Quick Navigation

Report Overview

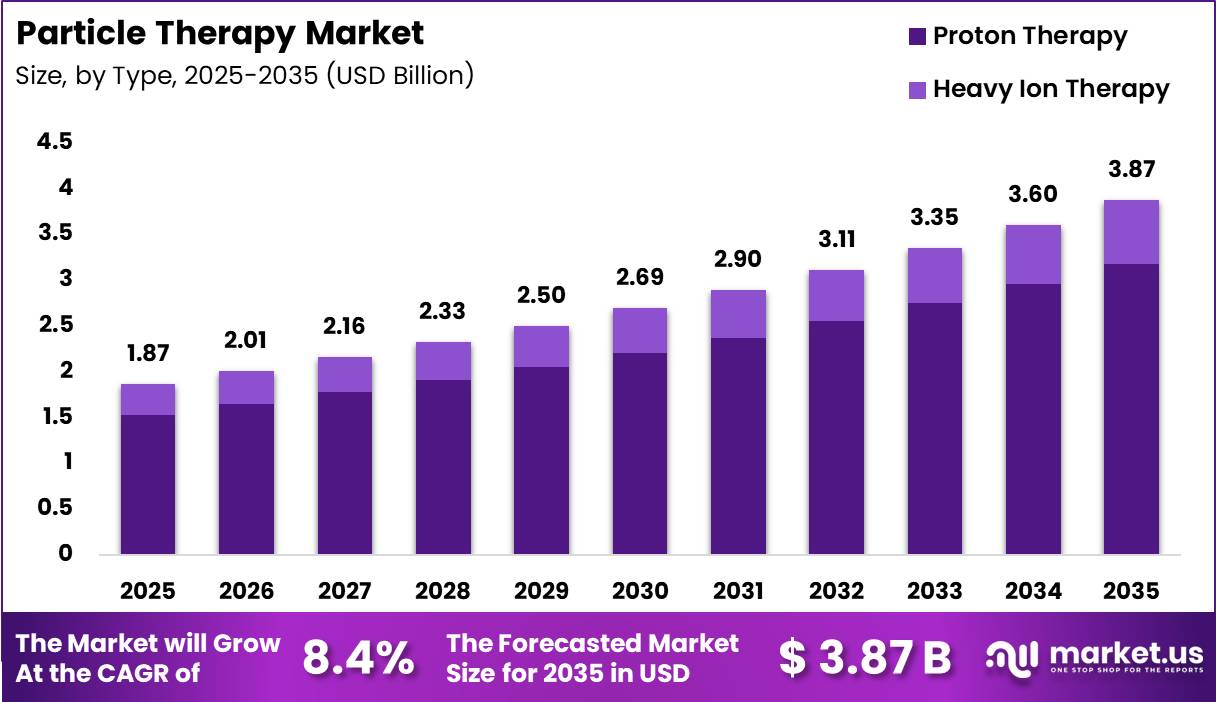

In 2025, the Global Particle Therapy Market was valued at US$ 1.87 Billion, and between 2026 and 2035, this market is estimated to register a CAGR of 8.4%, reaching about US$ 3.87 Billion by 2035. North America held a dominant market position, capturing more than a 39% share, holding USD 0.72 Billion in revenue.

The particle therapy market is experiencing sustained growth as healthcare providers increasingly invest in advanced radiation technologies that offer greater treatment precision for complex cancer cases. Demand is being driven by the clinical need to reduce radiation exposure to healthy tissues while improving treatment outcomes, particularly for pediatric and difficult-to-treat tumors.

As cancer centers focus on expanding high-value oncology services, particle therapy is becoming a strategic investment area despite its significant infrastructure requirements. The market is also benefiting from rising awareness among physicians and patients regarding the long-term advantages of highly targeted radiation treatment.

Technology innovation remains a key competitive differentiator across the industry. Equipment manufacturers are focusing on compact system designs, enhanced treatment planning software, image-guided therapy capabilities, and workflow automation to improve operational efficiency and broaden adoption beyond large academic institutions.

The shift toward more space-efficient and cost-effective proton therapy solutions is helping address historical barriers associated with facility size and capital expenditure. This evolution is enabling hospitals and cancer centers to evaluate particle therapy as a more commercially viable addition to their oncology portfolios.

The competitive landscape is shaped by continuous investments in treatment capacity expansion, product innovation, and strategic healthcare partnerships. Leading companies are strengthening their market positions through new system installations, technology upgrades, and collaborations with major cancer treatment centers. These developments underscore the market’s transition toward broader accessibility, improved clinical capabilities, and long-term capacity expansion.

- In February 2025, Ion Beam Applications (IBA) secured a contract to supply its ProteusONE proton therapy system to AIG Hospitals in India, highlighting growing demand for compact proton therapy solutions.

- In July 2025, Hitachi received an order for a proton therapy system from Tokyo Metropolitan Cancer and Infectious Diseases Center Komagome Hospital, reflecting continued global investment in advanced cancer treatment infrastructure.

Key Takeaways

- The global Particle Therapy market was valued at US$ 1.87 Billion in 2025.

- The global Particle Therapy market is projected to grow at a CAGR of 8.4% and is estimated to reach US$ 3.87 Billion by 2035.

- On the basis of type, the Proton Therapy dominated the market, constituting 82.0% of the total market share.

- Based on the Product / System, the Multi-Room Systems dominated the Particle Therapy Market, with a substantial market share of around 62.5%.

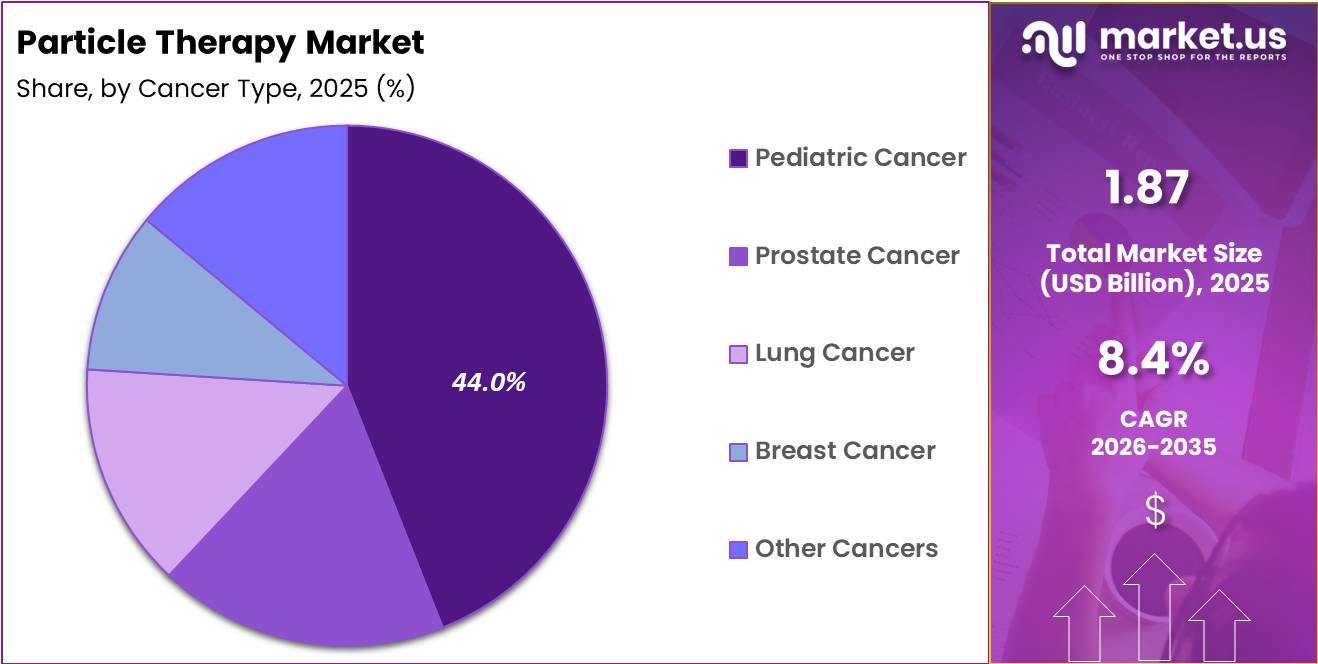

- Pediatric cancer represents the largest cancer-type segment with 44.0% share, driven by the need to minimize long-term radiation-related complications.

- Based on the Applicatiion, the Treatment applications dominate with 57.0% share as commercialization remains concentrated around clinical oncology services.

- Among the End Users, Hospitals & Clinics dominated with a 56.0% market share due to their extensive oncology infrastructure and high adoption of advanced cancer treatment technologies.

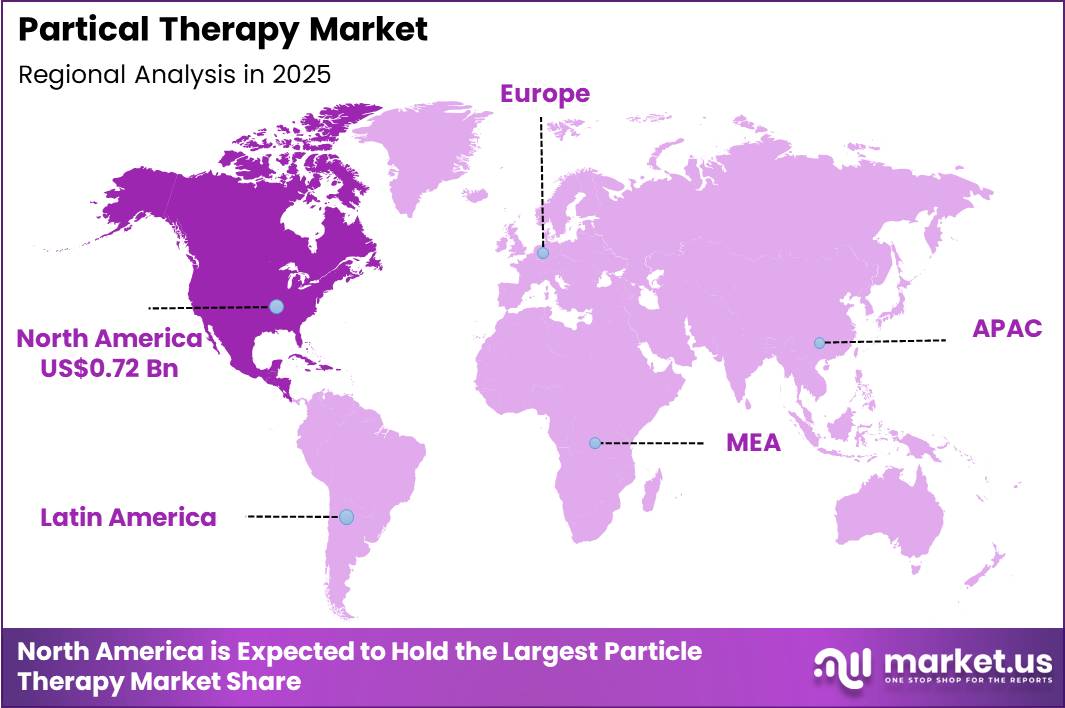

- In 2025, the North America was the most dominant region in the Particle Therapy Market, accounting for 39.0% of the total global consumption.

Type Analysis

Proton Therapy Represents the dominant Segment in the Global Particle Therapy Market.

Proton therapy accounted for 82.0% of the global particle therapy market, making it the leading treatment modality across particle-based cancer therapies. Its dominance is driven by strong clinical acceptance, particularly in pediatric and complex cancer treatments where precise dose delivery and reduced radiation exposure to healthy tissues are critical.

The technology has established a broader commercial footprint than other particle therapy modalities, supported by a growing installed base, expanding treatment capacity, and increasing integration into comprehensive oncology programs.

The segment also benefits from continuous technological advancements and increasing efforts to expand clinical expertise worldwide.

- In June 2025, Ion Beam Applications (IBA) launched the Proton Therapy Academy, a global training initiative developed with leading proton therapy institutions to strengthen workforce capabilities and accelerate adoption of proton therapy across emerging and established treatment centers.

The initiative highlights the industry’s focus on addressing skill gaps and supporting broader utilization of proton therapy. Meanwhile, heavy ion therapy continues to gain attention for selected complex and radio resistant tumors, although its wider adoption remains constrained by higher infrastructure requirements, limited treatment center availability, and greater capital intensity.

Product / System Analysis

Multi-Room Systems Represent the Leading Product Segment in the Global Particle Therapy Market.

Multi-room systems accounted for 62.5% of the global particle therapy market, driven by their superior operational efficiency, higher patient throughput, and stronger long-term economic viability for large oncology centers. These systems allow a single accelerator to serve multiple treatment rooms, enabling continuous patient flow and better utilization of high-cost infrastructure. This model is particularly preferred by large hospitals and dedicated cancer centers where demand concentration is high and treatment schedules require maximum capacity optimization.

As healthcare systems increasingly prioritize scalable oncology infrastructure, multi-room configurations remain the preferred choice for institutions investing in long-term particle therapy capabilities. The segment’s dominance is reinforced by continued adoption across major oncology infrastructure programs led by established industry players.

- In June 2025, Sumitomo Heavy Industries, Ltd. began installing its next-generation multi-room proton therapy system at Taichung Veterans General Hospital in Taiwan.

- In October 2025, Sumitomo Heavy Industries, received an order for its next-generation multi-room system to power the newly established Bangkok Proton Center at Wattanosoth Cancer Hospital in Thailand.

While single-room systems are gaining traction among mid-sized hospitals due to lower capital requirements and smaller facility footprints, multi-room systems continue to dominate revenue contribution due to their ability to support high-volume clinical operations and integrated oncology service delivery.

Cancer Type Analysis

Pediatric Cancer Represents the Leading Cancer Type Segment in the Global Particle Therapy Market

Pediatric cancer accounted for 44.0% of the global particle therapy market, making it the most dominant cancer-type segment due to its strong clinical alignment with the precision benefits of particle therapy. The segment’s leadership is driven by the critical need to minimize radiation exposure to developing tissues and sensitive organs, which significantly reduces long-term complications and secondary cancer risks. As a result, proton and particle therapy have become increasingly preferred in pediatric oncology, particularly for complex tumor cases where treatment precision directly influences survivorship outcomes and quality of life.

The segment’s dominance is reinforced by deepening integration of particle therapy within specialized pediatric oncology ecosystems and dedicated treatment networks. For instance, Varian Medical Systems, Inc. (Siemens Healthineers) continues to integrate its ProBeam systems within leading pediatric cancer centers such as the Cincinnati Children’s Proton Therapy Center, which serves as a key hub for pediatric-specific clinical advancement and research in next-generation treatment approaches. This reflects the growing strategic focus on aligning advanced particle therapy technologies with pediatric clinical excellence and research-driven care models.

While adult oncology applications such as prostate, lung, and breast cancer are gradually increasing adoption, their contribution remains secondary as pediatric oncology continues to anchor clinical utilization and investment focus across the particle therapy landscape.

Application Analysis

Treatment Applications Represent the Dominant Revenue-Generating Segment in the Global Particle Therapy Market.

Treatment applications accounted for 57.0% of the global particle therapy market, making it the dominant segment due to its direct association with clinical cancer treatment procedures and sustained patient treatment volumes. Its leadership is driven by the need to maximize utilization of high-cost particle therapy infrastructure, as hospitals and cancer centers depend on consistent reimbursed treatments to achieve operational efficiency and generate returns on significant capital investments.

As particle therapy becomes increasingly integrated into routine radiation oncology practice, particularly for complex and difficult-to-treat cancers, treatment applications remain the primary source of market revenue.

The segment’s dominance is further supported by the transition of particle therapy from a specialized treatment modality to a more established component of advanced cancer care. Growing clinical acceptance, improved integration into precision oncology workflows, and expanding indications are contributing to higher system utilization and strengthening the segment’s commercial significance across healthcare facilities.

In contrast, Research Applications represent a smaller segment focused on clinical studies, treatment protocol development, and radiotherapy innovation. Although essential for advancing particle therapy technologies and expanding future clinical use cases, their market contribution remains comparatively limited due to lower revenue generation and greater reliance on institutional, academic, and government funding.

End-User Analysis

Hospitals & Clinics Represent the Dominant End User Segment in the Global Particle Therapy Market.

Hospitals & Clinics accounted for 56.0% of the global particle therapy market, making them the leading end-user segment due to their strong financial resources, established oncology infrastructure, and ability to integrate particle therapy into comprehensive cancer treatment pathways. Their dominance is primarily driven by the high capital and operational requirements of particle therapy systems, which necessitate specialized facilities, multidisciplinary expertise, and sufficient patient volumes to ensure efficient utilization.

Consequently, large hospitals and multi-specialty healthcare networks remain the primary adopters, as they are best equipped to manage both the complexity and long-term demand associated with these technologies.

The segment’s leadership is further supported by the ongoing consolidation of advanced oncology services within major hospital systems, enabling centralized delivery of precision cancer care and higher treatment throughput. This trend is reflected in the deployment strategies of companies such as ProTom International, Inc., whose compact synchrotron-based systems are designed for integration into existing hospital environments, allowing healthcare providers to adopt advanced proton therapy capabilities with minimal disruption to established clinical workflows.

While Specialty Cancer Treatment Centers and Research & Academic Institutes are expanding through increased investment in dedicated oncology infrastructure and clinical research, their overall market share remains comparatively smaller than that of hospitals and clinics.

Key Market Segments

By Type

- Proton Therapy

- Heavy Ion Therapy

By Product/System

- Single-Room Systems

- Multi-Room Systems

By Cancer Type

- Pediatric Cancer

- Prostate Cancer

- Lung Cancer

- Breast Cancer

- Other Cancers

By Application

- Treatment Applications

- Research Applications

By End-User

- Hospitals & Clinics

- Specialty Cancer Treatment Centers / Proton & Particle Therapy Center

- Research & Academic Institutes

Driver

Pediatric and CNS case expansion through toxicity-sparing adoption

Particle therapy demand is being pulled first by the indications where clinical utility is least disputed, especially pediatric tumors, skull-base tumors, selected brain and spinal tumors, and other cases where organ-at-risk sparing directly changes long-term morbidity economics.

In Europe, pediatric indications are broadly accepted as standard, and proton therapy can cut out-of-target body dose by roughly 4.5 to 6.0 times versus photon-based craniospinal approaches, which materially strengthens the health-economic case through avoided growth, neurocognitive, endocrine, and secondary malignancy burdens over a child’s lifetime.

This driver has an outsized CAGR effect because pediatric and CNS referrals are high-value, multidisciplinary cases that improve room utilization, justify premium reimbursement, and create durable referral moats for major centers; it also accelerates conversion from “optional advanced radiotherapy” to “clinically preferred standard” in tumor boards.

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pediatric and CNS case expansion through toxicity-sparing adoption | +2.4% | North America core, Western Europe core, Japan, South Korea, China tier-1 centers | Short term (≤ 2 years) |

| Reimbursement normalization and cross-border access pathways | +1.9% | EU core, UK, selected U.S. states, Gulf referral corridors | Short term (≤ 2 years) |

| Single-room systems and lower capex architecture | +2.1% | U.S. community-academic hubs, Europe secondary cities, APAC private hospital corridors | Medium term (2-4 years) |

| Carbon-ion and high-LET platform build-out for radioresistant tumors | +1.6% | China core, Japan core, Germany, Italy, selective Middle East spill-over | Medium term (2-4 years) |

| Evidence-generation networks, registries, and indication broadening | +1.5% | Europe core, North America core, Japan, Australia | Medium term (2-4 years) |

| Emerging-market medical travel and price arbitrage | +1.2% | China, Southeast Asia, Middle East referral inflows, South America spill-over | Long term (≥ 4 years) |

Challenge

Structural shortages in particle-therapy-trained clinical workforce

Particle therapy scaling is being constrained less by headline machine availability than by the narrow global pool of radiation oncologists, medical physicists, dosimetrists, gantry engineers, and treatment-planning specialists who can safely commission and optimize proton or carbon-ion workflows; this is reinforced by the fact that the IAEA’s DIRAC framework explicitly tracks staff strength as part of radiotherapy capacity assessment, while industry organizations continue to emphasize workforce development as new centers open.

In practical terms, a new multi-room center may need roughly 25 to 45 staff with particle-specific competencies before reaching mature utilization, yet many sites still operate with cross-trained photon teams that require 12 to 24 months of supervised upskilling, producing planning backlogs, narrower treatment indication selection, and slower referral conversion.

This creates an estimated -1.3 percentage point drag on achievable market CAGR because undertrained teams depress room utilization, extend commissioning sequences, and raise replan rates, forcing operators to absorb higher labor cost per fraction and to build longer-term mitigation through academic fellowships, remote planning networks, vendor-supported training academies, and hub-and-spoke credentialing systems rather than expecting a quick labor-market normalization.

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Specialist staffing bottleneck | -1.3% | North America core, EU university hubs, East Asia leaders, India ramp-up markets | Long term (≥ 4 years) |

| Multi-vendor integration complexity | -1.1% | U.S. hospital networks, EU regulatory hubs, Japan/Korea advanced centers | Medium term (2-4 years) |

| Throughput ramp inefficiency | -1.4% | New APAC sites, U.S. greenfield builds, Southern Europe expansions | Medium term (2-4 years) |

| Reimbursement evidence and adoption lag | -1.2% | U.S. payor-intensive markets, EU public budget systems, selective APAC markets | Long term (≥ 4 years) |

| Component and specialized service dependence | -1.0% | APAC logistics corridors, Europe import-dependent sites, LatAm/Middle East new adopters | Medium term (2-4 years) |

| Carbon-ion capacity and localization gap | -0.8% | Western Hemisphere, EU late adopters, India and Southeast Asia future entrants | Long term (≥ 4 years) |

Restraints

Supply chain concentration in accelerators and gantries

Particle therapy hardware supply chains are heavily concentrated, with a handful of OEMs producing cyclotrons or synchrotrons, rotating gantries, and critical components such as superconducting magnets and high-precision beam delivery systems, leading to manufacturing lead times of 18–30 months for complete systems and exposure to disruptions in a small vendor base.

Post-2020 logistics volatility, including higher freight costs, intermittent semiconductor shortages affecting control systems, and constraints in specialized forgings and vacuum components, has extended delivery schedules by 3–6 months on average and, in some projects, caused contractual penalties or forced sequencing of room commissioning, with only 1–2 treatment rooms going live initially instead of the full planned set.

With a typical turnkey equipment package for a multi-room proton center valued at 120–200 million USD, even a 5–10% cost overrun due to supply chain issues equates to 6–20 million USD in incremental CapEx, often requiring renegotiation of financing or re-phasing of construction to stay within lender covenants, thereby delaying revenue generation.

Furthermore, the dominance of a few OEMs gives them pricing power that limits aggressive discounting, especially as their own cost bases rise, compressing hospital ROI and reducing the number of projects that clear hurdle rates at current reimbursement levels.These supply chain and vendor concentration frictions, particularly acute in EU and APAC corridors where cross-border logistics and regulatory export controls can add complexity, are estimated to subtract around 1.5 % points from global CAGR in the short to medium term by slowing system shipments, inflating project budgets, and amplifying execution risk for both providers and financiers.

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-high CapEx and financing constraints | -2.8% | North America core, EU, high-income APAC | Long term (≥ 4 years) |

| Limited reimbursement and patient affordability gaps | -2.2% | Emerging APAC, Latin America, Middle East, India | Medium term (2-4 years) |

| Workforce and expertise bottlenecks | -1.7% | EU, North America, Japan, selected APAC | Medium term (2-4 years) |

| Supply chain concentration in accelerators and gantries | -1.5% | Global, more acute in EU and APAC corridors | Short to medium term (≤ 4 years) |

| Regulatory, siting, and radiation safety approvals | -1.3% | EU, North America, densely populated APAC | Long term (≥ 4 years) |

| Clinical evidence and indication expansion lag | -1.1% | Global | Medium term (2-4 years) |

Opportunity

Scaling single-room proton centers for capital-light growth

This is an opportunity rather than a current driver because the baseline market already reflects existing multi-room center utilization, whereas the real upside comes from widening the investable buyer universe through capex-light, single-room deployment that can open second-tier academic hospitals and large private oncology chains that historically could not justify a full campus-scale build.

Global radiotherapy access remains structurally uneven, with a median 5.1 machines per million people in high-income countries versus 0 in low-income countries, while Asia-Pacific had 39 proton facilities as of October 2023 across only nine countries, showing how narrow the installed base still is relative to cancer demand.

If vendors compress project capex by roughly 35% to 50% versus traditional multi-room systems and reduce ramp-to-breakeven from about 5 to 7 years toward 3 to 4 years, the addressable customer pool could plausibly expand by 2 to 3 times, especially in India, the Gulf, Southern Europe, and US regional cancer systems; that can add about 2.4% points to baseline CAGR by converting latent hospital demand into orders, service contracts, shielding retrofits, and software revenue rather than merely increasing utilization at existing sites.

| Opportunity | (~) % Potential CAGR Upside | Geographic Relevance | Execution Window |

|---|---|---|---|

| Single-room proton rollout | +2.4% | North America, EU, Japan, India, GCC | Short term (≤ 2 years) |

| Pediatric referral networks | +1.8% | APAC emerging, Latin America, Middle East, CEE | Short term (≤ 2 years) |

| Re-irradiation service lines | +1.5% | North America core, EU, South Korea, Japan | Medium term (2-4 years) |

| Cross-border treatment hubs | +1.7% | Southeast Asia, Gulf, Central/Eastern Europe, North Africa | Medium term (2-4 years) |

| Carbon-ion adjacency buildout | +2.1% | Japan, China, Germany, Italy, GCC | Long term (≥ 4 years) |

| Outcome-linked reimbursement | +1.3% | US private payers, Germany, Nordics, UK, Australia | Medium term (2-4 years) |

Regional Analysis

North America Held the Largest Share of the Global Particle Therapy Market.

North America commands a 39% share of the global particle therapy market, anchored by the United States’ position as the world’s largest single national installed base of operational proton therapy centers, with over 40 centers as of 2025 and continued expansion through active construction programs at leading cancer institutions. This dominance is driven by a mature oncology infrastructure, strong reimbursement support for advanced cancer treatments, and the financial capacity of integrated healthcare systems to support highly capital-intensive particle therapy deployments.

The region benefits from early adoption of precision oncology, extensive clinical experience in proton therapy utilization, and a well-established network of academic medical centers that enables seamless integration of particle therapy into complex cancer care pathways.

The market leadership is further reinforced by sustained investments in technology innovation and system upgrades across radiation oncology platforms, supported by key industry players such as Varian (Siemens Healthineers) and Accuray Incorporated. These companies contribute to continuous improvements in treatment planning, delivery efficiency, and workflow integration, strengthening system utilization and operational performance across installed centers. This combination of large installed base, strong reimbursement environment, and advanced clinical infrastructure positions North America as the central hub for particle therapy deployment and technological advancement globally.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global particle therapy treatment market is moderately consolidated, with a small group of established medical technology and industrial engineering companies accounting for the majority of installed proton and heavy ion therapy systems worldwide. Ion Beam Applications S.A. maintains a leading position through its extensive installed base and comprehensive proton therapy portfolio, while Varian Medical Systems, Inc. leverages integrated radiation oncology software and treatment planning capabilities to strengthen its market presence.

Japanese leaders including Hitachi, Ltd., Sumitomo Heavy Industries, Ltd., and Mitsubishi Electric Corporation benefit from strong domestic deployment, long-term R&D investments, and established export capabilities.

Below this leading tier, the market is increasingly fragmented and innovation-driven, with companies such as Mevion Medical Systems, Inc., ProTom International, Inc., and ProNova Solutions, LLC advancing compact single-room proton therapy systems designed to reduce capital requirements and expand adoption beyond major academic centers.

Specialized participants including Optivus Proton Therapy, Inc. and Advanced Oncotherapy plc, alongside ecosystem contributors such as Elekta AB, Accuray Incorporated, Danfysik A/S, and P-Cure Ltd., support market growth through innovations in treatment planning, accelerator technology, component engineering, and workflow optimization. Overall, market competition is defined by the dominance of a few large system providers and a growing group of innovators focused on improving affordability, accessibility, and operational efficiency.

Major Players In The Industry

- Ion Beam Applications S.A. (IBA Worldwide)

- Varian Medical Systems, Inc. (Siemens Healthineers)

- Hitachi, Ltd.

- Sumitomo Heavy Industries, Ltd.

- Mitsubishi Electric Corporation

- Mevion Medical Systems, Inc.

- ProTom International, Inc.

- Provision Healthcare, LLC

- Optivus Proton Therapy, Inc.

- Advanced Oncotherapy plc

- Elekta AB

- ProNova Solutions, LLC

- Accuray Incorporated

- Danfysik A/S

- P-Cure Ltd.

Key Development

- In April 2026, IBA Worldwide received regulatory clearance for its ProteusNEXT adaptive proton therapy platform incorporating real-time anatomical imaging and automated plan adaptation, enabling the first commercially available adaptive proton therapy delivery system and establishing a new clinical standard for treatment precision.

- In March 2026, Varian Medical Systems (Siemens Healthineers) announced a strategic partnership with a leading Middle Eastern comprehensive cancer center to deploy its ProBeam multi-room proton therapy system as the anchor technology for the center’s new particle therapy program, expanding Siemens Healthineers’ installed base in the MENA region.

- In February 2026, Hitachi, Ltd. delivered and commissioned a new carbon ion therapy system at a provincial comprehensive cancer hospital in China under a bilateral Japan-China technology cooperation framework, representing Hitachi’s first carbon ion system deployment in Mainland China.

- In January 2026, Mevion Medical Systems announced a clinical partnership with a U.S. academic medical center to evaluate FLASH proton therapy—ultra-high dose rate delivery—using the MEVION S250i system, positioning Mevion at the forefront of the FLASH therapy clinical development program.

- In December 2025, Sumitomo Heavy Industries signed a contract for the delivery of a proton therapy system to a new cancer center in Southeast Asia under JBIC (Japan Bank for International Cooperation) export financing, reflecting Japan’s state-supported radiological technology export strategy.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 1.87 Bn |

| Forecast Revenue (2035) | US$ 3.87 Bn |

| CAGR (2026-2035) | 8.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Type (Proton Therapy, Heavy Ion Therapy / Carbon Ion Therapy); By Product/System (Single-Room Systems, Multi-Room Systems); By Cancer Type (Pediatric Cancer, Prostate Cancer, Lung Cancer, Breast Cancer, Other Cancers); By Application (Treatment Applications, Research Applications); By End User (Hospitals & Clinics, Specialty Cancer Treatment Centers / Proton & Particle Therapy Centers, Research & Academic Institutes) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA |

| Competitive Landscape | Ion Beam Applications S.A. (IBA Worldwide), Varian Medical Systems Inc. (Siemens Healthineers), Hitachi Ltd., Sumitomo Heavy Industries Ltd., Mitsubishi Electric Corporation, Mevion Medical Systems Inc., ProTom International Inc., Provision Healthcare LLC, Optivus Proton Therapy Inc., Advanced Oncotherapy plc, Elekta AB, ProNova Solutions LLC, Accuray Incorporated, Danfysik A/S, P-Cure Ltd. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |