Quick Navigation

Report Overview

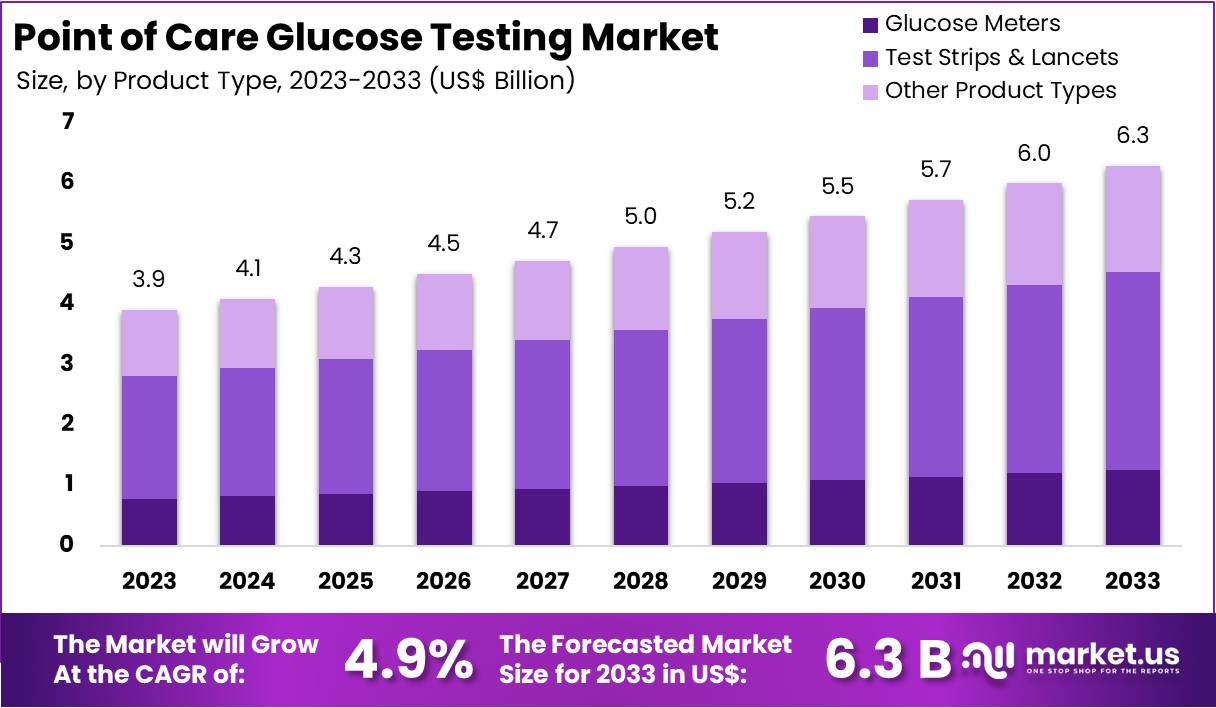

The Global Point of Care Glucose Testing Market size is expected to be worth around US$ 6.3 Billion by 2033, from US$ 3.9 Billion in 2023, growing at a CAGR of 4.9% during the forecast period from 2024 to 2033.

Point of Care (POC) glucose testing is crucial for managing diabetes, providing immediate blood glucose level assessments directly at care sites, such as homes or clinics. These tests are especially prevalent in hospitals, where they’re the most commonly performed diagnostic tests. The market includes traditional meters, continuous monitoring systems, and emerging non-invasive technologies. Factors like the growing diabetes prevalence and advancements in glucose testing technologies drive market growth, catering to the demand for quick, reliable results and the shift towards personalized healthcare.

Accuracy in POC glucose testing can vary due to physiological and external factors. For example, low hematocrit levels can cause falsely elevated glucose readings in some devices. Recognizing this, the U.S. Food and Drug Administration (FDA) has set strict guidelines to ensure reliability, particularly in professional settings.

A study reported by Diabetes Journals indicates that the U.S. Food and Drug Administration (FDA) has set strict guidelines to ensure the accuracy of Point-of-Care (POC) glucose meters in professional healthcare environments. These guidelines require that 99% of glucose measurements should fall within ±10% of a reference method when glucose concentrations exceed 70 mg/dL, and within ±7 mg/dL when concentrations are below 70 mg/dL. This ensures reliable glucose monitoring for patient care.

Recent technological advancements are reshaping the POC glucose testing landscape. Notably, the FDA has cleared new over-the-counter continuous glucose monitoring devices, such as Abbott Laboratories’ Libre Rio and Lingo. These innovations are designed to enhance accessibility, offering critical health insights not only to diabetics but also to individuals focused on general wellness. Such developments highlight the evolving nature of glucose monitoring technologies in facilitating effective diabetes management.

According to the World Health Organization, diabetes caused 1.5 million deaths in 2019, with nearly half of these occurring in individuals under 70. The International Diabetes Federation paints a starker picture, attributing 6.7 million deaths to diabetes in 2021. Currently, an estimated 537 million people worldwide live with diabetes, a number projected to rise to 643 million by 2030. This escalating global burden underscores the critical need for efficient diabetes management and monitoring solutions.

Despite the prevalence of diabetes, significant disparities exist in treatment and diagnosis, particularly in low- and middle-income countries (LMICs). In 2021, diabetes led to 1.6 million deaths, with another 530,000 from kidney disease linked to diabetes, showcasing the extensive impact of this noncommunicable disease. With rising mortality rates since 2000, combating diabetes, especially Type 2, which is predominant in LMICs, has become a public health priority. Efforts are increasingly focused on improving diagnosis rates and optimizing care for those already diagnosed, highlighting the integral role of POC glucose testing in global health strategies.

Key Takeaways

- The Point of Care Glucose Testing Market is projected to grow from US$ 3.9 billion in 2023 to US$ 6.3 billion by 2033, with a CAGR of 4.9%.

- In 2023, Test Strips & Lancets led the product types in the market, accounting for over 52.1% of the total share.

