Quick Navigation

Report Overview

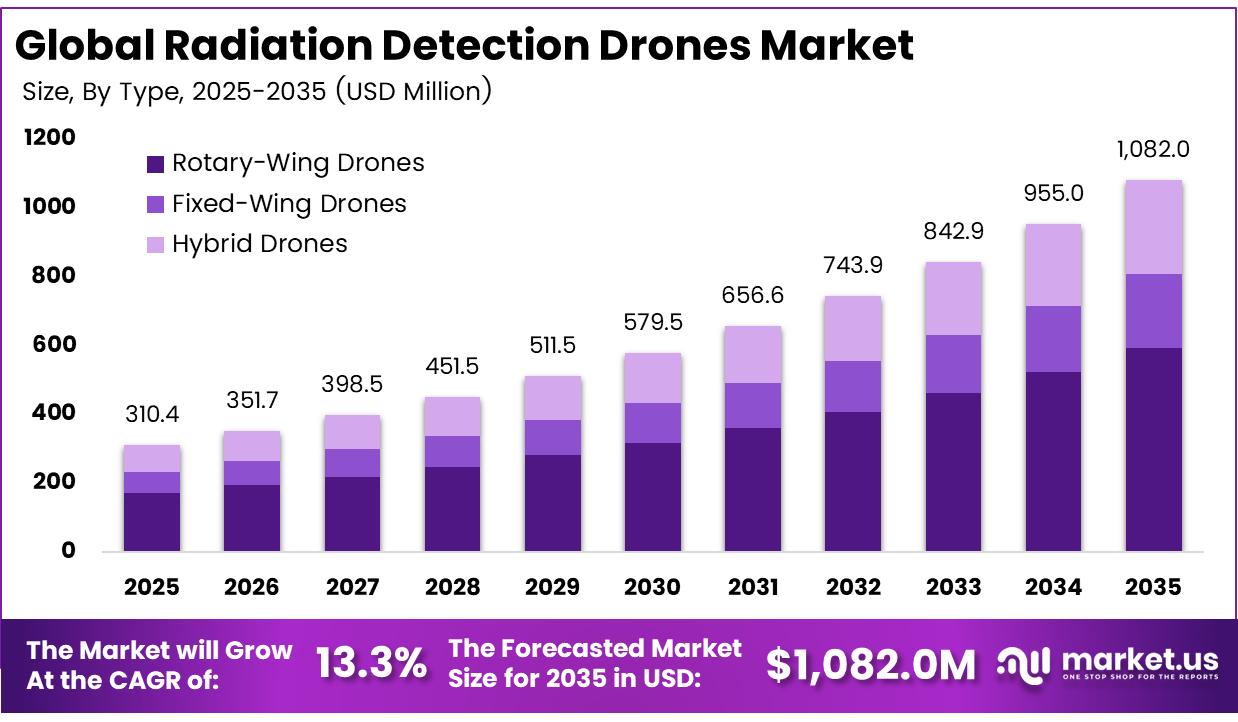

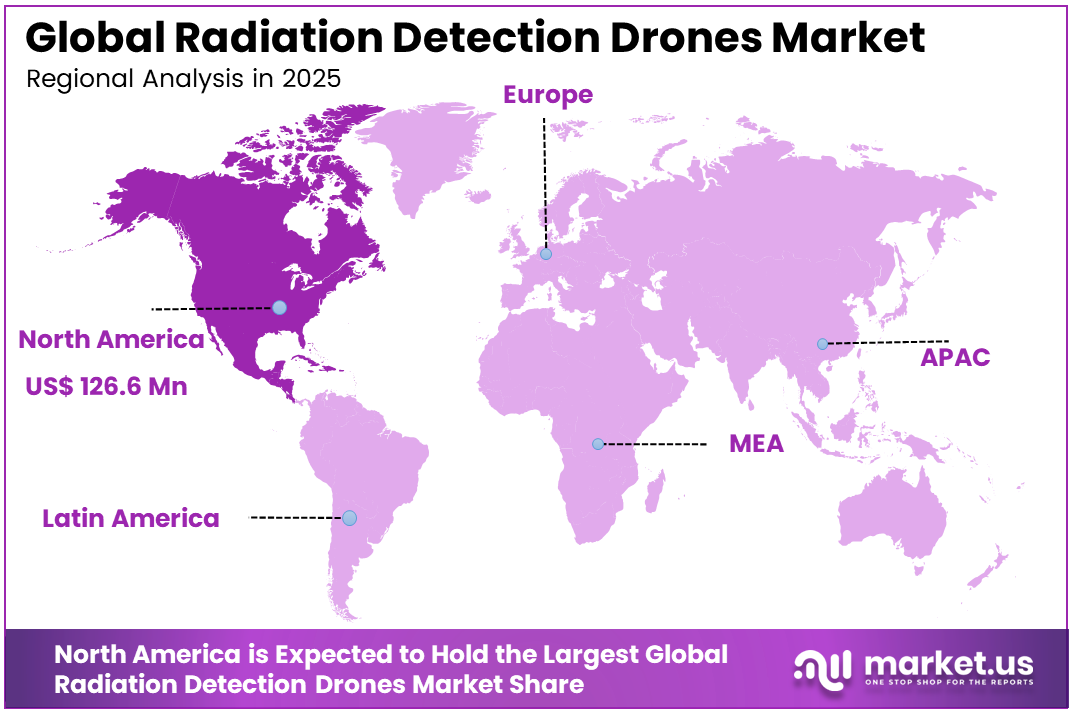

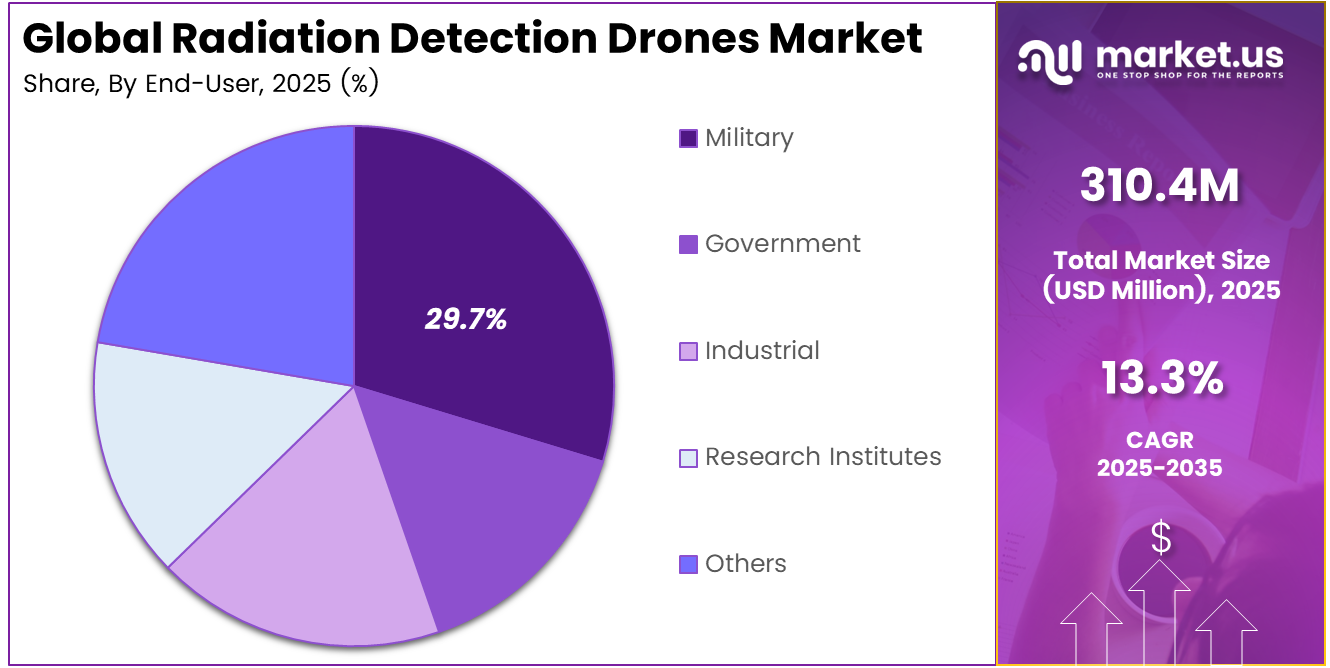

The Global Radiation Detection Drones Market size is expected to be worth around USD 1,082.0 million by 2035, from USD 310.4 million in 2025, growing at a CAGR of 13.3% during the forecast period from 2025 to 2035. North America held a dominant market position, capturing more than a 40.8% share, holding USD 126.6 million in revenue.

Radiation Detection Drones refer to unmanned aerial systems fitted with radiation sensors to identify, measure, and map radioactive materials from the air. These drones are used in nuclear plants, defense areas, emergency response, and environmental monitoring to collect safer, faster, and more accurate radiation data without exposing workers to hazardous sites.

Top driving factors include rising concern about nuclear safety, tighter site monitoring rules, and lessons from past accidents where slow ground surveys delayed action. Defense and security agencies are also supporting adoption, as drones help detect radiological threats around borders, ports, and urban areas with faster coverage and lower human exposure during sensitive inspections.

The market for Radiation Detection Drones is driven by rising nuclear safety needs, stricter site monitoring requirements, and growing demand for safer inspection methods. These drones help operators detect radiation risks without sending workers into hazardous areas. Their use is increasing across nuclear plants, defense sites, emergency response teams, and environmental monitoring agencies that need faster and more accurate survey data.

Demand is increasing as users need systems that reduce worker exposure, shorten survey time by more than 50% compared with manual checks, and maintain high accuracy in complex locations. Nuclear operators, emergency teams, and environmental bodies are now adding drones into regular inspection plans, making them part of routine safety operations.

For instance, in August 2025, Yuneec and Parrot expanded their professional drone ecosystems with open payload interfaces and SDKs that third-party radiation-sensor vendors can leverage. This openness enables faster customization for environmental agencies and research institutes that require affordable, flexible platforms for experimental radiation-mapping and training missions.

Key Takeaway

- In 2025, the Rotary-Wing Drones segment held a dominant market position, capturing a 54.8% share of the Global Radiation Detection Drones Market.

- In 2025, the Scintillation Detector segment held a dominant market position, capturing a 35.6% share of the Global Radiation Detection Drones Market.

- In 2025, the Nuclear Power Plants segment held a dominant market position, capturing a 31.5% share of the Global Radiation Detection Drones Market.

- In 2025, the Military segment held a dominant market position, capturing a 29.7% share of the Global Radiation Detection Drones Market.

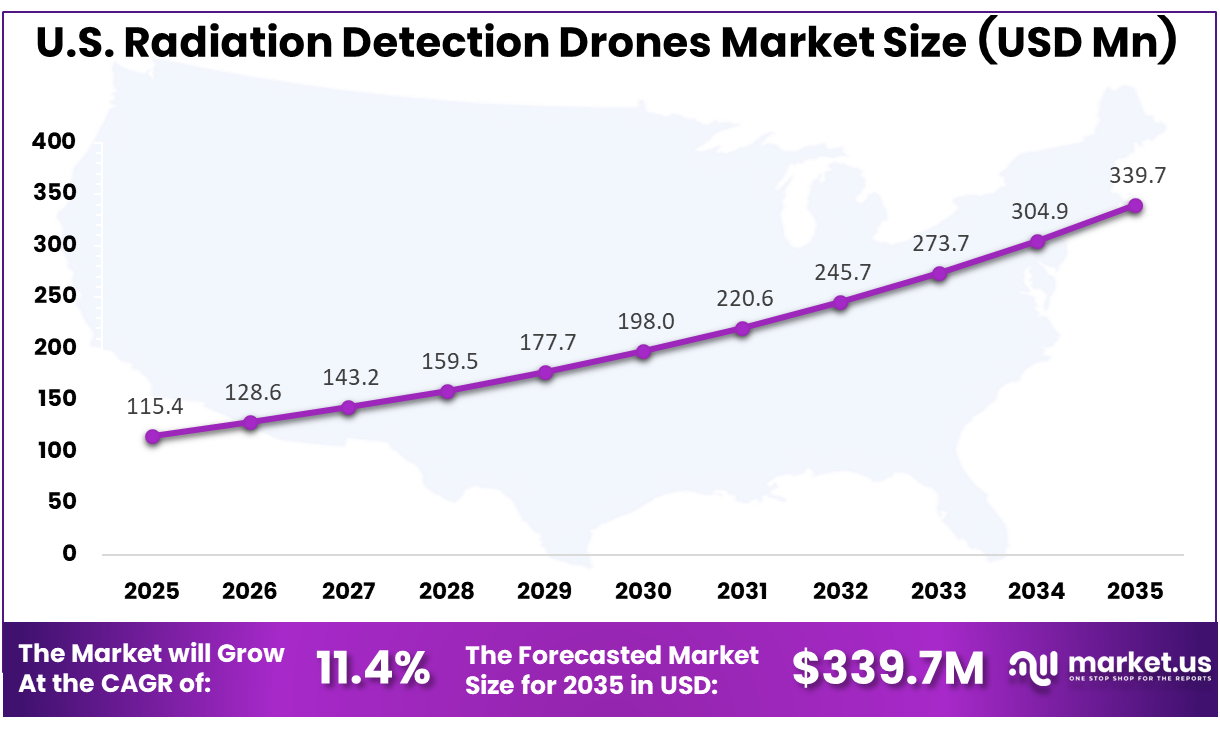

- The U.S. Radiation Detection Drones Market was valued at USD 115.4 Million in 2025, with a robust CAGR of 11.4%.

- In 2025, North America held a dominant market position in the Global Radiation Detection Drones Market, capturing more than a 40.8% share.

Role of Generative AI

Generative AI is increasingly being used to convert radiation data streams and drone flight logs into clear risk summaries for operators. In broader drone workflows, over 60% of new AI features launched by leading cloud providers in 2023 used generative models, showing strong relevance for inspection and safety applications.

In radiological missions, generative models can support mission planning, summarise multi-hour inspection flights, and highlight unusual spectral signatures against site baselines. Across industrial and infrastructure uses, more than 35% of drone software users already use or plan to use generative AI for reporting and data review.

Investment and Business Benefits

Investment opportunities focus on smart payloads, including high-sensitivity detectors that can identify different radiation energy levels and software that uses AI to flag unusual readings automatically. Service providers also have growth potential by offering drone-based radiation surveys to smaller plants, hospitals, and research labs that cannot afford their own fleet.

Business benefits include faster regulatory survey completion, better asset visibility, and stronger compliance proof through detailed digital data logs. Drone-based inspection also supports long-term asset protection by detecting hotspots early and helping predictive maintenance in high-dose areas, where manual inspection can be slow, costly, and risky for workers.

Regional Analysis

In 2025, North America held a dominant market position in the Global Radiation Detection Drones Market, capturing more than a 40.8% share, holding USD 126.6 million in revenue. North America held a dominant position due to strong nuclear safety standards, advanced defense spending, and wider drone use in emergency response and environmental monitoring. The region has a mature nuclear power base, active decommissioning programs, and strict compliance needs that encourage faster radiation mapping. Demand is also supported by homeland security agencies using drones to detect radiological risks across borders, ports, and sensitive infrastructure.

For instance, in April 2026, Teledyne FLIR Defense expanded its Third-Party Payload Integration Program by certifying Emesent’s Hovermap LiDAR payload across its unmanned aerial systems, ground robots, and radiation detection platforms in the U.S. market. Integrated with the MUVE R430 radiation sensor on drones, it gives CBRN teams fast, geo-referenced 3D radiation maps, reinforcing North America’s lead in radiation-detection drone solutions.

U.S. Radiation Detection Drones Market Size

The market for Radiation Detection Drones within the U.S. is growing tremendously and is currently valued at USD 115.4 million; the market has a projected CAGR of 11.4%. The market is growing due to stronger nuclear safety needs, rising investment in emergency response tools, and wider use of drones for defense and homeland security missions. Demand is also supported by aging nuclear infrastructure, decommissioning activities, border monitoring, and environmental inspection requirements. Operators are adopting these drones to reduce worker exposure, speed up radiation surveys, and generate accurate digital records for compliance and risk management.

For instance, in February 2026, Mirion Technologies’ collaboration with Swiss drone firm Flyability continued to gain traction in North America, integrating the Mirion RDS-32 radiation survey meter as a payload on the Elios 3 inspection drone. The solution lets operators capture live and post-processed radiation readings while mapping confined or hazardous spaces, underscoring U.S. leadership in Radiation Detection Drones.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Product Type Analysis

In 2025, the Rotary-Wing Drones segment held a dominant market position, capturing a 54.8% share of the Global Radiation Detection Drones Market. This dominance is due to the strong operating flexibility of rotary-wing drones in radiation monitoring work. These drones can hover, move slowly, and stay stable over a selected area, which helps teams collect more reliable readings across nuclear sites, industrial zones, and emergency locations.

Rotary-wing drones are also preferred because they can work in confined or difficult spaces where ground teams may face safety risks. Their ability to carry detection payloads, cameras, and navigation tools makes them practical for faster site checks and safer radiation survey operations.

For instance, in November 2022, Teledyne FLIR Defense introduced the MUVE R430 radiation detection payload designed for unmanned aerial systems, enabling remote detection and mapping of radioactive sources from the air. The payload integrates with existing drone platforms and supports safer inspection of hazardous areas without exposing personnel to direct radiation.

Sensor Type Analysis

In 2025, the Scintillation Detector segment held a dominant market position, capturing a 35.6% share of the Global Radiation Detection Drones Market. This dominance is due to the strong sensitivity and field reliability of scintillation detectors in radiation detection tasks. These sensors are valued because they can detect gamma radiation effectively and support clearer identification of radioactive sources during aerial surveys.

Scintillation detectors are widely used with drones because they offer a good balance of performance, size, and practical deployment. Their use supports nuclear monitoring, source search, emergency response, and environmental inspection, where accurate readings are important for safe decision-making.

For instance, in January 2024, Kromek Group plc showcased its isotope-identifying drone solutions using compact detectors capable of distinguishing different gamma sources, demonstrating how advanced scintillation technology is being adapted for airborne missions in civil nuclear, environmental, and security applications.

Application Analysis

In 2025, the Nuclear Power Plants segment held a dominant market position, capturing a 31.5% share of the Global Radiation Detection Drones Market. Nuclear power plants use radiation detection drones to improve inspection safety and reduce the need for workers to enter high-risk areas. These drones help monitor plant surroundings, check restricted zones, and support faster decision-making during routine surveys or unusual site conditions.

Their adoption is also supported by the need for reliable compliance records and regular site monitoring. Drone-based surveys provide structured digital data, which helps plant teams track radiation patterns, identify hotspots early, and maintain safer operating conditions.

For instance, in March 2025, in a detailed article on drone-based radiation detection, Flyability described how nuclear plants deploy indoor drones to support regular inspections and incident response. The company showed how mapping tools and real-time readings from the drone help radiation protection teams plan work more effectively and limit exposure time.

End-User Analysis

In 2025, the Military segment held a dominant market position, capturing a 29.7% share of the Global Radiation Detection Drones Market. This dominance is due to the rising use of drones by military agencies for threat detection, border surveillance, and hazardous area assessment. Radiation detection drones allow defense teams to examine risky locations remotely before personnel are sent into the field.

Military users value these systems because they support faster decisions during security, disaster response, and contamination-related operations. Their use is important in ports, border areas, conflict zones, and urban security settings where quick radiological awareness can improve safety and response planning.

For instance, in June 2025, the RaDron project’s miniature radiation-detecting drone was tested in multiple civil-defence exercises with national nuclear and CBRN institutes. While focused on civil use, the scenarios mirror many military needs in contaminated areas, showing how compact radiation drones can support operations without exposing personnel.

Key Market Segments

By Product Type

- Fixed-Wing Drones

- Rotary-Wing Drones

- Hybrid Drones

By Sensor Type

- Geiger Counter

- Scintillation Detector

- Semiconductor Detector

- Dosimeter

- Others

By Application

- Environmental Monitoring

- Nuclear Power Plants

- Defense and Homeland Security

- Emergency Response

- Others

By End-User

- Military

- Government

- Industrial

- Research Institutes

- Others

Emerging Trends

A major trend is the movement from basic Geiger counters to scintillation and semiconductor detectors, which can identify isotopes and measure radiation levels more precisely. European nuclear research trials showed that multi-detector drones can map dose variations with spatial resolution down to a few metres.

Another trend is the rise of autonomous drone operations in cluttered or partly GPS-denied sites, including reactor buildings and decommissioning areas. Research programmes show that autonomous path planning and obstacle avoidance can improve effective coverage by over 30% for the same battery budget, helping operators scan complex structures efficiently.

Growth Factors

Safety and workforce protection remain the strongest growth factors for drone-based radiation monitoring. After major industrial or nuclear incidents, international reviews show that more than 70% of early-phase radiological survey tasks expose field teams to avoidable risk, which supports wider use of unmanned aerial surveys.

Regulatory pressure is also supporting adoption across decommissioning, waste management, and environmental monitoring activities. In nuclear and heavy industry clusters, regulators in several regions have reported annual increases above 10% in required monitoring campaigns or survey frequency, making repeatable drone-based radiation mapping more attractive for operators.

Market Dynamics

Drivers - Rising Focus on Nuclear and Radiological Safety

Rising focus on nuclear and radiological safety is increasing the use of radiation detection drones across nuclear plants, defense sites, research facilities, and emergency zones. These drones help teams inspect risky areas from a safer distance while collecting radiation data more quickly than traditional ground-based checks.

Their adoption is also supported by the need for faster response during leaks, accidents, or suspected radiological threats. Operators are using drone-based surveys to reduce worker exposure, improve site awareness, and create reliable inspection records for safety planning and compliance activities.

For instance, in April 2026, Flyability released a new firmware update for the Elios 3 that optimizes missions with its radiation payload, helping nuclear operators capture more stable data in confined, high-dose environments. The update reflects how plant owners increasingly rely on indoor radiation survey drones to keep staff out of hazardous areas.

Restraint - High Capital Investment

High capital investment remains a major restraint for the Radiation Detection Drones Market. Specialized drones require radiation sensors, stable navigation systems, secure communication tools, software, training, and maintenance support, which increases the total cost for buyers with limited budgets.

Smaller facilities, hospitals, laboratories, and regional emergency teams may find it difficult to purchase and operate their own systems. This cost barrier can slow adoption, especially where radiation surveys are occasional, and decision makers need strong proof of long-term operational value.

For instance, in May 2023, the new Mirion-Flyability payload offers sophisticated indoor radiation surveying but involves purchasing specialized meters, drone platforms, and analysis software. For smaller plants or research labs, this combined hardware and integration cost can be a hurdle, slowing broader deployment despite strong safety arguments.

Opportunities - Integration of AI for Autonomous Radiation Mapping

Integration of artificial intelligence creates a strong opportunity for autonomous radiation mapping. AI can help drones plan safe routes, process radiation readings, detect unusual patterns, and convert complex data into clearer maps for operators who need fast decisions during inspections or emergency response.

AI-enabled systems can also support repeated surveys by comparing current radiation levels with past site records. This improves hotspot detection, reduces manual review work, and helps nuclear operators, defense agencies, and environmental teams move toward more predictive and data-driven monitoring practices.

For instance, in April 2026, Teledyne FLIR Defense expanded its third-party payload integration program, certifying Emesent’s Hovermap LiDAR across unmanned platforms and radiation detection systems. By combining MUVE R430 radiation payloads with autonomous 3D mapping, CBRN teams can build detailed radiation maps in GPS-denied spaces with less manual piloting effort.

Challenges - Regulatory Barriers

Regulatory barriers remain a key challenge because drone operations near nuclear plants, defense zones, airports, and critical infrastructure require strict approvals. Operators must follow airspace rules, safety procedures, data security controls, and site access requirements before radiation detection drones can be deployed.

Acceptance also depends on whether regulators trust the accuracy and repeatability of drone-collected radiation data. Any concern around sensor calibration, flight stability, or data validation can delay approval, making clear standards and certified operating procedures important for wider market adoption.

For instance, in April 2026, DJI highlighted that new US Federal Communications Commission restrictions could block approval of several upcoming drone models, with significant expected revenue loss in that market. For public safety or inspection users considering DJI platforms for radiation payloads, this uncertainty around authorizations complicates long-term fleet planning and regulatory compliance strategies.

Key Players Analysis

One of the leading players in July 2024, Radiation Solutions expanded deployment of its aerial radiation-mapping systems, adapting proven ground and vehicle-based spectrometers for drone use. The company’s payloads deliver precise radionuclide identification from low-altitude flights, supporting mine remediation, nuclear-site surveys, and homeland-security sweeps over large or inaccessible areas.

Top Key Players in the Market

- Flyability SA

- DJI Innovations

- Aerialtronics

- FLIR Systems (Teledyne FLIR)

- Kromek Group plc

- Polaris Alpha (Parsons Corporation)

- H3 Dynamics

- Mirion Technologies

- DroneShield Limited

- AeroVironment, Inc.

- Northrop Grumman Corporation

- Lockheed Martin Corporation

- Radiation Solutions Inc.

- General Atomics Aeronautical Systems, Inc.

- Yuneec International

- Parrot Drones SAS

- Others

Recent Developments

- In July 2024, DroneShield, known for counter-UAS systems, broadened its defense offering by supporting integrations where radiation-aware drones work alongside detection and mitigation platforms. This combined approach lets security forces achieve layered protection, detecting both hostile drones and possible radiological threats in high-risk venues and border areas.

- In August 2025, Flyability’s collision-tolerant indoor drones gained wider use for inspecting confined nuclear and industrial spaces with radiation sensors. Their caged designs let operators fly into tight pipe runs, reactor buildings, and storage halls to gather dose data, drastically cutting personnel exposure and downtime during routine inspections or incident assessments.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 310.4 Million |

| Forecast Revenue (2035) | USD 1,082.0 Million |

| CAGR (2026-2035) | 13.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Fixed-Wing Drones, Rotary-Wing Drones, Hybrid Drones), By Sensor Type (Geiger Counter, Scintillation Detector, Semiconductor Detector, Dosimeter, Others), By Application (Environmental Monitoring, Nuclear Power Plants, Defense and Homeland Security, Emergency Response, Others), By End-User (Government, Military, Industrial, Research Institutes, Others) |

| Regional Analysis | North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape | Flyability SA, DJI Innovations, Aerialtronics, FLIR Systems (Teledyne FLIR), Kromek Group plc, Polaris Alpha (Parsons Corporation), H3 Dynamics, Mirion Technologies, DroneShield Limited, AeroVironment, Inc., Northrop Grumman Corporation, Lockheed Martin Corporation, Radiation Solutions Inc., General Atomics Aeronautical Systems, Inc., Yuneec International, Parrot Drones SAS, Others |

| Customization Scope | Customization at the segment and region/country levels will be provided. Moreover, customization can be tailored to the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |