideal, as it provides a substantial reduction in fat without compromising on the sensory experience.

The 25-40% fat content segment also performed well, appealing to consumers who desire a more significant fat reduction but are still looking for a product that delivers on taste. These butters often cater to those who want healthier options for spreading and cooking, while also benefiting from fewer calories.

The Less than 25% category, though still a part of the market, saw a smaller share due to the trade-off in texture and flavor that some consumers are unwilling to make. While popular among those looking for low-calorie options, these products are often perceived as less indulgent. 60% and above fat content products, while technically reduced fat, typically cater to a niche market. These products have a richer taste but aren’t as commonly preferred due to their higher fat content.

By Application Analysis

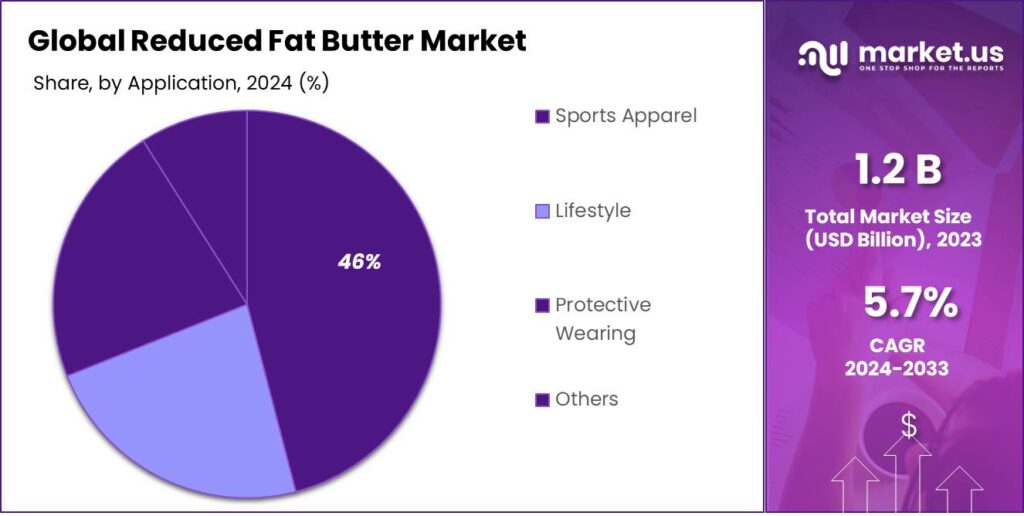

In 2023, Spreading held a dominant market position in the By Application segment of the Reduced Fat Butter market, capturing more than a 45.8% share. This strong performance is largely driven by consumer demand for convenient, healthier alternatives to traditional butter for use in daily spread applications, such as on toast, sandwiches, and crackers.

Spreading reduced fat butter offers the ideal combination of lower fat content without sacrificing the familiar, creamy texture and flavor that consumers expect. This makes it the go-to choice for health-conscious individuals looking to enjoy classic butter spreads in a more nutritious way.

The Baking segment also played a significant role in the market, with reduced-fat butter being used in a variety of baking applications, from cakes to pastries. While the Baking application holds a smaller share than spreading, it remains important for those seeking healthier baking alternatives. However, reduced fat butter for baking can sometimes face limitations in flavor and texture, which may make it less popular compared to full-fat butter for certain recipes.

Cooking applications, which include using reduced-fat butter for sautés and frying, also contributed to market growth, though at a lower rate. Consumers who prefer cooking with reduced-fat products for healthier meal preparation are becoming more aware of these options.

By End-Use Analysis

In 2023, Household held a dominant market position in the By End-Use segment of the Reduced Fat Butter market, capturing more than a 55.7% share. This strong performance is driven by the increasing demand for healthier, lower-fat options in everyday consumer kitchens. Households are the primary consumers of reduced-fat butter, using it for a wide range of applications such as spreading, baking, and cooking.

The shift towards healthier eating habits has led to a growing preference for reduced-fat products, making household consumption the largest contributor to market growth. The convenience, affordability, and availability of reduced-fat butter in retail outlets have further solidified its popularity among home users.

The food service segment, while smaller, also plays a key role in the market, particularly in restaurants, hotels, and catering services. These establishments increasingly use reduced-fat butter to meet consumer demand for healthier menu options. However, food service applications often face challenges related to maintaining flavor and texture, which can sometimes limit the adoption of reduced fat butter compared to traditional full-fat butter.

The Food Industry segment, which includes use in packaged foods, sauces, and ready meals, represents another important market. Reduced-fat butter is often incorporated into processed foods to cater to the growing demand for healthier, low-fat products.

By Sales Channel Analysis

In 2023, Supermarkets/Hypermarkets held a dominant market position in the By Sales Channel segment of the Reduced Fat Butter market, capturing more than a 44.3% share. This large market share is attributed to the convenience, wide selection, and competitive pricing offered by these large retail outlets.

Supermarkets and hypermarkets serve as primary shopping destinations for consumers looking to purchase reduced-fat butter due to their easy accessibility and the ability to compare multiple brands and products in one location. The prominence of these retailers in both urban and rural areas ensures that reduced-fat butter reaches a broad consumer base.

Departmental Stores also play a significant role in the market, holding a smaller but notable share. These stores often target middle-to-high-income consumers and focus on premium or niche products, which include various reduced-fat butter options. While not as dominant as supermarkets, departmental stores cater to a specific demographic seeking convenience and quality.

The Convenience Store segment, while representing a smaller share, serves a vital role in quick, on-the-go purchases. These stores typically offer smaller packaging of reduced-fat butter, ideal for consumers needing quick replenishment.

The Online Sales Channel has seen steady growth, driven by the increasing trend of e-commerce and home delivery services. Consumers are becoming more comfortable purchasing grocery items online, including reduced-fat butter, for convenience and to have a range of options available.

Key Market Segments

By Form

- Spreadable

- Non-spreadable

By Product Type

- Unsalted

- Salted

- Spreadable

- Others

By Fat Content

- Less than 25%

- 25-40%

- 40-60%

- 60% and above

By Application

- Spreading

- Baking

- Cooking

- Others

By End-Use

- Household

- Foodservice

- Food Industry

- Others

By Sales Channel

- Supermarkets/Hypermarkets

- Departmental Stores

- Convenience Store

- Online Sales Channel

- Others

Driving factors

Rising Demand for Nutritional Supplements

One of the key drivers for the growth of the fish peptones market is the increasing demand for nutritional supplements. Fish peptones are rich in amino acids, peptides, and essential nutrients that are beneficial for human health, particularly in promoting immune system function, improving skin health, and supporting muscle recovery.

As consumers become more health-conscious and seek natural sources of protein, fish-derived ingredients, including fish peptones, are gaining popularity in the nutraceutical sector. This trend is amplified by the rise in lifestyle-related diseases, such as obesity, diabetes, and cardiovascular issues, which encourage individuals to incorporate healthier, more natural supplements into their diets.

Fish peptones offer a sustainable, high-quality protein alternative, making them an attractive ingredient in dietary supplements. As a result, the increasing awareness about the importance of nutrition and natural supplements, along with the shift toward clean-label products, is expected to drive the demand for fish peptones in the coming years.

Restraining Factors

Limited Availability of Raw Materials

A significant restraint for the fish peptones market is the limited availability of raw materials, particularly fish. While fish peptones are derived from fish protein hydrolysates, the overfishing of marine species and environmental regulations around fishing are making it more difficult to obtain a consistent, high-quality supply of fish.

Sustainability concerns have led to a growing emphasis on responsible fishing practices, but these regulations often result in supply chain disruptions and fluctuations in raw material prices. Furthermore, the fish species used for producing fish peptones, such as cod, herring, and sardines, are vulnerable to depletion, leading to concerns over long-term supply stability.

For manufacturers, this can create challenges in ensuring the continuous availability of fish peptones for production, ultimately affecting pricing and the overall growth potential of the market. As a result, companies in the fish peptones industry may face difficulties in scaling up production or meeting the increasing demand for these ingredients, particularly if raw material availability becomes more restricted.

Growth Opportunity

Expansion in Animal Feed Industry

The growing interest in the use of fish peptones in the animal feed industry presents a significant opportunity for market growth. Fish peptones are highly digestible and nutritious, making them an ideal ingredient for enhancing the nutritional value of animal feed, particularly for aquaculture and livestock farming. As the global demand for animal protein increases, there is a corresponding need for high-quality feed ingredients to improve animal health and productivity.

Fish peptones contain essential nutrients that promote the growth of animals, improve their immunity, and enhance overall feed conversion rates. In particular, the aquaculture industry stands to benefit from the inclusion of fish peptones in feed formulations, as they can help improve fish growth rates, skin quality, and resistance to diseases.

As sustainable farming practices become more important, fish peptones offer an eco-friendly alternative to synthetic additives and low-quality protein sources. With aquaculture and livestock farming sectors increasingly adopting sustainable and high-performance feed ingredients, the demand for fish peptones in the animal feed industry is expected to expand in the coming years, creating a valuable growth opportunity for manufacturers.

Challenge

Consumer Perception and Acceptance

One of the primary challenges facing the fish peptones market is consumer perception and acceptance. Despite their nutritional benefits, fish-derived ingredients can sometimes be met with skepticism due to concerns over taste, odor, and potential allergens. Many consumers are wary of products containing fish, particularly those who avoid seafood for dietary or ethical reasons.

Additionally, there is a stigma around animal-based ingredients, especially among plant-based or vegan consumers. As the trend toward plant-based diets continues to grow, manufacturers of fish peptones may struggle to convince certain market segments of the benefits and safety of incorporating fish-derived ingredients into their products. This challenge is compounded by the need for transparent labeling and clear communication about sourcing and sustainability practices.

Educating consumers about the advantages of fish peptones, such as their high bioavailability and digestibility, will be crucial to overcoming these perceptions. Companies in the market will need to invest in consumer awareness campaigns, as well as explore alternatives or hybrid formulations, to broaden the appeal of fish peptones to a wider, more diverse consumer base.

Emerging Trends

Fish peptones, derived from by-products, are used in biotechnology, pharmaceuticals, and sustainable aquaculture.

Fish peptones, derived from fish processing by-products such as fish scales, bones, and skin, have emerged as a significant ingredient in various industries due to their unique nutritional profile and bioactive properties. In recent years, these peptones have gained attention primarily in the fields of biotechnology, pharmaceuticals, and agriculture.

As consumers become more conscious about sustainability and resource utilization, fish-derived ingredients, including peptones, are being explored for their ability to reduce waste and provide a cost-effective, high-quality alternative to traditional peptones from other animal or plant sources.

One of the key emerging trends is the application of fish peptones in the production of growth media for culturing microorganisms, which is essential for biopharmaceutical production. These peptones provide essential amino acids, vitamins, and trace elements that promote the growth and yield of cells in culture. Fish peptones are also being studied for their potential role in enhancing the efficacy of vaccines and therapeutics, thanks to their ability to stimulate immune responses.

Another trend is the use of fish peptones in aquaculture, where they are incorporated into feed formulations to promote the health and growth of farmed fish. As fish farming grows worldwide, there is an increasing demand for alternative feed ingredients that are both sustainable and beneficial for aquatic animals. Fish peptones are a promising solution, as they support digestion and improve the overall health of the fish, leading to better production outcomes.

Business Benefits

Fish peptones offer cost-effective, sustainable solutions in the biotechnology, pharmaceuticals, and aquaculture industries.

Fish peptones offer several key business benefits across multiple sectors, especially in industries related to biotechnology, aquaculture, and pharmaceuticals. The growing interest in sustainable practices, coupled with the increasing demand for high-quality, natural ingredients, has made fish peptones a valuable resource for companies looking to innovate and reduce their environmental footprint.

For businesses in biotechnology and pharmaceuticals, fish peptones offer a cost-effective, high-quality alternative to traditional animal or plant-derived peptones used in cell culture and microbial fermentation. They help improve the yield and growth of microbial cultures, which is crucial for producing biopharmaceuticals, vaccines, and other therapeutic products.

In the aquaculture industry, incorporating fish peptones into fish feed has shown promising results in improving fish health, growth rates, and overall feed conversion efficiency. For companies in aquaculture, the adoption of fish peptones can lead to increased production yields and lower mortality rates among farmed fish, which directly impacts profitability. Moreover, as consumers continue to demand sustainably produced seafood, companies that embrace fish-based ingredients for their feeds can capitalize on this trend, appealing to eco-conscious markets.

Additionally, the eco-friendly nature of fish peptones is a significant selling point. By utilizing fish by-products that would otherwise be discarded, businesses can contribute to the circular economy while meeting consumer demand for sustainable products. This not only improves the company’s environmental credentials but also creates new revenue streams from waste materials.

Regional Analysis

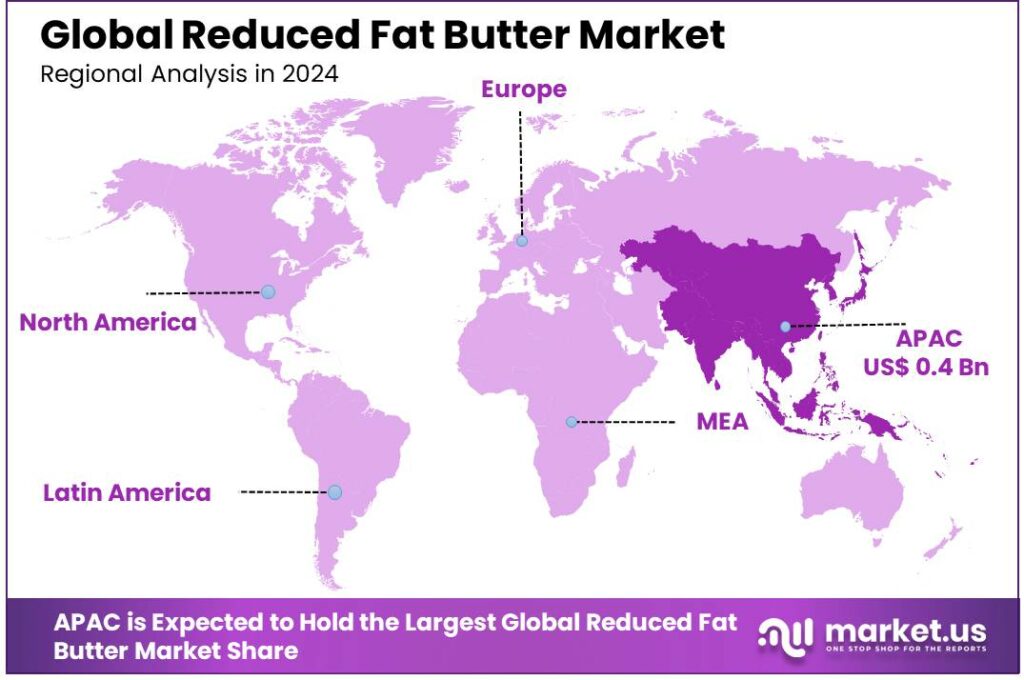

Asia-Pacific dominated the reduced fat butter market with a 37.6% share, USD 0.4 billion.

In 2023, Asia-Pacific held a dominant market position in the reduced fat butter market, capturing more than 37.6% of the global market share, which translates to a revenue of approximately USD 0.4 billion. This leadership can be attributed to several key factors driving growth in the region.

First, the increasing demand for healthier alternatives to traditional butter, especially among health-conscious consumers in countries like China, India, and Japan, has spurred the adoption of reduced-fat butter. Rising concerns over obesity, heart disease, and cholesterol levels are prompting a shift toward lower-fat dairy options, making reduced-fat butter a favorable choice.

Additionally, the growing population in APAC, coupled with rising disposable incomes, is fueling the demand for processed food products, including dairy items. As more consumers have the purchasing power to opt for premium and health-oriented food products, the market for reduced-fat butter continues to expand. Furthermore, APAC’s large food processing industry, which frequently uses butter as an ingredient, is increasingly incorporating reduced fat variants to meet consumer preferences and health trends.

Moreover, APAC’s shift toward modern retail formats, such as supermarkets and hypermarkets, has enhanced the accessibility of reduced-fat butter products. The region’s robust distribution networks and the rapid expansion of international food brands have also played a significant role in driving market penetration. These factors combined position APAC as the leading region in the reduced fat butter market, with growth expected to continue in the coming years.

Key Regions and Countries

North America

- The US

- Canada

- Rest of North America

Europe

- Germany

- France

- The UK

- Spain

- Netherlands

- Russia

- Italy

- Rest of Europe

Asia-Pacific

- China

- Japan

- Singapore

- Thailand

- South Korea

- Vietnam

- India

- New Zealand

- Rest of Asia Pacific

Latin America

- Mexico

- Brazil

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of the Middle East & Africa

Key Players Analysis

In 2024, the global reduced fat butter market will be influenced significantly by key players such as Arla Foods, Danone, Kerry Group, and Lactalis. These companies stand out due to their strategic initiatives, comprehensive product ranges, and deep market penetration, driving innovation and consumer acceptance in this sector.

Arla Foods has been a frontrunner in sustainability and product innovation, catering to the growing consumer demand for healthier dairy alternatives. With its global footprint, Arla has effectively leveraged its brand reputation to promote reduced-fat butter products that promise both quality and taste. Their commitment to environmentally friendly practices and transparent supply chains continues to resonate well with eco-conscious consumers, enhancing their market position.

Danone, known for its focus on health-oriented products, capitalizes on its strong R&D capabilities to meet diverse consumer needs. Danone’s reduced-fat butter products are often enriched with additional nutrients, appealing to health-conscious consumers looking for multifunctional dairy products. Their marketing strategies, which emphasize wellness and nutritional benefits, have effectively positioned them as a top choice for health-aware shoppers.

Kerry Group excels in the integration of innovative flavors and textures, setting them apart in the reduced fat butter market. Their ability to adapt quickly to changing consumer preferences and the latest culinary trends has helped them maintain a competitive edge. Kerry’s expertise in taste and nutrition technologies also allows them to offer superior products that meet both the taste and health criteria demanded by today’s consumers.

Lactalis has leveraged its extensive distribution network to ensure the widespread availability of its reduced-fat butter products. Their strategic focus on both domestic and international markets has facilitated strong growth, particularly in emerging markets where demand for healthier dairy products is rapidly expanding. Lactalis’s commitment to quality and continuous improvement in product offerings reinforces its market leadership in the reduced fat butter segment.

Market Key Players

- Agral S.A.

- Amul

- Arla Foods

- Aurivo Co-operative Society Ltd.

- Britannia

- Dairy Crest

- Danone

- Finlandia Cheese, Inc

- Fonterra

- FrieslandCampina

- GCMMF

- Haldiram Snacks and Foods

- ITC

- Kerry Group

- Kerrygold USA

- Lactalis

- Lam Soon Group

- Land O’Lakes, Inc

- Mother Dairy

- Nestlé

- Ornua Co-operative Limited

- Palsgaard

- Raisio Group plc

- Rockview Farms

- Saputo Dairy Australia Pty Ltd

- Saputo Inc.

- SAVENCIA SA

- Unilever

Recent Development

- In July 2024, Kerry Group announced a major investment in a new production facility in Ireland, dedicated to the manufacturing of reduced-fat butter and other health-oriented dairy products. The company is investing EUR 35 million to expand production capacity by 20%, with an expected increase in revenue from its reduced-fat butter portfolio of approximately EUR 60 million by the end of 2025. The new facility will enable Kerry to meet the growing demand for healthier, functional dairy products in Europe and North America.

- In June 2024, Nestlé North America expanded its range of reduced-fat butter under its leading brand, Land O’Lakes. The company reported a 12% increase in sales of their reduced-fat butter products in Q2 2024, amounting to USD 75 million in additional revenue. The expansion includes distribution in over 5,000 stores across the U.S. and Canada, focusing on healthier choices as consumer preference shifts towards lower-fat dairy options.

- In March 2024, Arla Foods introduced a new range of reduced-fat butter across Europe, specifically targeting health-conscious consumers. The new product line, which contains 40% less fat than traditional butter, was launched in response to rising consumer demand for healthier dairy alternatives. This launch is expected to generate an additional revenue of EUR 50 million for Arla Foods in the next two years, as the company aims to expand its market share in the health-focused segment.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | USD 1.2 Billion |

| Forecast Revenue (2033) | USD 2.1 Billion |

| CAGR (2024-2032) | 5.7% |

| Base Year for Estimation | 2023 |

| Historic Period | 2016-2023 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Form (Spreadable, Non-spreadable), By Product Type (Unsalted, Salted, Spreadable, Others), By Fat Content (Less than 25%, 25-40%, 40-60%, 60% and above), By Application (Spreading, Baking, Cooking, Others), By End-Use (Household, Foodservice, Food Industry, Others), By Sales Channel (Supermarkets/Hypermarkets, Departmental Stores, Convenience Store, Online Sales Channel, Others) |

| Regional Analysis | North America – The US, Canada, Rest of North America, Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe, Asia-Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Asia Pacific, Latin America – Brazil, Mexico, Rest of Latin America, Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of Middle East & Africa |

| Competitive Landscape | Agral S.A., Amul, Arla Foods, Aurivo Co-operative Society Ltd., Britannia, Dairy Crest, Danone, Finlandia Cheese, Inc, Fonterra, FrieslandCampina, GCMMF, Haldiram Snacks and Foods, ITC, Kerry Group, Kerrygold USA, Lactalis, Lam Soon Group, Land O’Lakes, Inc, Mother Dairy, Nestlé, Ornua Co-operative Limited, Palsgaard, Raisio Group plc, Rockview Farms, Saputo Dairy Australia Pty Ltd, Saputo Inc., SAVENCIA SA, Unilever |

| Customization Scope | We will provide customization for segments and at the region/country level. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |