Quick Navigation

Report Overview

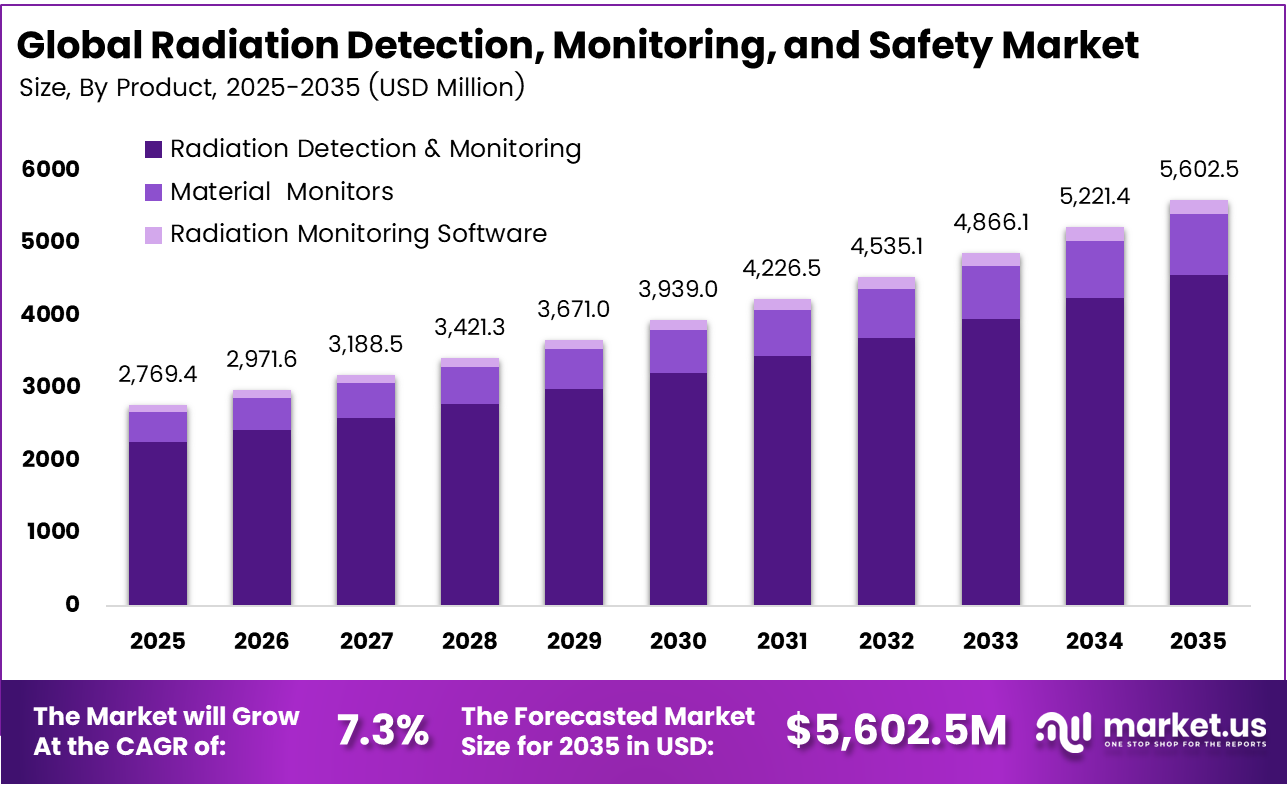

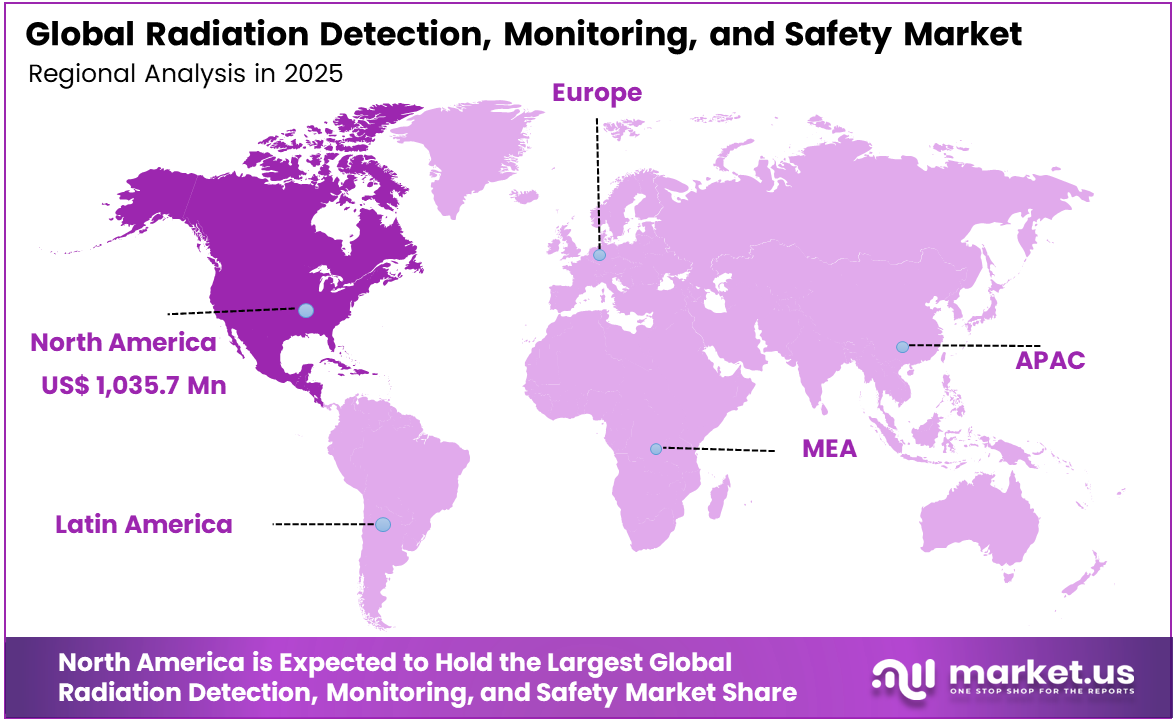

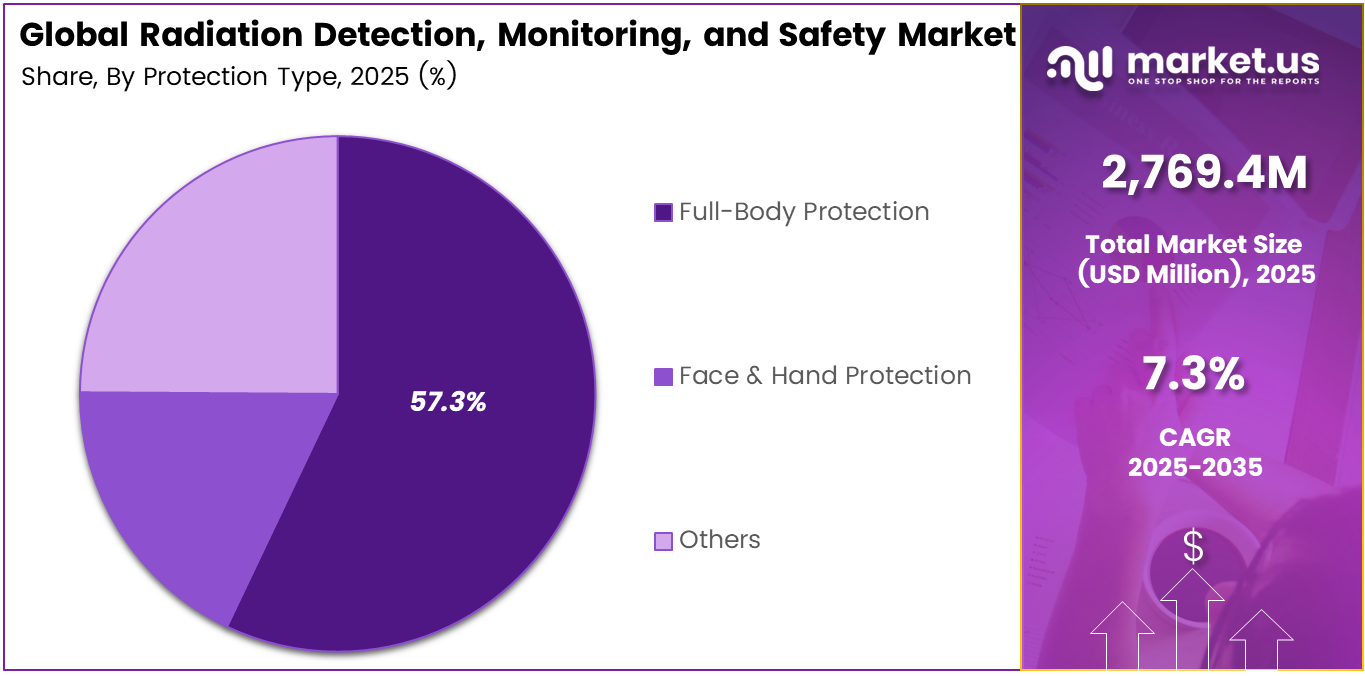

The Global Radiation Detection, Monitoring, and Safety Market size is expected to be worth around USD 5,602.5 million by 2035, from USD 2,769.4 million in 2025, growing at a CAGR of 7.3% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than 37.4% share and generating USD 1,035.7 million in revenue.

Radiation Detection, Monitoring, and Safety refers to the systems and practices used to identify, measure, and control exposure to ionizing radiation. These solutions include detectors, dosimeters, and protective equipment that help ensure safe environments in healthcare, nuclear, industrial, and research settings while protecting people and surroundings from harmful radiation effects.

Stricter occupational and environmental rules are accelerating the adoption of advanced radiation monitoring systems. Regulators now require routine dosimetry, incident tracking, and emergency drills across hospitals, nuclear plants, and industrial facilities. This compels organizations to replace analog meters with connected instruments that securely store long-term exposure data for audits, compliance reviews, and insurance validation.

The market for Radiation Detection, Monitoring, and Safety is driven by increasing use of radiation in healthcare, nuclear energy, and industrial applications. Growing focus on worker and patient safety is encouraging the adoption of reliable monitoring systems. Strict regulatory requirements and rising awareness about radiation risks are also supporting demand for advanced detection technologies and continuous monitoring solutions across various environments.

Demand is increasing due to the growing number of imaging and nuclear medicine procedures worldwide. Rising cancer and chronic disease cases are adding several million patients annually, leading hospitals to expand CT, PET, and interventional units. Accurate dose monitoring is becoming essential to protect both patients and healthcare workers in these high-exposure environments.

For instance, in September 2025, Burlington Medical entered a strategic partnership with Radiaction Medical to pair lighter, lead-free protective garments with Radiaction’s Dynamic Smart Shield system in cath labs. The collaboration targets a step-change reduction in scatter radiation and orthopedic strain for interventional teams, signaling a clear shift away from traditional heavy aprons.

Key Takeaway

- In 2025, the Radiation Detection & Monitoring segment held a dominant market position, capturing a 81.4% share of the Global Radiation Detection, Monitoring, and Safety Market.

- In 2025, the Solid-state Detectors segment held a dominant market position, capturing a 40.5% share of the Global Radiation Detection, Monitoring, and Safety Market.

- In 2025, the Full-Body Protection segment held a dominant market position, capturing a 57.3% share of the Global Radiation Detection, Monitoring, and Safety Market.

- In 2025, the Non-Hospitals segment held a dominant market position, capturing a 74.1% share of the Global Radiation Detection, Monitoring, and Safety Market.

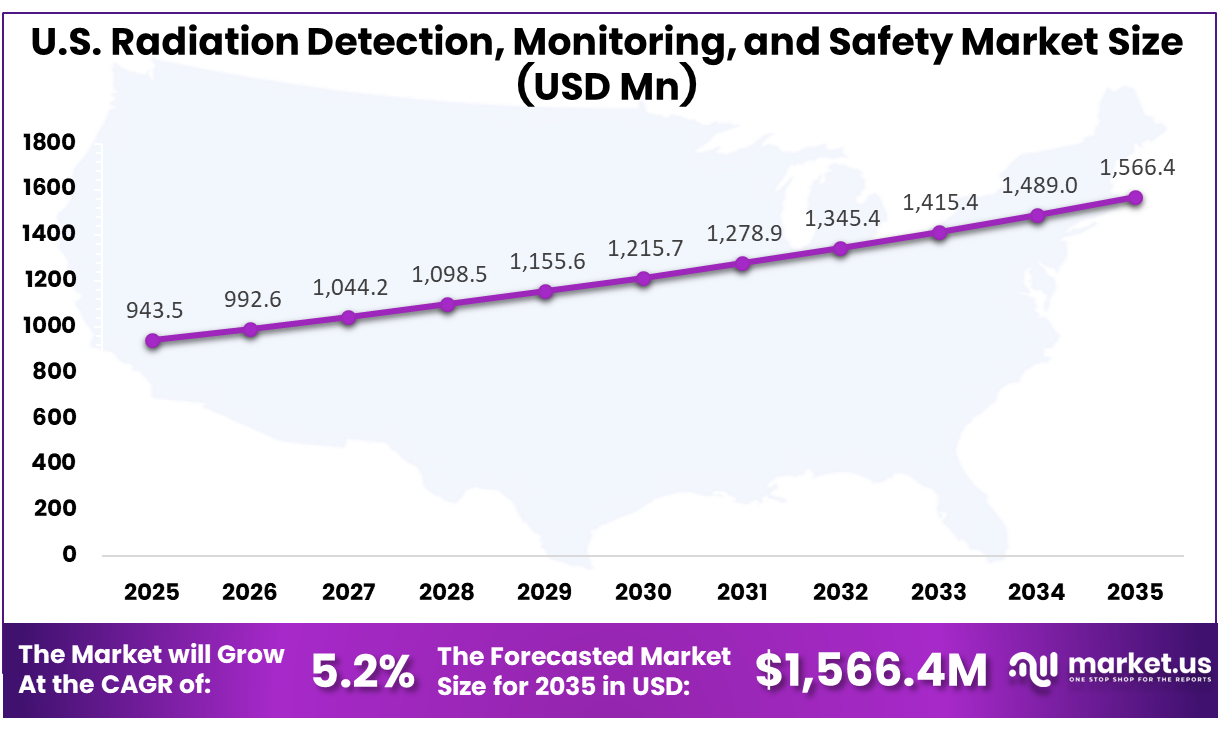

- The U.S. Radiation Detection, Monitoring, and Safety Market was valued at USD 943.5 Million in 2025, with a robust CAGR of 5.2%.

- In 2025, North America held a dominant market position in the Global Radiation Detection, Monitoring, and Safety Market, capturing more than a 37.4% share.

Role of Generative AI

Generative AI is being layered onto radiation monitoring systems, converting detector counts into meaningful patterns and early warnings. In medical imaging, AI-based protocol optimization is helping reduce repeat scans, lowering patient exposure by around 20–30% in some workflows when implemented effectively across radiology departments.

In nuclear and industrial environments, machine learning models process continuous sensor data to detect anomalies and predict equipment issues. Studies indicate improvements in detection accuracy and faster response times, with some pilot programs showing double-digit percentage gains in sensitivity and decision speed compared with traditional manual monitoring approaches.

Investment and Business Benefits

Investment opportunities are opening in portable instruments, rugged wireless networks, and analytics platforms as buyers shift toward integrated systems. Recurring software and service revenue can represent over 40% of total spending across equipment life cycles. Startups combining low-power sensors, secure connectivity, and simple dashboards are gaining attention from investors seeking stable, regulation-driven returns.

The business benefits of modern radiation detection programs are reflected in fewer incidents, reduced compensation claims, and smoother inspections. Some facilities report double-digit reductions in unscheduled downtime after adopting automated alarms and geo-tagged dose reporting. Clear exposure history supports better decision-making, allowing safety managers to justify infrastructure upgrades based on measurable radiation trends.

Regional Analysis

In 2025, North America held a dominant market position in the Global Radiation Detection, Monitoring, and Safety Market, capturing more than 37.4% share and generating USD 1,035.7 million in revenue. This dominance is due to strong radiation safety rules, advanced healthcare infrastructure, and wide use of nuclear medicine, diagnostic imaging, and radiation therapy across the region. North America also has a well-established nuclear power, defense, research, and industrial testing base that requires continuous monitoring. High awareness of occupational safety, faster adoption of advanced detectors, and regular investments in emergency preparedness further support the region’s leading position.

For instance, in October 2024, Ludlum Measurements expanded deliveries of portable survey meters, area monitors, and contamination detectors to U.S. nuclear utilities and federal sites, supported by broader North American demand highlighted in recent market studies. Its rugged instruments remain standard in many U.S. facilities, reinforcing North America’s central role in field-deployable radiation monitoring for power generation, research, and emergency response.

U.S. Radiation Detection, Monitoring, and Safety Market Size

The market for Radiation Detection, Monitoring, and Safety within the U.S. is growing tremendously and is currently valued at USD 943.5 million. The market has a projected CAGR of 5.2%. The market is growing due to the rising use of diagnostic imaging, nuclear medicine, and radiation therapy across U.S. healthcare facilities. Strong safety rules for hospitals, nuclear plants, laboratories, and industrial sites are increasing the demand for accurate monitoring systems. Growing investment in worker safety, emergency preparedness, and contamination control is also supporting the adoption of advanced detectors, dosimeters, and protective equipment across the country.

For instance, in September 2024, General Atomics Electronic Systems advanced U.S. leadership in radiation-hardened electronics and monitoring for defense and space applications, as noted in industry reporting on North American radiation-detection markets. Its high-reliability sensors and power systems, integrated into U.S. military and space programs, strengthen North America’s technological edge in extreme-environment radiation detection and protection.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Product Analysis

In 2025, the Radiation Detection & Monitoring segment held a dominant market position, capturing a 81.4% share of the Global Radiation Detection, Monitoring, and Safety Market. This dominance is due to the essential role of monitoring systems in ensuring safe use of radiation across industries. Hospitals, nuclear sites, and industrial facilities depend on accurate detection to track exposure and prevent risks. Continuous monitoring supports compliance and helps maintain controlled environments where radiation is actively used.

Radiation detection systems are widely adopted because they provide real-time visibility of dose levels and contamination. Their use supports routine operations and emergency response. Growing safety awareness and regulatory pressure encourage organizations to invest in reliable monitoring tools that protect workers, patients, and the surrounding environments from potential radiation exposure.

For instance, in February 2026, Teledyne FLIR increased production of its handheld radiation detection devices to support security operations at major global events, showing how portable instruments are now standard in field screening and emergency readiness. Higher demand from security and public safety agencies directly lifts the need for detection and monitoring products in non-medical settings.

Composition Analysis

In 2025, the Solid-state Detectors segment held a dominant market position, capturing a 40.5% share of the Global Radiation Detection, Monitoring, and Safety Market. This dominance is due to the efficiency and compact design of solid-state detectors, which support modern radiation monitoring needs. Their ability to deliver quick and precise readings makes them suitable for portable devices and advanced systems. They are increasingly preferred in applications that require accuracy and ease of integration.

Solid state detectors are gaining importance as industries move toward digital and connected safety systems. Their durability and low maintenance needs support long-term use in challenging environments. These detectors also enable the development of smaller and more efficient monitoring devices, improving accessibility across healthcare, research, and industrial operations.

For instance, in April 2026, at a technical conference on sensing for hazardous threats, engineers from Teledyne FLIR presented work on optical and spectral techniques for remote detection, building on solid-state sensor platforms with sophisticated signal processing. Continued R&D around compact sensors and advanced algorithms supports broader adoption of solid-state detectors across security and industrial markets.

Protection Type Analysis

In 2025, the Full-Body Protection segment held a dominant market position, capturing a 57.3% share of the Global Radiation Detection, Monitoring, and Safety Market. This dominance is due to the need for complete safety coverage in environments where radiation exposure is possible. Workers handling radiation sources require protection for the entire body to reduce health risks. Full body shielding solutions are commonly used in medical, nuclear, and industrial settings to ensure safety.

Protective equipment, such as aprons, suits, and shields, helps reduce cumulative exposure during routine and high-risk tasks. Organizations prioritize full body protection to meet safety standards and protect staff over long working hours. Strong regulatory focus on worker safety continues to support the use of comprehensive protective solutions.

For instance, in June 2025, the Navy dosimetry program awarded to Thermo Fisher includes integrated monitoring and data systems that help manage exposure across whole crews rather than just individual hotspots. When organisations track doses more accurately at the workforce level, they are more likely to invest in full-body shielding solutions to reduce long-term occupational risk.

End-Use Analysis

In 2025, the Non-Hospitals segment held a dominant market position, capturing a 74.1% share of the Global Radiation Detection, Monitoring, and Safety Market. This dominance is due to the widespread use of radiation monitoring across industrial, nuclear, and security-related environments. Facilities such as power plants, research centers, and border control points require continuous monitoring to manage exposure and detect contamination. These sectors operate under strict safety guidelines that drive consistent demand.

Non-hospital environments rely on radiation detection systems for daily operations and risk management. Monitoring tools are used to protect workers, maintain compliance, and support safe handling of materials. Expanding industrial applications and increased focus on environmental safety continue to strengthen the adoption of radiation monitoring solutions outside healthcare settings.

For instance, in February 2026, Mirion noted record annual orders led by nuclear power and related infrastructure, underlining how non-hospital users such as utilities and fuel cycle facilities remain a core demand base. These projects often involve large fleets of area monitors and dosimetry devices, reinforcing the dominance of non-clinical end users in the market.

Key Market Segments

By Product

- Radiation Detection & Monitoring

- Personal Dosimeters

- Area Process Monitors

- Environmental Radiation Monitors

- Surface Contamination Monitors

- Material Monitors

- Radiation Monitoring Software

By Composition

- Gas-filled Detectors

- Solid-state Detectors

- Scintillators

By Protection Type

- Full-Body Protection

- Face & Hand Protection

- Others

By End-Use

- Non-Hospitals

- Hospitals

Emerging Trends

A clear shift toward solid-state and digital detectors is being observed across healthcare and nuclear facilities. These systems provide higher precision, real-time readouts, and easier integration with IT and control systems. In medical applications, solid-state detectors are reported to grow at high single-digit percentage rates annually.

Wearable and portable devices are becoming more advanced, enabling real-time exposure tracking through connected dosimeters. Remote monitoring is also expanding, with data streamed to centralized dashboards. This approach supports continuous oversight across large facilities and multi-site operations, especially with the increasing adoption of IoT-enabled radiation monitoring systems.

Growth Factors

Worker safety remains the core driver, supported by stricter regulatory frameworks across industrial, medical, and nuclear sectors. Compliance requirements are tightening, which increases the adoption of structured radiation safety programs. In many regions, new standards are observed to raise implementation rates by several percentage points following enforcement.

Healthcare demand is also strengthening due to rising imaging procedures and radiation-based therapies. Hospitals are focusing on balancing clinical outcomes with dose control, driving adoption of accurate detectors and integrated systems. AI-assisted planning tools in radiology and therapy further support efficient dose management and improved patient safety.

Market Dynamics

Drivers - Rising Healthcare Needs

The growing use of medical imaging and radiation-based therapies is increasing demand for reliable radiation monitoring systems. Hospitals are handling higher patient volumes for CT scans, nuclear medicine, and cancer treatment, which requires accurate dose tracking to ensure safety for both patients and healthcare professionals during routine procedures.

Healthcare providers are focusing more on patient safety and reducing unnecessary exposure. This has increased the need for advanced detection tools and monitoring systems that support better dose management. As imaging procedures expand across diagnostic and treatment areas, the importance of effective radiation safety solutions continues to rise steadily.

For instance, in February 2025, Ludlum Measurements expanded outreach to healthcare and research centers with portable survey meters designed for daily use around imaging rooms and isotope labs. The company has been underscoring the need for routine contamination checks and area monitoring as more facilities adopt advanced diagnostic and therapeutic equipment.

Restraint - High Equipment Costs

High equipment costs remain a key restraint for many organizations, especially smaller hospitals, clinics, and industrial users. Advanced radiation detection systems, along with maintenance and calibration needs, require significant investment. This often limits adoption or delays upgrades, particularly in cost-sensitive environments with limited budgets.

In addition to initial purchase costs, users must invest in training, system integration, and ongoing monitoring processes. These added expenses can increase the total cost of ownership over time. For many facilities, balancing compliance requirements with financial constraints remains a challenge when adopting modern radiation safety solutions.

For instance, in June 2025, Thermo Fisher’s contract to supply advanced dosimetry systems to the U.S. Navy highlighted that top-tier integrated monitoring and software platforms are often adopted first by well-funded defense customers. Smaller healthcare or industrial users may find similar systems difficult to justify financially, even if they see the safety benefits.

Opportunities - Tech Improvements

Technological advancements are creating new opportunities for the market, especially with the development of compact, accurate, and connected radiation detection systems. Innovations in sensor design and digital monitoring allow real-time data collection and improved visibility of exposure levels. These improvements support better decision-making in both healthcare and industrial settings.

The integration of cloud platforms and mobile applications is further enhancing system capabilities. Users can monitor radiation levels remotely, receive alerts, and maintain digital records for compliance. These features are encouraging organizations to shift from basic monitoring tools to integrated solutions that offer long-term operational benefits and improved safety outcomes.

For instance, in September 2024, Mirion’s acquisition of Advanced Measurement Technology broadened its capabilities in continuous air monitoring and detection electronics, strengthening its position to deliver more integrated, sensor-rich radiation safety solutions. This move supports smarter monitoring architectures that can feed richer data into facility safety programs across regions.

Challenges - Regulatory Complexity

Radiation safety regulations vary across regions and industries, making compliance a complex process for organizations. Facilities must follow strict guidelines related to exposure limits, monitoring practices, and reporting standards. Managing these requirements often requires dedicated expertise, which can be challenging for smaller organizations with limited resources.

Frequent updates to safety standards also create uncertainty, as organizations must continuously adapt their systems and processes. Ensuring compliance across multiple locations adds further complexity. This challenge increases the need for reliable monitoring solutions, but also slows adoption as users evaluate how to meet evolving regulatory expectations.

For instance, in February 2026, Teledyne FLIR’s identiFINDER devices are used by agencies that must comply with national standards for personal detectors and radionuclide identification. Ensuring instruments meet evolving technical norms and interoperability expectations across different regions remains a persistent challenge, especially when products are deployed internationally for major events.

Key Players Analysis

One of the leading players, in September 2024, Mirion completed a roughly $45 million acquisition of Advanced Measurement Technology, adding continuous air-monitoring and specialty detector capabilities to its portfolio. The deal strengthens Mirion’s installed base in nuclear facilities and research labs and deepens its reach in Asia-Pacific safety and environmental monitoring projects.

Top Key Players in the Market

- Mirion Technologies Inc.

- Thermo Fisher Scientific Inc.

- Teledyne FLIR LLC

- Fuji Electric Co., Ltd.

- Unfors RaySafe AB

- Arktis Radiation Detectors Ltd.

- Kromek Group plc

- Berthold Technologies GmbH & Co. KG

- Alpha-Spectra, Inc.

- Radiation Detection Company

- Centronic Ltd.

- Burlington Medical LLC

- Amray Group Ltd.

- Atomtex SPE

- Polimaster Ltd.

- Smiths Detection Group Ltd.

- Ludlum Measurements, Inc.

- Hitachi-Aloka Medical, Ltd.

- General Atomics Electronic Systems

- Else Nuclear s.r.l.

- Silena Group s.r.l.

- Others

Recent Developments

- In March 2026, Teledyne FLIR continued to build out its radiation-capable sensing portfolio by integrating compact gamma and neutron detection into multi-sensor security platforms. These rugged units combine thermal imaging, visual cameras, and spectroscopic radiation detection, giving defense, border security, and critical-infrastructure customers a single, mobile toolkit for CBRN threat monitoring.

- In February 2026, Berthold expanded its process radiation measurement solutions for steel, mining, and chemical plants, adding higher-sensitivity detectors and enhanced digital interfaces. These systems allow continuous, non-contact density and level measurement in harsh environments, improving process control while maintaining strict safety margins around radioactive sources.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 2,769.4 Million |

| Forecast Revenue (2035) | USD 5,602.5 Million |

| CAGR (2026-2035) | 7.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product (Radiation Detection & Monitoring, Material Monitors, Radiation Monitoring Software), By Composition (Gas-filled Detectors, Solid-state Detectors, Scintillators), By Protection Type (Full-Body Protection, Face & Hand Protection, Others), By End-Use (Non-Hospitals, Hospitals) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Mirion Technologies Inc., Thermo Fisher Scientific Inc., Teledyne FLIR LLC, Fuji Electric Co., Ltd., Unfors RaySafe AB, Arktis Radiation Detectors Ltd., Kromek Group plc, Berthold Technologies GmbH & Co. KG, Alpha-Spectra, Inc., Radiation Detection Company, Centronic Ltd., Burlington Medical LLC, Amray Group Ltd., Atomtex SPE, Polimaster Ltd., Smiths Detection Group Ltd., Ludlum Measurements, Inc., Hitachi-Aloka Medical, Ltd., General Atomics Electronic Systems, Else Nuclear s.r.l., Silena Group s.r.l., Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |