Global Pantograph Charger Market Size, Share, Growth Analysis, Charging Type (Direct Current Fast Charging (DCFC), Level 1 Charging, Level 2 Charging), Component Type (Hardware, Software, Services), Charging Infrastructure Type (Off-Board Top-Down Pantograph, On-Board Bottom-Up Pantograph), Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Feb 2026

- Report ID: 179721

- Number of Pages: 218

- Format:

-

keyboard_arrow_up

Quick Navigation

Market Overview

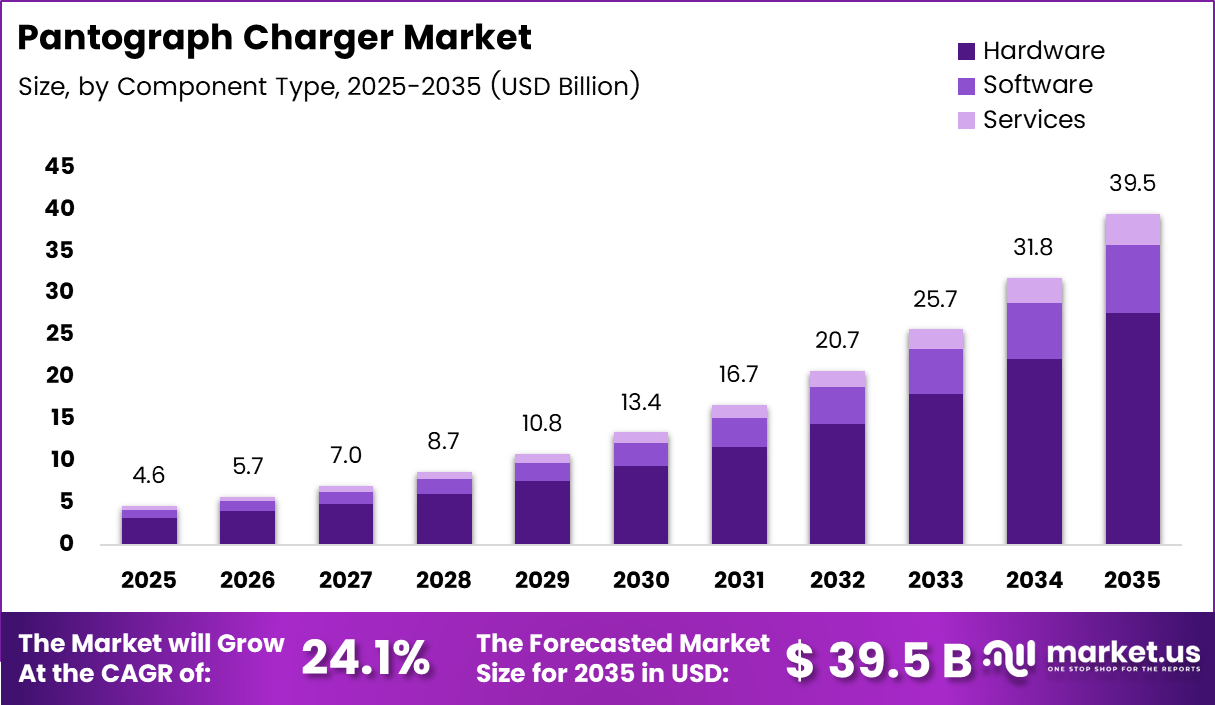

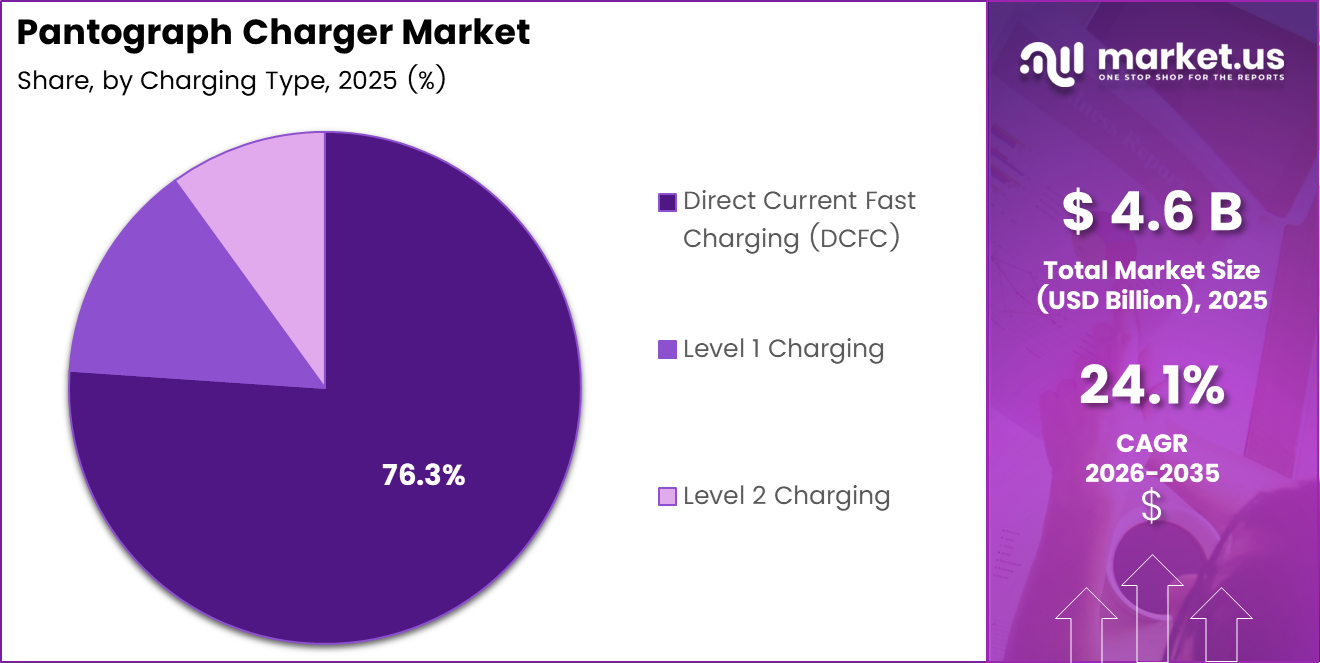

Global Pantograph Charger Market size is expected to be worth around USD 39.5 Billion by 2035 from USD 4.6 Billion in 2025, growing at a CAGR of 24.1% during the forecast period 2026 to 2035.

The pantograph charger market refers to the segment of electric vehicle charging infrastructure that uses automated overhead or roof-mounted contact systems. These chargers enable high-power opportunity charging for electric buses and transit vehicles. They are a critical component of zero-emission public transportation networks worldwide.

Pantograph charging systems are designed to minimize downtime by delivering fast, automated charging during brief stops. Unlike conventional plug-in chargers, they use mechanical arms to make electrical contact. This makes them especially effective for depot charging and in-route opportunity charging for urban transit fleets.

Rapid urbanization and the global push toward zero-emission public transit are accelerating market demand. Governments across North America, Europe, and Asia Pacific are mandating the phase-out of diesel buses. Consequently, transit authorities are investing heavily in overhead charging infrastructure to support large electric bus fleets at scale.

Smart city initiatives are further strengthening market growth. Many municipalities are integrating electric public transportation into broader urban mobility strategies. Additionally, increasing government funding and policy incentives are lowering the financial barriers for transit operators adopting pantograph-based charging solutions.

According to Kempower, their Pantograph Up system can connect up to 12 charging points to a 450 kW or 600 kW Power Unit, delivering a maximum charging power of 500 kW per unit. This level of scalability is enabling operators to charge larger bus fleets within existing depot footprints efficiently.

According to ABB, pantograph systems support a voltage range of 150 to 850 V and a power range from 50 kW to 600 kW, covering both overnight and opportunity charging needs. Moreover, sequential charging with up to 3 outlets further optimizes fleet management for transit operators globally.

Key Takeaways

- The global Pantograph Charger Market was valued at USD 4.6 Billion in 2025 and is projected to reach USD 39.5 Billion by 2035.

- The market is growing at a CAGR of 24.1% during the forecast period 2026 to 2035.

- By Charging Type, Direct Current Fast Charging (DCFC) dominates with a market share of 76.3% in 2025.

- By Component Type, Hardware holds the leading position with a share of 69.9% in 2025.

- By Charging Infrastructure Type, Off-Board Top-Down Pantograph leads the segment with a share of 72.4% in 2025.

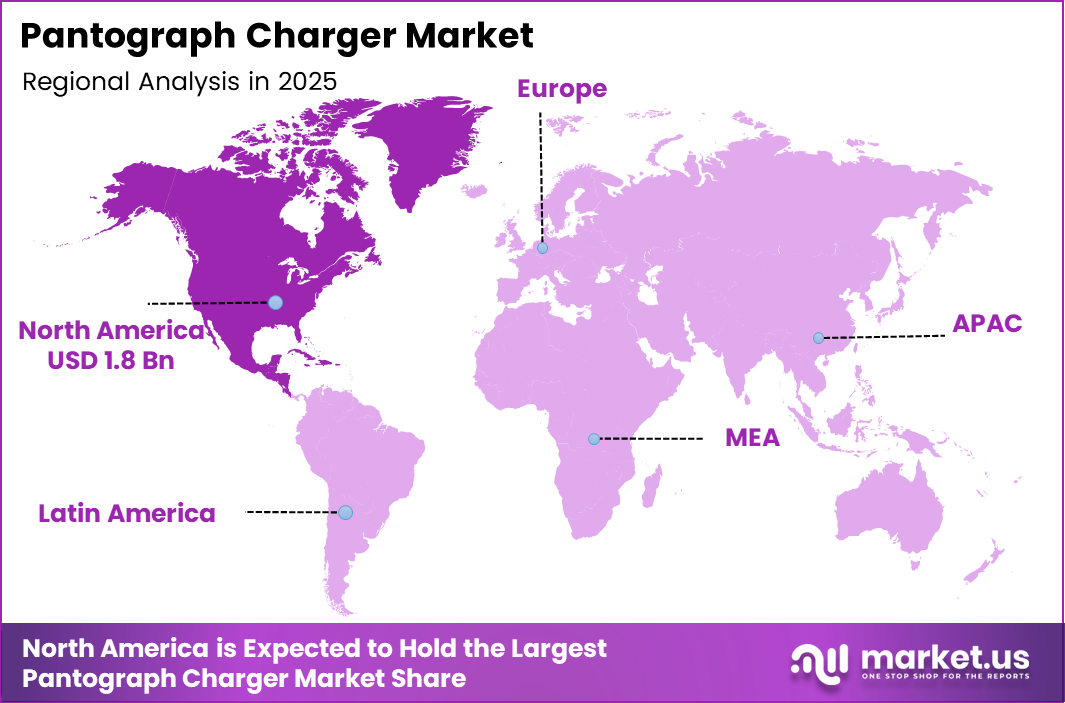

- North America dominates the regional landscape with a market share of 41.80%, valued at USD 1.8 Billion in 2025.

Charging Type Analysis

Direct Current Fast Charging (DCFC) dominates with 76.3% due to its high-power delivery capability for opportunity charging in transit operations.

In 2025, Direct Current Fast Charging (DCFC) held a dominant market position in the Charging Type segment of the Pantograph Charger Market, with a 76.3% share. DCFC systems deliver high-power charging in short timeframes, making them ideal for electric bus fleets requiring opportunity charging during route stops or at terminals. Their efficiency and speed have made them the preferred choice for transit operators globally.

Level 1 Charging represents a smaller portion of the market, primarily used for low-power overnight depot charging applications. However, it serves transit operators in regions with lower power grid capacities or budget-constrained infrastructure deployments. Level 1 systems offer a cost-effective entry point for municipalities beginning their electrification journey.

Level 2 Charging occupies a mid-tier position within the charging type segment. It supports moderate overnight and extended depot charging scenarios for electric bus fleets. Additionally, Level 2 infrastructure is increasingly being considered as a complementary solution alongside faster DCFC systems in mixed-use transit depot environments.

Component Type Analysis

Hardware dominates with 69.9% due to the high demand for physical charging units, pantograph arms, and power delivery systems.

In 2025, Hardware held a dominant market position in the Component Type segment of the Pantograph Charger Market, with a 69.9% share. Hardware encompasses the physical charging units, pantograph arms, contact systems, and power electronics. The large capital investment required for physical charging infrastructure installation drives this segment’s leading share across transit projects globally.

Software is a growing component within the pantograph charger ecosystem. It includes charging management platforms, real-time monitoring tools, and predictive maintenance applications. Moreover, as transit operators seek to optimize fleet uptime and energy consumption, software integration is becoming an increasingly essential part of pantograph charging deployments.

Services cover installation, commissioning, maintenance, and technical support for pantograph charging systems. Consequently, as the installed base of pantograph chargers expands worldwide, demand for after-sales services is expected to grow steadily. Service contracts are becoming a key revenue stream for charging infrastructure providers operating in this market.

Charging Infrastructure Type Analysis

Off-Board Top-Down Pantograph dominates with 72.4% due to its compatibility with high-power charging and ease of fleet-wide deployment.

In 2025, Off-Board Top-Down Pantograph held a dominant market position in the Charging Infrastructure Type segment of the Pantograph Charger Market, with a 72.4% share. In this design, the pantograph arm extends downward from an overhead structure onto the vehicle’s roof contact. This approach simplifies vehicle design and allows centralized installation at bus stops or depots, making it highly scalable for large transit fleets.

On-Board Bottom-Up Pantograph systems feature a pantograph arm mounted on the vehicle itself, which extends upward to connect with a fixed overhead contact point. Therefore, this design provides flexibility in infrastructure placement and is commonly adopted in transit networks where overhead gantry installation is impractical. Adoption is growing steadily in specific urban transit corridors across Europe and Asia Pacific.

Key Market Segments

By Charging Type

- Direct Current Fast Charging (DCFC)

- Level 1 Charging

- Level 2 Charging

By Component Type

- Hardware

- Software

- Services

By Charging Infrastructure Type

- Off-Board Top-Down Pantograph

- On-Board Bottom-Up Pantograph

Drivers

Rapid Electrification of Public Bus Fleets and Urban Emission Regulations Drive Pantograph Charger Market Growth

The rapid electrification of public bus fleets is a primary driver of pantograph charger adoption. Transit authorities worldwide are replacing diesel buses with electric alternatives to meet emission reduction targets. Consequently, the need for high-power, automated overhead charging systems that minimize fleet downtime has grown significantly across urban transit networks.

Urban emission regulations are further accelerating market expansion. Many city governments have introduced strict zero-emission zones and mandated the adoption of clean public transportation. Therefore, transit operators are under regulatory pressure to invest in pantograph charging infrastructure that supports full fleet electrification without service interruptions.

Additionally, demand for reduced downtime through automated overhead charging is reshaping how transit operators plan their charging strategies. Pantograph systems eliminate manual plug-in processes, enabling faster turnaround at terminals. Moreover, the expansion of smart city projects that integrate electric public transportation is creating large-scale deployment opportunities for pantograph charging solutions globally.

Restraints

High Capital Investment and Standardization Challenges Restrain Pantograph Charger Market Adoption

High initial capital investment remains one of the most significant barriers to pantograph charger adoption. The installation of overhead charging infrastructure, including gantry structures, power electronics, and grid connections, requires substantial upfront expenditure. Consequently, smaller transit operators and municipalities in developing regions often struggle to justify the financial commitment required for deployment.

Standardization challenges across vehicle platforms and charging interfaces further complicate market growth. Different electric bus manufacturers use varying pantograph designs and voltage specifications. Therefore, transit authorities procuring mixed-brand fleets face interoperability issues that increase integration complexity and overall project costs for pantograph charging infrastructure deployments.

Moreover, the lack of universally accepted technical standards creates uncertainty for infrastructure investors and operators. Fragmented regulatory frameworks across countries add another layer of complexity. However, ongoing international standardization efforts by industry bodies are gradually addressing these issues, which may help reduce barriers over the medium to long term.

Growth Factors

Government Funding, Fleet Expansion, and Renewable Energy Integration Accelerate Pantograph Charger Market Growth

Government funding and incentive programs are playing a critical role in accelerating pantograph charger deployments. Public grants, subsidies, and low-interest financing are reducing the financial burden on transit operators. Additionally, national clean transportation programs in the United States, European Union, and China are directly supporting the buildout of electric bus charging infrastructure.

Rising adoption of pantograph chargers in electric truck and logistics fleets presents a significant new growth avenue. Beyond public transit, commercial vehicle operators are exploring overhead charging for depot-based truck fleets. Therefore, the addressable market for pantograph charging technology is expanding well beyond traditional urban bus applications into freight and logistics sectors.

Integration of pantograph chargers with renewable energy sources and energy storage systems is another key growth factor. Combining solar or wind power with battery buffers at charging depots reduces grid strain and operating costs. Moreover, emerging demand from developing cities transitioning to electric mass transit is opening new high-growth markets across Asia, Africa, and Latin America.

Emerging Trends

Ultra-Fast Charging, Smart Monitoring, and OEM Partnerships Are Reshaping the Pantograph Charger Market

A clear shift toward ultra-fast and high-capacity pantograph charging solutions is underway. Transit operators are demanding systems capable of delivering higher power outputs in shorter windows to maximize fleet availability. Consequently, manufacturers are developing next-generation pantograph units with power ratings exceeding 600 kW to meet the growing needs of high-frequency bus routes.

Increasing use of inverted and roof-mounted pantograph designs is changing infrastructure planning for transit authorities. These configurations offer greater architectural flexibility and reduce the visual impact of overhead charging structures in urban environments. Additionally, the growing variety of pantograph designs is enabling more customized deployment approaches for different city layouts and bus terminal configurations.

Integration of real-time monitoring and predictive maintenance software is becoming a standard expectation in modern pantograph charging systems. Smart platforms allow operators to track charging performance, detect faults early, and schedule maintenance proactively. Moreover, growing partnerships between original equipment manufacturers, utilities, and transit authorities are accelerating the deployment of integrated, end-to-end pantograph charging ecosystems globally.

Regional Analysis

North America Dominates the Pantograph Charger Market with a Market Share of 41.80%, Valued at USD 1.8 Billion

North America leads the global pantograph charger market, accounting for 41.80% of total market share and valued at USD 1.8 Billion in 2025. The region’s dominance is driven by aggressive federal and state-level investments in zero-emission transit infrastructure. Strong regulatory mandates, particularly in the United States and Canada, are compelling transit agencies to rapidly deploy electric bus fleets supported by high-power pantograph charging systems.

Europe Pantograph Charger Market Trends

Europe is a mature and rapidly growing market for pantograph chargers, supported by the European Green Deal and strict urban emission standards. Countries such as Germany, the UK, and France are leading deployments across municipal transit networks. Moreover, European OEMs and charging infrastructure providers are actively shaping international standards for pantograph charging interoperability.

Asia Pacific Pantograph Charger Market Trends

Asia Pacific represents the fastest-growing regional market, driven by China’s large-scale electric bus adoption and expanding smart city programs across India, Japan, and South Korea. China in particular has deployed pantograph charging infrastructure at scale across hundreds of cities. Consequently, the region is expected to close the gap with North America significantly over the forecast period.

Middle East and Africa Pantograph Charger Market Trends

The Middle East and Africa market is at an early but promising stage of development. Gulf Cooperation Council nations are investing in electric public transit as part of broader sustainability and economic diversification initiatives. Additionally, South African cities are beginning to explore electric bus programs that will require supporting pantograph charging infrastructure in the coming years.

Latin America Pantograph Charger Market Trends

Latin America is gradually emerging as a new frontier for pantograph charging adoption. Brazil and Mexico are the primary markets, with several city governments piloting electric bus fleets in major metropolitan areas. However, infrastructure funding constraints and grid reliability challenges remain key factors that transit planners must address to accelerate broader market expansion across the region.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

ABB Ltd. is a global leader in electric vehicle charging infrastructure, including pantograph-based systems for electric buses and transit fleets. The company offers a comprehensive range of pantograph chargers supporting voltage ranges from 150 V to 850 V and power outputs from 50 kW to 600 kW. ABB’s scalable architecture and global service network make it a preferred partner for large transit authorities worldwide.

Siemens AG brings deep expertise in rail electrification and smart grid technology to the pantograph charger market. The company delivers integrated charging solutions combining hardware, energy management software, and grid connectivity. Siemens has also expanded its capabilities through strategic acquisitions, positioning itself to address growing demand for high-power charging solutions across urban electric bus and logistics fleet applications.

Wabtec Corporation leverages its heritage in transit technology to provide advanced pantograph charging infrastructure tailored for heavy-duty electric transit applications. The company’s solutions focus on reliability, system integration, and long-term lifecycle performance for transit operators. Moreover, Wabtec’s strong relationships with transit agencies across North America give it a competitive advantage in the rapidly growing electric bus market.

Schunk Transit Systems GmbH specializes in current collector systems and pantograph technology for electric buses, trams, and rail vehicles. The company is recognized for its engineering precision and expertise in contact strip technology used in overhead charging systems. Additionally, Schunk’s focused product portfolio and technical depth in pantograph components make it a key supplier to OEMs and transit operators seeking reliable overhead charging solutions.

Key Players

- ABB Ltd.

- Siemens AG

- Wabtec Corporation

- Schunk Transit Systems GmbH

- Vector Informatik GmbH

- SETEC Power

- Valmont Industries, Inc

- Comeca Group

- Hangzhou Aoneng Power Supply Equipment Co., Ltd

- ChargePoint Inc.

Recent Developments

- January 2024 – Hitachi Energy acquired Coet, a manufacturer of specialized electrical equipment, strengthening its position in the electric transit infrastructure sector. This strategic move expands Hitachi Energy’s product portfolio and technical capabilities in the growing pantograph and transit electrification market.

- January 2024 – Siemens AG acquired Heliox, a specialist in fast charging solutions for electric trucks and buses, marking a significant expansion of its e-Mobility charging portfolio. This acquisition enhances Siemens’ ability to deliver high-power charging infrastructure, including pantograph systems, across European and global transit markets.

Report Scope

Report Features Description Market Value (2025) USD 4.6 Billion Forecast Revenue (2035) USD 39.5 Billion CAGR (2026-2035) 24.1% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered Charging Type (Direct Current Fast Charging (DCFC), Level 1 Charging, Level 2 Charging), Component Type (Hardware, Software, Services), Charging Infrastructure Type (Off-Board Top-Down Pantograph, On-Board Bottom-Up Pantograph) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape ABB Ltd., Siemens AG, Wabtec Corporation, Schunk Transit Systems GmbH, Vector Informatik GmbH, SETEC Power, Valmont Industries Inc., Comeca Group, Hangzhou Aoneng Power Supply Equipment Co. Ltd., ChargePoint Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- ABB Ltd.

- Siemens AG

- Wabtec Corporation

- Schunk Transit Systems GmbH

- Vector Informatik GmbH

- SETEC Power

- Valmont Industries, Inc

- Comeca Group

- Hangzhou Aoneng Power Supply Equipment Co., Ltd

- ChargePoint Inc.

Our Clients

- 179721

- Feb 2026