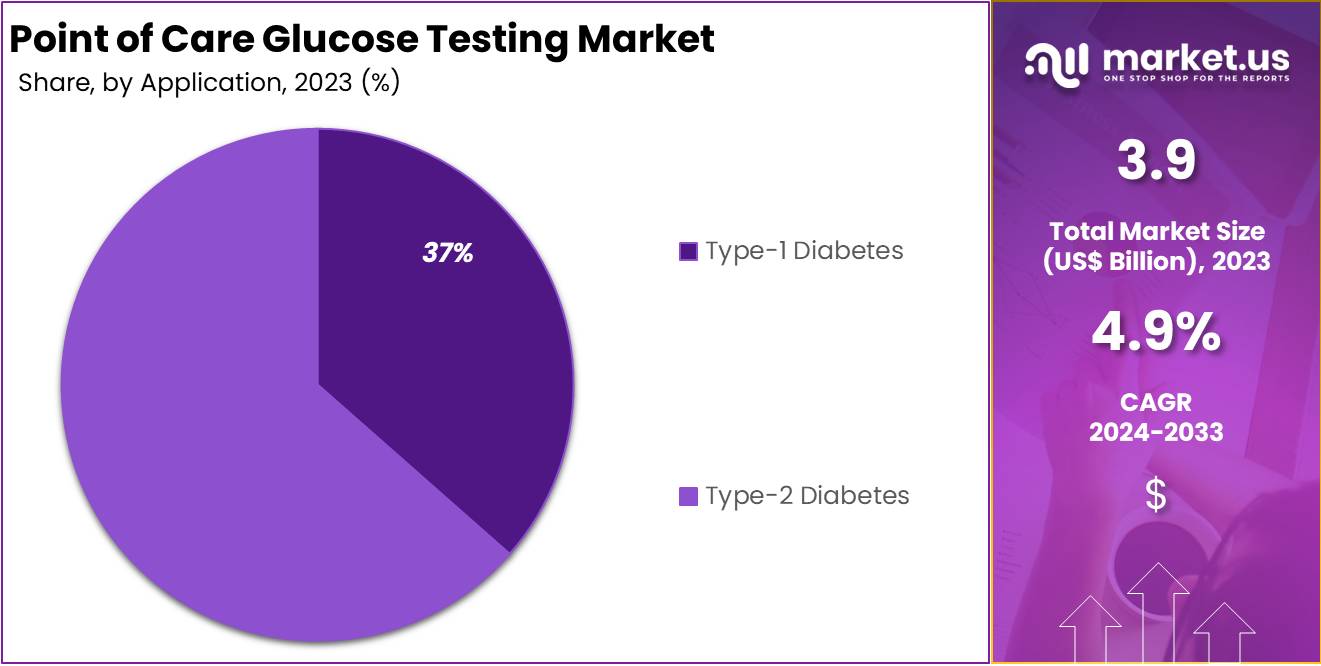

- The Type-2 Diabetes application was the most significant in 2023, holding a commanding 63.5% of the market share.

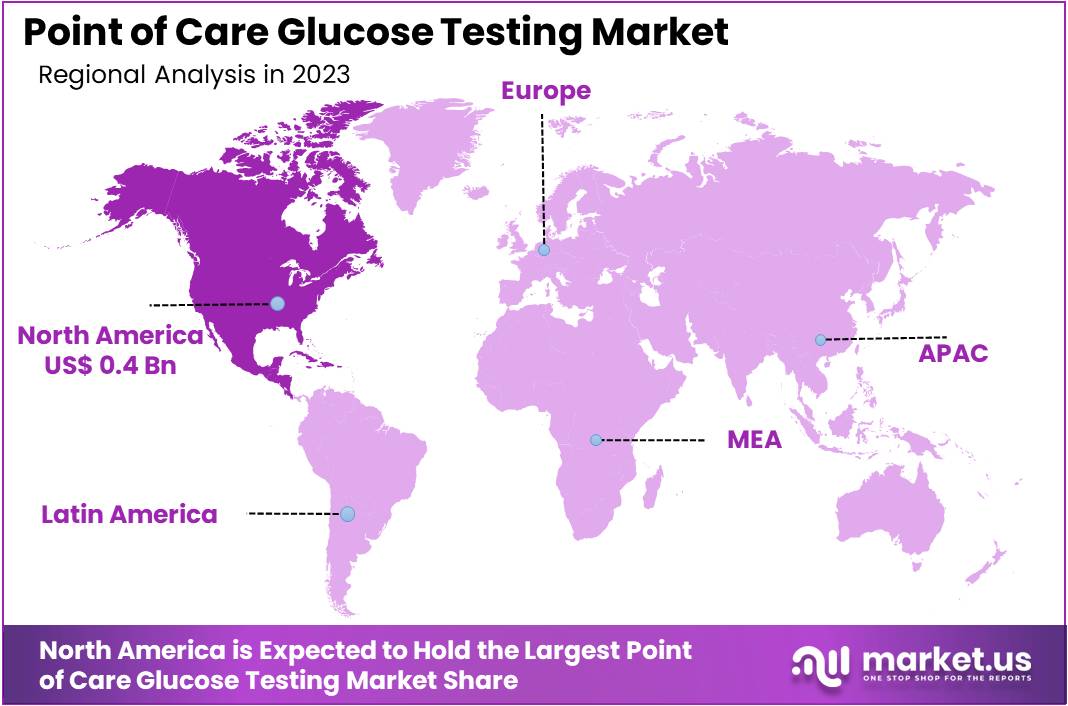

- North America dominated the market in 2023, with a 41.4% share and a market value of US$ 0.4 billion.

Product Type Analysis

In 2023, the Test Strips & Lancets segment held a dominant market position in the Product Type Segment of the Point of Care Glucose Testing Market, capturing more than a 52.1% share. This segment’s leading status is driven by its crucial role in everyday glucose monitoring for individuals with diabetes. The consistent use of these products underscores their importance in managing this chronic condition effectively.

Test strips and lancets are favored for their ease of use and quick results. These attributes make them indispensable in both clinical and home settings. Patients and healthcare providers rely on these tools for their dependability, which in turn supports their widespread adoption across the market.

The surge in diabetes prevalence worldwide has further fueled the demand for test strips and lancets. This trend is expected to continue, thus bolstering the segment’s growth. Their affordability and accessibility contribute to their extensive use, making them fundamental components of diabetes care routines.

While glucose meters and other related products also play a significant role, they occupy a smaller portion of the market compared to test strips and lancets. The primary focus on the latter highlights their critical position in the Point of Care Glucose Testing Market. Their straightforward application and cost-effectiveness continue to support their dominance in the field.

Application Analysis

In 2023, the Type-2 Diabetes segment held a dominant position in the Application Segment of the Point of Care Glucose Testing Market, capturing more than a 63.5% share. This significant market share underscores the widespread incidence of Type-2 Diabetes worldwide. It primarily affects adults and is closely linked to lifestyle factors such as diet and physical activity.

The prevalence of this condition drives the demand for efficient point of care glucose testing solutions. These tools are crucial for managing the disease effectively. They enable rapid, on-the-spot glucose monitoring, which is essential for daily diabetes management.

Point of care devices are valued for providing immediate feedback. This instant data helps patients and healthcare providers make quick decisions about treatment adjustments. This capability is vital in preventing the long-term complications commonly associated with unmanaged blood sugar levels.

The trend towards more patient-centered care continues to boost the demand for these devices. As healthcare moves towards models that prioritize patient empowerment, point of care glucose testing devices are expected to maintain, if not increase, their essential role in diabetes management.

End User Analysis

In 2023, the Hospitals & Clinics segment held a dominant market position in the End User Segment of the Point of Care Glucose Testing Market, capturing more than a 45.9% share. This segment’s leadership is attributed to the essential role of quick testing in patient management. Hospitals and clinics prioritize rapid test results to make timely decisions that impact patient care, making point of care devices crucial in these settings.

The Home Care Settings segment is also notable, driven by the rising demand among individuals managing diabetes at home. As technology advances, these devices have become more user-friendly and accurate, appealing to a broader user base. This shift supports the growth of home care applications, where convenience and cost efficiency are key.

Other segments, like remote clinics and long-term care facilities, show a smaller yet growing adoption rate. These areas are increasingly turning to point of care glucose testing to improve care standards. Their usage underscores a trend towards expanding point of care applications beyond conventional hospital environments.

This expansion highlights the market’s potential growth, driven by the overarching need for accessible and efficient healthcare solutions. As different end-user segments recognize the benefits of point of care glucose testing, its integration across varied healthcare settings is expected to increase, supporting broader market development.

Key Market Segments

By Product Type

- Glucose Meters

- Test Strips & Lancets

- Others

By Application

- Type-1 Diabetes

- Type-2 Diabetes

By End User

- Hospitals and Clinics

- Home Care Settings

- Others

Drivers

Increasing Prevalence of Diabetes

The global rise in diabetes is a significant driver for the Point of Care (POC) glucose testing market. According to the latest International Diabetes Federation (IDF) Diabetes Atlas, the prevalence of diabetes has reached 10.5% worldwide. This increasing trend underscores the urgent need for reliable and convenient glucose monitoring solutions. POC glucose testing devices fulfill this need by providing quick and accurate results, essential for effective diabetes management.

Diabetes management requires regular monitoring, making the convenience of POC glucose testing devices highly attractive. These devices offer rapid results, which are crucial for patients to adhere to their glucose monitoring routines effectively. As diabetes continues to be a major health challenge globally, the demand for such efficient testing solutions is expected to grow, supporting the expansion of the POC glucose testing market.

The growing incidence of diabetes is particularly pronounced in densely populated regions undergoing rapid urbanization. Lifestyle changes, such as decreased physical activity and increased obesity rates, contribute to the rising diabetes cases. This scenario highlights the critical role of POC glucose testing devices in managing this disease, as they provide a practical solution for patients needing frequent glucose assessments.

Study findings reveal that a significant portion of the global diabetic population remains undiagnosed—44.7% according to the IDF. This highlights a vast potential market for POC glucose testing, as early detection and management of diabetes can greatly benefit from the accessibility and ease of use provided by these devices.

Projections indicate a dramatic increase in diabetes prevalence, with estimates suggesting that by 2045, around 783 million adults will be living with the condition. This represents a 46% increase, more than double the expected population growth over the same period. Such statistics emphasize the growing need for POC glucose testing devices, positioning them as essential tools in combating the diabetes epidemic.

Restraints

High Cost of Devices

The high costs associated with advanced point-of-care (POC) glucose testing devices present a significant restraint in the market, particularly impacting low and middle-income countries. These advanced devices, including continuous glucose monitors and wearable sensors, while beneficial for diabetes management, are priced at a premium. This pricing strategy limits their accessibility and adoption in economically constrained regions, affecting market growth negatively.

Market analysis highlights the integration of sophisticated sensor technologies and digital health solutions as contributing factors to the cost of POC glucose testing devices. Such integrations improve functionality and patient compliance but also increase the price, making them less accessible in less affluent areas. Addressing these cost barriers is crucial for manufacturers aiming to expand their market reach and ensure broader global access to these advanced diabetes management technologies.

To overcome these challenges, there is a focus on developing cost-effective solutions that do not compromise on the effectiveness of managing diabetes. The industry is pushing for innovations that maintain quality while being financially accessible to broader demographics. As the market continues to evolve, providing affordable glucose monitoring solutions will be key to enhancing market penetration and improving access to these critical health technologies globally.

Opportunities

Technological Advancements In Glucose Testing

Technological advancements in glucose testing present significant opportunities for the Point of Care Glucose Testing Market. Innovations such as Continuous Glucose Monitoring (CGM) systems have revolutionized diabetes management by offering more accurate, convenient, and less invasive methods for monitoring blood glucose levels. According to the American Diabetes Association, these advancements have notably improved patient outcomes and quality of life, appealing especially to tech-savvy populations seeking efficient healthcare solutions.

Continuous Glucose Monitoring (CGM) systems are a key driver of market growth. These systems provide real-time data on glucose levels, enabling better glycemic control. Studies indicate that CGM use can lead to substantial improvements in HbA1c levels and significantly reduce the risk of hypoglycemia. For instance, a real-world analysis found that CGM use in adults with type 2 diabetes resulted in a 1% reduction in HbA1c across various therapy groups, showcasing the system’s effectiveness.

Automated Insulin Delivery (AID) systems, also known as artificial pancreas systems, further illustrate the impact of technological advancements. These systems integrate CGM data with insulin pumps to automate insulin delivery. A study by the American Diabetes Association, the SECURE-T2D pivotal trial, showed that using the Omnipod® 5 AID System led to a significant reduction in HbA1c levels, from a baseline average of 8.2% to 7.4% over 13 weeks.

Research into non-invasive glucose monitoring methods is advancing, aiming to eliminate the need for finger pricks. Technologies like near-infrared spectroscopy and the integration of deep learning with ECG signals are under development. These methods strive to provide accurate glucose measurements without physical invasiveness, enhancing patient comfort and compliance, and opening new avenues for market expansion.

Overall, these technological advancements are poised to broaden market penetration and attract new user segments by offering enhanced accuracy, connectivity, and ease of use. As these innovations continue to evolve, they hold the potential to transform the Point of Care Glucose Testing Market, making diabetes management more accessible and less burdensome for patients globally.

Trends

Integration With Digital Health Platforms

Integration with digital health platforms is increasingly prominent in the Point of Care (POC) glucose testing market. This trend reflects a shift towards more interconnected and accessible healthcare solutions. POC glucose testing devices are being integrated with these digital platforms to enhance diabetes management. This integration allows for real-time data analysis and better patient engagement with their health metrics. It enables healthcare providers to access up-to-date information, facilitating immediate feedback and personalized care plans. Such connectivity is becoming essential in providing efficient and effective diabetes care.

Mobile health applications, an integral part of these digital platforms, have shown significant benefits in managing diabetes. For instance, mHealth apps support continuous monitoring and can trigger personalized interventions based on the data received from POC glucose testing devices. This capability leads to improved health behaviors and better management outcomes for patients with diabetes.

The integration of POC glucose testing with digital health platforms exemplifies the evolution of healthcare towards more integrated and patient-centric models. As this trend continues, it is expected to drive advancements in diabetes care, emphasizing the importance of technology in managing chronic conditions and enhancing patient quality of life.

Regional Analysis

In 2023, North America held a dominant market position, capturing more than a 41.4% share and holds US$ 0.4 Billion market value for the year. This region’s leadership is largely due to its high diabetes prevalence, necessitating widespread access to point of care glucose testing. The region’s advanced healthcare infrastructure also supports the rapid adoption and integration of these technologies.

Significant healthcare investments enhance the growth of this market. Both public and private sectors in North America are committed to funding healthcare innovations. This financial support helps accelerate the availability and improvement of point of care testing solutions, which are essential for managing diabetes effectively.

Awareness around diabetes management is increasing in North America. More individuals are taking proactive steps towards managing their health, which boosts the demand for point of care glucose testing. Regulatory support further strengthens this trend, with guidelines that ensure the safety and efficacy of these devices, thereby increasing user confidence.

The technological integration in medical devices, particularly those enabling point of care glucose testing, is transforming the market. Digital tools enhance device functionality and accessibility, appealing to a tech-savvy population. As technology advances and healthcare access expands, North America is poised to maintain its lead in the global point of care glucose testing market.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

The Point-of-Care Glucose Testing Market includes several key players that drive innovation and improve product accessibility. F. Hoffmann-La Roche Ltd. is a leader in this market, offering a variety of glucose testing devices. The company invests heavily in research to enhance product accuracy and ease of use. Its global presence and strong brand recognition position it as a top competitor. Roche’s continued commitment to quality ensures its sustained dominance in the market, appealing to both healthcare providers and individual users.

Abbott plays a major role in this market, especially with its FreeStyle Libre system. This product reduces the reliance on traditional finger-prick tests through continuous glucose monitoring (CGM) technology. Abbott focuses on real-time monitoring solutions and affordability, which boost its market appeal. Nipro, another prominent player, provides a range of glucose testing devices known for their quality and reliability. The company targets both hospitals and homecare, strengthening its market presence with cost-effective and versatile solutions.

Lifescan Inc., operated by Platinum Equity Advisors LLC, is widely recognized for its OneTouch range of glucose meters. The company integrates smart technologies, allowing users to sync devices with mobile apps for better diabetes management. Strategic acquisitions and partnerships further enhance its market position. Nova Biomedical is another key player, focusing on glucose meters designed for critical care. Its products are known for their precision and fast results, making them highly valued in professional healthcare settings.

ACON Laboratories addresses the need for affordable glucose testing solutions, especially in underserved regions. The company offers a wide range of products that cater to individuals and healthcare providers. By targeting emerging markets, ACON has expanded its global presence. Other players in the market, including regional companies and startups, contribute to a competitive landscape. Their focus on niche innovations ensures a variety of options for consumers. Together, these companies drive advancements and growth in the POC glucose testing market.

Market Key Players

- F. Hoffmann-La Roche Ltd.

- Abbott

- Nipro

- PlatInium Equity Advisors LLC (Lifescan Inc.)

- Nova Biomedical

- ACON Laboratories

- Trividia Health Inc.

- Prodigy Diabetes Care LLC

- Bayer AG/Ascensia Diabetes Care Holdings AG

- EKF Diagnostics

Industrial Advantages and Opportunities For Market Players

Point-of-care glucose testing offers numerous business benefits for market players. It provides instant diagnostic results, allowing healthcare providers to make quick decisions, which builds trust in these products. The rising prevalence of diabetes worldwide ensures consistent demand, creating a stable revenue source. Additionally, cost-efficient devices attract healthcare providers aiming to reduce expenses while maintaining quality care. Many companies benefit from recurring revenues generated through consumables like test strips and lancets. This market also offers global expansion opportunities, particularly in emerging regions with increasing diabetes rates.

The industrial advantages of point-of-care glucose testing are significant. The development of innovative technologies, such as biosensors and AI-integrated monitors, is transforming the sector. Regulatory approvals for portable devices enable faster market entry, giving companies a competitive edge. These devices also reduce training requirements, cutting operational costs for medical facilities. Connectivity with digital health platforms enhances data management. Moreover, scalable production processes allow manufacturers to meet rising demand, while eco-friendly materials align with global sustainability goals.

Opportunities in the point-of-care glucose testing market are diverse and promising. Integrating wearable technologies provides real-time monitoring, enhancing convenience for users. The growing popularity of telemedicine supports the adoption of remote glucose monitoring. Companies can collaborate with healthcare providers to create comprehensive chronic disease management solutions. Advancements in AI and big data offer innovative ways to manage glucose levels. Personalizing testing solutions caters to individual needs, differentiating products in the market. The increasing demand for home healthcare also creates new revenue opportunities for key players.

Emerging markets present untapped potential for point-of-care glucose testing companies. Regions like Asia-Pacific and Africa are witnessing a rise in diabetes cases, creating a demand for affordable and accessible testing solutions. Wearable and connected devices cater to the needs of these regions, offering ease of use and affordability. With the focus on improving healthcare infrastructure, companies have opportunities to strengthen their presence. These markets also provide a platform for innovative solutions tailored to specific regional healthcare challenges, boosting growth prospects for key industry players.

Recent Developments

- July 2024: Nipro announced a significant expansion with an investment of US$ 397.8 million to establish its first North American manufacturing facility in Greenville, North Carolina. This facility is set to create 232 new jobs and will produce state-of-the-art medical devices, including precision needles for insulin therapies, essential for diabetes management.

- June 2023: Roche launched the cobas® pulse system, a next-generation device designed to enhance the efficiency of blood glucose monitoring in Point of Care (POC) settings. This system integrates high-performance glucose meter technology with cobas® infinity edge, a secure, digital management software. This innovation aims to optimize workflows, reduce operational costs, and improve patient care by providing quick and reliable POC glucose testing results. The system features an intuitive, Android-based interface, which simplifies user interactions and supports integration with health apps to extend its functionality.

- 2023: Abbott received FDA clearance for its FreeStyle Libre 2 Plus sensor, making it the first and only continuous glucose monitoring (CGM) system in the U.S. with a 15-day wear time for all age groups. This advancement is part of Abbott’s continuous effort to improve diabetes care by integrating with automated insulin delivery systems, enhancing user convenience and reducing costs compared to other CGM systems

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2023) | US$ 3.9 Billion |

| Forecast Revenue (2033) | US$ 6.3 Billion |

| CAGR (2024-2033) | 4.9% |

| Base Year for Estimation | 2023 |

| Historic Period | 2019-2022 |

| Forecast Period | 2024-2033 |

| Report Coverage | Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments |

| Segments Covered | By Product Type (Glucose Meters, Test Strips & Lancets, Others), By Application (Type-1 Diabetes, Type-2 Diabetes), By End User (Hospitals and Clinics, Home Care Settings, Others) |

| Regional Analysis | North America – The US, Canada, & Mexico; Western Europe – Germany, France, The UK, Spain, Italy, Portugal, Ireland, Austria, Switzerland, Benelux, Nordic, & Rest of Western Europe; Eastern Europe – Russia, Poland, The Czech Republic, Greece, & Rest of Eastern Europe; APAC – China, Japan, South Korea, India, Australia & New Zealand, Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, & Rest of APAC; Latin America – Brazil, Colombia, Chile, Argentina, Costa Rica, & Rest of Latin America; Middle East & Africa – Algeria, Egypt, Israel, Kuwait, Nigeria, Saudi Arabia, South Africa, Turkey, United Arab Emirates, & Rest of MEA |

| Competitive Landscape | F. Hoffmann-La Roche Ltd., Abbott, Nipro, PlatInium Equity Advisors LLC (Lifescan Inc.), Nova Biomedical, ACON Laboratories, Trividia Health Inc., Prodigy Diabetes Care LLC, Bayer AG/Ascensia Diabetes Care Holdings AG, EKF Diagnostics |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |