Global Pancreatic and Bile Duct Stone Management Market By Product (ERCP Catheters, Guidewires, Sphincterotomes, Dilation Balloon Catheters, Extraction Balloon Catheters, Extraction Basket Catheters, Biliary Stents, Self-Expandable Biliary Stents and Others), By End User (Hospitals, Ambulatory Surgical Centers and Specialty Clinics), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 182478

- Number of Pages: 224

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

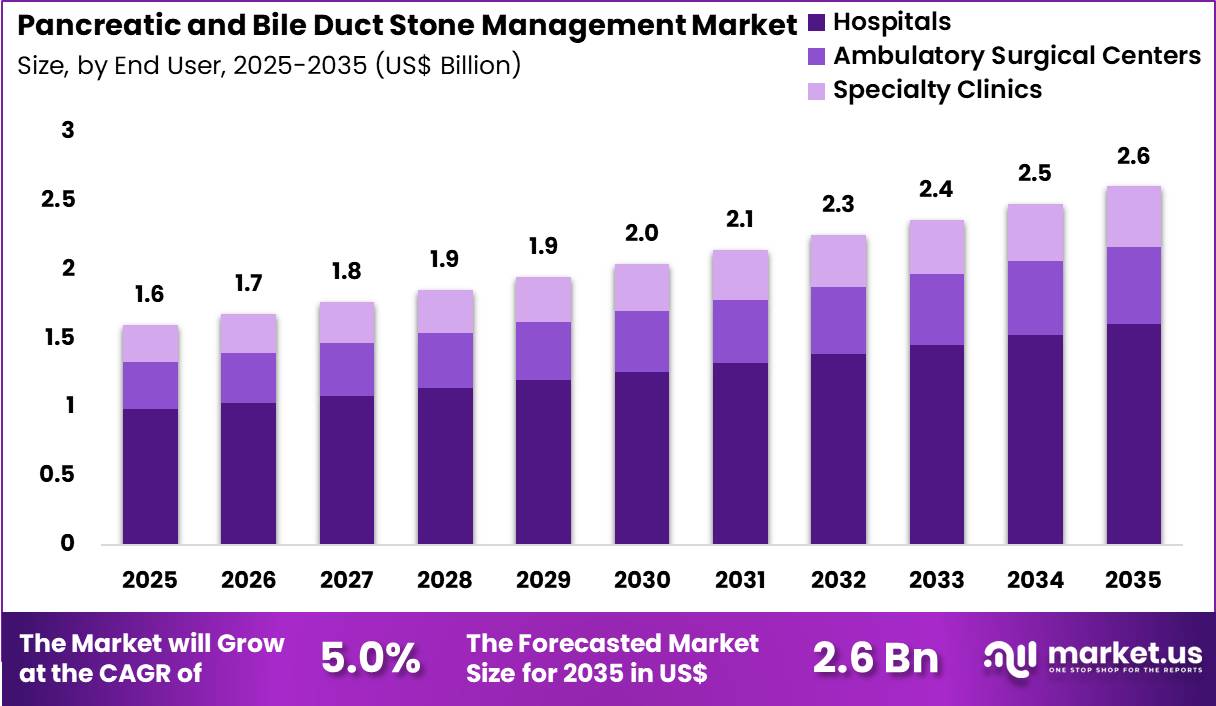

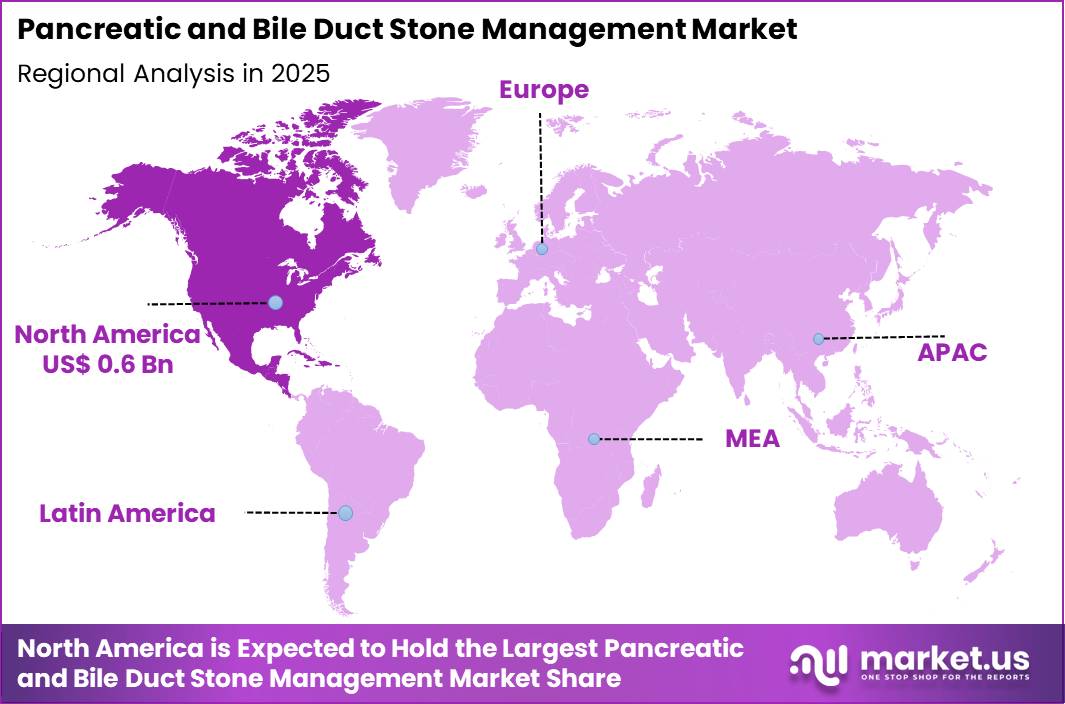

The Global Pancreatic and Bile Duct Stone Management Market size is expected to be worth around US$ 2.6 Billion by 2035 from US$ 1.6 Billion in 2025, growing at a CAGR of 5.0% during the forecast period 2026-2035. In 2025, North America led the market, achieving over 39.4% share with a revenue of US$ 0.6 Billion.

Rising prevalence of gallstone disease and pancreaticobiliary disorders drives the Pancreatic and Bile Duct Stone Management market as gastroenterologists and surgeons require advanced tools to effectively remove stones and relieve obstructions with minimal complications.

Endoscopists increasingly perform endoscopic retrograde cholangiopancreatography with sphincterotomy and balloon dilation to extract common bile duct stones in patients with choledocholithiasis, restoring biliary flow and preventing cholangitis or pancreatitis. These procedures support mechanical lithotripsy for large or impacted stones that resist standard extraction, fragmenting calculi into smaller pieces for safe removal during the same session.

In cases of recurrent or refractory stones, clinicians apply extracorporeal shock wave lithotripsy to break down stones in the pancreatic duct or bile duct, facilitating subsequent endoscopic clearance in chronic pancreati

tis or primary sclerosing cholangitis patients. Interventional radiologists utilize percutaneous transhepatic cholangiography with basket retrieval or laser lithotripsy to manage intrahepatic stones or stones inaccessible via endoscopic routes, providing decompression in malignant biliary obstructions or post-surgical strictures.

These interventions also address Mirizzi syndrome and gallstone ileus complications, where combined endoscopic and surgical approaches restore patency and prevent recurrent episodes.

Manufacturers pursue opportunities to refine retrieval devices and imaging-guided systems that improve stone capture and procedural success rates, expanding applications in high-risk patients with large stones or altered anatomy. These advancements support real-time visualization enhancements that delineate stone boundaries and optimize extraction pathways during complex procedures.

Throughout 2025, Medtronic advanced its imaging capabilities by integrating artificial intelligence into fluoroscopy-compatible biliary systems. The software assists clinicians during procedures by highlighting stone boundaries and guiding optimal intervention pathways in real time.

In September 2025, Cook Medical received updated regulatory clearance for its VistaWay biliary extraction baskets. The revised design incorporates enhanced nitinol construction to maintain structural integrity during repeated use within a single procedure, supporting more efficient stone retrieval.

Recent trends emphasize AI-assisted imaging, durable retrieval tools, and minimally invasive techniques that reduce procedure time and complications, positioning the market for growth in effective, patient-centered management of pancreatic and bile duct stones across endoscopic, radiologic, and hybrid approaches.

Key Takeaways

- In 2025, the market generated a revenue of US$ 1.6 Billion, with a CAGR of 5.0%, and is expected to reach US$ 2.6 Billion by the year 2035.

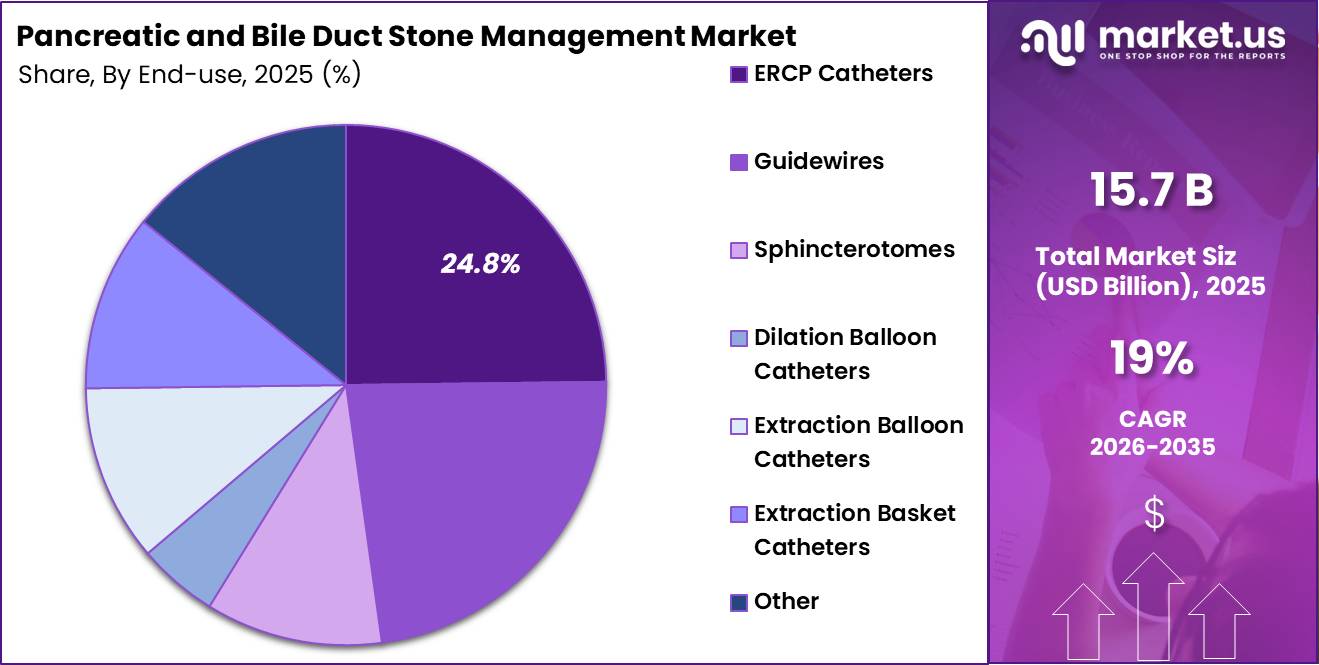

- The product segment is divided into ercp catheters, guidewires, sphincterotomes, dilation balloon catheters, extraction balloon catheters, extraction basket catheters, biliary stents, self-expandable biliary stents and others, with ercp catheters taking the lead with a market share of 24.8%.

- Considering end user, the market is divided into hospitals, ambulatory surgical centers and specialty clinics. Among these, hospitals held a significant share of 61.5%.

- North America led the market by securing a market share of 39.4%.

Product Analysis

ERCP catheters accounted for 24.8% of growth within product and dominate the pancreatic and bile duct stone management market because they are the primary access tools used at the start of most ERCP-based stone procedures.

ERCP itself remains a core therapeutic approach for bile and pancreatic duct obstruction, and NIDDK notes that doctors use ERCP to treat problems of the bile and pancreatic ducts, especially when blockage or narrowing is present.

Catheters hold a central role because physicians use them for duct access, contrast delivery, cannulation support, and procedural control before stone extraction devices come into play. Their use is expected to stay high because almost every therapeutic ERCP workflow depends on successful initial duct entry.

Clinical practice also increasingly favors wire-assisted cannulation, and published evidence shows guidewire-assisted cannulation improves primary cannulation rates while reducing the risk of post-ERCP pancreatitis compared with contrast-assisted methods. That pattern strengthens demand for compatible ERCP catheter systems designed for precision and maneuverability.

The segment is projected to grow further as hospitals handle more complex biliary and pancreatic cases and as endoscopists seek faster, safer access in technically difficult anatomy. Ongoing product refinements in tip control, radiopacity, and compatibility with guidewire-based techniques are likely to reinforce segment leadership.

As procedural success in stone management continues to depend heavily on reliable duct access, ERCP catheters are anticipated to remain the leading product segment in this market.

End-User Analysis

Hospitals accounted for 61.5% of growth within end user and dominate the pancreatic and bile duct stone management market because they provide the infrastructure, imaging support, anesthesia backup, and specialist teams required for ERCP-led interventions.

Stone management in the bile or pancreatic duct often involves fluoroscopy, therapeutic endoscopy, and complication monitoring, which makes hospital settings the most suitable site of care. NIDDK describes ERCP as a procedure that combines upper GI endoscopy and x-rays, and that technical requirement directly favors hospitals with advanced endoscopy units.

Hospitals also lead this market because ERCP carries meaningful clinical risk and ASGE notes that ERCP-guided treatment of bile duct stones has major adverse event rates in the 6% to 15% range, which increases the importance of emergency readiness and multidisciplinary oversight.

These institutions are expected to remain dominant as they manage higher-acuity patients, more complex stones, and cases involving cholangitis, pancreatitis, or altered anatomy. They are also more likely to have experienced gastroenterologists, endoscopy nurses, and post-procedure observation capacity under one system.

ASGE quality guidance further notes that expert centers can achieve bile duct clearance rates well above 90% for bile duct stones, which supports concentration of these procedures in hospital-based advanced endoscopy programs.

As procedure complexity, safety expectations, and demand for specialized therapeutic endoscopy continue to rise, hospitals are projected to retain their leading end-user position in this market.

Key Market Segments

By Product

- ERCP Catheters

- Guidewires

- Sphincterotomes

- Dilation Balloon Catheters

- Extraction Balloon Catheters

- Extraction Basket Catheters

- Biliary Stents

- Self-Expandable Biliary Stents

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

Drivers

Rising incidence of choledocholithiasis and pancreatic duct stones is driving the market.

Endoscopic retrograde cholangiopancreatography (ERCP) remains the primary therapeutic modality for managing common bile duct stones and pancreatic duct calculi. The procedure volume has increased in response to improved detection through routine abdominal imaging and magnetic resonance cholangiopancreatography.

Gastroenterologists perform sphincterotomy and balloon dilation with greater frequency in patients presenting with obstructive jaundice or recurrent pancreatitis. The driver aligns with aging populations exhibiting higher gallstone prevalence and associated biliary complications. Facilities report consistent utilization of basket extraction and mechanical lithotripsy for large or impacted stones.

The trend supports multidisciplinary management involving gastroenterology, surgery, and interventional radiology teams. Enhanced procedural success rates encourage earlier intervention in symptomatic cases.

Sustained diagnostic advancements maintain demand for specialized ERCP accessories and lithotripsy devices. This factor reinforces market stability through reliable procedural requirements in hepatobiliary and pancreatic care.

Overall, the growing burden of stone-related pathology sustains demand for effective endoscopic and percutaneous management solutions

Restraints

High procedural complication rates and need for repeat interventions are restraining the market.

Large or multiple common bile duct stones frequently require mechanical lithotripsy or multiple ERCP sessions when initial extraction fails. Pancreatic duct stones often necessitate extracorporeal shock wave lithotripsy or repeated endoscopic sessions due to stone hardness and duct strictures.

The restraint increases cumulative procedural risks including post-ERCP pancreatitis, bleeding, and perforation. Facilities face elevated readmission rates and extended hospital stays in complex cases. The factor contributes to cautious adoption of aggressive endoscopic approaches in high-risk patients.

Providers encounter challenges justifying additional interventions when outcomes remain uncertain. The dynamic moderates enthusiasm for routine use of advanced fragmentation devices. This constraint limits broader application of minimally invasive techniques in certain patient subgroups.

The limitation persists in influencing procedural selection and resource allocation. Complication-related concerns continue to temper market expansion for specialized stone management tools.

Opportunities

Development of single-session large stone clearance techniques is creating growth opportunities.

Endoscopic papillary large balloon dilation combined with limited sphincterotomy has emerged as an effective strategy for extracting stones larger than 15 mm in a single procedure. These techniques reduce the need for mechanical lithotripsy and subsequent sessions.

Opportunities arise for improved patient throughput and decreased cumulative procedural risk. The framework supports expanded utilization in ambulatory endoscopy units. Developers can pursue refined balloon designs with controlled radial expansion profiles.

The development facilitates training programs focused on safe papillary dilation protocols. Such advancements attract high-volume centers seeking efficiency gains. The opportunity fosters differentiation through superior stone clearance rates and shorter fluoroscopy times.

Stakeholders anticipate reduced healthcare resource utilization in complex biliary cases. This progression positions participants for innovation in efficient stone extraction methods.

Impact of Macroeconomic / Geopolitical Factors

Macroeconomic conditions and geopolitical factors are shaping cost structures, access to care, and procedural volumes in the pancreatic and bile duct stone management market.

Rising healthcare spending and improved hospital infrastructure support higher adoption of advanced endoscopic procedures, while inflation increases the cost of devices such as endoscopes, baskets, and lithotripsy systems, which can limit affordability in some settings.

Currency fluctuations and global trade disruptions affect the pricing and availability of specialized components and accessories sourced from multiple regions. Geopolitical tensions also influence medical tourism flows and cross-border training programs for skilled endoscopists, which impacts procedural capacity in emerging markets.

Current US tariffs on imported medical devices and components raise procurement costs for healthcare providers, leading to budget adjustments and delayed equipment upgrades in certain facilities.

At the same time, these tariffs encourage domestic manufacturing and regional supply diversification, which strengthens long-term supply resilience. Healthcare systems continue to prioritize minimally invasive treatments due to shorter recovery times and better patient outcomes.

Overall, despite short-term cost pressures and supply uncertainties, ongoing technological advancements and expanding clinical expertise are expected to support sustained market growth.

Latest Trends

Increased utilization of digital single-operator cholangioscopy for complex stone management is driving the market.

Digital single-operator cholangioscopy systems have gained wider adoption for direct visualization and targeted lithotripsy of difficult bile duct and pancreatic duct stones during 2024-2025. These platforms enable precise electrohydraulic or laser fragmentation under direct endoscopic guidance.

The 2024-2025 expansion reflects growing availability of reusable and disposable cholangioscopes with improved image quality. Endoscopists benefit from enhanced ability to treat impacted stones and strictures in a single session. The development aligns with preferences for minimally invasive approaches in refractory cases.

Facilities integrate the technology into advanced ERCP suites for complex hepatobiliary interventions. The trend supports reduced reliance on percutaneous or surgical alternatives. Early clinical series demonstrate high technical success rates in large or multiple calculi.

The increased deployment accelerates training initiatives and protocol standardization. Overall, this technological advancement elevates management capabilities for challenging intraductal stone disease.

Regional Analysis

North America is leading the Pancreatic and Bile Duct Stone Management Market

North America accounted for 39.4% of the pancreatic and bile duct stone management market in 2025 as hospitals and gastroenterology centers expanded advanced endoscopic procedures for treating biliary and pancreatic disorders.

High procedural volumes of endoscopic retrograde cholangiopancreatography and minimally invasive interventions have strengthened demand for specialized devices used in stone extraction and duct clearance.

According to the National Institute of Diabetes and Digestive and Kidney Diseases, gallstones affect around 10% to 15% of adults in the United States, creating a large patient pool requiring clinical management of biliary complications.

Gastroenterologists across the region are increasingly adopting advanced endoscopic tools such as lithotripsy systems, extraction baskets, and balloon catheters to improve treatment outcomes. Hospitals are also integrating imaging technologies that enhance procedural accuracy and reduce complication rates.

Rising incidence of obesity and metabolic disorders has contributed to higher prevalence of gallstone-related conditions. Training programs in advanced endoscopy are improving physician expertise and expanding procedural capabilities across healthcare centers.

Medical device manufacturers are introducing innovative solutions that enhance efficiency and patient safety during complex procedures. These developments collectively supported steady expansion of minimally invasive biliary and pancreatic treatment solutions across North America in 2025.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

Asia Pacific is expected to experience strong growth during the forecast period as healthcare systems expand access to advanced gastroenterology services and minimally invasive procedures. Countries such as China, India, Japan, and South Korea are witnessing rising incidence of biliary and pancreatic disorders linked to dietary changes, aging populations, and urban lifestyles.

The World Health Organization has highlighted that digestive diseases contribute significantly to global morbidity, increasing the need for early diagnosis and effective treatment solutions across emerging healthcare systems. Hospitals across the region are expanding endoscopy units and adopting modern equipment for stone management procedures.

Healthcare providers are increasingly using minimally invasive techniques that reduce hospital stay and improve recovery outcomes. Governments are investing in healthcare infrastructure and training programs that strengthen gastroenterology services. Private healthcare providers are also expanding specialized treatment centers focused on digestive diseases.

Medical device companies are introducing cost-effective technologies tailored to high-volume clinical settings. Growing awareness of digestive health and improved access to care are encouraging patients to seek timely treatment.

These developments are expected to accelerate adoption of advanced biliary and pancreatic treatment solutions across Asia Pacific in the coming years.

Key Regions and Countries

North America

- The US

- Canada

Europe

- Germany

- France

- The U.K.

- Italy

- Spain

- Russia & CIS

- Rest of Europe

Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Australia & New Zealand

- Rest of Asia Pacific

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

Latin America

- Brazil

- Mexico

- Rest of Latin America

Key Players Analysis

Key participants in the Pancreatic and Bile Duct Stone Management market expand their footprint by advancing minimally invasive endoscopic technologies, strengthening collaborations with gastroenterologists, and improving device precision for complex stone removal procedures.

Companies invest in innovative lithotripsy systems, extraction baskets, and balloon catheters that enhance procedural efficiency and patient safety during ERCP interventions. They also focus on training programs and clinical partnerships that support adoption of advanced stone management techniques across hospitals and specialty centers.

Boston Scientific Corporation represents a prominent participant in the Pancreatic and Bile Duct Stone Management market and operates as a U.S.-based medical technology company that develops endoscopy devices, interventional tools, and surgical solutions for gastrointestinal procedures.

The company emphasizes continuous innovation in stone management devices and physician education initiatives. Industry competitors continue to introduce next-generation endoscopic tools, expand global distribution, and strengthen clinical collaborations to improve treatment outcomes and drive sustained market growth.

Top Key Players

- Boston Scientific Corporation

- Olympus Corporation

- Cook Medical

- Medtronic plc

- CONMED Corporation

- BD (Becton, Dickinson and Company)

- KARL STORZ SE & Co. KG

- Medi-Globe GmbH

Recent Developments

- In late 2025, Boston Scientific introduced upgrades to its SpyGlass DS II direct visualization platform, enhancing image clarity during endoscopic procedures. The improvements support more accurate targeting and fragmentation of complex biliary stones during electrohydraulic and laser lithotripsy.

- In January 2026, Olympus expanded its accessory range for the PowerSpiral enteroscopy system with new single-use tools designed for deeper access within the small intestine. These accessories help clinicians reach and manage stones in areas that are difficult to access using conventional endoscopic techniques.

Report Scope

Report Features Description Market Value (2025) US$ 1.6 Billion Forecast Revenue (2035) US$ 2.6 Billion CAGR (2026-2035) 5.0% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product (ERCP Catheters, Guidewires, Sphincterotomes, Dilation Balloon Catheters, Extraction Balloon Catheters, Extraction Basket Catheters, Biliary Stents, Self-Expandable Biliary Stents and Others), By End User (Hospitals, Ambulatory Surgical Centers and Specialty Clinics) Regional Analysis North America – The US, Canada; Europe – Germany, France, The U.K., Italy, Spain, Russia & CIS, Rest of Europe; Asia Pacific – China, India, Japan, South Korea, ASEAN, Australia & New Zealand, Rest of Asia Pacific; Middle East & Africa – GCC, South Africa, Rest of Middle East & Africa; Latin America – Brazil, Mexico, Rest of Latin America Competitive Landscape Boston Scientific Corporation, Olympus Corporation, Cook Medical, Medtronic plc, CONMED Corporation, BD, KARL STORZ SE & Co. KG, Medi-Globe GmbH. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Pancreatic and Bile Duct Stone Management MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample

Pancreatic and Bile Duct Stone Management MarketPublished date: March 2026add_shopping_cartBuy Now get_appDownload Sample -

-

- Boston Scientific Corporation

- Olympus Corporation

- Cook Medical

- Medtronic plc

- CONMED Corporation

- BD (Becton, Dickinson and Company)

- KARL STORZ SE & Co. KG

- Medi-Globe GmbH

Our Clients

- 182478

- March 2026