Quick Navigation

Report Overview

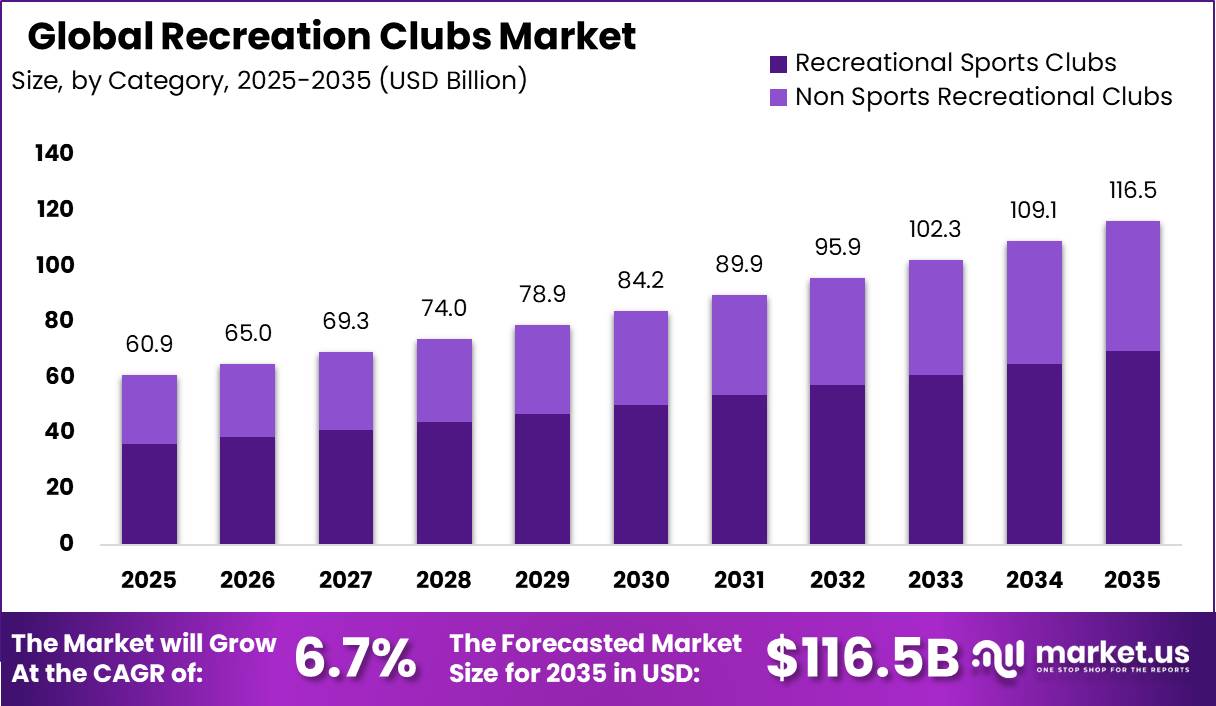

Global Recreation Clubs Market size is expected to be worth around USD 116.5 Billion by 2035 from USD 60.9 Billion in 2025, growing at a CAGR of 6.7% during the forecast period 2026 to 2035. This expansion reflects strong member demand for structured social, fitness, and lifestyle experiences across global markets.

This reflects how recreation clubs combine sports facilities, social spaces, and wellness programs under single membership models. The market spans private members clubs, sports academies, and lifestyle communities serving distinct age and income groups. Operators structure offerings around category type, age demographic, and travel behavior to match diverse member needs.

Key Takeaways

- The Recreation Clubs Market is valued at USD 60.9 Billion in 2025 and is projected to reach USD 116.5 Billion by 2035, registering a CAGR of 6.7%.

- Recreational Sports Clubs lead the By Category segment with a 59.7% share.

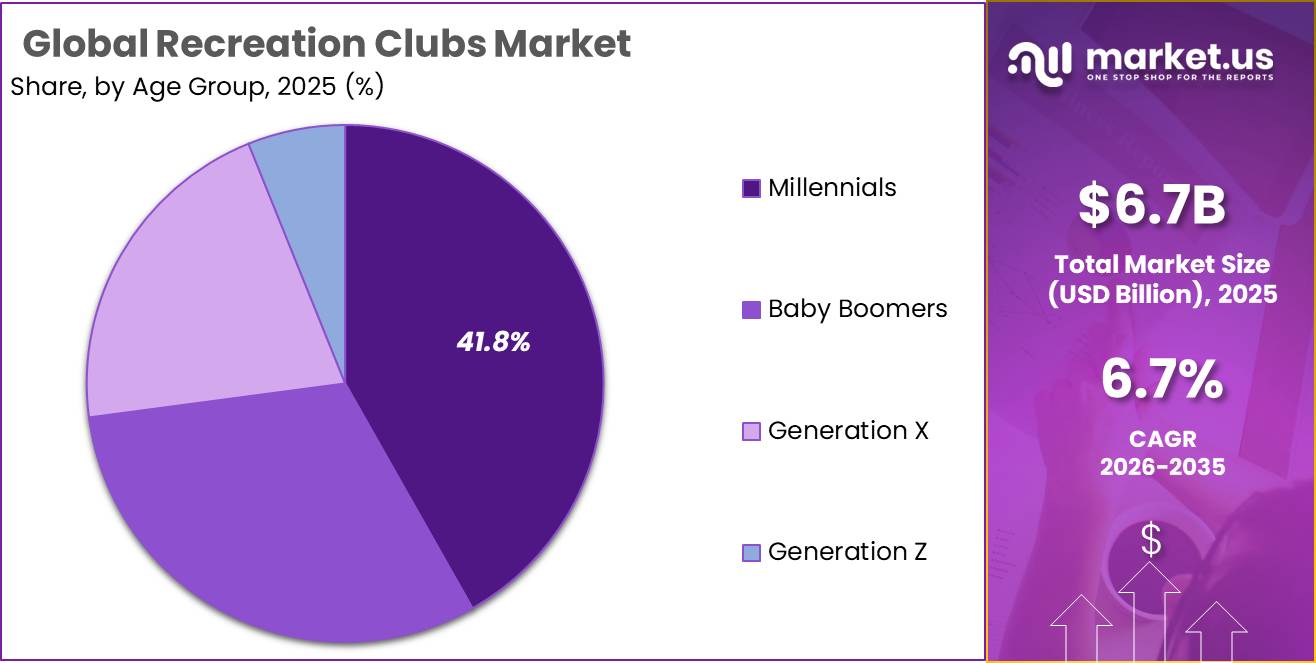

- Millennials lead the By Age Group segment with a 41.8% share.

- Group travelers lead the By Travelers Type segment with a 65.9% share.

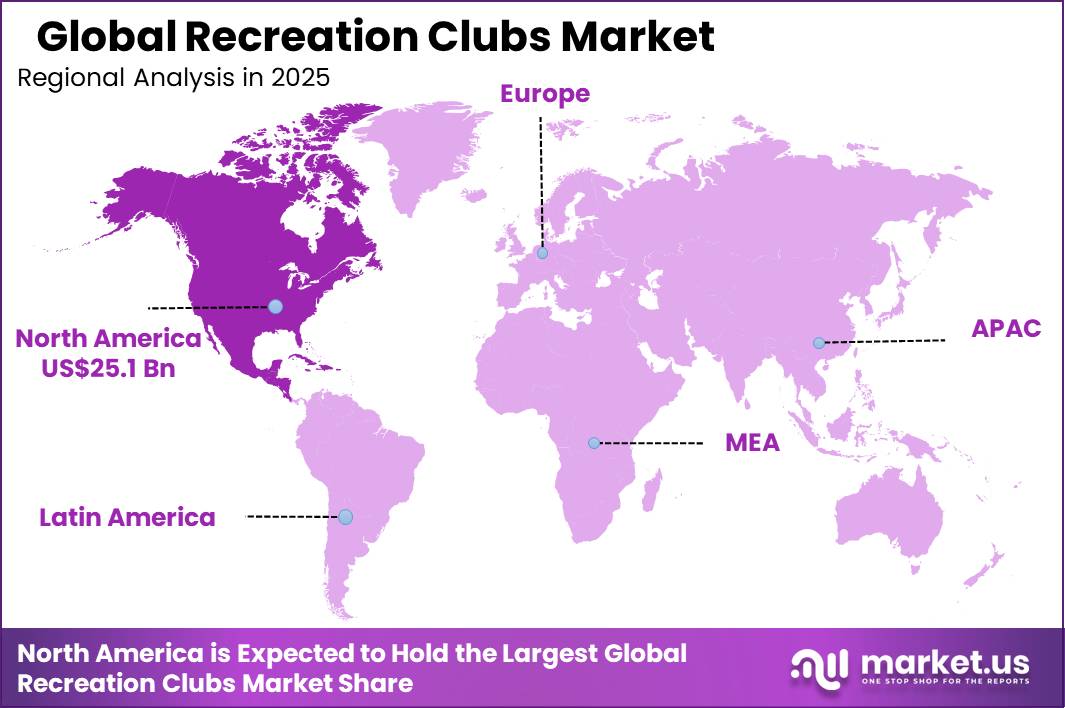

- North America leads the regional market with a 41.25% share.

Data from SFIA shows 250 million Americans participated in at least one sport, fitness, or recreational activity in 2025. This wide participation base expands the addressable pool for recreation club operators. As a result, operators targeting first-time participants gain a larger pipeline of potential members entering the category.

SFIA found that 158.8 million Americans engaged in CORE sport and fitness activity that same year. This reinforces a steady baseline of structured demand beyond casual participation. This signals that club operators offering consistent, repeatable programming can convert CORE participants into long-term paying members.

Category Analysis

Recreational Sports Clubs dominates with 59.7% due to structured athletic programming demand.

In 2025, Recreational Sports Clubs held a dominant market position in the By Category segment of Recreation Clubs Market, with a 59.7% share. These clubs operate structured athletic programs across tennis, swimming, and team sports facilities. This reflects steady member preference for organized physical activity over passive social spaces. Operators investing in coaching staff and tournament schedules capture the largest share of new memberships.

Non Sports Recreational Clubs serve members seeking social and lifestyle amenities rather than athletic programming. These venues focus on dining, networking, and leisure spaces over competitive facilities. As a result, this segment attracts professionals and retirees prioritizing community connection over fitness routines. Operators in this category compete on ambiance and exclusivity rather than sport infrastructure.

Age Group Analysis

Millennials dominates with 41.8% due to peak career and family life stage.

In 2025, Millennials held a dominant market position in the By Age Group segment of Recreation Clubs Market, with a 41.8% share. This generation drives membership growth through family-oriented programming and active social networking needs. Consequently, clubs targeting millennials emphasize flexible scheduling and child-friendly amenities. Operators aligning programming with career and parenting demands retain this segment longest.

Baby Boomers represent an aging member base seeking low-impact fitness and social engagement options. Data from Health Club Management shows adults aged 65+ grew as fitness members by 8.6% year over year in 2025. This signals rising demand for senior-focused wellness programming within recreation clubs. Operators expanding accessible facilities can capture this fast-growing demographic.

Generation X members typically hold established careers and higher discretionary income for premium memberships. This group favors structured fitness routines combined with networking opportunities at recreation clubs. By contrast, their engagement centers on convenience and time efficiency over social exploration. Clubs offering express fitness formats retain Generation X members effectively.

Travelers Type Analysis

Group dominates with 65.9% due to strong shared social travel preference.

In 2025, Group held a dominant market position in the By Travelers Type segment of Recreation Clubs Market, with a 65.9% share. Members traveling in groups prioritize shared social experiences and collective club events. This reflects how recreation clubs function as community hubs rather than individual fitness destinations. Operators hosting group travel packages and events capture stronger loyalty within this segment.

Solo travelers represent members seeking independent recreation experiences without group commitments. These members value flexible scheduling and personal wellness routines over scheduled social activities. Instead, solo-focused offerings emphasize private training and individual amenity access. Clubs catering to this segment differentiate through personalized service models.

Key Market Segments

By Category

- Recreational Sports Clubs

- Non Sports Recreational Clubs

By Age Group

- Millennials

- Baby Boomers

- Generation X

- Generation Z

By Travelers Type

- Group

- Solo

Drivers

The aging population is reshaping recreation club demand worldwide. By 2030, the global population aged 65 and above will exceed 1 billion people, while adults over 65 already represent more than 29% of Japan’s population. Approximately 10,000 Americans enter this age group daily, expanding the senior membership pool.

Senior-focused programs ranked among the top three global fitness trends in 2025. Structured strength training increases muscular strength by around 40% and cuts fall risk by nearly 30%, while 75% of participants report improved mood. Therefore, senior members typically show lower churn and higher lifetime value for club operators.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health & Wellness Consciousness — Rising prevalence of lifestyle diseases and preventive health adoption accelerating membership demand | +2.1% | Global core; highest intensity in North America & EU; rapid adoption in APAC urban corridors | Medium term (2–4 years) |

| Disposable Income Expansion — APAC middle-class surge and rising per-capita spending power unlocking first-time club memberships | +1.8% | APAC (China, India) core; South America spill-over; MEA emerging | Long term (≥ 4 years) |

| Digital-Physical Integration — AI-powered club management, hybrid fitness models, and SaaS platform adoption reshaping operational economics | +1.6% | North America & EU early adopters; APAC fast-follower corridors | Short term (≤ 2 years) |

| Corporate Wellness Mandates — Employer-sponsored recreation partnerships and preventive care programs institutionalizing B2B membership demand | +1.3% | North America & EU core; emerging in APAC enterprise hubs (Singapore, Mumbai, Beijing) | Medium term (2–4 years) |

| Emerging Sports Formats — Padel, pickleball, and experiential sports driving greenfield club investment and member acquisition | +1.2% | EU & North America core; India, Southeast Asia spill-over | Short-to-Medium term (1–3 years) |

| Aging Population & Senior Fitness — Longevity-focused programs and 65+ demographic expansion creating an underserved, high-LTV membership segment | +1.0% | North America, Western Europe, Japan core; China emerging | Long term (≥ 4 years) |

Restraints

Macroeconomic pressure is weighing on recreation club spending in 2026. US PCE inflation reached 4.5% in Q1 2026, while euro area inflation accelerated to 3.0% in April, including energy price inflation of 10.9%. These pressures push households to prioritize essential expenses over discretionary club memberships.

The US personal savings rate fell 26% in April to a pre-pandemic low, while real disposable income contracted by 0.5%. Consumer confidence weakened, with the Expectations Index at 74.4 in May. As a result, operators face renewal hesitancy, lower per-member spending, and slower new member acquisition.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic Headwinds & Discretionary Spend Compression | -1.5% | North America, Western Europe (EU core) | Short term (≤ 2 years) |

| Prohibitive Membership Fee Structures & Affordability Barriers | -1.2% | North America core, ANZ, UK | Medium term (2–4 years) |

| Structural Labor Shortages & Escalating Wage Costs | -0.9% | North America, Western Europe, Australia | Short–Medium term |

| Digital Disruption from Home Fitness & App-Based Platforms | -0.8% | Global (APAC + North America most acute) | Medium–Long term (≥ 3 years) |

| Tariff-Driven Equipment & Infrastructure CapEx Inflation | -0.7% | North America, EU, APAC import corridors | Short–Medium term |

| Demographic Misalignment & Generational Membership Attrition | -0.6% | North America, Western Europe, Japan | Long term (≥ 4 years) |

Challenges

Facility infrastructure costs are straining recreation club operators through rising occupancy and energy expenses. Lease agreements typically include annual rent escalations of 2 to 3%, while prime club locations command rental rates of USD 25 to 65 per square foot annually in major North American markets.

US commercial electricity prices rose 6.4% between January 2025 and January 2026, pressuring climate-controlled pools and fitness equipment. Emergency repairs can cost 10 to 15 times more than routine upkeep. Consequently, operators must balance facility modernization against expansion plans while managing rising capital demands.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Chronic Skilled Workforce Attrition | -1.4% | North America, EU, APAC developed markets | Medium term (2–4 years) |

| Member Retention & Churn Pressure | -1.2% | Global; acute in North America & EU mature markets | Medium term (2–4 years) |

| Digital Integration & Tech Debt | -1.0% | North America core; EU regulatory hubs; APAC urban corridors | Long term (≥ 4 years) |

| Facility Infrastructure CapEx Burden | -0.9% | North America, Western EU; high-rent urban clusters globally | Short term (≤ 2 years) |

| Supply Chain & Equipment Cost Inflation | -0.8% | Global; acute in APAC manufacturing corridors & North America | Medium term (2–4 years) |

| Cybersecurity & Data Governance Risk | -0.6% | North America, EU compliance hubs; APAC digital-first markets | Long term (≥ 4 years) |

Opportunities

Recreation clubs hold an untapped opportunity to monetize member data from check-ins, wearables, and spending patterns. AI-powered personalization can optimize pricing, predict churn, and increase adoption of high-margin services such as personal training, nutrition coaching, and spa treatments.

Operators with large member bases can build anonymized, consent-compliant wellness insights for adjacent sectors like health insurance and wellness real estate. This signals an incremental revenue stream worth approximately 8 to 12% of total operating revenues for first-mover operators investing in data monetization capabilities.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Corporate Wellness B2B Channel Monetization | +1.8% | North America, UK, Western Europe | Short term (≤ 2 years) |

| APAC & Middle East Greenfield Market Expansion | +2.2% | India, GCC, Southeast Asia, China Tier-2/3 | Medium term (2–4 years) |

| AI-Driven Member Data Monetization & Personalization-as-a-Service | +1.5% | North America, EU, APAC | Medium term (2–4 years) |

| Healthspan & Longevity Services Integration | +1.7% | North America, UK, GCC, APAC premium | Medium term (2–4 years) |

| PE-Backed M&A Roll-Up & Consolidation | +2.5% | North America, Western Europe | Short–Medium term (1–4 years) |

| Mixed-Use Real Estate & Live-Work-Play Embedded Club Models | +1.4% | APAC, MENA, North America suburban | Long term (≥ 4 years) |

Regional Analysis

North America Dominates the Recreation Clubs Market with a Market Share of 41.25%, Valued at USD 25.1 Billion

North America leads the Recreation Clubs Market through dense urban populations and an established private membership culture. As reported by The Club, the operator opened a second fitness studio location in Charlotte during April 2026. This expansion introduced heated workout concepts and expanded wellness programming for regional members. Such localized growth reinforces the structural advantage North American operators hold in mature, high-density metropolitan markets.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East and Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

The Arts Club, founded in 1863 in Mayfair, London, operates a dual-location model spanning London and Dubai. This cross-market footprint positions the club directly within two of the world’s highest-spending private membership corridors. However, its culturally exclusive positioning limits addressable membership volume, creating concentration risk if high-net-worth discretionary spending contracts in either market.

Soho House has built a global network of members clubs targeting creative professionals across urban markets. This multi-city infrastructure creates retention advantages through reciprocal access, which reduces churn among members who travel frequently. By contrast, high expansion costs and a younger, income-variable membership base expose Soho House to affordability pressure when discretionary budgets tighten across its core demographic.

Key Players

- The Arts Club

- Soho House

- The Hurlingham Club

- Carolina Country Club

- The Battery

- The Tanglin Club

- New York Yacht Club

- Northwood Club

- CORE Club

- 5 Hertford Street

- The Carnegie Club at Skibo Castle

Recent Developments

- May 2025 – TSG Consumer signed a definitive agreement to acquire EōS Fitness, a gym chain operating more than 200 locations, to accelerate expansion into new markets and support innovation across its fitness offerings.

- February 2026 – Planet Fitness announced the opening of 181 new clubs during 2025, expanding its global footprint to 2,896 clubs and adding approximately 1.1 million net new members.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 60.9 Billion |

| Forecast Revenue (2035) | USD 116.5 Billion |

| CAGR (2026-2035) | 6.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Market Opportunity Analysis, Technology and Innovation Landscape, Competitive Landscape, Recent Developments |

| Segments Covered | By Category (Recreational Sports Clubs, Non Sports Recreational Clubs), By Age Group (Millennials, Baby Boomers, Generation X, Generation Z), By Travelers Type (Group, Solo) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East and Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | The Arts Club, Soho House, The Hurlingham Club, Carolina Country Club, The Battery, The Tanglin Club, New York Yacht Club, Northwood Club, CORE Club, 5 Hertford Street, The Carnegie Club at Skibo Castle |

| Customization Scope | Customization for segments, region/country-level will be provided. Additional customization can be done based on requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |