Quick Navigation

Report Overview

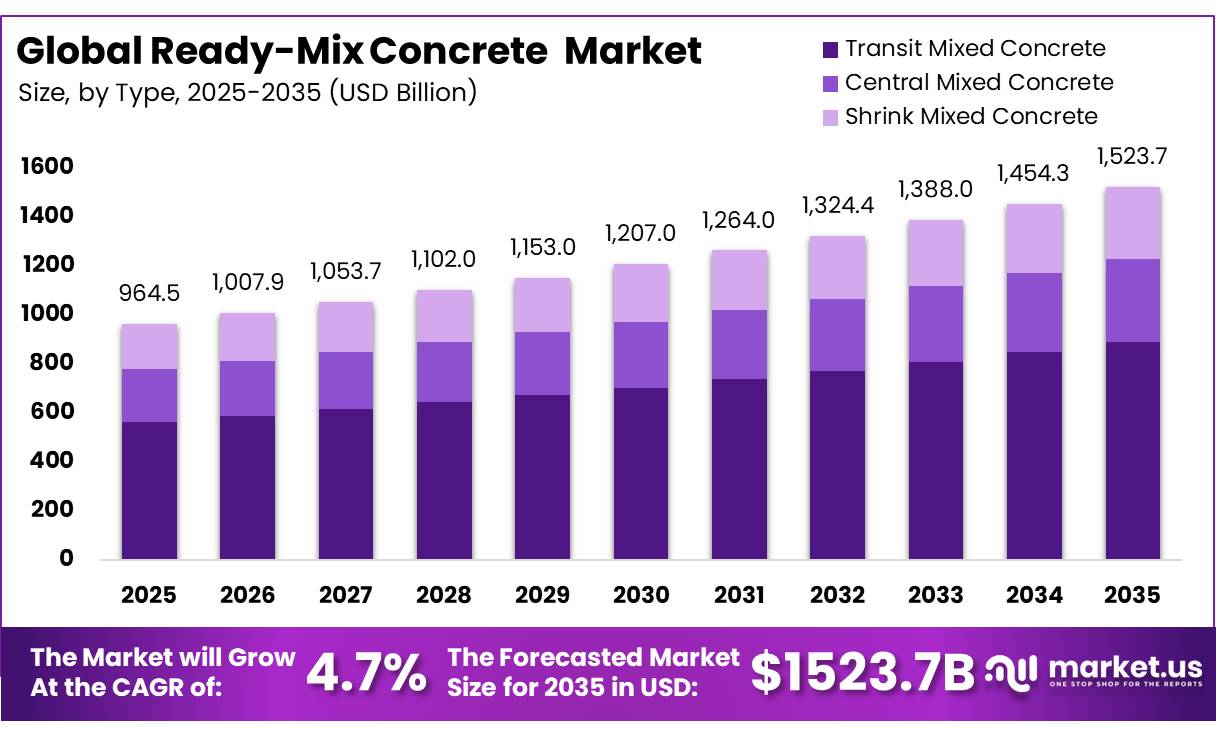

In 2025, the Global Ready Mix Concrete Market was valued at USD 964.5 billion, and between 2026 and 2035, this market is estimated to register a CAGR of 4.7%, reaching about USD 1523.7 billion by 2035. Asia Pacific held a dominant market position, capturing more than a 70.40% share, holding USD 679.01 billion in revenue.

The ready-mix concrete industry supplies factory-batched concrete directly to construction sites, improving mix consistency, placement speed, labor efficiency, and quality control. Demand is closely linked to housing, commercial buildings, highways, bridges, utilities, and industrial facilities. The industry remains highly local because fresh concrete must be transported and placed within controlled time limits, making plant location, fleet utilization, raw-material access, and project scheduling central to profitability. The current industrial scenario is mixed but resilient.

- The U.S. Geological Survey estimated that U.S. cement shipments reached 100 million metric tons, valued at USD 17 billion, in 2025; ready-mix producers purchased about 70%–75% of cement sales.

- S. Census Bureau data showed total construction spending at a seasonally adjusted annual rate of USD 2.172 trillion in April 2026, including USD 532.7 billion in public construction and USD 149.6 billion in highway construction. These figures indicate a substantial demand base for concrete despite interest-rate, labor, energy, and transport-cost pressures.

Key Takeaways

- The Global ready-mix concrete market was valued at USD 964.5 billion in 2025.

- The Global market is projected to grow at a CAGR of 4.7% and is estimated to reach USD 1,523.7 billion by 2035.

- On the basis of type, transit mixed concrete dominated the market, constituting 58.3% of the total market share.

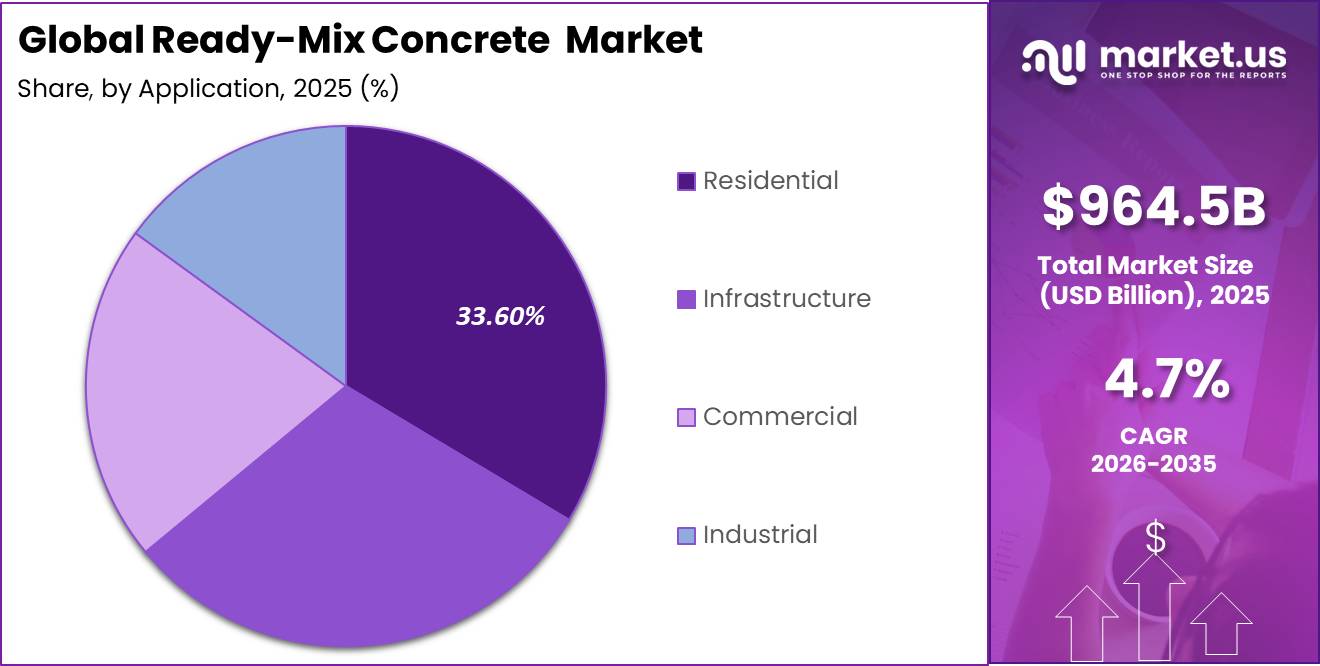

- Based on application, the residential segment dominated the ready-mix concrete market, with a substantial market share of around 33.6%.

- Based on the production method, off-site production led the market, comprising 63.0% of the total market.

- Among the mixer types, barrel truck/in-transit mixers held a major share in the ready-mix concrete market, accounting for 73.0% of the market share.

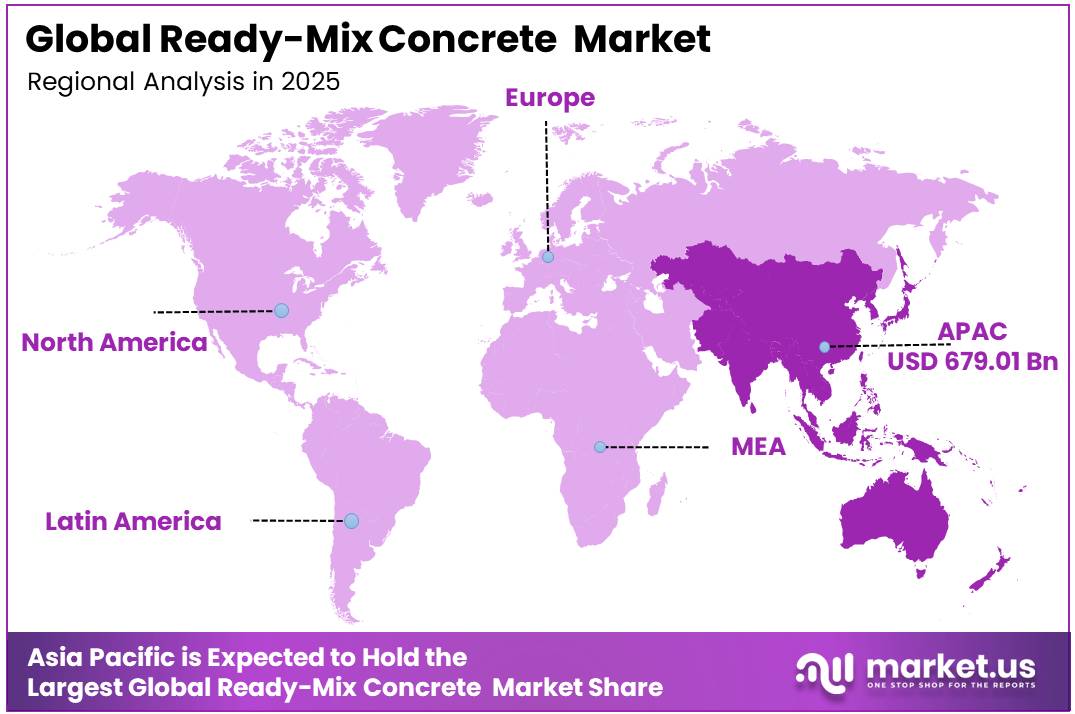

- In 2025, Asia-Pacific was the most dominant region in the ready-mix concrete market, accounting for 70.4% of the total global market.

Infrastructure renewal, urban development, logistics facilities, data centers, and public works remain major demand drivers. In March 2026, Eurostat reported that civil-engineering output increased 5.7% month over month in the euro area and 4.8% in the European Union, although total construction remained below the previous year. This uneven performance favors suppliers with flexible batching capacity, disciplined fleet management, and exposure to infrastructure projects.

Future opportunities will increasingly center on low-carbon mixes, supplementary cementitious materials, recycled aggregates, digital dispatch, automated batching, and zero-emission delivery fleets. The American Cement Association reports that about 5% of concrete is returned from construction sites annually and targets a 100% reduction in concrete-production energy emissions by 2050. Meanwhile, the OECD estimates that USD 6.9 trillion of annual infrastructure investment will be required by 2030, supporting long-term concrete demand while encouraging durable, efficient, and lower-carbon construction solutions across both developed and emerging urban economies.

Ready-Mix Concrete Market Segmentation

Type Analysis

Transit Mixed Concrete leads with 58.30% due to flexible delivery and reliable on-site placement.

In 2025, Transit Mixed Concrete held a dominant market position, capturing more than a 58.30% share. As of June 2026, it remained preferred because concrete ingredients are mixed during transportation, helping contractors receive a workable and uniform product at the project location. This method supports residential, commercial, and infrastructure construction where delivery timing and mix consistency are important. Its use also reflects transit mixer availability and the ability to serve projects away from batching plants. Contractors value the method because it reduces the need for separate mixing equipment at the construction site and supports continuous concrete placement.

Central Mixed Concrete is the fastest-growing segment. Its growth is supported by quality control, accurate batching, and consistent mixing at centralized plants. The segment is gaining attention for projects that require dependable strength, uniformity, and efficient production.

Application Analysis

Residential leads with 33.60% as steady housing construction supports concrete demand.

In 2025, Residential held a dominant market position, capturing more than a 33.60% share. As of June 2026, the segment continued to benefit from demand for houses, apartments, renovation projects, and urban residential developments. Ready-mix concrete is used in foundations, floors, walls, driveways, and structural frames because it supports consistent quality and faster placement. Residential builders prefer centrally prepared concrete because it reduces on-site mixing work, improves material control, and helps maintain construction schedules. Urban expansion and the need for durable housing continue to support the segment’s leading position across established and developing construction markets.

Infrastructure remained the fastest-growing application segment. Its expansion is supported by rising work on roads, bridges, tunnels, airports, rail systems, and public utilities. Infrastructure projects require dependable concrete volumes, uniform strength, timely delivery, and efficient placement across long construction periods.

Production Method Analysis

Off-site Production leads as controlled batching improves consistency and efficiency.

In 2025, Off-site Production held a dominant market position, capturing more than a 63.00% share. As of June 2026, the method remained preferred because concrete is prepared in batching plants under controlled conditions before delivery to construction sites. This approach supports accurate material measurement, uniform mixing, quality, and faster site operations. Contractors benefit from lower on-site equipment needs, reduced material handling, and better coordination for residential, commercial, and infrastructure projects.

On-site Production continues to serve projects where flexible batching and immediate concrete placement are important. It is useful for remote locations, specialized construction work, and sites with changing volume requirements. The method gives contractors control over production timing, although it requires sufficient space, equipment, labor, and material storage at the project location.

Mixer Type Analysis

Barrel Truck/In-transit Mixers lead as reliable transport supports continuous concrete delivery.

In 2025, Barrel Truck/In-transit Mixers held a dominant market position, capturing more than a 73.00% share. As of June 2026, these mixers remained used because they combine concrete transportation with continuous drum rotation during delivery. This process helps maintain workable consistency, limits early setting, and supports timely placement at residential, commercial, industrial, and infrastructure sites. Their broad availability, familiar operating process, and suitability for delivery routes strengthen their role across ready-mix operations.

Volumetric Mixers are gaining attention for projects requiring flexible batch sizes and fresh mixing at the point of use. They allow materials to be measured and mixed on demand, helping contractors manage changing requirements, remote jobs, small pours, and specialized applications.

Key Market Segments

By Type

- Transit Mixed Concrete

- Central Mixed Concrete

- Shrink Mixed Concrete

By Application

- Residential

- Infrastructure

- Commercial

- Industrial

By Production Method Type

- Off-site Production

- On-site Production

By Mixer Type

- Barrel Truck/In-transit Mixers

- Volumetric Mixers

Driver

Government-Led Mega Infrastructure Investment Surge

In the United States, the Infrastructure Investment and Jobs Act (IIJA) — originally a USD 550 billion+ new spending commitment — continues disbursing funds through 2026–2027, with the American Society of Civil Engineers (ASCE) estimating a USD 373 billion bridge repair funding gap and system rehabilitation needs of USD 191.3 billion in bridge infrastructure alone; this creates a structurally protected federal demand pipeline for specialty concrete mixes including High-Density Concrete (HDC), Internally Cured Concrete (ICC), and Rapid-Set Concrete used in accelerated bridge replacement programs.

Across the GCC, infrastructure investments exceed USD 300 billion in planned future commitments, with Saudi Arabia’s Giga Projects — NEOM, The Line, Qiddiya — sustaining bulk cement and RMC consumption across the Tabuk and Riyadh regions, while the UAE’s Dubai Urban Plan 2040 and Abu Dhabi smart city initiatives reinforce a regional concrete market valued at USD 115 billion.

Morgan Stanley projects India’s infrastructure investment to rise from 5.3% of GDP in FY2024 to 6.5% by FY2029, and CRISIL estimates India will spend nearly ₹143 lakh crore on infrastructure across seven fiscal years through 2030 — more than double the preceding seven-year cumulative figure — ensuring that the government infrastructure vector remains the dominant, most durably funded demand driver for the RMC market through the medium term with a CAGR uplift conservatively modeled at +2.2 percentage points.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Led Mega Infrastructure Investment Surge | +2.2% | APAC (India, China); North America; GCC Middle East | Medium term (2–4 years) |

| Rapid Urbanization & Affordable Housing Demand | +1.6% | APAC (India, SE Asia); Sub-Saharan Africa; LatAm | Long term (≥ 4 years) |

| Structural Shift from On-Site Mixing to RMC | +1.2% | India, SE Asia, Africa, LatAm emerging markets | Medium term (2–4 years) |

| Green Concrete & Low-Carbon SCM Integration | +0.9% | EU regulatory core; North America; APAC; GCC | Long term (≥ 4 years) |

| Digital Batching, IoT & Smart Delivery Technology | +0.8% | North America, EU; APAC high-growth corridors | Medium term (2–4 years) |

| High-Performance & Specialty Concrete Admixtures | +0.7% | North America, EU; GCC; Tier-1 APAC urban markets | Medium term (2–4 years) |

Restraints

Escalating Environmental & Emissions Compliance Burden

In the United States, the Buy Clean Executive Order mandates that all federal purchasing agencies obtain Environmental Product Declarations (EPDs) for concrete building materials on federal projects, effective since January 2023 and expanding in scope through 2026 to cover additional project categories and lower Global Warming Potential (GWP) thresholds — with the GSA specifying maximum GWP limits as low as 404 kg CO₂ per cubic meter for 5,500–6,499 psi concrete mixes — a requirement that imposes LCA documentation costs of USD 15,000–45,000 per unique mix design per plant plus third-party EPD verification fees of USD 5,000–12,000, creating a cumulative compliance infrastructure investment of USD 80,000–250,000 per multi-plant RMC operator.

The GCCA launched its Low Carbon Ratings (LCR) framework for cement and concrete in April 2025, and in March 2026, mandatory environmental disclosure became a standard legal requirement for structural materials across multiple jurisdictions; specifying concrete strength at 56 days rather than 28 days can save 20 kg/m³ of cement and approximately 10 kg/m³ CO₂, but this requires contractual renegotiation with structural engineers and project owners who remain resistant to extending specification cure cycles that affect project handover timelines.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw Material Price Volatility (Cement, Aggregates, Energy) | -1.4% | Global — APAC, North America, EU, GCC | Short term (≤ 2 years) |

| Perishability Constraint & Logistics Radius Limitation | -1.1% | Global — acute in APAC, LatAm congested corridors | Medium term (2–4 years) |

| Escalating Environmental & Emissions Compliance Burden | -0.9% | EU primary; North America, India, GCC secondary | Medium term (2–4 years) |

| High CapEx Barriers & Fragmented Market Structure | -0.8% | India, SE Asia, Africa, LatAm emerging markets | Long term (≥ 4 years) |

| Interest Rate Sensitivity & Real Estate Investment Slowdown | -0.7% | North America, EU; emerging market spill-over | Short term (≤ 2 years) |

| Regulatory Fragmentation & Multi-Jurisdiction Permitting | -0.6% | India primary; SE Asia, Sub-Saharan Africa, LatAm | Medium term (2–4 years) |

Opportunity

Sub-Saharan Africa First-Time RMC Penetration

The RMI estimates that 80% of Africa’s 2050 building stock is yet to be constructed, implying that the overwhelming majority of the continent’s ultimate concrete demand is unserved by organized RMC operators — a white space with no parallel in any other major geographic market. Nigeria, Ethiopia, Kenya, Ghana, and Côte d’Ivoire are experiencing urban population growth rates of 3.5–5.2% per annum — 3–4× the global average — and collectively represent an urban construction investment addressable market of approximately USD 180–240 billion annually through 2035, yet RMC penetration across the region is estimated below 5–8% of concrete volumes, compared to 75–85% in mature markets.

The strategic entry thesis is not merely volume capture: Africa’s cement and concrete supply chains are highly localized, incumbents are still learning from global best practices given the industry’s relative youth, and the abundance of natural supplementary cementitious materials means that low-carbon RMC can be formulated at cost structures 25–35% below those requiring imported fly ash or GGBS — creating a first-mover who enters with lean, SCM-integrated plant configurations a structural and sustainable unit cost advantage over subsequent entrants.

Opportunity Impact Analysis

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Sub-Saharan Africa First-Time RMC Penetration | +1.8% | Nigeria, Ethiopia, Kenya, Ghana, Côte d’Ivoire | Medium term (2–4 years) |

| Data Center & Semiconductor Fab Specialty Concrete | +1.5% | North America; APAC (India, Taiwan, Korea); EU | Short term (≤ 2 years) |

| 3D Printable Concrete Mix Formulation Supply | +1.3% | North America, EU; APAC (India at 74.5% CAGR) | Medium term (2–4 years) |

| Carbon-Negative Concrete Premium Product Line | +1.1% | EU regulatory core; North America; GCC | Long term (≥ 4 years) |

| M&A Consolidation & Vertical Integration Roll-Up | +0.9% | APAC fragmented markets; North America; Australia | Short term (≤ 2 years) |

| AI-Driven Predictive Concrete-as-a-Service (CaaS) Model | +0.7% | North America, EU; Tier-1 APAC metro corridors | Medium term (2–4 years) |

Challenge

Mixer Driver Chronic Turnover & CDL Shortage

Each percentage point of annual turnover represents approximately 26,500 driver-exits nationally in a US industry of 95,000 mixer drivers, with 75% of those departing having more than one year’s tenure — meaning the sector is systematically losing its most productive, lowest-error-rate personnel while retaining only the newest and least experienced cohort; MIT’s MIT Concrete Sustainability Hub analysis corroborates this dynamic, finding that increasing average driver tenure would yield significant productivity gains as more experienced drivers reduce truck idle time substantially compared to newer drivers.

The federal enforcement tightening in 2025–2026 has materially worsened the structural hiring pool: FMCSA initiatives including Drug and Alcohol Clearinghouse CDL downgrades, non-domiciled CDL restrictions, and English language proficiency enforcement that can trigger immediate out-of-service orders are projected to remove as many as 200,000 commercially licensed drivers from eligibility across all trucking categories, directly compressing the pool from which RMC producers recruit.

The productivity arithmetic is stark: an RMC plant operating a fleet of 20 transit mixers with a 28% annual driver turnover replaces 5–6 drivers per year; each driver replacement cycle costs USD 8,000–14,000 in recruitment advertising, pre-employment medical and licensing verification, onboarding, and productivity ramp-up time at 5 replacements per year, the annual people-friction cost per plant is USD 40,000–70,000 before accounting for the 30–45 load per month productivity deficit during the transition period.

Challenges Impact Analysis

| Challenge | (~) % CAGR Friction | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Mixer Driver Chronic Turnover & CDL Shortage | -1.2% | North America primary; EU, APAC secondary | Long term (≥ 4 years) |

| Water Scarcity & Washwater Recycling Complexity | -0.9% | APAC (India, SE Asia); GCC; Mediterranean EU | Medium term (2–4 years) |

| Decarbonization Cost Transition & CCUS Deployment Gap | -0.9% | EU primary; North America, India, GCC secondary | Long term (≥ 4 years) |

| On-Site Pour Scheduling & Coordination Breakdown | -0.8% | Global — acute in APAC congested corridors | Medium term (2–4 years) |

| Digital Technology Adoption Gap in SME Base | -0.7% | APAC, LatAm, Africa fragmented SME markets | Medium term (2–4 years) |

| Aggregate Quality Variability & Supply Chain Friction | -0.6% | APAC; Sub-Saharan Africa; South America | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Geopolitical Realignment and Trade Barriers Reshaping Ready-Mix Concrete Supply Networks

Current geopolitical tensions are reshaping the ready-mix concrete market through unstable shipping routes, changing trade policies, carbon-border measures, and growing pressure to secure cement and clinker closer to construction markets. Although ready-mix concrete is produced locally, its cost structure remains exposed to internationally traded cement, clinker, supplementary materials, fuel, machinery, and spare parts. As a result, disruptions in maritime trade can quickly affect batching costs, delivery schedules, and project pricing.

UN Trade and Development reported in September 2025 that global seaborne trade was expected to increase by only 0.5% during the year, while geopolitical rerouting had driven nearly 6% growth in ton-miles during 2024. Ship tonnage passing through the Suez Canal remained approximately 70% below its 2023 average by early May 2025. These longer routes increase fuel use, insurance expenses, freight charges, and delivery times for imported cementitious materials.

Import dependence also creates regional supply risks. The U.S. Geological Survey estimated that the United States imported 23 million metric tons of hydraulic cement and 660,000 metric tons of clinker in 2025, with net import reliance equal to 21% of apparent cement consumption. Turkey supplied 32% of U.S. cement imports during 2021–2024, followed by Canada at 20%, Vietnam at 13%, and Greece at 9%. This concentration encourages producers to expand terminals, storage capacity, and alternative sourcing arrangements.

Regulatory fragmentation is adding another layer of pressure. The European Union’s Carbon Border Adjustment Mechanism entered its definitive phase on January 1, 2026, covering imported cement and requiring authorization, emissions reporting, and customs validation. These developments are encouraging ready-mix producers to prioritize domestic cement supply, lower-carbon binders, regional sourcing, and longer-term procurement contracts. However, higher compliance costs, shipping uncertainty, and supplier qualification requirements may continue to raise operating complexity across internationally exposed construction markets.

Regional Analysis

Asia-Pacific leads the Ready-Mix Concrete Market with 70.40% and USD 673.01 billion.

In 2025, Asia-Pacific held the dominant position in the Ready-Mix Concrete Market, accounting for 70.40% and USD 673.01 billion. The region benefits from large urban populations, expanding transport networks, residential development, and sustained investment in industrial and public infrastructure. China remains a major production base; its National Bureau of Statistics reported cement output of 178.27 million tonnes during January–February 2026, up 6.8% year over year.

Regional financing also supports construction activity. The Asian Development Bank committed USD 29.3 billion across Asia and the Pacific in 2025, including USD 23.5 billion for public-sector projects. Australia further recorded AUD 80.01 billion of total construction work during the December 2025 quarter. These indicators support steady demand for factory-batched concrete across roads, bridges, housing, utilities, logistics facilities, and urban redevelopment projects throughout the region. Local batching networks also improve timely project delivery.

Key Regions and Countries Covered

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Ready-mix concrete producers focus on strengthening regional batching networks, delivery efficiency, product quality, and raw material security to maintain competitiveness. A major priority is developing specialized concrete mixes, including high-strength, self-compacting, fiber-reinforced, rapid-setting, and lower-carbon formulations that meet the changing needs of residential, commercial, industrial, and infrastructure projects. Companies also invest in automated batching systems, digital order management, fleet tracking, and predictive maintenance to improve mix accuracy, reduce delivery delays, and control operating costs.

Vertical integration with cement, aggregate, and admixture operations helps producers secure material availability and manage price volatility. Strategic plant expansion near urban construction zones and major infrastructure corridors supports faster deliveries and wider customer coverage. Producers further strengthen their market position through acquisitions of local batching plants, recycling facilities, and aggregate suppliers. Long-term supply contracts with contractors and public infrastructure agencies support stable order volumes. In addition, companies increasingly focus on recycled aggregates, supplementary cementitious materials, water reuse, and energy-efficient production to meet sustainability requirements and compete for high-value construction projects.

Market Key Players

- Holcim Group

- Cemex

- Heidelberg Materials

- CRH plc

- UltraTech Cement

- ACC Limited

- U.S. Concrete

- Vicat

- Buzzi

- China National Building Material

- Vulcan Materials Company

- Barney & Dickenson

- Dillon Bros Concrete

- Livingston’s Concrete Service

Key Development

- In November 2025, Holcim Group completed the acquisition of P. J. Thory Limited, Gemmix Limited, and Pro Minimix Limited in the United Kingdom. The transaction added nine operating sites, including ready-mix concrete plants, quarries, and a recycled-aggregate facility, while bringing around 130 employees into Holcim’s regional network.

- In September 2025, CRH plc completed its US$2.1 billion acquisition of Eco Material Technologies, a major North American supplier of supplementary cementitious materials. The transaction strengthened CRH’s access to fly ash, pozzolans, synthetic gypsum, and green cement used in next-generation cement and ready-mix concrete production.

- In October 2025, Cemex completed the sale of its Panama operations to Grupo Estrella for an enterprise value of approximately US$200 million. The divested portfolio included a cement plant, ready-mix concrete and aggregate assets, while Cemex increased its ownership in Couch Aggregates to expand its materials position in the southeastern United States.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 964.5 Bn |

| Forecast Revenue (2035) | USD 1523.7 Bn |

| CAGR (2026-2035) | 4.7% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Transit Mixed Concrete, Central Mixed Concrete, and Shrink Mixed Concrete), By Application (Residential, Infrastructure, Commercial, and Industrial), By Production Method (Off-site Production and On-site Production), By Mixer Type (Barrel Truck/In-transit Mixers and Volumetric Mixers) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Holcim Group, Cemex, Heidelberg Materials, CRH plc, UltraTech Cement, ACC Limited, U.S. Concrete, Vicat, Buzzi, China National Building Material, Vulcan Materials Company, Barney & Dickenson, Dillon Bros Concrete, Livingston’s Concrete Service, and Infra.Market. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |