Global Phytogenic Feed Additives Market By Animal (Poultry, Ruminants, Swine and Others), By Application (Antimicrobial Effect, Growth Promotion, Digestion Enhancement, AGP Replacement and Others), By Distribution Channel (Animal Production Operations, Retail, Research/Academic Institutions and E-commerce), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Feb 2026

- Report ID: 176996

- Number of Pages: 275

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

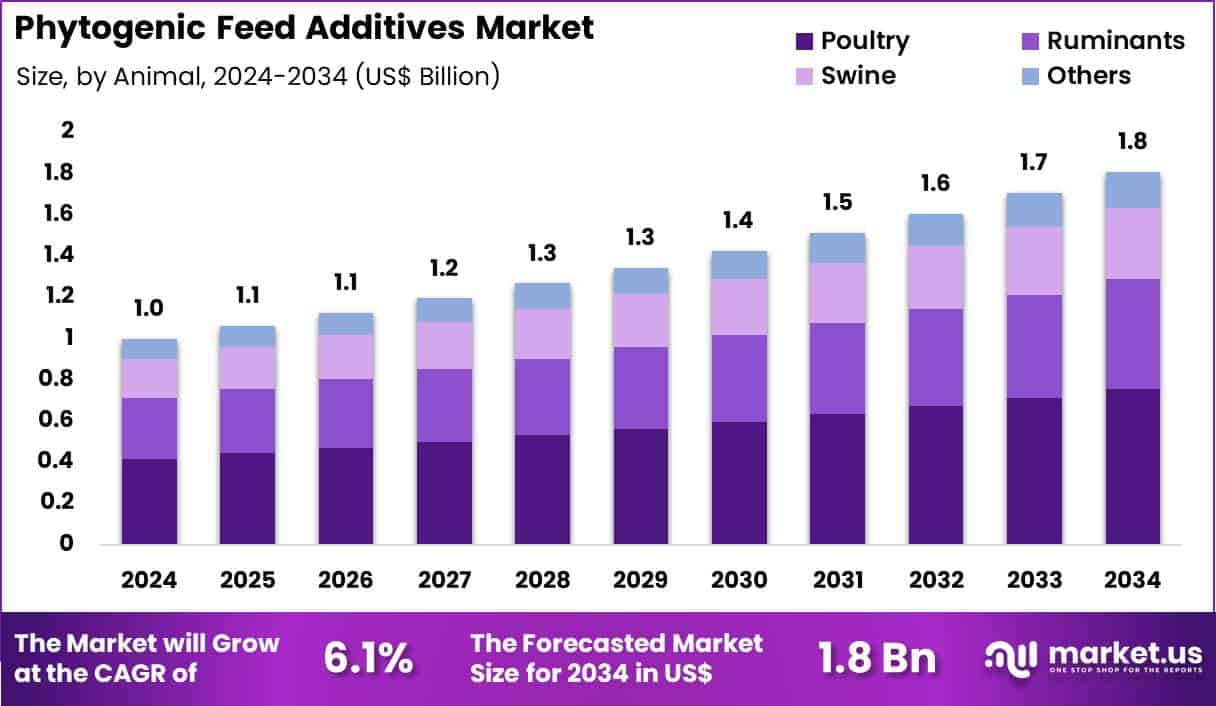

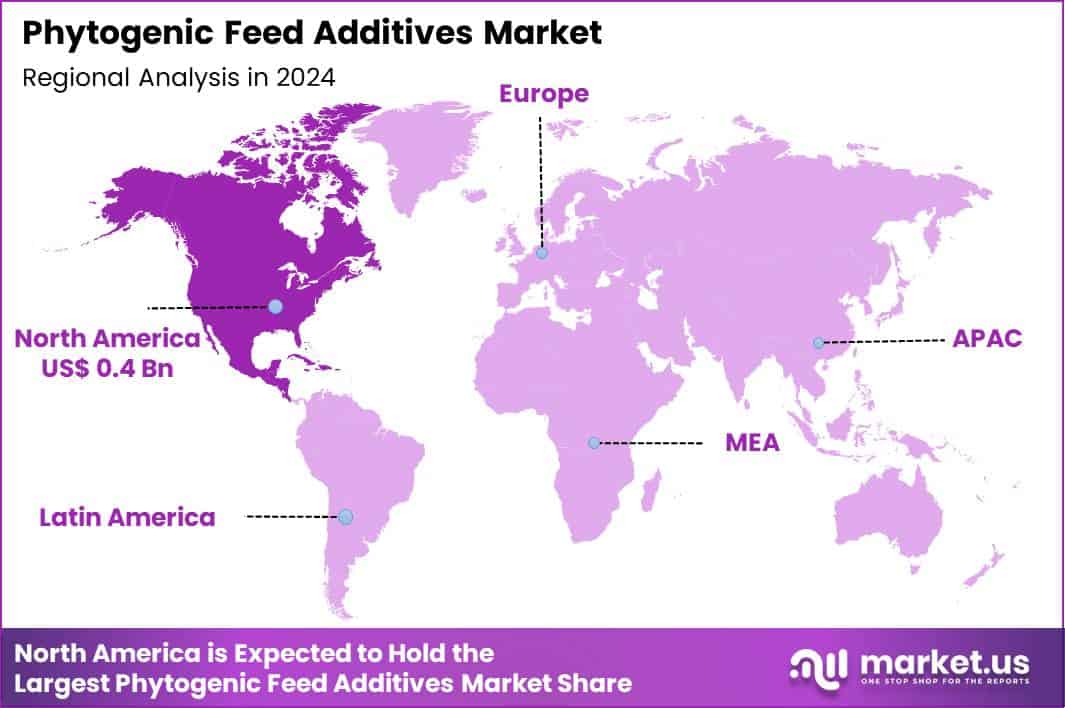

Global Phytogenic Feed Additives Market size is expected to be worth around US$ 1.8 Billion by 2034 from US$ 1.0 Billion in 2024, growing at a CAGR of 6.1% during the forecast period 2025 to 2034. In 2024, North America led the market, achieving over 38.8% share with a revenue of US$ 0.4 Billion.

Increasing consumer demand for antibiotic-free animal products accelerates the phytogenic feed additives market as livestock producers seek natural alternatives that enhance animal health and performance without synthetic residues.

Poultry farmers increasingly incorporate essential oils from thyme and oregano into feeds to boost immune responses and reduce pathogen loads, improving weight gain and feed conversion ratios in broiler chickens. These additives support swine nutrition by blending cinnamon and garlic extracts to promote gut microbiota balance, alleviating diarrhea in piglets and enhancing overall herd productivity.

Aquaculture operators apply phytogenics like ginger and turmeric in fish feeds to strengthen antioxidant defenses and disease resistance, sustaining growth in salmon and tilapia farming. Dairy producers utilize these compounds in cattle rations to optimize rumen fermentation, elevating milk yield and quality while minimizing methane emissions.

Companion animal feed manufacturers integrate herbal blends into pet foods, addressing digestive issues and coat health in dogs and cats through sustained supplementation. Feed additive companies pursue opportunities to formulate multi-herb synergies that target specific livestock challenges, expanding applications in organic farming where regulatory restrictions favor plant-derived solutions.

Developers advance microencapsulation technologies that protect active phytogenic compounds from degradation, broadening utility in high-temperature pelleting processes for poultry and swine feeds. These innovations facilitate customized blends for emerging aquaculture species, optimizing omega-3 profiles and survival rates.

Opportunities emerge in sustainable sourcing of botanicals that align with eco-friendly practices, appealing to producers focused on carbon footprint reduction. Manufacturers invest in evidence-based trials that validate efficacy, building trust for novel applications in equine and exotic animal nutrition.

Recent trends emphasize precision delivery systems and microbiome-modulating formulations, positioning phytogenic additives as integral to resilient, antibiotic-reduced animal husbandry models.

Key Takeaways

- In 2024, the market generated a revenue of US$ 1.0 Billion, with a CAGR of 6.1%, and is expected to reach US$ 1.8 Billion by the year 2034.

- The animal segment is divided into poultry, ruminants, swine and others, with poultry taking the lead with a market share of 41.8%.

- Considering application, the market is divided into antimicrobial effect, growth promotion, digestion enhancement, AGP replacement and others. Among these, antimicrobial effect held a significant share of 36.7%.

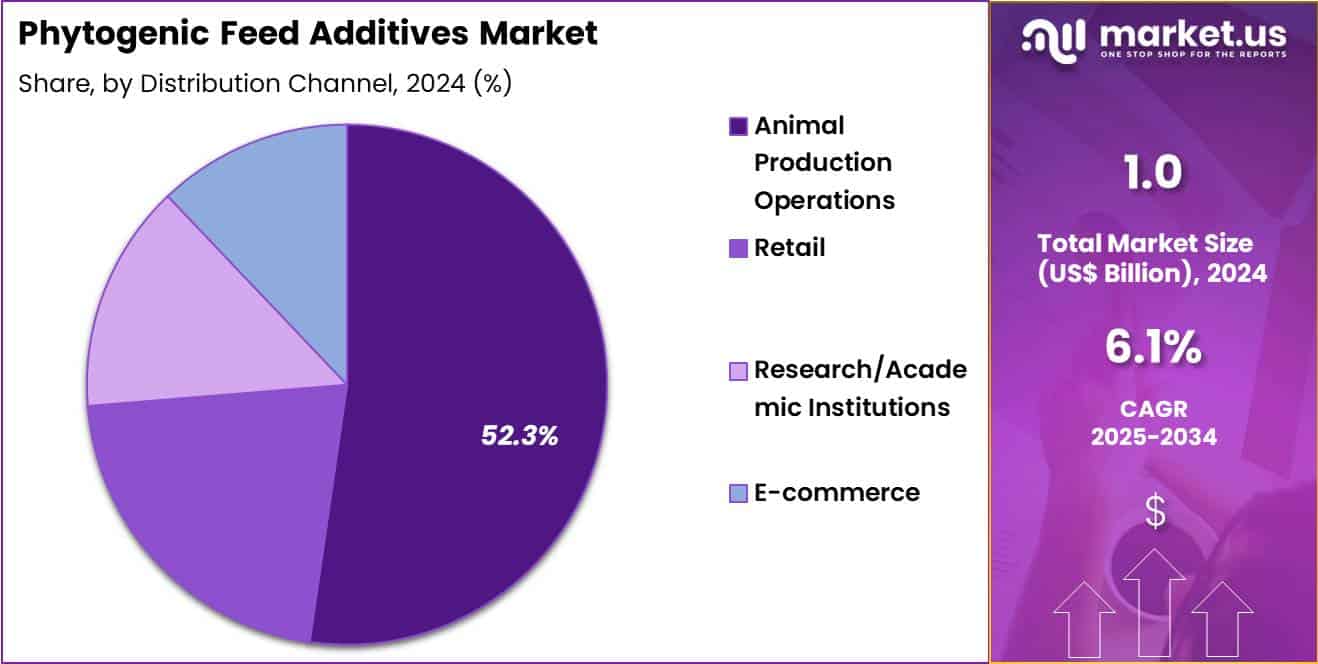

- Furthermore, concerning the distribution channel segment, the market is segregated into animal production operations, retail, research/academic institutions and e-commerce. The animal production operations sector stands out as the dominant player, holding the largest revenue share of 52.3% in the market.

- North America led the market by securing a market share of 38.8%.

Animal Analysis

Poultry contributed 41.8% of growth within animal and led the phytogenic feed additives market due to high production intensity and strong disease management needs in commercial poultry farming. Poultry producers prioritize phytogenic additives to support gut health, immunity, and feed efficiency under high-density rearing conditions.

Short production cycles amplify the impact of feed performance improvements, which encourages rapid adoption. Rising global demand for poultry meat and eggs increases flock sizes, strengthening additive consumption across feed formulations.

Growth strengthens as antibiotic use restrictions intensify across regions, pushing producers toward plant-based alternatives. Phytogenic solutions help stabilize gut microbiota and reduce pathogen load, which improves flock uniformity.

Integrators favor poultry-specific blends to maintain productivity without antibiotics. Cost-effective dosing and fast measurable outcomes reinforce uptake. The segment is expected to remain dominant as poultry continues to represent the most industrialized and fast-scaling animal protein sector.

Application Analysis

Antimicrobial effect generated 36.7% of growth within application and emerged as the leading segment due to rising pressure to control pathogenic bacteria without antibiotics. Livestock producers adopt phytogenic additives to suppress harmful microbes while preserving beneficial gut flora.

This function supports disease prevention and lowers mortality risk across intensive farming systems. Regulatory scrutiny on antimicrobial resistance accelerates demand for non-antibiotic solutions that maintain animal health.

Growth accelerates as producers integrate phytogenics into preventive health strategies rather than reactive treatment. Essential oils and plant extracts demonstrate consistent antimicrobial activity under commercial conditions.

Feed manufacturers promote these additives as clean-label solutions aligned with consumer expectations. Reduced reliance on medicated feeds strengthens long-term adoption. The segment is anticipated to sustain leadership as antimicrobial stewardship remains a priority across animal agriculture.

Distribution Channel Analysis

Animal production operations accounted for 52.3% of growth within distribution channel and dominated the phytogenic feed additives market due to direct bulk procurement by large-scale producers. Integrated operations prefer sourcing additives directly to maintain formulation control and cost efficiency.

High-volume feed manufacturing at production sites increases steady consumption of phytogenic inputs. Long-term supply agreements further stabilize demand through this channel.

Growth continues as vertical integration expands across poultry and livestock industries. Producers seek consistent additive quality to support standardized feeding programs. Direct technical support from suppliers strengthens operational confidence. Reduced dependency on intermediaries improves margin control. The segment is projected to remain the primary growth driver as industrial animal production continues to scale globally.

Key Market Segments

By Animal

- Poultry

- Ruminants

- Swine

- Others

By Application

- Antimicrobial Effect

- Growth Promotion

- Digestion Enhancement

- AGP Replacement

- Others

By Distribution Channel

- Animal Production Operations

- Retail

- Research/Academic Institutions

- E-commerce

Drivers

Increasing demand for natural alternatives to antibiotics is driving the market.

The worldwide push for antibiotic-free livestock production has markedly boosted the adoption of phytogenic feed additives as safe, plant-based substitutes to enhance animal health and performance. Regulatory restrictions on antibiotic growth promoters have accelerated this shift, encouraging farmers to seek effective natural options for disease prevention and growth promotion.

Phytogenic additives, derived from herbs, spices, and essential oils, offer antimicrobial and digestive benefits without contributing to resistance development. According to the U.S. Food and Drug Administration, in 2023, the transition of over-the-counter medically important antimicrobials to prescription status for animals came into full effect, prompting greater reliance on alternatives like phytogenics.

This policy change has directly influenced feed formulation practices in the U.S., a major livestock producer, fostering market growth for phytogenic products. Key players are responding by expanding their portfolios to meet the rising need for sustainable feed solutions in poultry, swine, and ruminant farming.

The correlation between consumer preferences for clean-label animal products and the use of natural additives further propels industry expansion. Government organizations in various regions promote these alternatives through guidelines on animal welfare and food safety.

Overall, this driver supports long-term market sustainability by aligning with global health priorities. The trend underscores the role of phytogenics in reducing environmental impacts associated with traditional feed practices.

Restraints

High production costs of phytogenic additives is restraining the market.

The elevated expenses involved in sourcing and processing plant-based materials for phytogenic feed additives limit their competitiveness against synthetic options in price-sensitive markets. Extraction methods for essential oils and bioactive compounds require specialized equipment, contributing to higher manufacturing overheads for producers.

Small-scale farmers often hesitate to adopt these additives due to the added cost burden on feed budgets. Quality control to ensure consistent potency in natural extracts adds further financial strain on supply chains. In regions with fluctuating raw material prices, such as herbs and spices, market volatility hinders stable pricing strategies.

Providers may prioritize conventional additives to maintain profitability in low-margin livestock operations. This restraint affects adoption rates, particularly in developing economies with limited subsidies for natural products.

Industry collaborations aim to optimize production techniques to reduce costs over time. Despite health benefits, economic factors impede broader integration into standard feed formulations. Addressing supply chain efficiencies is key to mitigating this market limitation.

Opportunities

Expansion into Asia-Pacific livestock sectors is creating growth opportunities.

The rapid growth in livestock production in Asia-Pacific countries provides substantial prospects for phytogenic feed additives to improve feed efficiency and animal health in expanding farms. Governmental investments in agriculture support the introduction of natural additives to meet rising demand for meat and dairy products.

Increasing export requirements for antibiotic-free animal products encourage the use of phytogenics in regional supply chains. Partnerships with local feed mills facilitate compliance and distribution for international suppliers. The large swine and poultry populations in the region amplify the potential for additive applications in disease management.

Training programs for farmers promote the benefits of natural feed solutions in high-density farming systems. This opportunity enables global firms to tap into high-growth markets beyond established regions. Key corporations are establishing operations to leverage lower production costs and proximity to raw materials.

Overall, Asia-Pacific expansions align with efforts to enhance food security in populous areas. Strategic initiatives can establish significant footholds in these vibrant agricultural landscapes.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions influence the phytogenic feed additives market through farm profitability, feed cost inflation, and purchasing discipline across livestock producers. Inflation and higher interest rates increase pressure on feed margins, which makes buyers more selective about additive inclusion and dosage levels.

Geopolitical tensions disrupt supplies of herbs, spices, essential oils, and botanical extracts, raising sourcing volatility and freight costs. Current US tariffs on imported plant based ingredients and processed extracts lift input costs for manufacturers, which tightens margins and affects pricing negotiations with feed mills. These factors challenge smaller producers and slow adoption in highly price sensitive markets.

On the positive side, trade pressure encourages local cultivation, regional extraction, and stronger supply traceability. Regulatory pressure to reduce antibiotic use and demand for natural performance enhancers continue to support adoption. With disciplined sourcing, formulation efficiency, and strong animal health fundamentals, the market remains positioned for steady and sustainable growth.

Latest Trends

Development of encapsulated phytogenic formulations is a recent trend in the market.

In 2024, the advancement of encapsulation technologies for phytogenic feed additives has improved stability and targeted delivery in animal digestive systems. These formulations protect bioactive compounds from degradation during feed processing and storage.

Manufacturers have emphasized controlled release mechanisms to maximize efficacy in poultry and swine nutrition. Clinical studies highlighted enhanced bioavailability for essential oils in encapsulated forms. Cargill launched a new phytogenic feed additive for poultry in the first quarter of 2024, incorporating encapsulation to boost performance. This innovation addresses challenges in heat-sensitive compounds under varying environmental conditions.

The trend focuses on sustainability by reducing dosage requirements without loss of effectiveness. Regulatory reviews in 2024 confirmed safety for these advanced products in global markets. Industry alliances refine coating materials for better palatability and animal acceptance. These developments aim to optimize outcomes in antibiotic-restricted farming practices.

Regional Analysis

North America is leading the Phytogenic Feed Additives Market

North America holds a 38.8% share of the global Phytogenic Feed Additives market, achieving notable expansion in 2024 as livestock producers increasingly substitute antibiotic growth promoters with plant-derived alternatives to comply with stricter regulations and meet consumer preferences for antibiotic-free animal products.

Companies such as Cargill and ADM have developed specialized blends incorporating essential oils from herbs like oregano and thyme, which enhance gut health and feed efficiency in poultry and swine operations facing disease pressures. The region’s large-scale farming operations have adopted these additives to improve animal performance amid rising feed costs, particularly in the U.S. where dairy and beef sectors prioritize sustainable practices.

Governmental oversight through the FDA has enforced reductions in antimicrobial use, prompting a transition to phytogenics for maintaining productivity in intensive systems. An upsurge in meat consumption has necessitated reliable additives that support faster growth rates without synthetic residues.

Joint ventures between feed mills and botanical suppliers have refined formulations for better palatability and bioavailability in diverse climates. Furthermore, educational programs from agricultural extensions have informed farmers about phytogenic benefits in reducing environmental impacts from manure.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Experts project substantial momentum in the botanical animal nutrition field across Asia Pacific over the forecast period, since authorities intensify subsidies for sustainable farming to elevate livestock yields amid urbanization strains.

Enterprises in China and India formulate herb-infused compounds that bolster immunity in aquaculture species, while veterinarians in Vietnam advocate thyme-based mixes to curb digestive issues in swine herds. Producers in Indonesia harness local spice extracts to amplify feed conversion ratios, targeting export markets with stringent residue limits.

Investors in the Philippines direct capital toward R&D for cinnamon-derived enhancers that mitigate heat stress in broilers during monsoons. Regulators in Thailand mandate trials demonstrating efficacy of garlic supplements against pathogens, fostering industry-wide standardization.

Specialists in Malaysia deploy oregano oil variants to optimize rumen function in dairy cattle, enhancing milk quality for regional trade. Manufacturers in Australia refine eucalyptus integrations for sheep nutrition, adapting to arid conditions that challenge conventional feeds. Alltech’s 2024 Agri-Food Outlook reveals that feed production in the region rose by 1.4% to 475.33 million metric tons in 2023, underscoring escalating demands for natural enhancers.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key competitors in the phytogenic feed additives market grow by enhancing botanical formulations with targeted functional benefits such as improved digestion, immune support, and feed efficiency that resonate with livestock producers seeking antibiotic-free solutions. They also invest in robust research partnerships with universities and animal nutrition institutes to validate efficacy and differentiate offerings in a crowded ingredient landscape.

Firms expand distribution networks through global feed ingredient suppliers and regional animal health partners to capture demand across poultry, swine, and ruminant segments. Strategic acquisitions help some players integrate complementary technologies and accelerate entry into emerging markets in Asia Pacific and Latin America.

Adisseo exemplifies a major animal nutrition company with a diversified additive portfolio, strong global footprint, and deep expertise in innovation that supports productivity and sustainability goals for feed formulators. The company advances performance through disciplined R&D investment, coordinated commercialization strategies, and close engagement with end users to align product development with evolving industry priorities.

Top Key Players

- Delacon Biotechnik

- BIOMIN

- Cargill

- DSM

- BASF

- Kemin Industries

- Adisseo

- Synthite Industries

- Phytobiotics

- Pancosma

Recent Developments

- In January 2025, EW Nutrition strengthened its global animal nutrition expertise by appointing two new professionals, Nadia Yacoubi and Marie Galissot, at its headquarters in Germany. The appointments support leadership across key functions, with responsibilities covering Phytogenic Products management and Feed Quality Solutions category oversight.

- In February 2024, Cargill announced the formation of Micronutrition and Health Solutions within its Animal Nutrition and Health division. The newly established unit focuses on delivering targeted nutritional and health-oriented feeding solutions tailored to animal production needs.

Report Scope

Report Features Description Market Value (2024) US$ 1.0 Billion Forecast Revenue (2034) US$ 1.8 Billion CAGR (2025-2034) 6.1% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Animal (Poultry, Ruminants, Swine and Others), By Application (Antimicrobial Effect, Growth Promotion, Digestion Enhancement, AGP Replacement and Others), By Distribution Channel (Animal Production Operations, Retail, Research/Academic Institutions and E-commerce) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Delacon Biotechnik, BIOMIN, Cargill, DSM, BASF, Kemin Industries, Adisseo, Synthite Industries, Phytobiotics, Pancosma Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Phytogenic Feed Additives MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample

Phytogenic Feed Additives MarketPublished date: Feb 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Delacon Biotechnik

- BIOMIN

- Cargill

- DSM

- BASF

- Kemin Industries

- Adisseo

- Synthite Industries

- Phytobiotics

- Pancosma

Our Clients

- 176996

- Feb 2026