Quick Navigation

Report Overview

The global Polyfluoroalkyl Substances (PFAS) Waste Management Market size is expected to be worth around USD 3.7 billion by 2033, from USD 2 billion in 2023, growing at a CAGR of 6.4% during the forecast period from 2023 to 2033.

The Polyfluoroalkyl Substances (PFAS) Waste Management Market involves strategies and solutions designed to effectively handle and dispose of wastes containing PFAS, a group of man-made chemicals notorious for their persistence in the environment and potential adverse health effects. PFAS are widely used in a variety of industrial applications and consumer products such as non-stick cookware, water-repellent fabrics, and firefighting foams, due to their resistance to heat, water, and oil.

The challenge in managing PFAS waste stems from their chemical stability, which prevents them from breaking down naturally in the environment. This persistence can lead to contamination of soil, water, and air, posing risks to human health and ecosystems. Effective management of PFAS waste requires specialized treatment technologies that can remove or destroy these compounds, preventing their release into the environment.

Key strategies in the PFAS Waste Management Market include advanced filtration, incineration at high temperatures, and chemical destruction methods such as electrochemical oxidation. These methods are designed to either contain or break down PFAS compounds safely.

Additionally, regulatory frameworks play a crucial role in guiding the practices and technologies used for PFAS waste management. Governments worldwide are implementing stricter regulations to control PFAS disposal and encourage the development of more effective waste management technologies.

The market for PFAS waste management is growing, driven by increasing awareness of the risks associated with PFAS pollution and the tightening of environmental regulations. This growth is further propelled by industries that are major producers of PFAS waste, seeking solutions to mitigate their environmental impact and comply with legal standards.

Overall, the PFAS Waste Management Market is focused on developing and implementing effective waste treatment and disposal methods that can address the challenges posed by the durability and toxicity of PFAS, ensuring environmental safety and public health.

Key Takeaways

By PFAS Type

In 2023, Perfluorooctanoic Acid (PFOA) held a dominant market position, capturing more than a 38.4% share. PFOA is extensively used in the manufacturing of non-stick cookware and waterproof fabrics, leading to significant waste that requires specialized management strategies due to its persistence and potential health risks.

Perfluorooctane Sulfonate (PFOS) is another major PFAS type, historically used in firefighting foams and various industrial applications. The phase-out and strict regulations have spurred demand for effective disposal and management solutions for existing PFOS waste, emphasizing its critical role in the market.

Perfluorabutanoic Acid (PFBA) and Perfluorodecanoic Acid (PFDA) represent smaller segments of the market. PFBA, with its shorter chain, generally poses less bioaccumulation risk, yet its waste management is crucial due to its wide application in the photographic and printing industries. PFDA, used in food packaging and textiles, requires rigorous waste treatment solutions to mitigate its longer-chain impacts on the environment.

By Process

In 2023, Incineration held a dominant market position, capturing more than a 42.6% share. This process is highly valued for its effectiveness in breaking down PFAS compounds at high temperatures, reducing the volume of waste and removing the risk of environmental contamination. Incineration is particularly crucial for treating PFAS-laden firefighting foams and industrial residues that cannot be safely managed through less intensive processes.

Landfilling is another method used in PFAS waste management. Although it is less ideal due to the risk of leachate and eventual environmental contamination, modern landfills equipped with advanced lining systems and leachate treatment facilities provide a temporary solution for PFAS disposal, especially where incineration is not feasible.

Chemical Oxidation represents an innovative segment in PFAS waste management. This process involves breaking down PFAS chemically, often using strong oxidizing agents. While still under development and optimization for broader application, chemical oxidation offers a potential for onsite treatment of PFAS-contaminated waters and soils, making it a promising area for growth.

By Waste Type

In 2023, PFAS Contaminated Water held a dominant market position, reflecting the widespread challenge of managing PFAS contaminants that leach into water supplies from industrial sites, landfills, and firefighting foam applications. The urgency to treat contaminated water is driven by the direct impact on public health and the stringent regulatory standards for drinking water quality. This segment’s growth is fueled by the increasing implementation of advanced filtration and treatment technologies designed to remove PFAS compounds effectively.

PFAS Contaminated Soil is another critical segment, dealing with soils impacted by the use of PFAS-containing products and waste. Remediation of such soils is essential to prevent further environmental contamination and safeguard agricultural productivity. Techniques such as soil washing, stabilization, and chemical oxidation are employed to manage and reduce PFAS levels in affected areas.

PFAS Contaminated Industrial Waste comprises wastes from various manufacturing processes that use PFAS for product performance enhancements. This segment requires specialized handling, treatment, or disposal methods to manage the high concentrations of PFAS typically found in industrial waste streams, highlighting the need for robust waste management systems.

Each of these segments addresses specific challenges associated with PFAS waste, with contaminated water taking precedence due to its direct and widespread impact on ecosystems and human health. Effective management in each category is crucial to mitigate the environmental and health risks posed by these persistent chemicals.

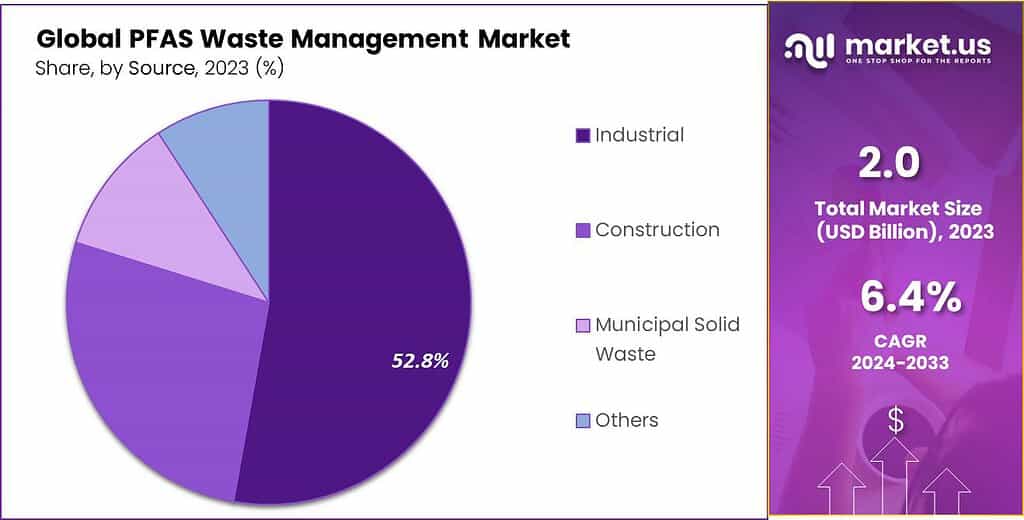

By Source

In 2023, Industrial held a dominant market position, capturing more than a 52.8% share in the PFAS Waste Management Market. This sector is the primary source of PFAS waste due to its extensive use of these chemicals in processes and products that require heat resistance, oil repellency, and chemical stability. Industries such as chemical manufacturing, automotive, and electronics are major contributors, necessitating robust and specialized waste management solutions to handle the high volumes of PFAS waste generated.

Construction is another significant source of PFAS waste, especially from sites where PFAS-containing materials such as paints, sealants, and firefighting foams have been used. Managing PFAS waste in construction involves careful handling and disposal to prevent leaching into the environment, making it a critical area for waste management practices.

Municipal Solid Waste (MSW) also contributes to PFAS contamination, primarily through consumer products that end up in landfills where PFAS can leach into groundwater. Efforts to manage PFAS waste from MSW focus on improving landfill designs and implementing pretreatment programs to intercept PFAS before they enter the waste stream.

Key Market Segments

By PFAS Type

- Perfluorooctane Sulfonate (PFOS)

- Perfluorooctanoic Acid (PFOA)

- Perfluorabutanoic Acid (PFBA)

- Perfluorodecanoic Acid (PFDA)

- Others

By Process

- Landfilling

- Incineration

- Chemical Oxidation

- Others

By Waste Type

- PFAS Contaminated Water

- PFAS Contaminated Soil

- PFAS Contaminated Industrial Waste

By Source

- Industrial

- Construction

- Municipal Solid Waste

- Others

Drivers

Stringent Regulatory Standards and Increasing Environmental Awareness

A major driver for the Polyfluoroalkyl Substances (PFAS) Waste Management Market is the tightening of regulatory standards coupled with growing environmental awareness about the risks associated with PFAS. As research has increasingly highlighted the persistent, bioaccumulative, and toxic nature of PFAS compounds, governmental bodies worldwide have moved to implement stricter regulations aimed at controlling the release and exposure of these substances in the environment.

This regulatory pressure is pushing industries to adopt more rigorous waste management practices to comply with legal standards, significantly driving the demand for PFAS waste management services.

The impact of PFAS on environmental health and safety has become a significant concern. PFAS compounds are known to contaminate water supplies, persist in soil and bioaccumulate in wildlife and humans, leading to various health issues, including cancer, immune system effects, and hormonal disruptions.

Public and governmental pressure has increased as these health implications have become more widely understood, leading to calls for action to reduce both the use and disposal impacts of PFAS. For instance, the United States Environmental Protection Agency (EPA) has included PFAS in its list of priority pollutants and is actively developing new guidelines and rules for PFAS treatment, disposal, and cleanup.

In response to these regulatory developments, industries that produce or handle PFAS are seeking effective ways to manage their litter, driving innovation and investment in the PFAS waste management sector. Technologies and processes such as high-temperature incineration, advanced oxidation processes, and specialized filtration systems are being developed and deployed to effectively destroy or remove PFAS from waste streams. The advancement in these technologies not only helps in complying with regulatory mandates but also aids companies in demonstrating their commitment to environmental stewardship.

Moreover, the rising public awareness and concern about environmental pollution are influencing consumer behavior and corporate policies. Consumers are increasingly demanding that businesses adopt sustainable practices, including the responsible management of hazardous substances like PFAS. Companies are responding by investing in environmentally friendly technologies and waste management practices to enhance their brand image and meet consumer expectations.

Additionally, international collaborations and agreements are also shaping the PFAS waste management market. Global environmental agencies and organizations are working together to establish common standards and practices for managing PFAS, fostering international cooperation in research, technology development, and policy-making. This global approach not only harmonizes the efforts against PFAS pollution but also creates a larger market for solutions providers in the PFAS waste management sector.

Restraints

High Costs and Technological Challenges in PFAS Treatment and Disposal

One of the significant restraints facing the Polyfluoroalkyl Substances (PFAS) Waste Management Market is the high cost and technological challenges associated with the treatment and disposal of PFAS-contaminated materials. PFAS are chemically stable compounds designed to resist heat, water, and oil, which makes them incredibly useful in various industrial applications. However, these same properties also make PFAS extremely difficult to break down, posing a significant challenge for effective waste management.

The treatment of PFAS often requires advanced and costly technologies. Traditional waste treatment methods are generally ineffective at breaking down PFAS, necessitating the development and use of specialized techniques such as high-temperature incineration or advanced chemical oxidation. These methods can effectively reduce PFAS levels in waste streams but come with high operational costs due to the energy demands and complexity of the processes. For instance, high-temperature incineration must be performed at specific temperatures to ensure the complete breakdown of PFAS molecules, which can be expensive to achieve and maintain.

Furthermore, the management of PFAS waste is compounded by the lack of universally accepted and standardized disposal methods. While research into PFAS waste management is ongoing, the field lacks comprehensive, proven strategies that are both cost-effective and environmentally sustainable. This uncertainty in effective waste treatment methodologies can lead to significant investments in research and development, which are not always feasible for smaller companies or municipalities with limited budgets.

Another significant hurdle is the regulatory landscape surrounding the disposal of PFAS, which is still evolving. Different countries and regions may have varying standards and regulations regarding PFAS handling and disposal, creating a complex environment for companies operating internationally. Compliance with these diverse regulations can require additional resources and adaptations, further increasing the costs and complexity of PFAS waste management.

The high costs and technological challenges associated with PFAS waste management not only limit the ability of industries and governments to effectively manage these pollutants but also slow the progress toward finding universal, sustainable solutions. As a result, these factors act as major restraints on the growth of the PFAS Waste Management Market, affecting the ability of stakeholders to respond adequately to the environmental and health challenges posed by PFAS.

Opportunity

Expansion of Regulatory Frameworks

A major opportunity within the Polyfluoroalkyl Substances (PFAS) Waste Management Market is the expansion of regulatory frameworks that mandate the monitoring, reduction, and treatment of PFAS. Governments worldwide are increasingly recognizing the environmental and health risks associated with PFAS, commonly referred to as “forever chemicals” due to their persistent nature in the environment and resistance to natural degradation processes. These substances are widely used in various industries, including manufacturing, aerospace, and consumer products, due to their unique properties such as resistance to heat, water, and oil.

The increasing scrutiny under environmental regulations is compelling companies and municipalities to adopt advanced waste management and treatment solutions, which in turn drives the demand for effective PFAS waste management strategies. For instance, the U.S. Environmental Protection Agency (EPA) has been actively working towards establishing stringent guidelines for the acceptable levels of PFAS in water systems, soil, and air. Such regulatory pressures are prompting a surge in research and development efforts to devise innovative and efficient technologies that can remove or degrade PFAS compounds effectively from contaminated sites.

The development of these regulations often comes with the establishment of cleanup standards and financial penalties for non-compliance, which can be seen as an incentive for affected industries to invest in state-of-the-art waste management technologies. Moreover, funding for research on PFAS pollution and its mitigation is increasing, as evidenced by federal initiatives and grants aimed at addressing this pervasive issue. This regulatory momentum is creating substantial market opportunities for companies specializing in environmental services, chemical analysis, and remediation technologies.

Furthermore, the push for tighter regulations is not limited to the United States. European, Asian, and other global markets are also seeing a trend towards the implementation of more rigorous environmental standards about PFAS. This global shift is enlarging the market space for PFAS waste management solutions and encouraging technological innovation and collaboration across borders. Companies are also likely to benefit from the growing market demand by diversifying their service offerings to include PFAS assessment, removal, disposal, and ongoing monitoring services.

Besides, public and corporate awareness about the dangers of PFAS is increasing, leading to greater consumer advocacy for products free from PFAS and industries adopting PFAS-free processes. This shift in consumer behavior and corporate policies further amplifies the need for effective PFAS waste management solutions, presenting a significant opportunity for growth in this sector.

Trends

Adoption of Advanced Remediation Technologies

One of the most significant trends in the Polyfluoroalkyl Substances (PFAS) Waste Management Market is the adoption of advanced remediation technologies. As the awareness of the adverse environmental and health impacts of PFAS compounds grows, there is an increasing push toward developing and implementing innovative technologies that can effectively treat and manage these persistent chemicals.

The unique properties of PFAS, which make them highly resistant to heat, water, and oil, also render them particularly challenging to manage. Consequently, the focus has shifted towards leveraging cutting-edge scientific and engineering solutions to tackle this issue.

Advanced remediation technologies such as high-pressure membrane filtration, adsorbent materials, and advanced oxidation processes are gaining traction. High-pressure membrane technologies, like nanofiltration and reverse osmosis, are proving to be effective in removing PFAS from water sources. These methods benefit from the ability to target the tiny molecular size of PFAS compounds, thereby providing a barrier that stops these chemicals from passing through. On the other hand, adsorbent materials, including activated carbon and ion exchange resins, are being widely adopted for their capacity to adsorb and remove PFAS from contaminated soil and water. These materials offer a cost-effective solution that can be implemented at a large scale for wide-area environmental remediation.

Another innovative approach is the use of advanced oxidation processes, which involve the generation of highly reactive radicals capable of breaking down PFAS compounds into less harmful substances. These processes are particularly valuable in dealing with aqueous film-forming foams (AFFFs), which are a major source of PFAS contamination. The technology is still in the developmental phase but promises to add a significant tool in the arsenal against PFAS pollution.

The development and adoption of these technologies are being driven by both regulatory pressure and the potential for economic gains. Regulatory bodies worldwide are setting stringent limits on PFAS levels in the environment and enforcing compliance with cleanup efforts. This regulatory environment creates a fertile ground for innovation, as companies and research institutions vie to offer effective solutions that can meet these new standards. Additionally, the growing market demand for PFAS remediation is seen as an economic opportunity by environmental service providers, chemical companies, and startups, which drives further investment in research and technology development.

Furthermore, collaboration among industry stakeholders, including government agencies, private companies, and academic institutions, is facilitating the rapid advancement and deployment of these technologies. These partnerships help in sharing knowledge, pooling resources, and scaling solutions that could otherwise be limited by individual capabilities. The trend towards collaboration not only accelerates technological advancements but also ensures that these solutions are viable at an economic and operational level.

Regional Analysis

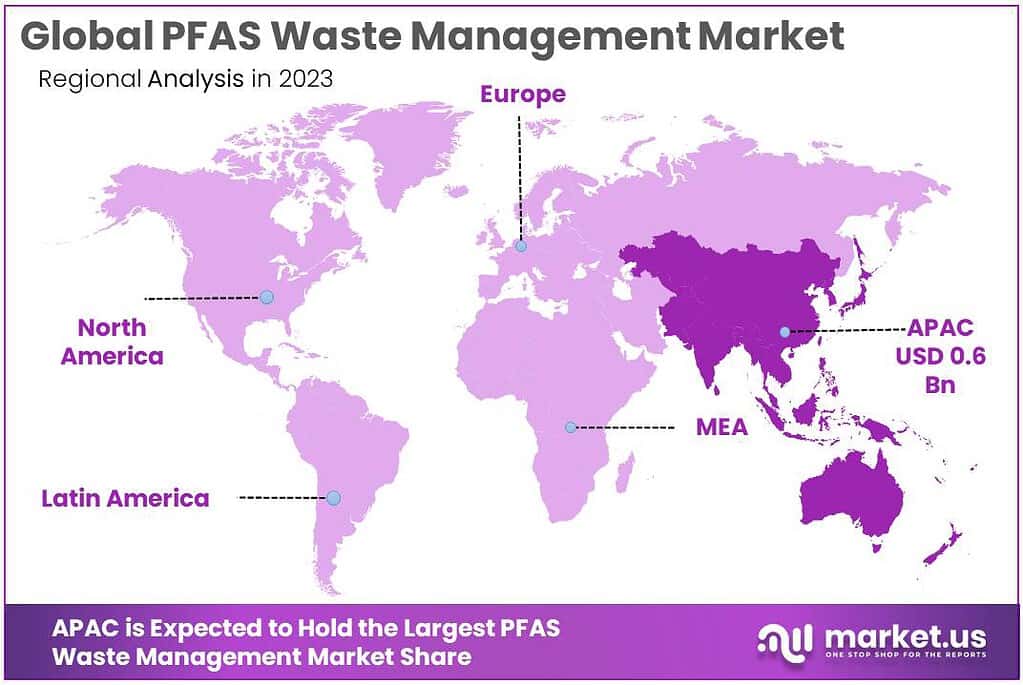

In 2023, the Asia Pacific region commanded a significant share, accounting for 28.4% of the Polyfluoroalkyl Substances (PFAS) Waste Management Market, with a total worth of USD 0.568 Billion.

The global PFAS Waste Management Market is segmented into distinct geographical regions, namely North America, Europe, Asia Pacific, Middle East & Africa, and Latin America, each displaying distinct growth patterns and opportunities.

North America has demonstrated consistent growth within the PFAS Waste Management Market, primarily fueled by advancements in waste management technologies and a heightened demand for sustainable waste disposal solutions. The region’s commitment to innovative and environmentally conscious practices contributes to its substantial market presence.

Europe closely follows suit, placing a strong emphasis on stringent environmental regulations that encourage the adoption of sustainable waste management practices, including the treatment and disposal of PFAS-contaminated waste. European nations lead in implementing rigorous environmental standards, thereby driving the demand for advanced PFAS waste management solutions.

The dominance of the Asia Pacific region in the PFAS Waste Management Market is evident, holding a noteworthy 28.4% market share valued at USD 0.568 Billion. This supremacy can be attributed to the rapid industrialization, urbanization, and burgeoning packaging sector in emerging economies such as China and India. The region’s extensive manufacturing activities, coupled with an increasing awareness of environmental concerns, propel the demand for effective PFAS waste management solutions.

Although smaller in market size, the Middle East & Africa region is witnessing growth attributed to escalating infrastructure developments and industrial ventures, necessitating efficient waste management solutions, including those for PFAS-contaminated waste.

Key Regions and Countries

- North America

- The US

- Canada

- Mexico

- Western Europe

- Germany

- France

- The UK

- Spain

- Italy

- Portugal

- Ireland

- Austria

- Switzerland

- Benelux

- Nordic

- Rest of Western Europe

- Eastern Europe

- Russia

- Poland

- The Czech Republic

- Greece

- Rest of Eastern Europe

- APAC

- China

- Japan

- South Korea

- India

- Australia & New Zealand

- Indonesia

- Malaysia

- Philippines

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Colombia

- Chile

- Argentina

- Costa Rica

- Rest of Latin America

- Middle East & Africa

- Algeria

- Egypt

- Israel

- Kuwait

- Nigeria

- Saudi Arabia

- South Africa

- Turkey

- United Arab Emirates

- Rest of MEA

Key Players Analysis

Market Key Players

- Republic Services, Inc.

- Veolia

- WSP

- Evoqua Water Technologies LLC

- Clean Harbors, Inc.

- Indaver

- Chemviron

- Clean Management Environmental Group, Inc.

- Wanless Waste Management

- Newterra

- TerraTherm

- OPEC Systems Pty Ltd

- Golder Associates

Recent Development

In January 2023 Republic Services, Inc, Company initiated a comprehensive review of its waste processing facilities to ensure compliance with stringent PFAS regulations, setting a precedent for responsible waste management practices within the industry.

In 2023, Veolia advanced PFAS management by deploying various technologies, including granular activated carbon, ion exchange systems, and reverse osmosis, tailored to specific contamination levels and local regulations.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 2 Bn |

| Forecast Revenue (2033) | US$ 3.7 Bn |

| CAGR (2024-2033) | 6.4% |

| Base Year for Estimation | 2023 |

| Historic Period | 2020-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By PFAS Type(Perfluorooctane Sulfonate (PFOS), Perfluorooctanoic Acid (PFOA), Perfluorabutanoic Acid (PFBA), perfluorodecanoic Acid (PFDA), Others), By Process(Landfilling, Incineration, Chemical Oxidation, Others), By Waste Type(PFAS Contaminated Water, PFAS Contaminated Soil, PFAS Contaminated Industrial Waste), By Source(Industrial, Construction, Municipal Solid Waste, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Republic Services, Inc., Veolia, WSP, Evoqua Water Technologies LLC, Clean Harbors, Inc., Indaver, Chemviron, Clean Management Environmental Group, Inc., Wanless Waste Management, Newterra, TerraTherm, OPEC Systems Pty Ltd, Golder Associates |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |

Frequently Asked Questions (FAQ)

Polyfluoroalkyl Substances (PFAS) Waste Management Market size is expected to be worth around USD 3.7 billion by 2033, from USD 2 billion in 2023

Republic Services, Inc., Veolia, WSP, Evoqua Water Technologies LLC, Clean Harbors, Inc., Indaver, Chemviron, Clean Management Environmental Group, Inc., Wanless Waste Management, Newterra, TerraTherm, OPEC Systems Pty Ltd, Golder Associates

Waste Management Market")