Global Perfumery Glass Bottle Market Size, Share, Growth Analysis By Form (Translucent, Transparent, Opaque), By Capacity (0–50 ml, 50–150 ml, >150 ml), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 182299

- Number of Pages: 334

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

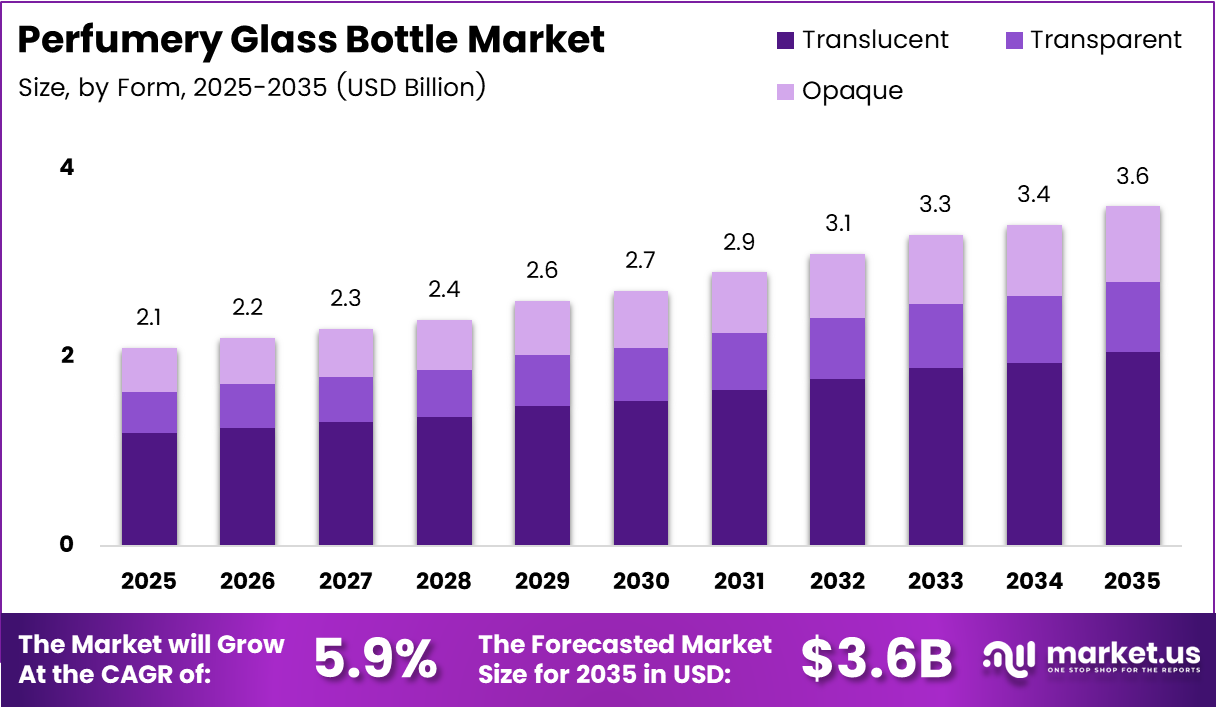

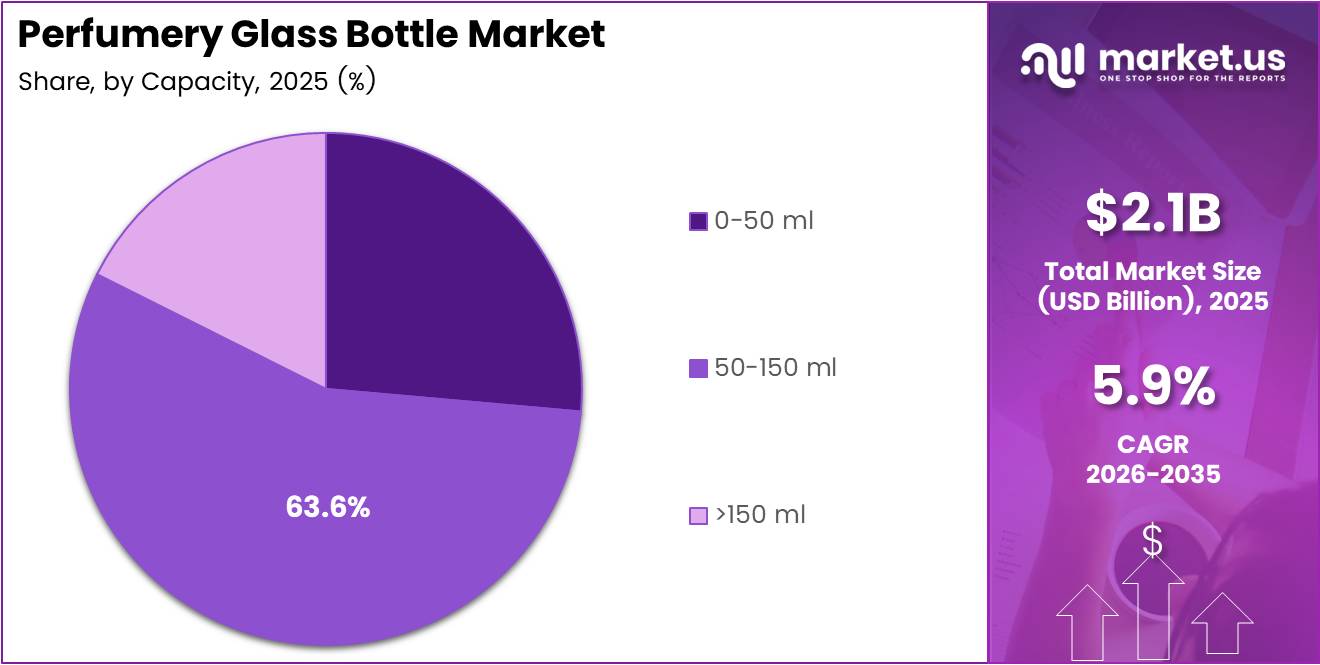

Global Perfumery Glass Bottle Market size is expected to be worth around USD 3.6 Billion by 2035 from USD 2.1 Billion in 2025, growing at a CAGR of 5.9% during the forecast period 2026 to 2035.

The perfumery glass bottle market covers decorative and functional glass containers designed specifically for fragrance and luxury perfume packaging. These vessels serve dual roles — protecting the fragrance formulation while acting as a brand statement on retail shelves. Manufacturers produce them in translucent, transparent, and opaque forms, spanning capacities from small 0-50 ml atomizers to large 150 ml-plus collector formats.

Premium and luxury fragrance brands treat glass bottle design as a core brand asset, not just packaging. The shift from commodity containers to highly customized designer bottles reflects a structural change in buyer behavior. Fragrance houses now commission bespoke glass designs to differentiate products in a crowded prestige retail environment, creating sustained demand for specialized glass manufacturers.

Sustainability has become a commercial differentiator in this market. Consumer preference for recyclable packaging has moved from a niche position to a procurement requirement, particularly among European luxury groups. Glass holds a structural advantage over plastic because it is infinitely recyclable without material degradation — a property that aligns directly with brand sustainability commitments across the fragrance industry.

The expansion of indie and artisanal perfume houses adds a new demand layer that established glass bottle suppliers were not historically designed to serve. Small-batch, custom orders require flexible manufacturing capabilities, creating an opening for mid-size glass producers. In March 2025, PGP Glass commissioned a new 120-tonne-per-day furnace at its Kosamba facility specifically for cosmetics and perfumery glass production — a direct operational response to this supply-demand gap.

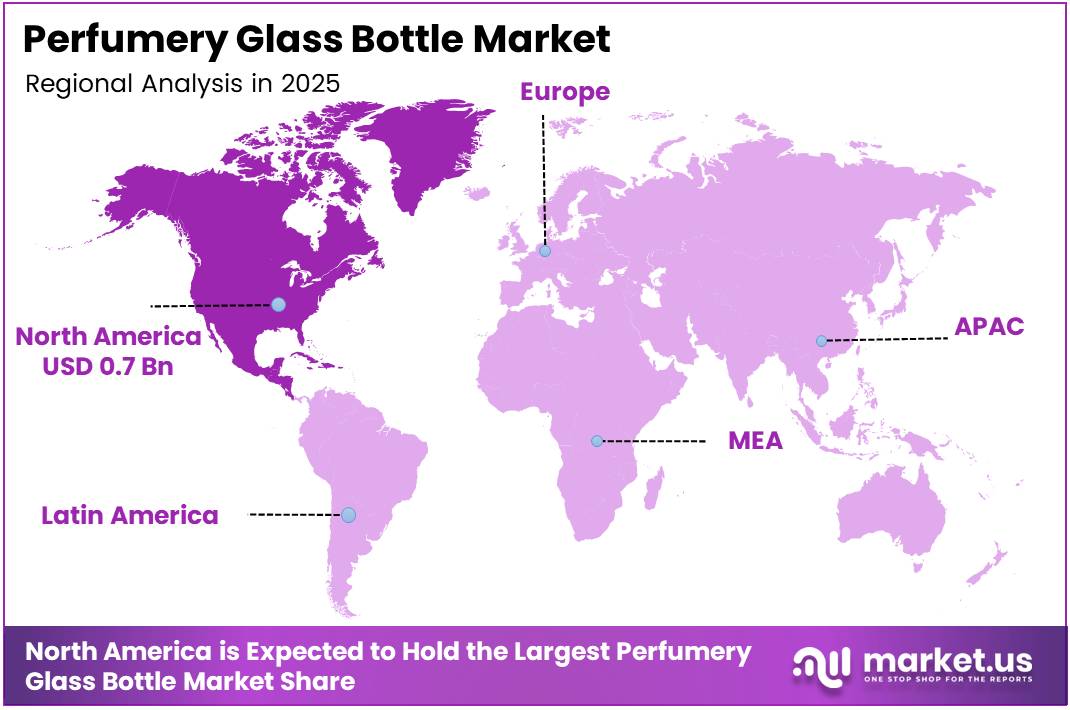

North America leads the global market with a 38.6% share valued at USD 0.7 Billion. This position reflects the concentration of major fragrance distribution infrastructure, mature specialty retail channels, and established procurement relationships between US fragrance brands and premium glass suppliers.

According to Verescence Sustainability Report 2024-2025, the company achieved an On Time In Full (OTIF) delivery rate of 95.6% — a 4-point increase — for glass bottle orders including perfumery lines. This operational benchmark signals that leading manufacturers are competing on supply reliability, not just design capability, which raises the baseline expectation for all suppliers serving luxury fragrance accounts.

According to a study published on PMC, Narrow-neck press-and-blow (NNPB) technology enables lightweighting of up to 30–35% for soda-lime container glass used in perfumery bottles while maintaining structural integrity. Lighter bottles reduce transportation costs and lower the carbon footprint per unit — two factors that are now actively evaluated in procurement decisions by major fragrance groups with published sustainability targets.

Key Takeaways

- The global Perfumery Glass Bottle Market is valued at USD 2.1 Billion in 2025 and is forecast to reach USD 3.6 Billion by 2035.

- The market grows at a CAGR of 5.9% during the forecast period 2026 to 2035.

- By Form, Translucent bottles dominate with a 56.9% market share in 2025.

- By Capacity, the 50–150 ml segment leads with a 63.6% share, reflecting the standard retail fragrance bottle size.

- North America holds the largest regional share at 38.6%, valued at USD 0.7 Billion.

Product Analysis

Translucent dominates with 56.9% due to luxury brand visibility and shelf appeal.

In 2025, Translucent held a dominant market position in the By Form segment of the Perfumery Glass Bottle Market, with a 56.9% share. Luxury and premium fragrance brands prefer translucent glass because it allows consumers to see the fragrance liquid, which functions as a visual quality cue at point of sale. This form supports brand storytelling without fully concealing the product, which is a deliberate positioning choice among prestige fragrance houses.

Transparent glass serves brands that prioritize full product visibility as part of their aesthetic identity. Transparent perfumery containers work especially well for light-toned or vividly colored fragrance liquids, where the liquid itself becomes part of the visual design. However, transparent formats occupy a smaller share because they limit design layering options that luxury brands frequently deploy to command premium shelf positioning.

Opaque glass differentiates through complete concealment of the fragrance formulation, allowing bottle form and surface treatment to carry the entire brand message. This format suits limited-edition and artisanal launches where the bottle object itself is the primary consumer experience. Opaque finishes — particularly frosted and matte textures — have seen growing application in niche perfume houses targeting collectors and design-conscious buyers.

Capacity Analysis

50–150 ml dominates with 63.6% due to alignment with standard retail fragrance sizing.

In 2025, the 50–150 ml segment held a dominant market position in the By Capacity segment of the Perfumery Glass Bottle Market, with a 63.6% share. This size range matches the volume standards that mainstream and premium fragrance brands use for their core retail SKUs globally. Fragrance brands default to this range because it balances product longevity, price point, and shelf footprint — factors that drive repeat purchase and retail placement decisions simultaneously.

The 0–50 ml capacity segment serves two structurally different buyer groups: discovery-format samplers sold by niche fragrance houses, and travel-size editions offered by luxury brands as entry-level or gift products. This segment benefits from the expansion of indie perfume brands, which use small-format bottles to lower consumer trial barriers. The economics favor glass manufacturers with flexible small-batch production capability over high-volume commodity producers.

The above 150 ml capacity segment targets collectors, fragrance enthusiasts, and luxury gifting channels where bottle size reinforces perceived value. These larger glass containers typically carry higher per-unit fabrication costs and more complex decoration specifications. Brands using this format treat the bottle as a display object, not just a delivery vessel — a positioning that supports premium pricing and creates a distinct product tier within fragrance retail.

Key Market Segments

By Form

- Translucent

- Transparent

- Opaque

By Capacity

- 0–50 ml

- 50–150 ml

- >150 ml

Drivers

Premium Fragrance Brand Expansion and Sustainability Mandates Accelerate Demand for Specialized Glass Bottles

Global luxury and premium fragrance brands treat glass bottle design as a primary brand asset. The expansion of international fragrance houses and niche perfume labels has created sustained demand for customized designer glass containers. These brands reject generic packaging because bottle form and aesthetic directly influence consumer perception of quality and pricing power at prestige retail.

Sustainability requirements now shape procurement decisions at major fragrance groups. Consumer preference for recyclable packaging has pushed glass ahead of plastic alternatives for luxury applications. Glass carries a structural recyclability advantage that plastic cannot match, which aligns with published environmental commitments from leading beauty conglomerates. According to a study published on PMC, hybrid-electric and oxy-fuel furnaces achieve 25–30% reductions in combustion-related emissions for container glass production — giving glass suppliers a credible sustainability argument to fragrance brand buyers with carbon reduction targets.

Shelf appeal and aesthetic differentiation also function as commercial drivers. Fragrance retail depends heavily on visual impact, and glass uniquely enables frosted, colored, and textured surface treatments that plastic cannot replicate. In March 2025, PGP Glass commissioned a new 120-tonne-per-day furnace at its Kosamba facility — a direct capacity investment signaling that glass producers see durable, structural procurement commitments from fragrance clients rather than cyclical demand.

Restraints

Fragility, High Production Costs, and E-commerce Logistics Challenges Limit Glass Bottle Adoption in Cost-Sensitive Channels

Glass perfume bottles carry significantly higher production and transportation costs compared to plastic alternatives. The raw material and energy intensity of glass manufacturing, combined with specialized decorating and finishing processes required for luxury applications, results in a per-unit cost structure that narrows adoption among value-positioned fragrance brands. Smaller fragrance producers operating on thin margins face direct pressure to evaluate lighter, cheaper packaging formats.

Breakage risk creates a specific and material barrier in e-commerce distribution. Unlike brick-and-mortar retail where handling is controlled, direct-to-consumer fragrance shipping exposes glass bottles to high-impact transit conditions. Returns from breakage damage brand reputation, increase per-order cost, and complicate logistics infrastructure for fragrance brands that are scaling online channels. This constraint is not theoretical — it directly affects packaging decisions for fragrance brands building DTC operations.

The combination of weight, fragility, and specialized packaging requirements means that glass bottle producers serving e-commerce fragrance clients must invest in protective secondary packaging systems. This adds cost at the brand level and reduces the cost-efficiency advantage that glass might otherwise offer through recyclability. Together, these logistics constraints create a ceiling on glass adoption outside traditional retail-led fragrance distribution.

Growth Factors

Refillable Formats, Lightweight Technology, and Emerging Market Expansion Create New Revenue Streams for Glass Bottle Producers

Refillable perfume packaging systems represent a structurally new revenue model for glass bottle manufacturers. Luxury fragrance brands adopting refill formats commit to longer product lifespans, which requires bottles engineered for repeated use rather than single application. This shift creates demand for higher-durability glass specifications and changes the procurement cycle — brands purchase fewer but more premium bottles, raising the average selling price per unit for glass manufacturers.

Lightweighting technology addresses both the cost and sustainability objections that have historically slowed glass adoption in some market segments. According to a study published on PMC, each additional 10% cullet content in soda-lime glass reduces furnace energy demand by approximately 3% and CO₂ emissions by approximately 5%. This relationship makes cullet-intensive production economically and environmentally efficient simultaneously — a rare alignment that enables glass producers to offer premium sustainable credentials without a cost premium to fragrance brand buyers.

Emerging economies across Asia, the Middle East, and Latin America present a geographic expansion path as luxury fragrance consumption broadens beyond established Western markets. New luxury consumers in these regions enter the category through aspirational purchases that mirror the aesthetic standards of European prestige brands. This behavior sustains demand for premium glass bottle designs rather than triggering a substitution toward cheaper packaging formats, which protects the value positioning of specialist glass manufacturers.

Emerging Trends

Smart Packaging, Collectible Bottle Design, and Advanced Glass Finishes Redefine the Competitive Basis in Fragrance Packaging

Luxury fragrance brands are integrating NFC tags and QR codes directly into glass bottle designs to create connected consumer experiences. This convergence of physical packaging with digital functionality extends brand engagement beyond the point of purchase. For glass bottle manufacturers, it introduces a new technical specification layer — embedding smart elements without compromising the structural integrity or aesthetic premium of the bottle itself.

Limited-edition designer perfume bottles have repositioned the glass container as a collectible luxury object, not just a product delivery format. Brands releasing numbered or artist-collaboration bottles generate secondary market demand and press coverage that extends marketing ROI beyond the retail transaction. According to Verescence Sustainability Report 2024-2025, the company recycled 98% of water used in glass bottle manufacturing operations — demonstrating that high-aesthetic luxury production and operational sustainability are not mutually exclusive, which strengthens the commercial case for glass in premium brand packaging decisions.

Frosted, colored, and textured glass finishes have moved from niche application to mainstream brand tool across prestige fragrance. These surface treatments allow brands to create visual differentiation without changing bottle form, reducing tooling costs while maintaining shelf distinctiveness. In September–December 2025, PGP Glass showcased sustainability innovations and advanced lightweight glass variants at Cosmoprof 2025, signaling that technical surface and weight innovations are now a primary competitive arena for glass bottle suppliers.

Regional Analysis

North America Dominates the Perfumery Glass Bottle Market with a Market Share of 38.6%, Valued at USD 0.7 Billion

North America holds a 38.6% share of the global perfumery glass bottle market, valued at USD 0.7 Billion in 2025. This position reflects the concentration of major fragrance brand headquarters, mature specialty retail infrastructure, and established procurement relationships between US-based fragrance groups and premium glass suppliers. These structural conditions create a self-reinforcing demand base that competitor regions have not yet replicated at scale.

Europe Perfumery Glass Bottle Market Trends

Europe holds a strategically important position in this market as the historic home of prestige fragrance — French and Italian luxury houses anchor global demand for premium glass bottle design. The region’s strict packaging recyclability regulations push brand owners toward glass over plastic alternatives, creating a compliance-driven tailwind for glass container producers. European glass manufacturers also benefit from proximity to the continent’s largest fragrance brand clients.

Asia Pacific Perfumery Glass Bottle Market Trends

Asia Pacific represents the fastest-expanding geographic opportunity for perfumery glass bottle producers. China, South Korea, and Japan host both domestic luxury fragrance consumption and large-scale glass manufacturing capacity. Rising disposable incomes and shifting consumer preferences toward premium fragrance categories in China and Southeast Asia are steadily expanding the addressable buyer base for premium glass perfume containers.

Middle East and Africa Perfumery Glass Bottle Market Trends

The Middle East carries disproportionate importance in the perfumery glass bottle market relative to its population size. The Gulf region maintains a deep cultural tradition of high-frequency, high-volume fragrance use — oud and concentrated perfume formats typically use larger, ornate glass bottles that command premium pricing. GCC consumers and regional fragrance houses create consistent demand for decorative, high-specification glass containers.

Latin America Perfumery Glass Bottle Market Trends

Latin America represents an emerging opportunity tier for perfumery glass bottle suppliers. Brazil and Mexico anchor regional demand, supported by growing fragrance retail penetration and a rising consumer preference for premium product formats. However, high import duties on specialty glass and fragmented local distribution infrastructure continue to constrain the pace at which premium glass bottle adoption expands across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

Verescence positions itself as the sustainability-led premium glass bottle manufacturer in the fragrance packaging sector. The company’s operational data — including a 95.6% OTIF delivery rate and a customer complaint rate of 0.57% — demonstrate a dual focus on operational reliability and quality consistency. For luxury fragrance clients with zero tolerance for supply disruption, Verescence’s performance metrics function as a commercial moat that price-competitive rivals struggle to match.

Vidraria Anchieta serves the Latin American fragrance and cosmetics glass packaging market, providing regional supply capability that imported glass cannot match on lead time or cost. Its geographic positioning reduces the logistics complexity that limits premium glass adoption in Brazil and surrounding markets. For fragrance brands targeting Latin American retail expansion, regional glass supply partnerships are a procurement necessity, not just a convenience.

Gerresheimer AG brings broad pharmaceutical and specialty glass manufacturing expertise into the cosmetics and fragrance packaging segment. This cross-sector capability gives Gerresheimer technical credibility in high-specification glass production, which translates directly into capacity for premium perfumery bottle applications. Its diversified portfolio reduces dependency on fragrance market cycles, giving it a more stable investment profile than pure-play perfumery glass specialists.

SGB Packaging Group competes through customization capability and design flexibility, serving fragrance brands that require differentiated bottle formats without the minimum order volumes that larger glass manufacturers typically impose. This positioning makes SGB strategically relevant to the growing indie and niche perfume house segment — a buyer group that established players have historically underserved due to volume requirements.

Key Players

- Verescence

- Vidraria Anchieta

- Gerresheimer AG

- SGB Packaging Group

- Stölzle-Oberglas GmbH

- Baralan International S.p.A.

- Consol Glass Pty Ltd.

- Continental Bottle Company Ltd.

- DSM Packaging Sdn Bhd

- HEINZ-GLAS GmbH & Co. KGaA

Recent Developments

- March 2026 — Estée Lauder confirmed merger talks with Puig Brands to create a potential beauty and fragrance conglomerate. If completed, this consolidation would concentrate significant fragrance brand procurement volumes under a single entity, reshaping supplier relationships across the premium glass bottle supply chain.

- December 2025 — Givaudan completed the acquisition of Belle Aire Creations to strengthen its fragrance offering in the US market. This acquisition expands Givaudan’s fragrance ingredient portfolio, which may increase demand for premium glass packaging among fragrance houses using Givaudan’s expanded formulation capabilities.

- April 2024 — Puig completed its IPO on the Spanish Stock Exchange, valuing the company at approximately €14 billion. The public listing provides Puig with capital to accelerate fragrance brand development and expand its luxury portfolio, which structurally benefits premium glass bottle suppliers serving Puig’s packaging requirements.

Report Scope

Report Features Description Market Value (2025) USD 2.1 Billion Forecast Revenue (2035) USD 3.6 Billion CAGR (2026-2035) 5.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Form (Translucent, Transparent, Opaque), By Capacity (0–50 ml, 50–150 ml, >150 ml) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Verescence, Vidraria Anchieta, Gerresheimer AG, SGB Packaging Group, Stölzle-Oberglas GmbH, Baralan International S.p.A., Consol Glass Pty Ltd., Continental Bottle Company Ltd., DSM Packaging Sdn Bhd, HEINZ-GLAS GmbH & Co. KGaA Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Perfumery Glass Bottle MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample

Perfumery Glass Bottle MarketPublished date: Mar 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Verescence

- Vidraria Anchieta

- Gerresheimer AG

- SGB Packaging Group

- Stölzle-Oberglas GmbH

- Baralan International S.p.A.

- Consol Glass Pty Ltd.

- Continental Bottle Company Ltd.

- DSM Packaging Sdn Bhd

- HEINZ-GLAS GmbH & Co. KGaA

Our Clients

- 182299

- Mar 2026