Red Team-as-a-Service Market By Component (Solutions, Services), By Deployment Mode (On-Premises, Cloud), By Organization Size (Small and Medium Enterprises, Large Enterprises), By Application (Network Security, Application Security, Cloud Security, Endpoint Security, Others), By End-User (BFSI, Healthcare, Government and Defense, IT and Telecom, Retail, Energy and Utilities, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

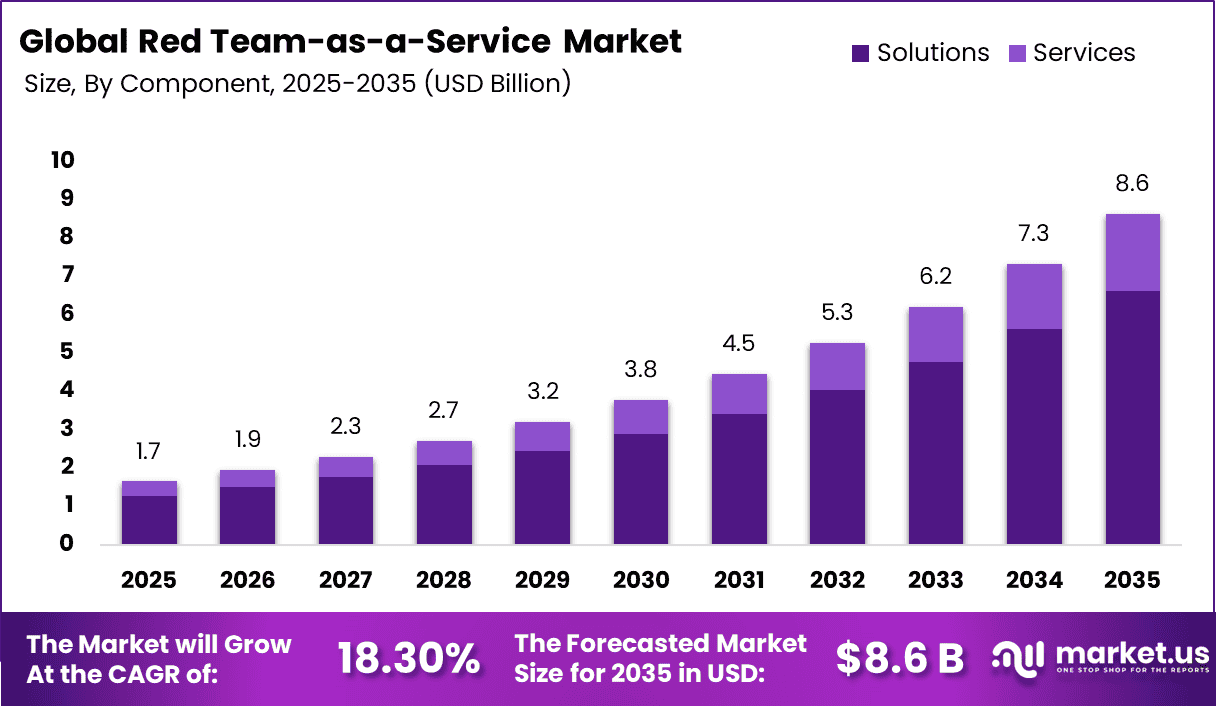

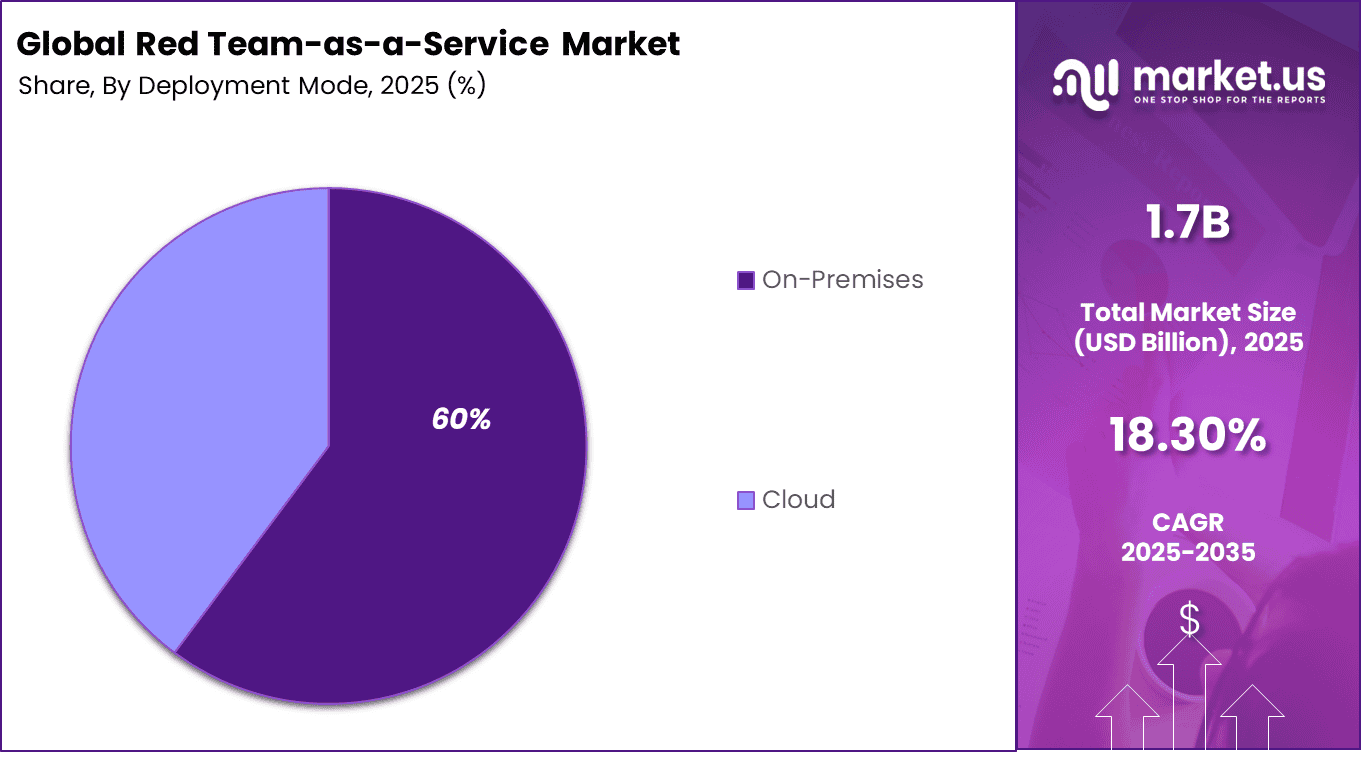

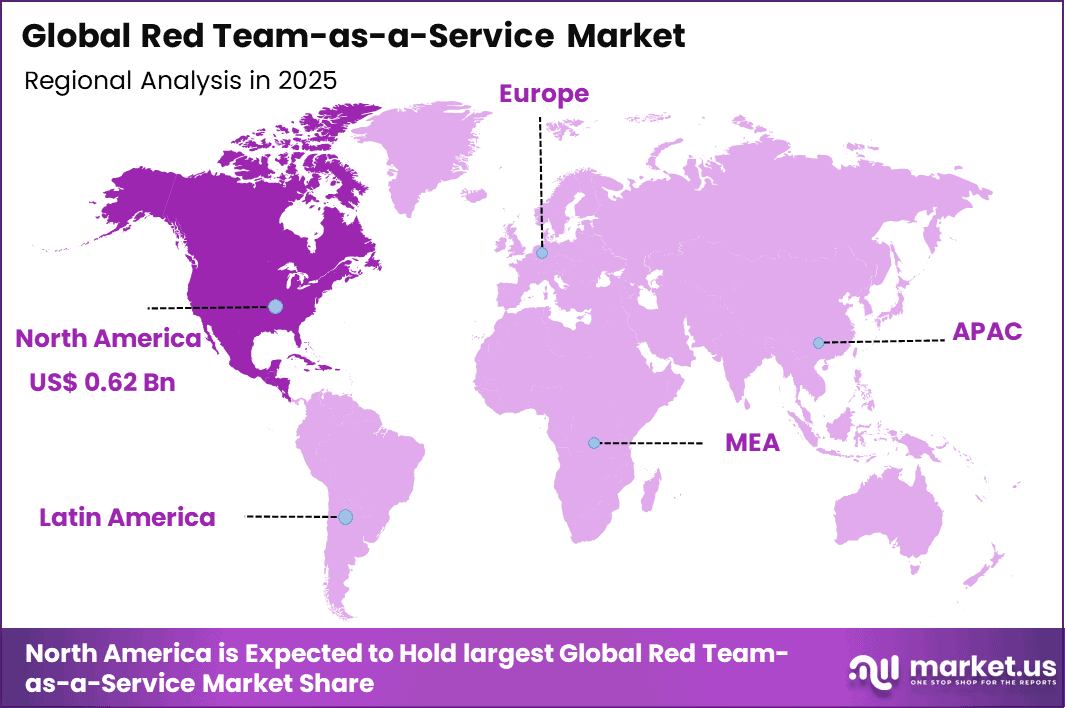

The Global Red Team-as-a-Service Market generated USD 1.7 billion in 2025 and is predicted to register growth from USD 1.9 billion in 2026 to about USD 8.6 billion by 2035, recording a CAGR of 18.30% throughout the forecast span. In 2025, North America held a dominan market position, capturing more than a 37.6% share, holding USD 0.62 Billion revenue.

The Red Team-as-a-Service market focuses on outsourced cybersecurity services that simulate real world cyber attacks to test an organization’s defenses. These services replicate attacker behavior across systems, networks, people, and processes to identify hidden vulnerabilities. Unlike periodic testing, the service model enables continuous and scalable security validation. This approach has gained importance as cyber threats become more advanced and unpredictable.

Market demand has increased due to the limitations of traditional security testing methods. Conventional assessments provide only a snapshot of security posture, while modern threats evolve continuously. Red Team-as-a-Service delivers ongoing testing that reflects real attack scenarios. This helps organizations identify weaknesses before they are exploited.

The growing complexity of digital infrastructure has further accelerated adoption. Enterprises operate across cloud, hybrid, and remote environments, increasing the attack surface. Red team simulations provide a comprehensive view of how defenses perform under realistic conditions. This has positioned the service as a critical component of proactive cybersecurity strategies.

One of the main factors driving this market is the growing need for realistic security validation as cyber risks become more complex. Organizations are no longer satisfied with one time testing and increasingly prefer ongoing assessments that reflect actual attacker behavior. Another important factor is the shortage of highly skilled offensive security professionals, which makes external red team services a practical choice for many businesses.

Demand for Red Team-as-a-Service is increasing among large enterprises, regulated industries, and digital first organizations that need stronger visibility into their security readiness. These buyers want flexible services that can identify hidden gaps in detection, response, privilege controls, and internal coordination. Demand is also rising because many companies now prefer security testing models that are easier to scale and align with regular risk management efforts.

Top Market Takeaways

By Component, hardware dominates with 56.9% share, delivering dedicated analytics appliances for real-time policy simulation, traffic pattern baselining, and convergence optimization across SD-WAN/ZTNA fabrics.

By Deployment Mode, on-premises captures 72.6%, ensuring sovereign visibility, air-gapped compliance reporting, and integration with legacy firewall rulebases during SASE migration.

By Organization Size, large enterprises hold 68.4%, orchestrating multi-cloud policy fabrics with automated drift detection and risk-prioritized remediation recommendations.

By Application, network security leads at 39.2%, powering CASB discovery, SWG optimization, and FWaaS rule rationalization through behavioral traffic analytics.

By End-User, BFSI commands 37.4%, addressing PCI-DSS convergence, regulatory audit trails, and zero-trust policy enforcement across global branch networks.

Regionally, North America accounts for 35.2% global share, with the U.S. market valued at USD 0.63 billion and a CAGR of 19.6%, driven by federal CISA directives and financial sector SASE adoption mandates.

Drivers Impact Analysis

Key Driver

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Strategic Effect

Rising frequency of advanced cyberattacks and breaches

+3.4%

North America, Europe, Asia Pacific

Short to Mid Term (2025–2031)

Increases demand for proactive security testing

Growing adoption of offensive security and penetration testing services

+3.1%

US, Europe

Mid Term (2026–2032)

Expands use of simulated attack scenarios

Regulatory pressure for cybersecurity resilience and compliance

+2.8%

North America, Europe

Mid to Long Term (2026–2035)

Drives enterprise investment in security validation

Increasing digital transformation and cloud adoption

+2.6%

Global

Mid Term (2026–2032)

Expands attack surface requiring testing

Demand for continuous security assessment and threat simulation

+2.4%

Global

Mid to Long Term (2026–2035)

Supports ongoing red team engagement

Restraints Impact Analysis

Key Restraint

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Strategic Effect

High cost of specialized red team services

-2.2%

Global

Mid Term (2026–2032)

Limits adoption among SMEs

Shortage of skilled cybersecurity professionals

-2.0%

Global

Mid Term (2026–2032)

Delays service delivery

Potential operational disruption during testing

-1.8%

North America, Europe

Short to Mid Term (2025–2031)

Creates hesitation among enterprises

Data privacy and compliance concerns

-1.7%

Europe, North America

Mid to Long Term (2026–2035)

Restricts testing scope

Limited awareness in emerging markets

-1.5%

Asia Pacific, Latin America

Short to Mid Term (2025–2030)

Slows adoption outside developed regions

By Component Analysis

Solutions account for 76.8% of the market, reflecting the growing reliance on structured platforms that deliver automated and continuous red team simulations. These solutions enable organizations to test network defenses, identify vulnerabilities, and assess incident response capabilities. By simulating real world attack scenarios, organizations can evaluate the effectiveness of their cybersecurity controls.

The dominance of solution platforms is also supported by their ability to integrate with existing security infrastructure such as threat detection systems and vulnerability management tools. Automated reporting and analytics provide actionable insights that help organizations strengthen their defenses. As cyber threats become more advanced, red team solutions continue to play a central role in cybersecurity strategies.

By Deployment Mode Analysis

On premises deployment represents 60.2% of the market, indicating a strong preference for maintaining testing environments within internal infrastructure. Organizations conducting red team exercises often handle sensitive data and security configurations that require strict control. Internal deployment allows enterprises to customize testing scenarios and maintain confidentiality.

Industries with strict regulatory requirements prefer on premises deployment to ensure compliance with data protection standards. This approach also supports integration with internal security systems and legacy infrastructure. As cybersecurity risks increase, on premises deployment remains widely adopted for red team operations.

By Organization Size Analysis

Large enterprises account for 70.2% of market adoption due to the complexity and scale of their IT and security environments. These organizations manage extensive networks, applications, and data systems that require continuous security testing. Red team platforms help identify vulnerabilities across multiple layers of enterprise infrastructure.

Large organizations also maintain dedicated cybersecurity teams responsible for monitoring threats and conducting security assessments. Automated red team tools enable these teams to perform continuous testing and improve security readiness. As enterprise digital ecosystems expand, large companies remain the primary adopters of red team as a service solutions.

By Application Analysis

Network security represents 42.4% of the market application segment due to the critical need to protect enterprise networks from cyber threats. Red team simulations are widely used to test network defenses, identify weaknesses, and evaluate response mechanisms. These exercises help organizations strengthen their network security frameworks.

Advanced testing scenarios simulate real attack techniques targeting network infrastructure, allowing organizations to identify vulnerabilities before they are exploited. Continuous testing improves the overall resilience of enterprise networks. As cyber threats targeting networks increase, network security remains a key focus area.

By End User Analysis

The BFSI sector accounts for 38.5% of market adoption due to strict regulatory requirements and the need to protect sensitive financial data. Financial institutions rely on red team exercises to evaluate the effectiveness of their cybersecurity defenses. Simulated attacks help identify vulnerabilities in banking systems, transaction platforms, and digital services.

Financial organizations also require continuous security testing to maintain compliance with regulatory standards and risk management frameworks. Red team platforms provide detailed insights that support proactive security improvements. As digital financial services expand, the BFSI sector continues to invest in advanced cybersecurity testing solutions.

Investor Type Impact Analysis

Investor Type

Growth Sensitivity

Risk Exposure

Geographic Focus

Investment Outlook

Venture Capital Firms

Very High

High

US, Europe, Israel

Strong offensive security opportunity

Private Equity Firms

High

Medium

North America, Europe

Expansion in cybersecurity services

Strategic Technology Investors

Very High

Medium

US, Japan, South Korea

Strengthens security ecosystem

Corporate Venture Arms

High

Medium

Global

Partnerships with security providers

Government and Cybersecurity Funds

Medium

Low to Medium

North America, Europe, Asia Pacific

Supports national cyber defense

Technology Enablement Analysis

Technology Enabler

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Implementation Significance

AI driven attack simulation and threat modeling

+3.5%

Global

Mid Term (2026–2032)

Improves testing efficiency

Cloud based red teaming platforms

+3.2%

Global

Short to Mid Term (2025–2031)

Enables scalable testing

Automated penetration testing tools

+2.9%

North America, Europe

Mid Term (2026–2032)

Reduces manual effort

Integration with SIEM and security platforms

+2.6%

Global

Mid to Long Term (2026–2035)

Enhances threat detection

Continuous security validation frameworks

+2.4%

Global

Mid to Long Term (2026–2035)

Supports ongoing risk assessment

Key Challenges

Service quality can vary because red team providers use different testing methods, skill levels, and reporting standards, which makes results difficult to compare.

Many organizations struggle with cost because red team as a service requires skilled experts, realistic attack simulation, and repeated testing over time.

Scope control is a major challenge because companies must clearly define which systems, users, and locations can be tested without disrupting business operations.

Internal coordination can be difficult because security teams, IT teams, and management must align before, during, and after the engagement.

Turning findings into action remains a challenge because many organizations identify security gaps during testing but take time to fix them due to limited staff, budget, or technical complexity.

Growth Factors

One of the primary growth factors driving the Red Team-as-a-Service market is the increasing sophistication of cyber threats. Attackers use advanced techniques such as multi-stage exploits, social engineering, and lateral movement to compromise systems. Organizations require realistic testing environments that replicate these tactics to evaluate their defenses effectively.

Another growth factor is the growing adoption of continuous security testing models. Traditional periodic assessments are no longer sufficient to address rapidly changing threat landscapes. Red Team-as-a-Service provides continuous testing and monitoring, allowing organizations to identify vulnerabilities and improve their security posture on an ongoing basis.

Emerging Trends

One emerging trend in the Red Team-as-a-Service market is the integration of automated attack simulation platforms. These platforms use predefined attack scenarios and AI-driven techniques to continuously test security systems without requiring constant manual intervention. Automation increases testing frequency and helps organizations identify vulnerabilities more quickly.

Another trend is the expansion of red teaming into cloud and hybrid environments. As organizations migrate to cloud infrastructure, red team services are evolving to simulate attacks across distributed systems, including cloud applications, APIs, and remote access environments.

Key Market Segments

By Component

Solutions

Services

By Deployment Mode

On-Premises

Cloud

By Organization Size

Small and Medium Enterprises

Large Enterprises

By Application

Network Security

Application Security

Cloud Security

Endpoint Security

Others

By End-User

BFSI

Healthcare

Government and Defense

IT and Telecom

Retail

Energy and Utilities

Others

Regional Analysis

North America accounted for 37.6% of the Red Team as a Service Market, reflecting strong adoption of advanced cybersecurity testing practices across enterprises. Organizations across sectors such as finance, healthcare, and technology increasingly rely on simulated attack services to identify vulnerabilities in their systems.

Red team services help businesses test real world threat scenarios, improve incident response readiness, and strengthen overall security posture. As cyber threats become more sophisticated, demand for continuous and realistic security testing continues to grow across the region.

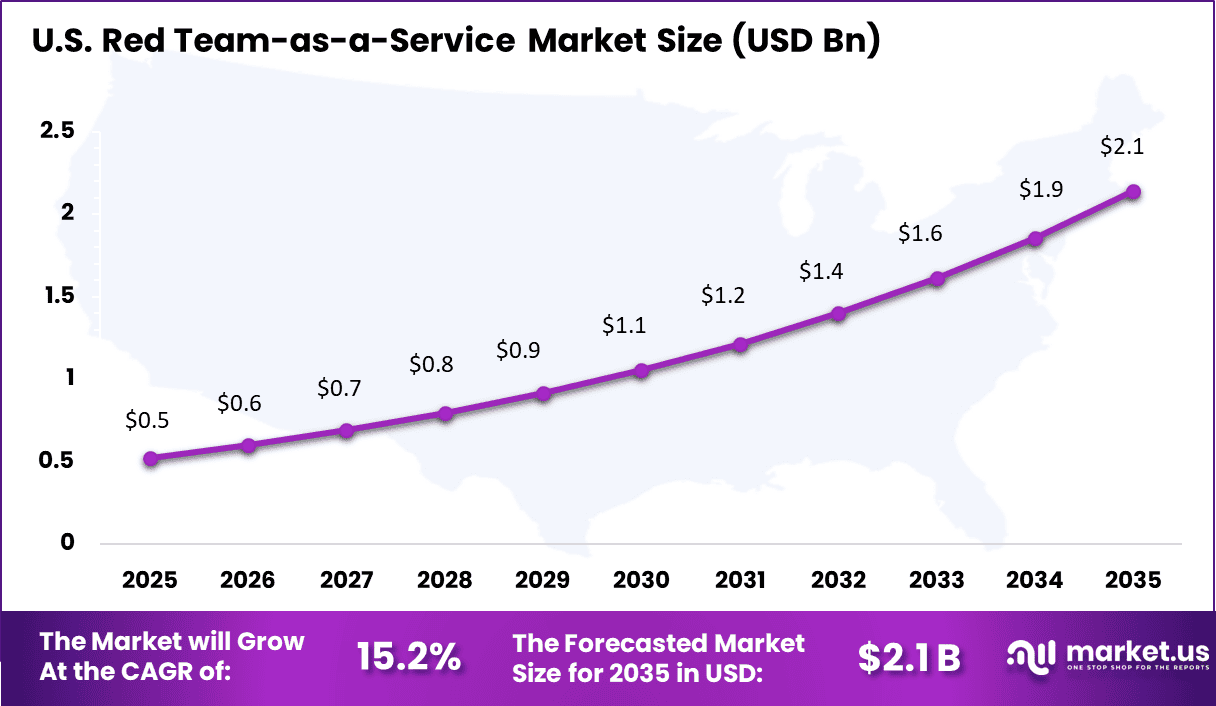

The U.S. generated about USD 0.52 Bn within the regional market and is projected to expand at a CAGR of 15.2%. Enterprises across the country continue to invest in proactive security strategies that go beyond traditional testing methods.

Red team as a service offerings allow organizations to conduct regular and scalable security assessments without maintaining in house expertise. As companies face rising risks from targeted cyber attacks and regulatory pressure to improve security standards, adoption of red team services continues to expand steadily across the US market.

Key Regions and Countries

North America

US

Canada

Europe

Germany

France

The UK

Spain

Italy

Russia

Netherlands

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Singapore

Thailand

Vietnam

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Competitive Analysis

The Red Team as a Service Market is driven by global cybersecurity providers that deliver advanced threat simulation and penetration testing services. IBM Corporation, CrowdStrike, Rapid7, and Trellix offer continuous security testing platforms that simulate real world cyber attacks. These services help organizations identify vulnerabilities and improve incident response readiness. Increasing cyber threats and regulatory requirements have accelerated adoption across enterprises.

Managed security and consulting firms also play a significant role in delivering red team services. KPMG, EY, PwC, and Kroll provide structured cybersecurity assessments combined with risk management and compliance consulting. Their services are widely used by financial institutions, government agencies, and large enterprises. These firms leverage global expertise and industry frameworks to deliver comprehensive security evaluations.

Specialized offensive security vendors further expand the competitive landscape. Mandiant, NCC Group, Cobalt.io, Bishop Fox, NetSPI, and Secureworks focus on continuous penetration testing, vulnerability assessments, and adversary simulation platforms. Additional providers such as Trustwave, Coalfire, Cynet, F Secure, Optiv Security, and Simeio Solutions offer tailored security testing and identity management services.

The future outlook for the Red Team-as-a-Service Market looks strong as organizations move beyond basic security checks and seek more realistic attack simulations that test people, processes, and technology together.

IBM describes red teaming as a simulated, nondestructive cyberattack used to identify weaknesses and improve security operations, and it also notes that continuous automated approaches can make this kind of testing more accessible. With AI creating new security concerns and the global cyber skills gap remaining wide, demand is expected to grow for service-based red team offerings that help businesses find gaps earlier and improve response readiness.

Recent Developments

December, 2025 – CrowdStrike Falcon Adversary launched continuous RTaaS with AI-driven attack paths. Teams simulate nation-state tactics across cloud and endpoints. Breaches dropped 65% post-engagement. Real-time Falcon Fusion correlates red team actions with detections. Pricing starts at $25K quarterly. CrowdStrike serves 29,000+ customers.

January, 2026 – Mandiant Red Team Advantage added breach-and-simulate for ransomware vectors. Financial firms test EDR gaps quarterly. Remediation velocity improved 50%. Google integration pulls live threat intel. Engagements scale from $40K single-ops to $150K annual retainers. Mandiant handles 2,000+ simulations yearly.

Report Scope

Report Features

Description

Market Value (2025)

USD 1.7 Billion

Forecast Revenue (2035)

USD 8.6 Billion

CAGR(2025-2035)

18.30%

Base Year for Estimation

2024

Historic Period

2020-2024

Forecast Period

2025-2035

Report Coverage

Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends

Segments Covered

By Component (Solutions, Services), By Deployment Mode (On-Premises, Cloud), By Organization Size (Small and Medium Enterprises, Large Enterprises), By Application (Network Security, Application Security, Cloud Security, Endpoint Security, Others), By End-User (BFSI, Healthcare, Government and Defense, IT and Telecom, Retail, Energy and Utilities, Others)

Regional Analysis

North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA