Quick Navigation

Report Overview

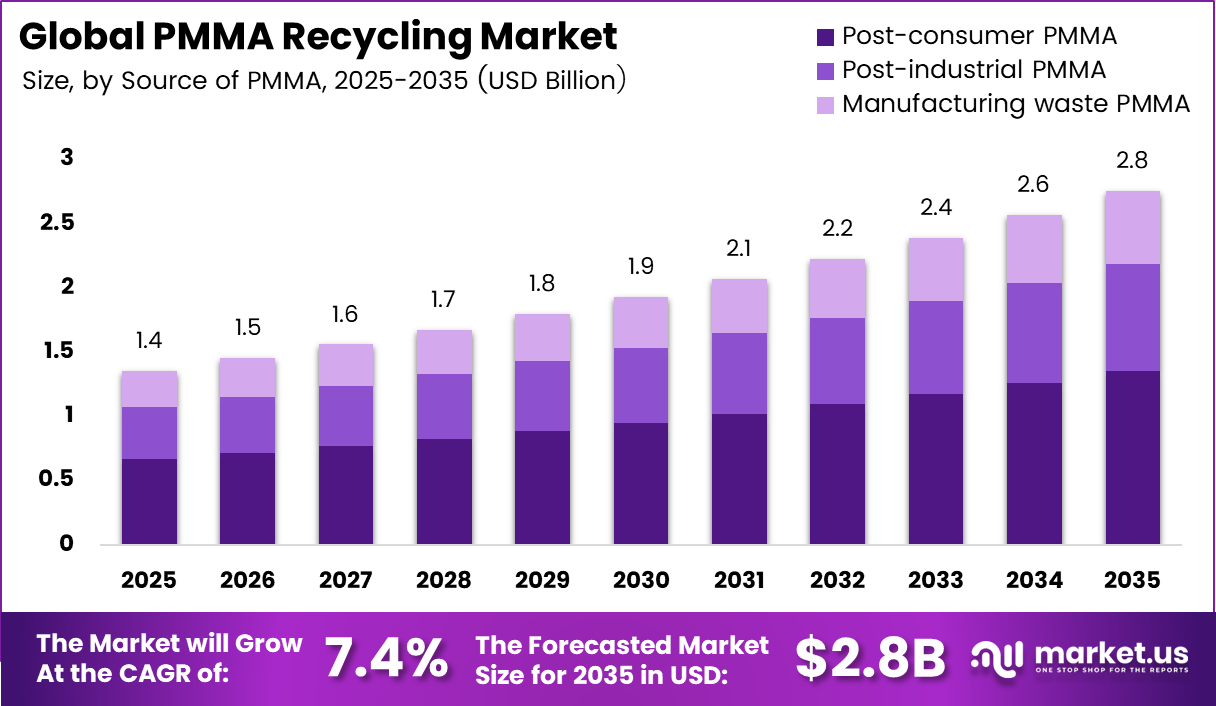

The Global PMMA Recycling Market was valued at USD 1.4 billion in 2025, and between 2026 and 2035, this market is estimated to register a CAGR of 7.4%, reaching about USD 2.8 billion by 2035. Asia Pacific held a dominant market position, capturing more than a 40.2% share, holding USD 0.56 billion in revenue.

The global PMMA recycling market is slowly growing as part of the larger sustainable plastics and circular economy efforts. This growth is because there is more focus on reducing plastic waste, using resources efficiently, and making materials with lower carbon emissions. PMMA recycling collects and processes acrylic materials from different sources like used products, industrial waste, and manufacturing leftovers. These recycled materials are used in important industries such as cars, buildings, electronics, and everyday products.

Newer environmental rules and increased awareness about sustainability are making more companies use recycled PMMA. The Organisation for Economic Co-operation and Development (OECD) reported that effective global policies could reduce plastic leakage into the environment by 96% by 2040, reinforcing the importance of advanced recycling technologies such as PMMA recycling in supporting circular economy goals and reducing plastic waste.

Production and consumption of materials are still mainly happening in the Asia Pacific region. This is because of strong plastic manufacturing industries, quick industrial growth, and more investments in recycling systems in countries like China, Japan, South Korea, and India. In these areas, there’s growing demand for eco-friendly materials from industries such as automotive, electronics, and construction.

New technologies like depolymerization, purification, and closed-loop recycling are slowly making recycled PMMA better in terms of quality and performance. Also, as companies make more promises to be sustainable, more circular economy practices are being used, and more money is being put into advanced recycling tech. These trends are expected to greatly increase the long-term need for recycled PMMA around the world.

Key Takeaways

- The global PMMA Recycling market was valued at US$ 1.4 billion in 2025.

- The global PMMA Recycling market is projected to grow at a CAGR of 7.4% and is estimated to reach US$ 2.8 billion by 2035.

- On the basis of source of PMMA, the post-consumer PMMA segment dominated the global PMMA recycling market, constituting 49.1% of the total market share.

- Based on installation, mechanical recycling dominated the PMMA recycling market, accounting for a substantial market share of around 71.3%.

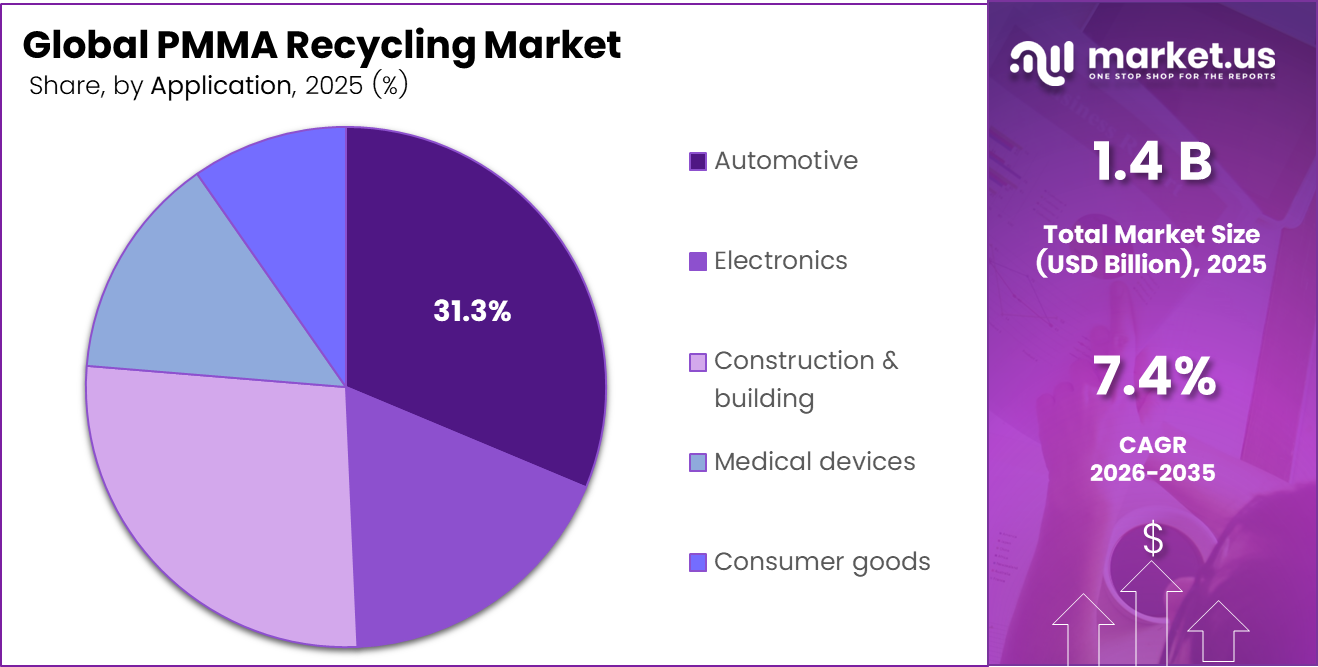

- Based on application, the automotive segment led the market, comprising 31.3% of the total market share.

- Among the product forms, granules emerged as the dominant segment in the PMMA recycling market, holding 45.2% of the overall market share.

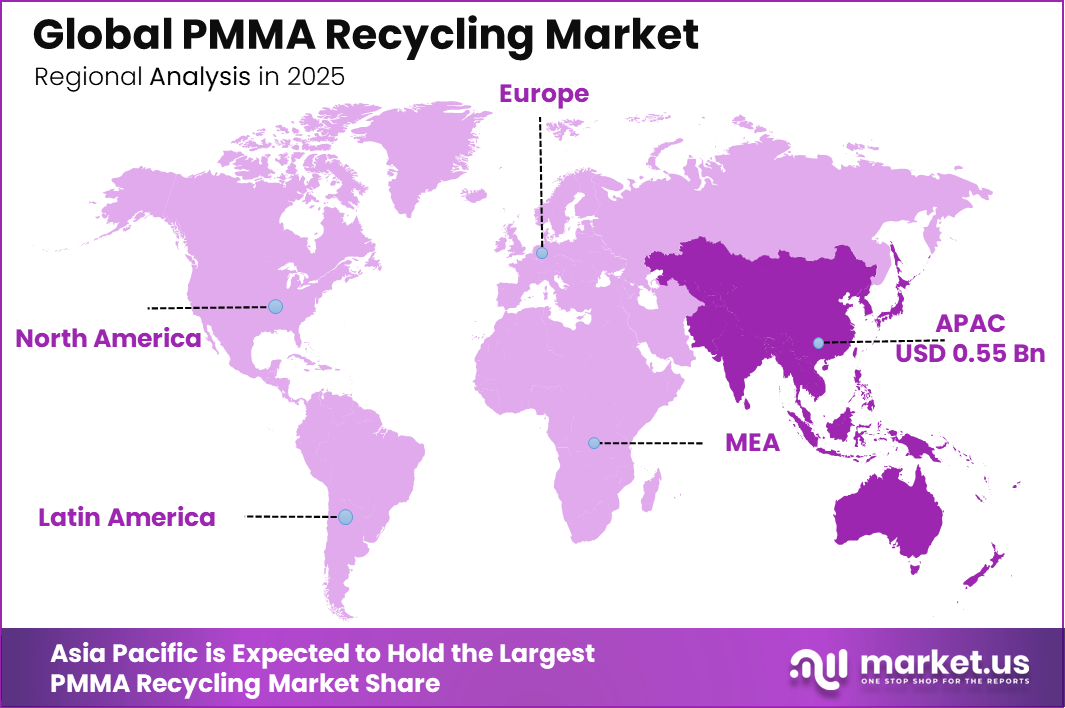

- In 2025, Asia Pacific was the most dominant regional market in the global PMMA recycling industry, accounting for 40.3% of the total global market share.

Source of PMMA Analysis

Post‑consumer PMMA represents the dominant Segment in the Market.

Post-consumer PMMA was the leading segment, holding 49.1% of the overall PMMA recycling market share. The leadership of this segment is mainly attributed to the rising amount of PMMA waste from various industries like automobiles, building, electronics, signage, and consumer goods. Acrylic sheets, car taillights, displays, and signboards are among other materials contributing to PMMA waste.

Increasing focus on environmental issues, stringent legislation regarding plastic waste disposal, and growing popularity of circular economy practices will continue to boost the growth of this segment. Besides, producers are using recycled PMMA more and more often owing to the reduction of their expenses on raw materials.

Manufacturing waste PMMA is gaining popularity due to the increased recovery and recycling of processing waste created during PMMA sheet, film, and component production. The growing emphasis on resource efficiency, waste reduction, and sustainable manufacturing techniques is driving global demand for PMMA recycling.

Installation Analysis

Mechanical recycling dominated the installation segment of the global PMMA recycling market, accounting for 71.3% of the total market share. The strong dominance of this segment is primarily driven by its cost-effectiveness, operational simplicity, and widespread commercial adoption across recycling facilities worldwide. The process involves collecting, sorting, cleaning, shredding, and reprocessing PMMA waste into reusable raw materials, making it highly efficient for large-scale recycling operations.

In addition, industries such as automotive, construction, electronics, and signage are increasingly utilizing mechanically recycled PMMA to reduce dependence on virgin plastics and support circular economy initiatives. Technological advancements in sorting and processing equipment are also improving recycling efficiency and enhancing the quality of recycled PMMA products.

Chemical recycling is gaining significant traction as it enables the recovery of high-purity monomers from PMMA waste, allowing manufacturers to produce recycled materials with properties similar to virgin PMMA. Rising advancements in depolymerization technologies and increasing demand for high-quality recycled acrylic materials are supporting segment growth.

Application Analysis

The automotive segment is the most widely used application.

The automotive sector emerged as the most prevalent application category in the worldwide PMMA Recycling Market, accounting for 31.3% of the market. The sector’s success can be due to the growing need for recycled PMMA in the manufacture of critical automotive components such as taillights, instrument panels, interior trimmings, windows, and advanced display systems.

As automakers around the world focus on building lighter, more fuel-efficient automobiles, recycled PMMA has become an increasingly appealing material alternative, providing the same excellent performance as virgin PMMA at a much lower cost and with less environmental impact. The Construction & Building category is fastest growing in the PMMA Recycling market, owing to the increasing usage of recycled PMMA in architectural panels, windows, skylights, and decorative components.

Rapid urbanization and large-scale infrastructure development in emerging markets continue to drive strong demand for this area. Meanwhile, the granules market is gaining traction, thanks to the increasing usage of PMMA in display screens, optical lenses, and light guides, where its optical clarity and durability make it a popular material choice.

Product Form Analysis

Granules Held a Major Share of the PMMA Recycling Market.

Granules were found to be the major product form category in the global PMMA recycling market, holding a market share of 45.2%. The significant dominance of the category is mainly credited to the extensive application of recycled PMMA granules as secondary raw material in various sectors, including automotive, construction, electronics, packaging, and consumer goods sectors.

The use of granules is highly favored by manufacturers owing to their easy handling, excellent storage capabilities, and high processability in various manufacturing methods like injection molding, extrusion, and compounding. Improvements in recycling technologies have also enhanced the performance properties of recycled PMMA granules, resulting in them being almost identical to virgin granules, thereby increasing their usage in high-performance industries.

The growing emphasis on sustainable manufacturing techniques and circular economy efforts is considerably fueling global demand for recycled PMMA granules. Manufacturers are progressively using recycled granules in their processes in order to minimize reliance on virgin plastics, lower manufacturing costs, and meet environmental sustainability goals.

Key Market Segments

By Source of PMMA

- Post‑consumer PMMA

- Post‑industrial PMMA

- Manufacturing waste PMMA

By Installation

- Mechanical recycling

- Chemical recycling

- Thermal recycling

By Application

- Automotive

- Electronics

- Construction & building

- Medical devices

- Consumer goods

By Product Form

- Sheets

- Granules

- Films

- Powders

Market Dynamics

Drivers

The Packaging and Packaging Waste Regulation (EU) 2025/40 (PPWR) entered into force on 11 February 2025 and applies market-wide from 12 August 2026, mandating all plastic packaging placed on the EU single market be designed for recyclability and stipulating post-consumer recycled (PCR) content minimums of 35% for non-contact-sensitive plastic packaging by 2030, escalating to 65% by 2040 thresholds that directly incentivize brand owners to procure rPMMA and rMMA at scale to avoid modulated EPR fee premiums.

In the UK, the Plastic Packaging Tax, now set at £223.69 per tonne, penalizes any plastic packaging containing less than 30% recycled content, while the UK EPR scheme, active from 2026, imposes the highest fee band on packaging not assessed through the Recyclability Assessment Methodology. In the United States,

California’s SB 54 mandates 100% recyclable or compostable single-use plastics by 2032 alongside a 65% recycling-rate target, and additional PCR mandates in New Jersey and Washington extend compliant rPMMA demand across an addressable US retail packaging market exceeding $50 billion.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening EPR & Mandatory Recycled Content Legislation | +2.4% | Europe (EU PPWR), UK, US State-Level (CA, NJ, WA) | Short term (≤ 2 years) |

| Depolymerization Technology Commercialization Reaching Industrial Scale | +2.1% | Europe, North America, Japan | Short term (≤ 2 years) |

| Automotive Lightweighting & EV Platform Expansion Driving EoL PMMA Recovery | +1.6% | Europe, China, South Korea | Medium term (2–4 years) |

| Carbon Footprint Reduction Mandates Elevating rMMA Procurement Priority | +1.2% | EU, Japan, North America | Short term (≤ 2 years) |

| Construction Sector Renovation Wave Generating Post-Consumer Acrylic Feedstock | +0.9% | Europe, India, Southeast Asia | Medium term (2–4 years) |

| Cross-Industry Strategic Alliances & Toll Manufacturing Networks Activating Collection Chains | +0.8% | Europe, North America | Short term (≤ 2 years) |

Restraints

China’s domestic MMA production capacity surged to approximately 2.655 million tonnes by end-2024, with an additional 305,000 tonnes of new capacity commissioned that year alone pushing the country from net importer to net exporter status, with exports reaching 300,000 tonnes in 2024, a 19.84% export-dependency ratio that has begun repricing the global spot market.

The East China annual average MMA price dropped by approximately 25.91% year-on-year in 2025, compressing the cost economics of rMMA producers who typically run depolymerization operating costs in the range of €200–350 per tonne for energy, catalyst, and logistics, a cost structure that only yields positive margin when virgin MMA prices hold above approximately €1,400–1,600 per tonne.

When virgin MMA trades near or below that threshold, off-takers in construction glazing, signage, and general PMMA compounding sectors, which account for approximately 57% of MMA downstream demand, have little financial incentive to pay the rMMA certification premium, directly freezing contract volumes and forcing rMMA producers to renegotiate take-or-pay offtake agreements at discounted rates.

This structural price suppression is not a temporary dislocation; the CR5 concentration ratio in Chinese MMA production fell from 60% in 2020 to 49% in 2024, indicating further fragmentation and ongoing capacity additions that will perpetuate oversupply unless sustained demand recovery from China’s real estate sector, currently constrained by regulatory deleveraging, absorbs the excess.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained Virgin MMA Price Depression Eroding Recycled MMA Price Premium | -2.2% | China, Global Spot Markets | Short term (≤ 2 years) |

| High Capital Intensity of Depolymerization Plant Build-Out Constraining New Entrants | -1.5% | Global, especially Emerging Markets | Medium term (2–4 years) |

| Absence of Standardized PMMA Waste Sorting & Certification Protocols | -1.0% | Global | Short term (≤ 2 years) |

| Lead-Based Thermal Depolymerization Legacy Infrastructure Limiting Feedstock Grades | -0.8% | Europe | Short term (≤ 2 years) |

| Restrictive Chemical Substance Regulations Limiting End-Use Approval for rMMA in Food-Contact & Medical Applications | -0.6% | EU, US (FDA) | Medium term (2–4 years) |

Challenges

Unlike commodity polymers such as PET or HDPE, which benefit from decades of established deposit-return and kerbside collection infrastructure post-consumer PMMA waste streams are inherently dispersed across heterogeneous end-use sectors: automotive lighting components (taillight assemblies averaging 3–5 kg PMMA per vehicle), architectural glazing panels, retail signage boards, and medical trays, none of which are captured by standard municipal sorting lines designed around packaging plastics.

The MMAtwo project, concluded under EU Horizon 2020 funding, identified the absence of coordinated collection logistics as the single largest operational bottleneck to scaling PMMA chemical recycling in Europe, noting that the continent’s existing PMMA recycling network is heavily reliant on industrial scrap rather than post-consumer streams, leaving the majority of the estimated 150,000–200,000 tonnes of annual European PMMA waste either landfilled or co-incinerated with mixed plastics at gate fees of €80–150 per tonne.

Röhm’s formation of a Europe-wide PMMA recycling alliance in December 2024 and the commissioning of its first industrial-scale depolymerization pilot at Worms designed for an initial throughput of approximately 5,000 tonnes per year represent a structural response to this constraint, but that figure represents less than 3% of European end-of-life PMMA generation, underscoring the scale gap.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Fragmented Post-Consumer PMMA Feedstock Collection | -1.8% | Global, especially Asia-Pacific & Emerging Markets | Medium term (2–4 years) |

| Mixed-Grade Contamination & Sorting Complexity | -1.3% | Global | Medium term (2–4 years) |

| High Specific Energy Demand in Thermal Depolymerization | -1.0% | Global (Energy-Cost-Sensitive Regions: South Asia, SE Asia) | Long term (≥ 4 years) |

| Skilled Technical Workforce Deficit in rMMA Processing | -0.7% | Global, especially India, Southeast Asia, Eastern Europe | Medium term (2–4 years) |

| Inconsistent Cross-Border Waste Export & Import Rules | -0.6% | EU-to-Asia Trade Corridors, Basel Convention Signatories | Long term (≥ 4 years) |

Opportunities

The opportunity remains commercially untapped because no automotive OEM has established a binding, closed-loop rMMA supply agreement covering full taillight assembly volumes. The closest precedents are Röhm’s K2025 prototype rear-lighting component containing 30% recycled PMMA, which has not entered volume production, and NEXTCHEM’s Worms pilot, designed to process 5,000 tonnes annually, equivalent to approximately 10 million car taillights. This remains a fraction of automotive PMMA demand, estimated at more than ¥8 billion, or approximately USD 1.1 billion, in China alone by 2025.

The structural opportunity is reinforced by the EU’s proposed ELV Regulation, which would require 25% of plastics in new vehicles to come from recycled sources, with 25% of that recycled content originating from end-of-life vehicles. Because compliance would be linked to EU type approval, OEMs would face a statutory procurement obligation, directly increasing the commercial value of certified rMMA and reducing current price-sensitivity barriers to adoption.

Under a closed-loop model, a major German automaker could contract a PMMA recycler to collect, depolymerize, and repolymerize taillight-grade material into certified rMMA. Recyclers could potentially charge a 15–25% premium over virgin MMA spot prices, supported by the OEM’s compliance value, while increasing estimated EBITDA margins from 8–12% to 18–22% at scale. The resulting TAM could reach at least 250,000–300,000 tonnes of automotive PMMA annually as recycled-content mandates expand across the EU, UK, and major Asian markets through 2030.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Closed-Loop Automotive Lighting PMMA Supply Contracts with Tier-1 OEMs | +2.6% | Europe, China, South Korea, US | Medium term (2–4 years) |

| Asia-Pacific Emerging Market Entry via Decentralized Micro-Depolymerization Units | +1.9% | India, Southeast Asia, South Korea | Medium term (2–4 years) |

| Low-Energy UV-Photocatalytic Recycling Technology Licensing | +1.4% | Global, pioneered in Europe (University of Bath, April 2026) | Long term (≥ 4 years) |

| Optical & Display-Grade rMMA Premium Segment Penetration | +1.1% | Japan, South Korea, China (display manufacturing hubs) | Long term (≥ 4 years) |

| Digital Product Passport & Chain-of-Custody Monetization for ESG-Compliant rMMA | +0.8% | EU (mandatory DPP under PPWR ecosystem by 2030), Global Brand Owners | Long term (≥ 4 years) |

| Bio-Based MMA Co-Processing Integration with Recycling Streams | +0.7% | Europe, North America, Japan | Long term (≥ 4 years) |

Geopolitical Impact Analysis

Global Regulations and Supply Chain Realignments Reshaping the PMMA Recycling Market.

Geopolitical events are progressively influencing the worldwide PMMA recycling market, primarily through changing environmental policies, trade rules, and supply chain restructuring activities. Governments in Europe, North America, and parts of Asia are tightening rules on plastic waste management, recycled content usage, and carbon emissions reduction, pushing the industry to increase investments in PMMA recycling infrastructure and sustainable material solutions.

Policies encouraging circular economy practices and limiting single-use plastics are increasing demand for recycled PMMA materials in the automotive, construction, and electronics industries. Geopolitical tensions, trade restrictions, and interruptions in global supply chains all have an impact on the availability and pricing of virgin petrochemical-based acrylic materials.

As businesses attempt to lessen their reliance on imported raw materials and improve supply chain resilience, recovered PMMA is becoming increasingly critical. Furthermore, increasing investments in domestic recycling capabilities and localized sustainable manufacturing ecosystems are likely to boost the global PMMA recycling market’s long-term growth prospects.

Regional Analysis

Asia Pacific Held the Largest Share of the Global PMMA Recycling Market.

In 2025, Asia Pacific dominated the global PMMA recycling market, with 40.3% of the overall market share. The region’s supremacy is fueled by fast industrialization, expanding plastics manufacturing operations, and increased demand for sustainable materials in China, India, Japan, and South Korea. Strong expansion in the automotive, electronics, construction, and consumer goods industries continues to drive up demand for recycled PMMA materials.

China is the largest contributor due to its enormous manufacturing base, expanding recycling infrastructure, and strong circular economy activities, while Japan and South Korea are developing chemical recycling technologies. Rising environmental legislation, urbanization, sustainable manufacturing practices, and investments in advanced recycling facilities are improving Asia Pacific’s position in the worldwide PMMA recycling market.

North America and Europe are important markets in the worldwide PMMA recycling business due to strict environmental legislation, increasing acceptance of sustainable plastics, and increased investment in advanced recycling technologies. Growing demand from the automotive, electronics, and construction industries continues to drive market expansion in both areas.

Latin America, the Middle East, and Africa are emerging markets fueled by rising industrialization, increased awareness of plastic waste management, and increased investments in recycling infrastructure and sustainable manufacturing methods.

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global PMMA recycling market has a competitive environment that is not too concentrated, with a mix of international chemical companies, specialty material makers, and recycling technology firms all trying to improve their position. Instead of just competing on price, top companies are focusing on innovation, sustainable practices, partnerships, and building more recycling facilities.

They understand that lasting success in this area depends on being able to provide high-quality, dependable recycled PMMA in large amounts. More companies, including Arkema, Mitsubishi Chemical Group, Röhm GmbH, Trinseo PLC, Chimei Corporation, and Sumitomo Chemical Co., Ltd., are investing in advanced recycling technologies, closed-loop systems, and the production of high-purity recycled PMMA. These efforts are being driven by rising demand from the automotive, construction, electronics, and consumer goods industries for reliable and sustainable acrylic materials.

At the same time, research and development is becoming a key area of competition. Companies are investing heavily to improve how well they break down PMMA, get more material from waste, and create recycled products that perform just like new materials. Outside the lab, the market is also changing through partnerships, mergers, and long-term agreements. These moves help companies expand globally, improve their circular economy efforts, and get reliable supplies and buyers to support growth in the PMMA recycling industry.

The Following are some of the Major Players in the Industry

- Röhm GmbH

- Trinseo S.A.

- Sumitomo Chemical Co., Ltd.

- SABIC

- Asahi Kasei Corporation

- Mitsub6ishi Chemical Group Corporation

- LX MMA

- CHIMEI Corporation

- Arkema S.A.

- Pekutherm Kunststoffe GmbH

- Polyvantis GmbH

- NEXTCHEM / MyRemono

- Lummus Technology

- Plastic Energy

- Solutions in Acrylics

- Others

Recent Development

- In April 2026, Röhm GmbH expanded its PMMA recycling initiatives by focusing on the development of high-quality recycled acrylic materials with properties comparable to virgin PMMA. The company strengthened its circular economy strategy through advanced depolymerization and material recovery technologies aimed at improving transparency, durability, and performance characteristics of recycled PMMA.

- In February 2024, Arkema increased investments in sustainable acrylic solutions and recycling technologies to strengthen circular economy initiatives and expand the adoption of recycled PMMA materials across various end-use industries.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 1.4 Billion |

| Forecast Revenue (2035) | USD 2.8 Billion |

| CAGR (2026-2035) | 7.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Source of PMMA (Post-consumer PMMA, Post-industrial PMMA, and Manufacturing Waste PMMA), By Installation (Mechanical Recycling, Chemical Recycling, and Thermal Recycling), By Application (Automotive, Electronics, Construction & Building, Medical Devices, Consumer Goods, and Others), By Product Form (Sheets, Granules, Films, and Powders) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Röhm GmbH, Trinseo S.A., Sumitomo Chemical Co., Ltd., SABIC, Asahi Kasei Corporation, Mitsubishi Chemical Group Corporation, LX MMA, CHIMEI Corporation, Arkema S.A., Pekutherm Kunststoffe GmbH, Polyvantis GmbH, NEXTCHEM / MyRemono, Lummus Technology, Plastic Energy, Solutions in Acrylics, and Other Players. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |