Quick Navigation

- Report Overview

- Key Takeaways

- Analysts’ Viewpoint

- US Market Expansion

- North America Economic Growth

- Market Scope

- By Speed Analysis

- By Product Analysis

- By Technology Analysis

- By Mode of Operation Analysis

- By Launch Platform Analysis

- Key Market Segments

- Driver

- Restraint

- Opportunity

- Challenge

- Growth Factors

- Emerging Trends

- Business Benefits

- Key Player Analysis

- Recent Developments

Report Overview

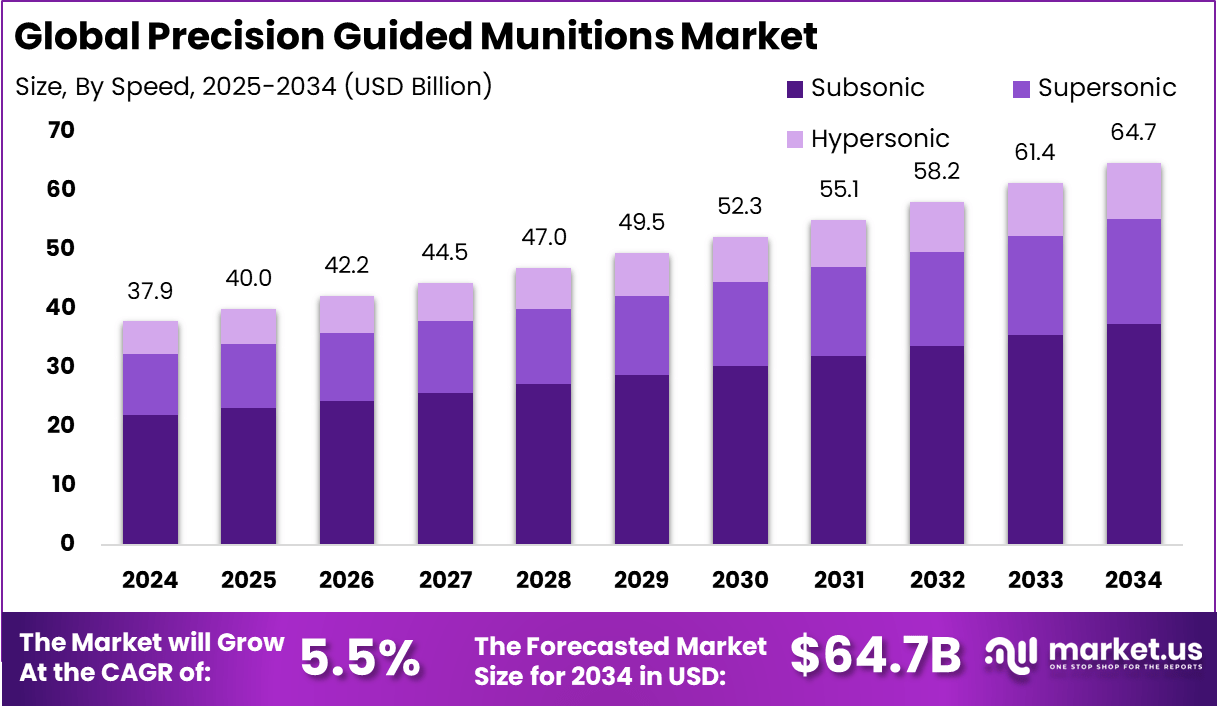

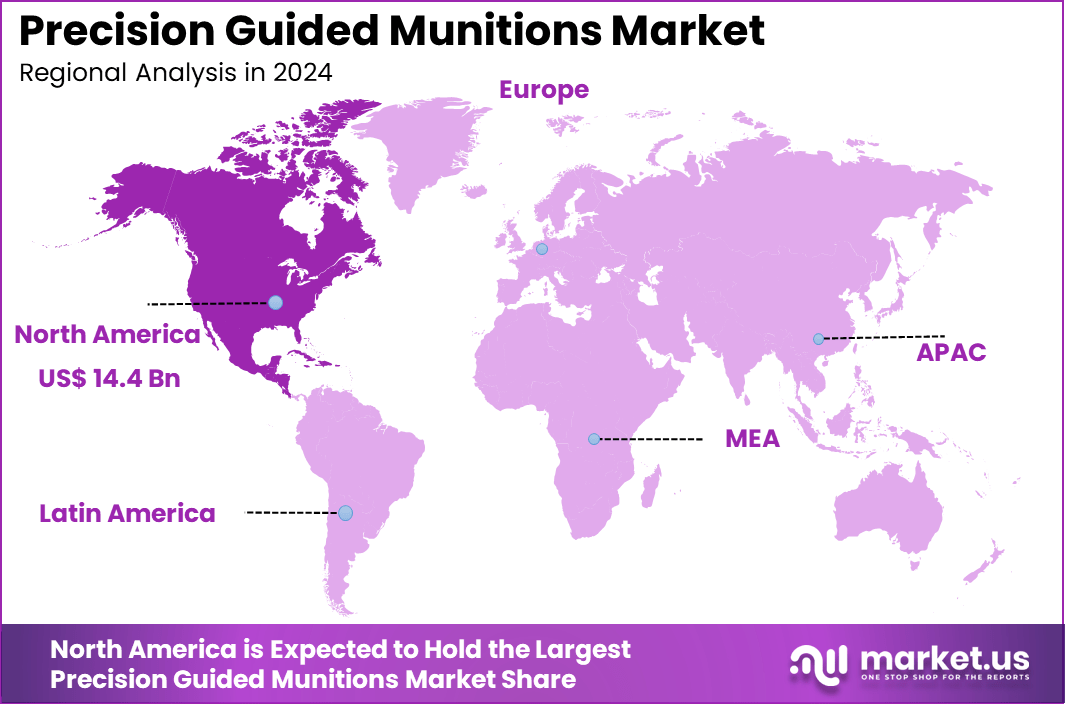

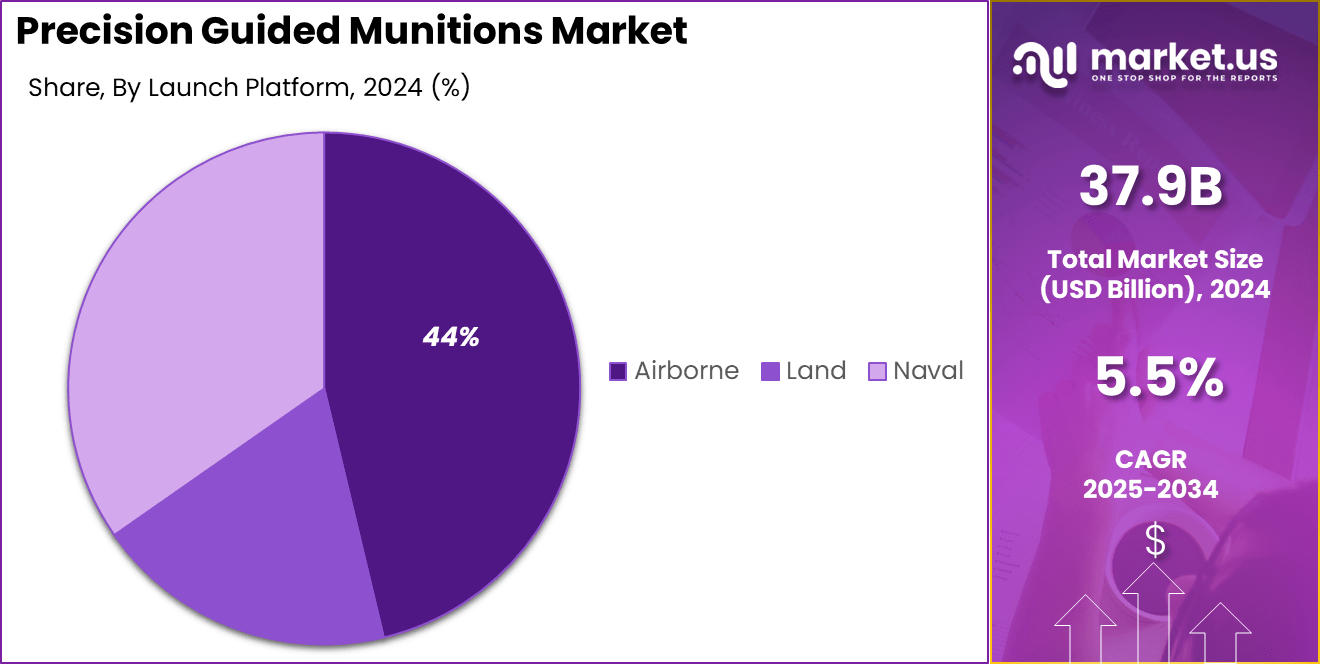

The Global Precision Guided Munitions Market size is expected to be worth around USD 64.7 Billion By 2034, from USD 37.9 billion in 2024, growing at a CAGR of 5.5% during the forecast period from 2025 to 2034. In 2024, North America held a dominant market position, capturing more than a 38% share, holding USD 14.4 Billion revenue.

The demand is being driven by an increasing reliance on advanced strike capabilities that offer greater accuracy, minimal collateral damage, and enhanced mission effectiveness in modern warfare scenarios. As nations continue to invest in upgrading their defense capabilities, particularly amid regional conflicts and border security threats, the adoption of guided munitions is being seen not only as a strategic necessity but also as a cost-effective solution over time.

The growth momentum is further strengthened by the integration of cutting-edge technologies such as satellite navigation, laser guidance, and AI-enabled targeting systems, which are transforming the way defense operations are executed. With growing military modernization programs across the U.S., China, India, and European nations, procurement of precision strike systems is becoming a top priority.

Moreover, the emergence of unmanned aerial vehicles (UAVs) and their compatibility with precision-guided payloads is expected to offer additional impetus to the market. Given the rising geopolitical tensions and the strategic shift towards smarter combat readiness, the market for precision guided munitions is likely to see sustained investment and innovation throughout the next decade.

For instance, General Atomics Electromagnetic Systems (GA-EMS) secured a contract from the U.S. Navy through Advanced Technology International (ATI) to support the advancement of the Long Range Maneuvering Projectile (LRMP) Common Round. This next-generation 155mm artillery round is engineered to reach distances beyond 120 kilometers, enabled by its foldable wing technology and advanced onboard guidance systems.

According to data from the Defense Technical Information Center (DTIC), all four U.S. military branches – the Air Force, Army, Navy, and Marine Corps – actively utilize precision-guided munitions (PGMs). In FY2021, the Department of Defense (DoD) allocated approximately $4.1 billion to procure over 41,337 weapons across 15 munitions programs.

However, a downward trend in volume is evident in subsequent years. The DoD projected $3.3 billion for 20,456 weapons in FY2022, followed by $3.9 billion for 23,306 units in FY2023, $3.9 billion for 18,376 units in FY2024, and $3.6 billion for 16,325 weapons in FY2025.

Technological advancements are central to the proliferation of PGMs. Innovations such as improved guidance systems, integration with unmanned platforms, and enhanced data processing capabilities have augmented the effectiveness of these munitions. The development of PGMs compatible with various launch platforms, including aircraft, naval vessels, and ground-based systems, has expanded their operational utility.

Key Takeaways

- Market Growth: The global PGM market is projected to grow from approximately USD 37.9 billion in 2024 to USD 64.7 billion by 2034, reflecting a compound annual growth rate (CAGR) of 5.5%.

- Regional Insights: North America maintained a leading position in 2024, accounting for over 38% of the global market share, with revenues surpassing USD 14.4 billion.

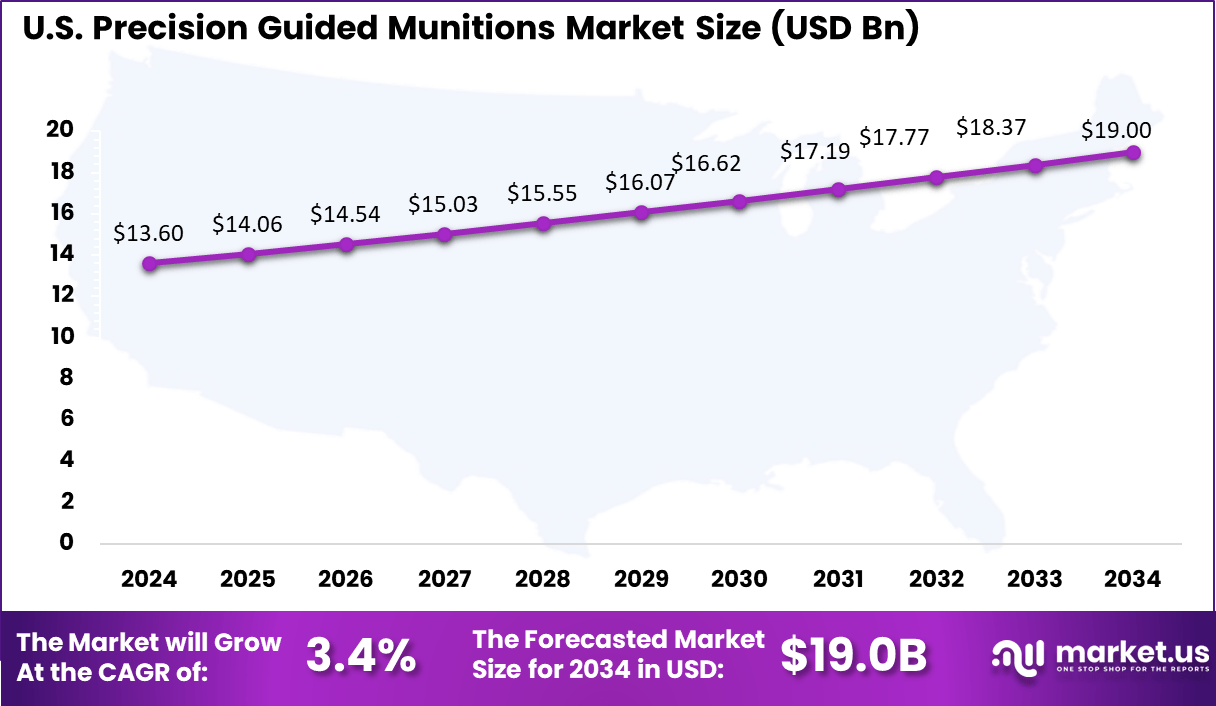

- United States Market: The U.S. PGM market was valued at approximately USD 13.6 billion in 2024 and is projected to reach around USD 19.0 billion by 2034, growing at a CAGR of 3.4%.

- Product Segmentation: The tactical missiles segment held a dominant position in the global PGM market in 2024, accounting for approximately 43.7% of the total market share.

- Technology Trends: The Global Positioning System (GPS) segment led the PGM market in 2024, capturing more than 28% of the total market share.

- Operational Modes: The autonomous segment held a dominant position in the PGM market in 2024, capturing over 54% of the total market share.

- Platform Deployment: The airborne segment led the global PGM market in 2024, accounting for more than 44% of the total market share.

- Speed Classification: The subsonic segment held a dominant position in the global PGM market in 2024, capturing over 58% of the total market share.

Analysts’ Viewpoint

The adoption of PGMs is underpinned by several strategic considerations. Foremost is the imperative to achieve tactical superiority through precision engagement, thereby reducing the duration and cost of military operations. PGMs also contribute to force protection by enabling stand-off engagements, minimizing exposure to hostile environments. Moreover, the interoperability of PGMs with existing military infrastructure facilitates seamless integration into current defense frameworks.

Investment opportunities within the PGM market are robust, particularly in regions prioritizing defense modernization. Countries are allocating substantial budgets toward the acquisition and development of PGMs to bolster their strategic capabilities. Collaborations between defense contractors and governments are fostering innovation and expediting the deployment of advanced munitions.

The regulatory environment governing PGMs is characterized by stringent controls to prevent proliferation and ensure compliance with international laws. Export regulations, arms control agreements, and end-use monitoring are integral components of the governance framework. Manufacturers and exporters must navigate complex legal landscapes to align with national and international mandates, thereby necessitating robust compliance mechanisms.

US Market Expansion

The US Precision Guided Munitions Market is valued at approximately USD 13.6 Billion in 2024 and is predicted to increase from USD 14.06 Billion in 2025 to approximately USD 19.0 Billion by 2034, projected at a CAGR of 3.4% from 2025 to 2034.

North America Economic Growth

In 2024, North America held a dominant position in the global precision guided munitions (PGM) market, capturing over 38% of the total market share, with revenue amounting to approximately USD 14.4 billion. This leadership is primarily attributed to the United States’ substantial defense budget, which facilitates extensive investments in advanced military technologies.

The U.S. Department of Defense’s focus on modernizing its arsenal, including the development and procurement of sophisticated PGMs, has significantly contributed to this market dominance. Additionally, the presence of major defense contractors such as Lockheed Martin, Raytheon Technologies, and Northrop Grumman, who are at the forefront of PGM innovation, further reinforces North America’s leading position in this sector.

Market Scope

| Report Features | Description |

|---|---|

| Market Value (2024) | USD 37.9 Bn |

| Forecast Revenue (2034) | USD 64.7 Bn |

| CAGR (2025-2034) | 5.5% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2023 |

| Forecast Period | 2025-2034 |

By Speed Analysis

In 2024, the subsonic segment held a dominant position in the global precision guided munitions (PGM) market, capturing over 58% of the total market share. This dominance is primarily attributed to the widespread adoption of subsonic PGMs, such as cruise missiles and guided bombs, which are integral to modern military operations.

These munitions are favored for their cost-effectiveness, reliability, and compatibility with existing military platforms, making them a practical choice for various defense strategies. The preference for subsonic PGMs is further reinforced by their proven track record in diverse combat scenarios. Their ability to deliver precise strikes with minimal collateral damage aligns with the evolving doctrines of modern warfare, which emphasize precision and efficiency.

Additionally, the integration of advanced guidance systems, including GPS and inertial navigation, enhances their accuracy and operational effectiveness. As defense forces worldwide continue to prioritize precision and cost-efficiency, the subsonic segment is expected to maintain its leading position in the PGM market.

By Product Analysis

In 2024, the tactical missiles segment held a dominant position in the global precision guided munitions market, accounting for approximately 43.7% of the total market share. This prominence is largely attributed to the versatility and strategic importance of tactical missiles in modern warfare.

Designed for short to medium-range engagements, these missiles are equipped with advanced guidance systems, including GPS, inertial navigation, and laser targeting, ensuring high precision and effectiveness in various combat scenarios.

The widespread adoption of tactical missiles is driven by their adaptability across multiple platforms, such as ground-based launchers, aircraft, and naval vessels. Their capability to deliver precise strikes minimizes collateral damage and enhances mission success rates, aligning with the evolving doctrines of modern militaries that prioritize precision and efficiency.

Furthermore, ongoing investments in defense modernization programs and the development of next-generation missile systems continue to bolster the growth and dominance of the tactical missiles segment in the precision guided munitions market.

By Technology Analysis

In 2024, the Global Positioning System (GPS) segment held a dominant position in the precision guided munitions (PGM) market, capturing more than 28% of the total market share. This leadership is primarily attributed to the widespread adoption of GPS technology in modern warfare, where precision and accuracy are paramount.

GPS-guided munitions offer reliable targeting capabilities, enabling forces to engage targets with high accuracy, even in challenging environments. The integration of GPS technology into various munitions, such as bombs, missiles, and artillery shells, has enhanced the effectiveness of military operations by reducing collateral damage and increasing mission success rates.

The preference for GPS-guided munitions is further reinforced by their cost-effectiveness and ease of integration into existing weapon systems. Unlike other guidance technologies that may require additional infrastructure or complex targeting systems, GPS-guided munitions utilize satellite signals, making them more adaptable and efficient.

By Mode of Operation Analysis

In 2024, the autonomous segment held a dominant position in the precision guided munitions (PGM) market, capturing over 54% of the total market share. This significant share is attributed to the increasing demand for advanced military capabilities that enhance operational efficiency and reduce the need for human intervention in high-risk combat scenarios.

Autonomous PGMs are equipped with sophisticated guidance systems, including artificial intelligence and machine learning algorithms, enabling them to identify, track, and engage targets with high precision. This capability not only improves mission success rates but also minimizes collateral damage, aligning with the evolving doctrines of modern warfare.

The growth of the autonomous segment is further fueled by substantial investments in defense modernization programs across various countries. Governments are prioritizing the development and acquisition of autonomous weapon systems to maintain strategic superiority and address emerging security challenges.

By Launch Platform Analysis

In 2024, the airborne segment held a dominant position in the global precision guided munitions (PGM) market, capturing more than 44% of the total market share. This leadership is primarily attributed to the increasing reliance on aerial platforms, such as fighter jets, bombers, and unmanned aerial vehicles (UAVs), for delivering precision strikes in modern warfare.

Airborne PGMs offer strategic advantages, including rapid deployment, extended range, and the ability to engage targets in complex and contested environments, making them indispensable assets in contemporary military operations.

The growth of the airborne segment is further fueled by significant investments in advanced technologies and the modernization of air forces worldwide. The integration of sophisticated guidance systems, such as GPS, laser, and infrared technologies, enhances the accuracy and effectiveness of airborne munitions.

Additionally, the development of next-generation aircraft capable of carrying a diverse array of PGMs expands the operational capabilities of air forces, enabling them to conduct precision strikes with minimal collateral damage.

Key Market Segments

By Speed

- Subsonic

- Supersonic

- Hypersonic

By Product

- Tactical Missiles

- Guided Rockets

- Guided Ammunition

- Torpedoes

- Loitering Munitions

By Technology

- Infrared

- Laser

- Inertial Navigation System (INS)

- Global Positioning System (GPS)

- Radar Homing

- Anti-radiation

By Mode of Operation

- Autonomous

- Semi-autonomous

By Launch Platform

- Land

- Airborne

- Naval

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Driver

Rising Demand for Precision Strike Capabilities

The modern battlefield has evolved into a complex environment where precision and minimal collateral damage are paramount. This shift has led to an increased demand for precision-guided munitions (PGMs), which offer the ability to engage targets with high accuracy.

The integration of advanced guidance systems, such as GPS and inertial navigation, allows these munitions to strike targets effectively, even in challenging conditions. This capability is particularly valuable in urban warfare scenarios, where distinguishing between combatants and civilians is crucial.

Restraint

High Development and Procurement Costs

While the benefits of PGMs are clear, their development and acquisition come with substantial financial implications. The research, testing, and production of these advanced munitions require significant investment, which can strain defense budgets, especially for countries with limited resources. The high costs associated with PGMs can limit their accessibility, potentially leading to disparities in military capabilities among nations.

Additionally, the maintenance and operational costs of PGMs add to the financial burden. Smaller nations or those facing economic challenges may find it difficult to allocate sufficient funds for the procurement and upkeep of these systems. This financial barrier can hinder the widespread adoption of PGMs, potentially affecting global security dynamics .

Opportunity

Integration with Unmanned Systems

The convergence of PGMs with unmanned systems presents a significant opportunity for enhancing military capabilities. Unmanned aerial vehicles (UAVs) equipped with PGMs can conduct precision strikes without risking human lives, offering a strategic advantage in various combat scenarios. This integration allows for extended operational reach and flexibility, enabling forces to engage targets in inaccessible or high-risk areas.

The collaboration between EDGE and Baykar to integrate Desert Sting 16 PGMs onto the Baykar TB2 UAV exemplifies this trend. Such partnerships highlight the potential for combining advanced munitions with unmanned platforms to create versatile and effective combat solutions. As technology continues to advance, the synergy between PGMs and unmanned systems is expected to play a pivotal role in future military operations.

Challenge

Vulnerability to Electronic Countermeasures

Despite their technological sophistication, PGMs are susceptible to electronic countermeasures employed by adversaries. Techniques such as GPS jamming and signal spoofing can disrupt the guidance systems of these munitions, reducing their effectiveness and reliability. The conflict in Ukraine has demonstrated how electronic warfare tactics can neutralize the advantages of PGMs, as evidenced by the diminished performance of certain U.S.-supplied weapons due to Russian electronic interference.

This vulnerability underscores the need for continuous innovation in counter-countermeasure technologies to ensure the resilience of PGMs in contested environments. Developing alternative guidance systems and enhancing the robustness of existing technologies are essential steps in maintaining the strategic value of PGMs. Addressing these challenges is critical to preserving the effectiveness of precision-guided munitions in modern warfare.

Growth Factors

Surge in Defense Spending and Technological Advancements

The global precision-guided munitions (PGM) market is experiencing significant growth, driven by increased defense spending and rapid technological advancements. Nations worldwide are allocating substantial budgets to modernize their military capabilities, focusing on enhancing precision strike capabilities to address evolving security challenges.

For instance, the U.S. Department of Defense allocated approximately USD 30.6 billion for munitions in its Fiscal Year 2024 budget, marking a 12% increase from the previous year. This trend reflects a global emphasis on strengthening military arsenals with advanced, accurate, and efficient weaponry.

Technological innovations are also propelling the PGM market forward. The integration of advanced guidance systems, such as GPS, inertial navigation, and laser targeting, has significantly improved the accuracy and effectiveness of munitions. Additionally, the development of hypersonic missiles and AI-enabled targeting systems is revolutionizing modern warfare, offering enhanced speed, precision, and adaptability.

Emerging Trends

Integration with Unmanned Systems and AI

A prominent trend in the PGM market is the integration of munitions with unmanned systems, such as drones and autonomous vehicles. This synergy enhances operational flexibility, allowing for precise strikes in inaccessible or high-risk areas while minimizing human risk.

The collaboration between EDGE and Baykar to integrate Desert Sting 16 PGMs onto the Baykar TB2 UAV exemplifies this trend . Such partnerships highlight the potential for combining advanced munitions with unmanned platforms to create versatile and effective combat solutions.

Furthermore, the incorporation of artificial intelligence (AI) into PGMs is transforming targeting and decision-making processes. AI algorithms enable munitions to analyze vast datasets, adapt to dynamic environments, and make real-time decisions, thereby increasing the effectiveness and efficiency of military operations.

Business Benefits

Enhanced Operational Efficiency and Cost-Effectiveness

The adoption of precision-guided munitions offers significant business benefits, particularly in terms of operational efficiency and cost-effectiveness. PGMs enable military forces to achieve mission objectives with fewer munitions, reducing the logistical burden and associated costs.

Their high accuracy minimizes collateral damage, thereby decreasing the need for subsequent operations and resource expenditure. This efficiency translates into substantial cost savings over time, making PGMs a financially prudent investment for defense organizations.

Moreover, the versatility of PGMs allows for their deployment across various platforms and mission types, enhancing the adaptability of military forces. This flexibility not only improves strategic responsiveness but also maximizes the return on investment in defense technologies.

Key Player Analysis

The precision guided munitions (PGM) market features several key players with strong global footprints. Lockheed Martin Corporation, RTX Corporation, and Northrop Grumman Corporation are consistently at the forefront due to their wide defense portfolios and strong R&D investments.

These companies have developed advanced missile systems with precision strike capabilities, supporting major defense programs worldwide. Their long-term contracts with U.S. and allied militaries enhance market reliability. Their innovations in guided technologies have made them dominant suppliers in air-to-ground and surface-to-air munitions systems.

Boeing Company, BAE Systems plc, and General Dynamics Mission Systems, Inc. are also prominent in the PGM landscape. These firms focus on multi-platform integration, ensuring that their munitions perform across land, air, and sea operations. BAE Systems, in particular, leverages its expertise in autonomous targeting systems, while Boeing offers precision bombs for tactical missions.

Top Key Players in the Market

- ATLAS ELEKTRONIK GmbH

- BAE Systems plc

- Boeing Company

- Denel Dynamics

- Elbit Systems Ltd.

- General Dynamics Mission Systems, Inc.

- Hanwha Aerospace

- Israel Aerospace Industries (IAI) Ltd.

- L3Harris Technologies, Inc.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- RTX Corporation

- Textron Systems

- Thales Group

- Others

Recent Developments

- In December 2024, Raytheon and Ursa Major completed a successful missile flight test for the U.S. Army using a long-range solid rocket motor developed by Ursa Major. This collaboration marks a strategic move to address the Army’s demand for cost-effective precision-guided munitions capable of operating at extended ranges. Raytheon’s investment into Ursa Major highlights the growing urgency to advance propulsion technologies for national defense applications.

- In October 2024, Boeing secured a ~$600 million contract from the U.S. Air Force to upgrade the Joint Direct Attack Munition (JDAM) and Laser JDAM systems. The contract includes technical integration and long-term sustainment services. JDAM technology enhances standard bombs by equipping them with GPS and inertial guidance, while Laser JDAM adds a laser sensor, allowing precise strikes on both fixed and moving targets in all weather conditions.