Quantum Key Distribution (QKD) Market By Component (Solutions (Discrete Variable QKD, Continuous Variable QKD), Services (Professional Services (Consulting & Training, Integration & Deployment), Managed Services)), By Type (Multiplexed QKD Systems, Long-Distance QKD Systems), By Transmission Medium (Fiber-Optic Cable Transmission, Satellite-based Transmission), By Organization Size (SMEs, Large Enterprises), By Application (Network Security, Data Encryption, Others), By Vertical (BFSI, Government & Defense, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2035

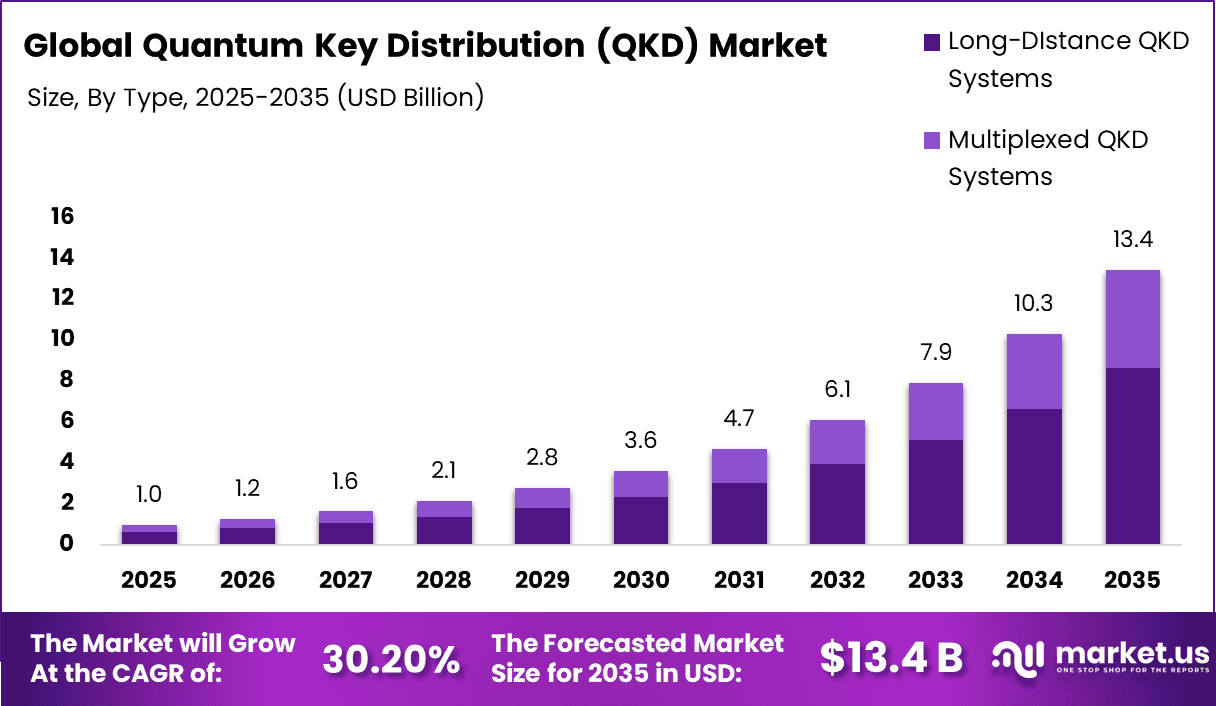

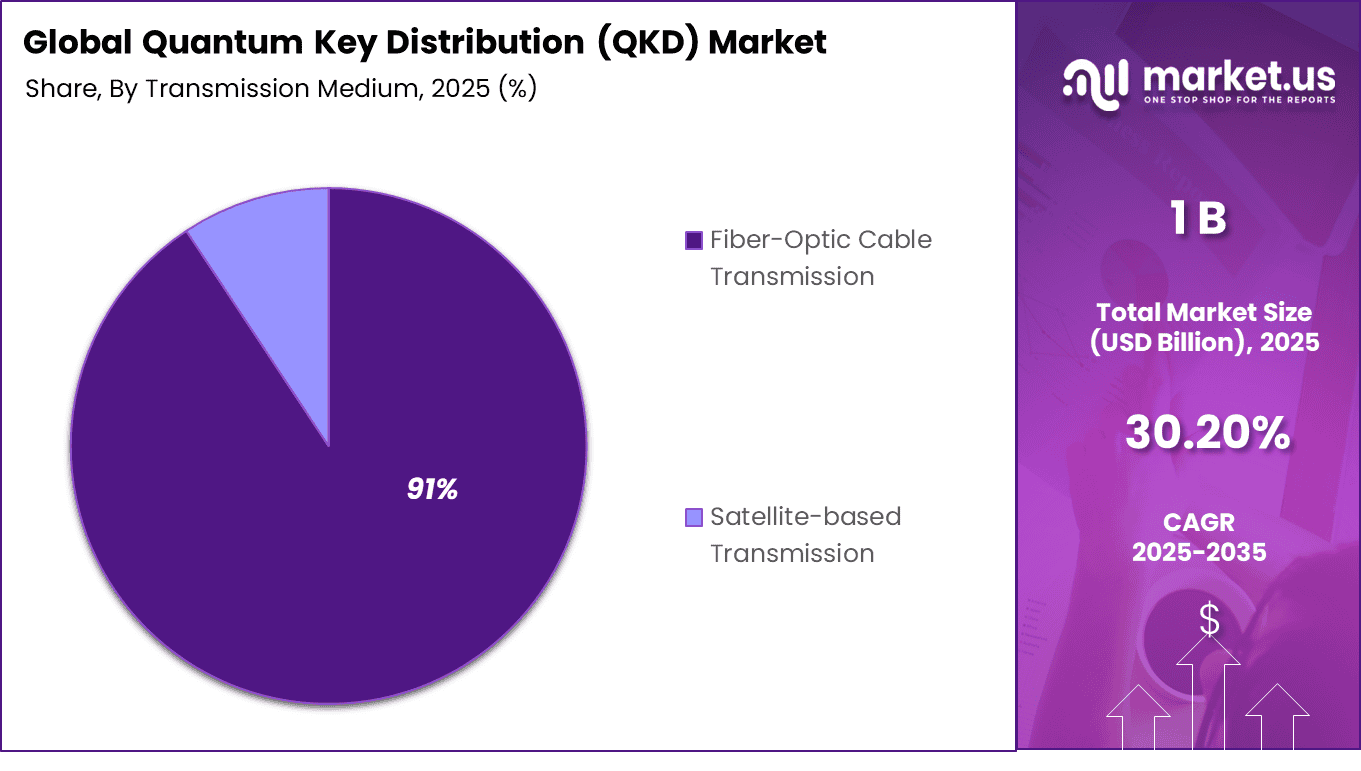

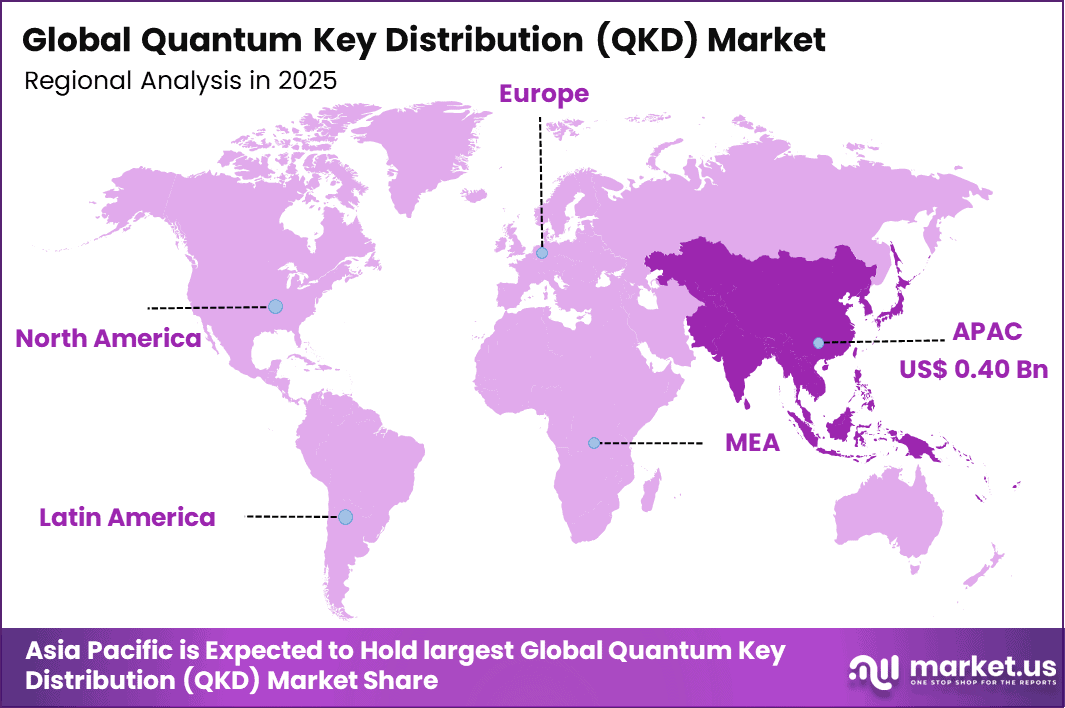

The Global Quantum Key Distribution (QKD) Market generated USD 1 billion in 2025 and is predicted to register growth from USD 1.2 billion in 2026 to about USD 13.4 billion by 2035, recording a CAGR of 30.20% throughout the forecast span. In 2025, Asia Pacific held a dominant market position, capturing more than a 41.8% share, holding USD 0.40 Billion revenue.

Top Market Takeaways

Component Solutions account for 85.2% of the QKD market, as most customers prefer complete, ready-to-use quantum security systems rather than separate hardware or software pieces.

Type Long-distance QKD systems hold 64.5% of the market, reflecting the need to secure data over wide-area networks such as intercity and cross-border links.

Transmission Medium Fiber-optic cable transmission represents 90.7% of the market, since existing fiber networks are a practical and stable medium for carrying quantum keys securely.

Organization Size Large enterprises account for 80.4% of demand, because they manage highly sensitive data and have the budgets to invest in advanced quantum encryption solutions.

Application Government and defense secure communication applications make up 45.6% of the market, as QKD is used to protect critical national security, military, and intelligence information.

Vertical The government and defense vertical overall accounts for 53.5%, showing that public sector and defense organizations are currently the main adopters of QKD technology.

Region Asia-Pacific represents 41.8% of the global market, driven by strong government-backed quantum communication initiatives and secure network deployments.

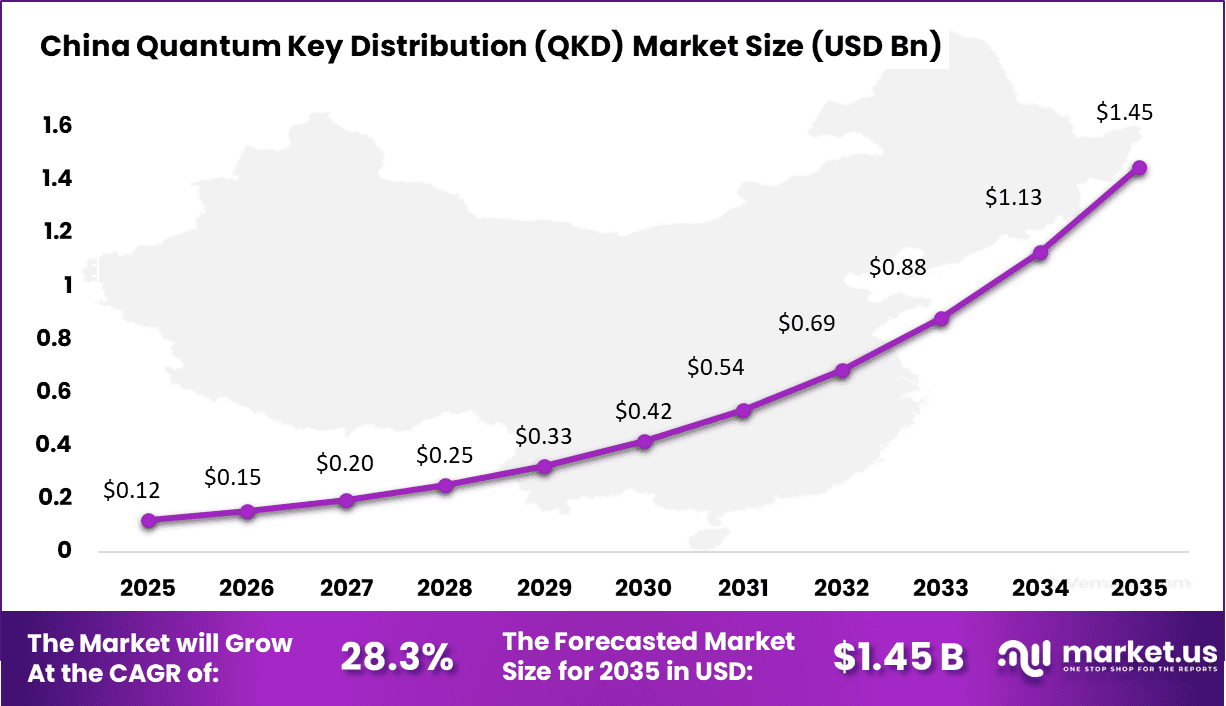

Country China’s QKD market is valued at 0.12 billion and is expected to grow at a CAGR of 28.3%, supported by large-scale quantum communication projects and rapid rollout of quantum-secure infrastructure.

Quantum key distribution is an advanced cybersecurity technology used to exchange encryption keys through quantum physics principles. It enables two parties to create and share secure keys while making any interception attempt detectable. This approach is gaining importance as organizations look beyond traditional encryption methods to protect highly sensitive communications.

QKD is being explored in government networks, defense systems, financial services, telecom infrastructure, and critical industries where long term data confidentiality is essential. As cyber threats become more sophisticated, quantum based security is emerging as a strategic area of investment.

One of the main driving factors is the growing concern that future quantum computing capabilities may weaken conventional encryption systems. Organizations handling sensitive information are preparing early by evaluating next generation security methods that can remain strong over time.

In addition, rising cyberattacks on critical infrastructure and national security systems are increasing demand for highly secure key exchange technologies. Government support for quantum research and secure communications programs is also accelerating development. The expansion of fiber networks and trusted communication infrastructure is further helping QKD deployment in practical environments.

Demand for quantum key distribution solutions is increasing as institutions seek stronger protection for mission critical data. There is a strong preference for systems that can integrate with existing encryption platforms, operate reliably over practical distances, and provide clear security assurance.

Buyers are also looking for scalable solutions that can support networked environments rather than only point to point links. The demand is particularly strong among defense agencies, telecom operators, research institutions, financial organizations, and operators of critical infrastructure. As long term data security becomes a higher priority, the need for trusted quantum communication solutions is expected to grow steadily.

Drivers Impact Analysis

Key Driver

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Additional Insight

Rising cybersecurity threats and data breach concerns

+5.8%

Asia Pacific, North America, Europe

Short to medium term

Security demand supports QKD adoption

Growing government and defense investment in secure communication

+5.3%

Asia Pacific, Europe, North America

Medium term

Public sector funding accelerates deployment

Increasing risk from quantum computing to classical encryption

+4.9%

Global

Medium to long term

Quantum-safe security gains urgency

Expansion of critical infrastructure protection needs

+4.4%

Global

Medium to long term

Critical sectors require stronger encryption

Advancements in fiber-based and satellite-based QKD networks

+4.0%

Asia Pacific, Europe

Medium to long term

Network progress improves commercialization

Restraints Impact Analysis

Key Restraint

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Additional Insight

High deployment and infrastructure costs

-4.1%

Emerging markets

Short to medium term

High costs limit broader rollout

Limited transmission distance and performance constraints

-3.6%

Global

Medium term

Distance limits large-scale deployment

Lack of standardization across QKD systems

-3.0%

Global

Medium to long term

Standards gaps slow interoperability

Complex integration with existing telecom infrastructure

-2.6%

Global

Medium term

Legacy networks complicate adoption

Shortage of skilled quantum technology professionals

-2.2%

Global

Long term

Talent gaps affect implementation

By Component Analysis

The solutions segment accounted for 85.2% of the market share, reflecting its dominant role in delivering complete secure communication frameworks for quantum encryption environments. This dominance is supported by the growing demand for integrated systems that combine key generation, management, transmission security, and network monitoring. Organizations are increasingly adopting end-to-end solutions to strengthen protection against advanced cyber threats.

Another factor driving this segment is the need for faster deployment and simplified management of highly specialized security infrastructure. Solution providers offer ready-to-use platforms that reduce implementation complexity and improve interoperability with existing communication networks. These advantages continue to support strong adoption across sensitive sectors.

By Type Analysis

The long-distance QKD systems segment held 64.5% share, driven by the increasing need to secure communications across cities, regions, and national networks. Long-distance systems are essential for organizations that require protected data exchange between geographically separated facilities. Their ability to maintain encryption integrity over extended routes has strengthened market demand.

In addition, rising investments in national digital infrastructure and secure backbone networks have encouraged adoption of long-distance QKD systems. Governments and enterprises are prioritizing secure wide-area communication channels, which continues to support growth in this segment.

By Transmission Medium Analysis

The fiber-optic cable transmission segment captured 91% of the market, reflecting its strong position as the preferred medium for quantum key distribution. Fiber networks provide stable and controlled transmission environments, making them highly suitable for secure key exchange. Existing telecom fiber infrastructure also supports easier deployment compared with alternative transmission methods.

Furthermore, many institutions already operate extensive fiber networks, allowing faster integration of QKD systems without major structural changes. Fiber transmission also offers dependable performance and lower environmental interference, reinforcing its leading share in the market.

By Organization Size Analysis

The large enterprises segment accounted for 80.4% of the market share, driven by their greater need to protect high-value data, intellectual property, and critical communications. These organizations often manage complex networks and face higher cybersecurity risks, making advanced encryption solutions a strategic priority. QKD platforms help strengthen long-term data security.

Moreover, large enterprises have stronger financial and technical capacity to invest in emerging security technologies. Their focus on regulatory compliance, risk reduction, and secure digital operations has significantly increased adoption of QKD solutions within this segment.

By Application Analysis

The government and defense secure communication segment held 45.6% share, driven by the need to protect classified information, military communications, and national security networks. These users require highly secure systems that can resist sophisticated interception attempts. QKD technology is increasingly viewed as a reliable option for future-proof communication security.

In addition, geopolitical risks and cyber warfare concerns have encouraged stronger investment in advanced encryption systems. Governments are prioritizing secure communication channels for command, intelligence, and diplomatic use, which continues to strengthen this application segment.

By Vertical Analysis

The government and defense segment captured 53.5% of the market, reflecting its leading adoption of quantum-secure technologies. Public sector and defense organizations are among the earliest investors in next-generation encryption systems due to the critical nature of their data and communications. They are actively deploying secure infrastructure to strengthen resilience.

Furthermore, national programs focused on cybersecurity modernization and strategic technology leadership have accelerated adoption in this vertical. The need for trusted communication networks and long-term data protection continues to make government and defense the dominant end-use sector in the QKD market.

Investor Type Impact Analysis

Investor Type

Growth Sensitivity

Risk Exposure

Geographic Focus

Investment Outlook

Venture capital firms

Very high

High

Asia Pacific, US, Europe

Investing in quantum security startups

Private equity firms

High

Moderate

North America and Europe

Scaling quantum communication providers

Corporate investors

Very high

Moderate

Global

Strategic investments in quantum-safe infrastructure

Institutional investors

Moderate to high

Moderate

Developed markets

Focus on long-term deep-tech growth

Government and public funding bodies

Very high

Low

Global

Supporting national quantum security programs

Technology Enablement Analysis

Technology

Impact on CAGR Forecast (~%)

Geographic Relevance

Impact Timeline

Additional Insight

Satellite-based QKD systems

+5.6%

Asia Pacific, Europe

Medium to long term

Expands long-distance secure communication

Advanced single-photon detectors

+5.1%

Global

Medium term

Improves QKD performance

Integration with fiber-optic communication networks

+4.7%

Global

Medium to long term

Supports commercial deployment

Quantum random number generation

+4.2%

Global

Medium term

Strengthens encryption security

Trusted node and repeater network architectures

+3.8%

Global

Long term

Extends network scalability

Key Challenges

High cost of QKD equipment and network deployment.

Limited transmission distance without signal loss.

Complex integration with existing communication networks.

Need for highly specialized technical expertise.

Slow adoption due to limited market awareness.

Lack of common standards across vendors and regions.

High maintenance cost for advanced optical systems.

Performance issues caused by environmental interference.

Regulatory and security policy uncertainty in some markets.

Limited scalability for large commercial networks.

Emerging Trends

The quantum key distribution market is evolving toward more practical and scalable secure communication systems designed for the next era of cybersecurity. One of the key emerging trends is the integration of QKD with existing fiber and telecom networks, allowing quantum safe encryption keys to be delivered without replacing core communication infrastructure.

Another important trend is the growing development of satellite based QKD systems that can extend secure key exchange over long distances where terrestrial links are limited. There is also increasing focus on compact and lower cost hardware that can support broader commercial deployment beyond specialized environments. In addition, hybrid security models are gaining traction, where QKD is combined with post quantum cryptography to create layered protection strategies. Network orchestration tools are also improving, helping manage key distribution, monitoring, and system performance across multiple nodes more efficiently.

Growth Factors

The growth of this market is driven by rising concern over future cyber threats and the potential impact of quantum computing on current encryption methods. Governments, defense agencies, financial institutions, and critical infrastructure operators are seeking stronger methods to protect sensitive communications, which is supporting adoption of QKD solutions. The increasing volume of confidential data moving across digital networks is also creating demand for long term security frameworks.

Another major factor is the modernization of national communication infrastructure, where secure backbone networks are becoming a strategic priority. Research funding and public private collaboration are further accelerating technological progress and pilot deployments. Additionally, stricter data privacy expectations and the need for trusted communication channels are encouraging organizations to invest early in quantum safe security technologies, supporting sustained market growth.

Key Market Segments

By Component

Solutions

Discrete Variable QKD

Continuous Variable QKD

Services

Professional Services

Consulting & Training

Integration & Deployment

Support & Maintenance

Managed Services

By Type

Multiplexed QKD Systems

Long-Distance QKD Systems

By Transmission Medium

Fiber-Optic Cable Transmission

Satellite-based Transmission

By Organization Size

SMEs

Large Enterprises

By Application

Network Security

Data Encryption

Secure Communication

Others

By Vertical

BFSI

Government & Defense

Healthcare

IT & ITes

Automotive

Energy & Utilities

Others

Regional Analysis

Asia Pacific accounted for 41.8% of the Quantum Key Distribution (QKD) market, supported by rising investments in advanced cybersecurity infrastructure and strong focus on next-generation communication security. The region is actively developing quantum technologies to protect sensitive data across government networks, financial systems, and critical infrastructure.

Growing concerns over future cyber threats and the limitations of conventional encryption methods are encouraging adoption of QKD solutions for highly secure data exchange. In addition, increasing research activity, telecom modernization, and public sector support are strengthening market growth across the region.

China market reached USD 0.12 Billion and is projected to grow at a CAGR of 28.3%, driven by significant progress in quantum communication programs and national emphasis on digital security. The country is investing in secure communication networks that can support government, defense, and enterprise data protection needs.

Expansion of fiber infrastructure and growing integration of advanced technologies are also supporting QKD deployment. In addition, rising awareness of long-term data security risks and continued innovation in quantum networking are expected to sustain strong growth in China over the coming years.

Key Regions and Countries

North America

US

Canada

Europe

Germany

France

The UK

Spain

Italy

Russia

Netherlands

Rest of Europe

Asia Pacific

China

Japan

South Korea

India

Australia

Singapore

Thailand

Vietnam

Rest of APAC

Latin America

Brazil

Mexico

Rest of Latin America

Middle East & Africa

South Africa

Saudi Arabia

UAE

Rest of MEA

Competitive Analysis

The competitive landscape of the Quantum Key Distribution (QKD) Market is driven by specialized quantum security companies and large technology providers investing in next-generation encryption solutions. Companies such as ID Quantique SA, Toshiba Digital Solutions Corporation, QuantumCTek Co., Ltd., SK Telecom Co., Ltd., NEC Corporation, and QuintessenceLabs Pty Ltd. hold strong positions by offering commercial QKD systems for secure communication networks.

These players focus on fiber-based and network-integrated solutions for government, telecom, defense, and financial sectors. Their strong research capabilities and early market presence help them maintain a leading position in the industry.

At the same time, emerging companies such as Quantum Xchange Inc., Qasky (Anhui Qasky Quantum Technology Co., Ltd.), MagiQ Technologies Inc., KETS Quantum Security Ltd., Qnu Labs, LuxQuanta Technologies S.L, ThinkQuantum S.r.l, KEEQuant GmbH, SpeQtral Pte Ltd, QEYnet Inc, Kloch, HEQA Security, and Quantum Telecommunication Italy compete by developing compact, scalable, and cost-effective QKD solutions.

Companies like IonQ also contribute through broader quantum technology expertise. Competition in this market is driven by innovation in transmission distance, integration with existing telecom networks, system affordability, and the growing need for protection against future cyber threats.

The future outlook for the Quantum Key Distribution (QKD) Market looks very strong as demand for ultra-secure communication continues to rise. The market is expected to grow with increasing concerns over cyber threats and the future risk posed by quantum computing to traditional encryption methods. Governments, defense agencies, and financial institutions are anticipated to invest more in QKD solutions to protect sensitive data. In the coming years, advancements in fiber networks, satellite-based quantum communication, and lower deployment costs are expected to improve adoption, making QKD an important part of next-generation cybersecurity infrastructure.

Recent Developments

March, 2026 – Toshiba is highlighted as having one of the most mature QKD programs, with operational metro QKD networks in London and Tokyo and long‑distance trials over existing fibre. Toshiba’s field deployments become key case‑studies for integrating QKD into live carrier infrastructure and for combining QKD keys with conventional VPN and optical encryption gear.

April, 2026 – SK Telecom appears among major QKD ecosystem players via Korea’s quantum‑safe network initiatives, where it integrates QKD with 5G infrastructure and explores QKD–PQC hybrid key exchange for mobile core security. Korean optical and quantum‑security stocks rally mid‑April on expectations that local telcos like SKT will accelerate quantum‑secure backbones for AI and cloud traffic.

Report Scope

Report Features

Description

Market Value (2025)

USD 1 Billion

Forecast Revenue (2035)

USD 13.4 Billion

CAGR(2025-2035)

30.20%

Base Year for Estimation

2024

Historic Period

2020-2024

Forecast Period

2025-2035

Report Coverage

Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends

Segments Covered

By Component (Solutions (Discrete Variable QKD, Continuous Variable QKD), Services (Professional Services (Consulting & Training, Integration & Deployment), Managed Services)), By Type (Multiplexed QKD Systems, Long-Distance QKD Systems), By Transmission Medium (Fiber-Optic Cable Transmission, Satellite-based Transmission), By Organization Size (SMEs, Large Enterprises), By Application (Network Security, Data Encryption, Others), By Vertical (BFSI, Government & Defense, Others)

Regional Analysis

North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA

Market")