Global Paddle Hair Brush Market Size, Share, Growth Analysis By Material (Synthetic, Organic), By End-User (Women, Men, Children), By Application (Personal, Professional), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181614

- Number of Pages: 249

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

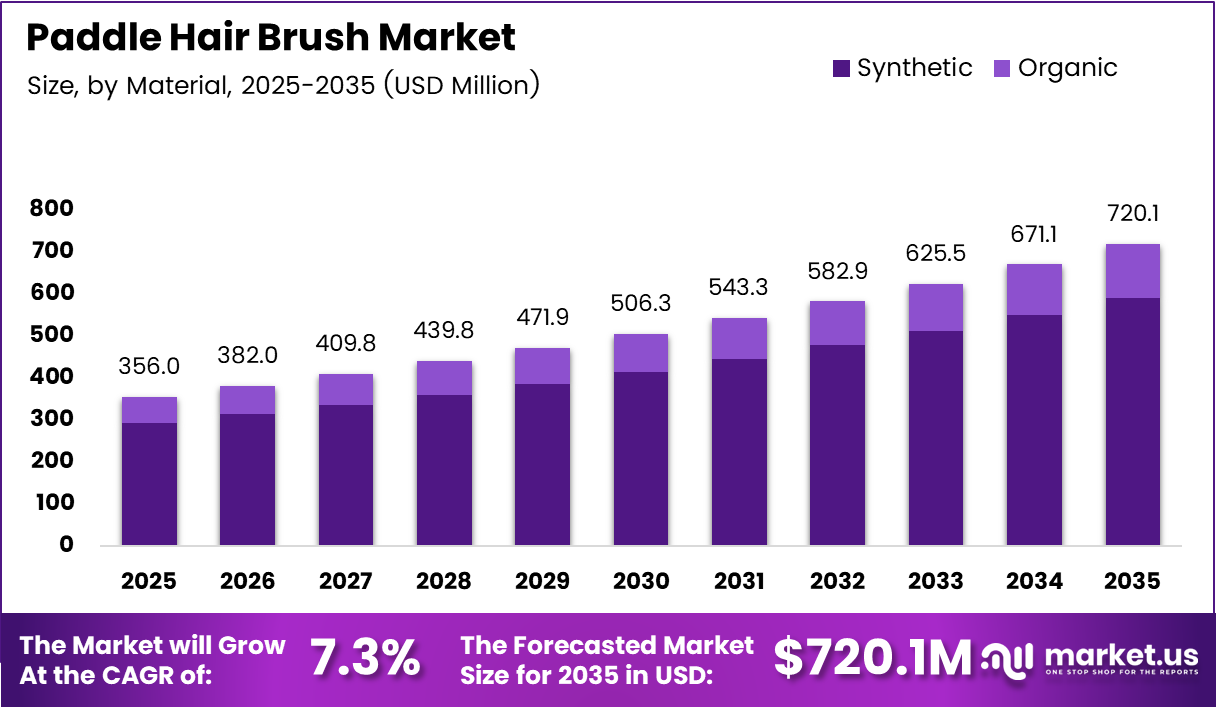

Global Paddle Hair Brush Market size is expected to be worth around USD 720.1 Million by 2035 from USD 356.0 Million in 2025, growing at a CAGR of 7.3% during the forecast period 2026 to 2035.

The paddle hair brush market covers wide, flat-surfaced brushes designed for detangling, smoothing, and styling medium to long hair. These tools serve both personal and professional users, spanning synthetic and organic material variants across women, men, and children segments.

Consumer behavior is the primary engine here. Buyers no longer treat hair brushes as commodity items. They actively seek tools that reduce breakage, support scalp health, and replicate salon-quality results at home. This shift in expectations elevates average selling prices and creates durable demand for premium formats.

E-commerce platforms have restructured how these products reach buyers. Online channels remove geographic barriers, allow niche brands to compete alongside established names, and support detailed product education — all of which accelerate conversion for higher-priced paddle brush SKUs.

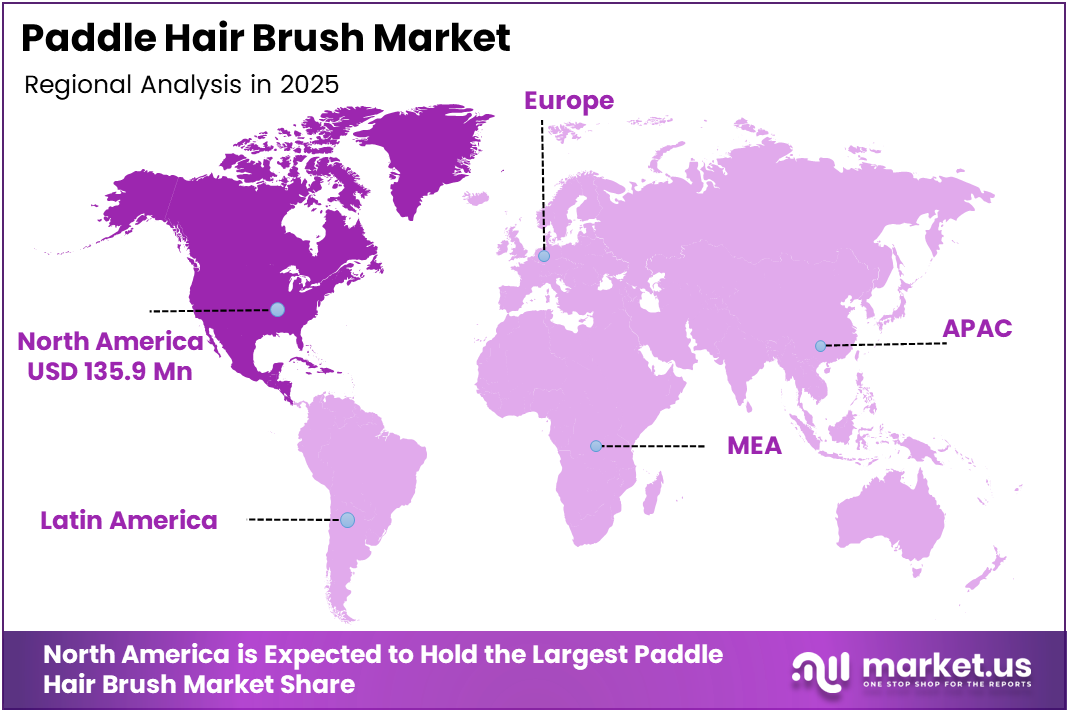

North America leads the global market, holding a 38.2% share valued at approximately USD 135.9 Million. This reflects mature grooming culture, high per-capita spending on personal care, and strong retail infrastructure — conditions that make premium paddle brushes a viable everyday purchase rather than an occasional upgrade.

According to the National Institutes of Health (NCBI), 80% of women in the U.S. report using hair styling tools as part of their regular grooming routine. This near-universal adoption rate signals that paddle brushes compete in a high-frequency, repeat-purchase category — not a discretionary one.

Additionally, according to NCBI, 33% of women report experiencing hair breakage or damage, which directly influences their choice of gentler grooming tools. This pain point translates into a concrete purchase trigger — consumers actively migrate toward detangling-friendly formats, making the paddle brush a functional solution rather than a lifestyle accessory.

Key Takeaways

- The global Paddle Hair Brush Market was valued at USD 356.0 Million in 2025 and is forecast to reach USD 720.1 Million by 2035.

- The market grows at a CAGR of 7.3% during the forecast period 2026 to 2035.

- North America dominates the market with a 38.2% share, valued at USD 135.9 Million.

- By Material, Synthetic leads with 81.2% market share in 2025.

- By End-User, Women hold the largest share at 67.5%.

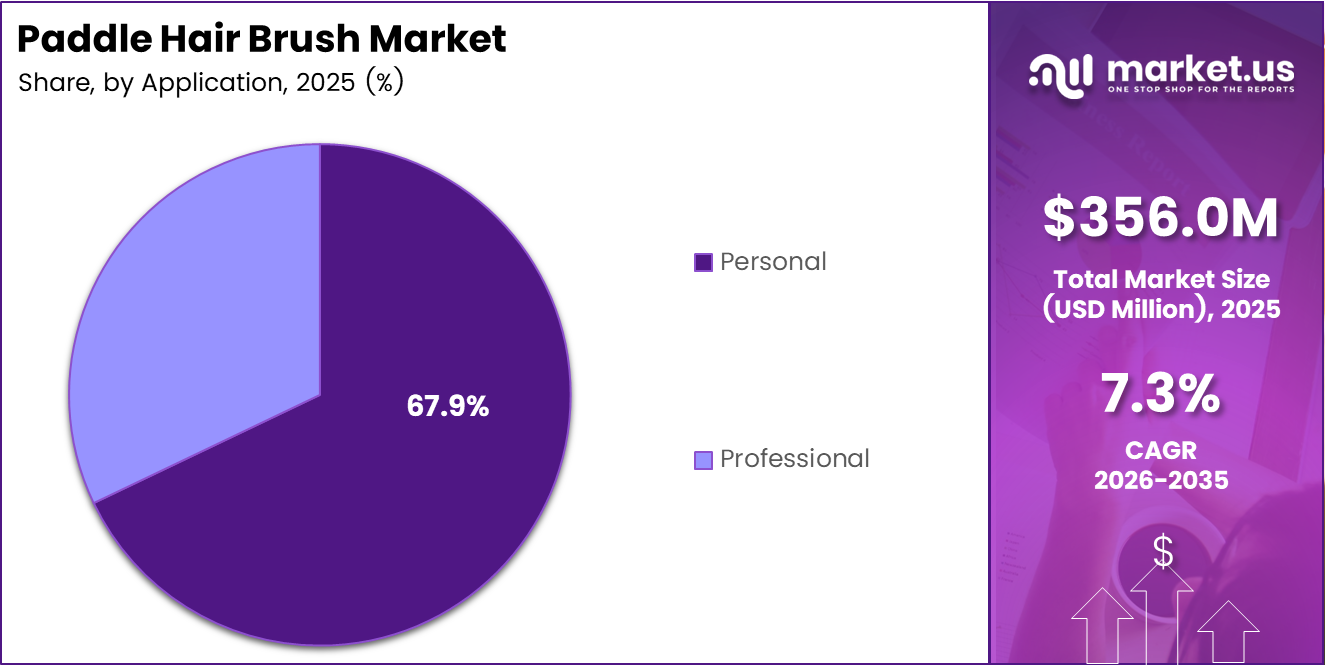

- By Application, Personal use accounts for 67.9% of total market demand.

Product Analysis

Synthetic dominates with 81.2% due to cost efficiency and broad consumer availability.

In 2025, Synthetic held a dominant market position in the By Material segment of the Paddle Hair Brush Market, with an 81.2% share. Synthetic bristles and frames offer consistent quality at accessible price points, making them the default choice for mass-market buyers across retail and e-commerce channels. Their durability and ease of manufacture sustain high volumes globally.

Organic brushes carry a structural premium within the material segment. Natural bristles — typically boar hair — and wood-based handles appeal to consumers in the clean beauty segment who prioritize scalp health and sustainable sourcing. However, organic formats remain a niche category constrained by higher production costs and limited mass-retail shelf presence.

End-User Analysis

Women dominate with 67.5% due to higher grooming frequency and styling tool dependency.

In 2025, Women held a dominant market position in the By End-User segment of the Paddle Hair Brush Market, with a 67.5% share. Women account for the majority of paddle brush purchases due to longer average hair length, higher grooming routine frequency, and stronger engagement with styling and detangling products. This segment drives both volume and premium SKU adoption.

Men represent an emerging but structurally underdeveloped segment. Male grooming awareness has expanded across major markets, but paddle brush adoption among men remains limited by narrower product ranges and lower styling routine engagement. Growth here depends on targeted product positioning and influencer-led education in the men’s grooming category.

Children as a sub-segment is purchase-driven by parents prioritizing gentle detangling solutions. Soft-bristle paddle brushes designed for fine or curly children’s hair occupy a specific functional niche. However, this segment’s size constrains its revenue contribution — parents typically purchase lower-priced formats, reducing average order value relative to the Women segment.

Application Analysis

Personal use dominates with 67.9% due to household grooming routine prevalence.

In 2025, Personal application held a dominant market position in the By Application segment of the Paddle Hair Brush Market, with a 67.9% share. Consumer preference for salon-quality results at home has elevated demand for professional-grade paddle brushes within personal use settings. This blurring of professional and personal categories sustains volume at higher price tiers.

Professional application encompasses salons, stylists, and beauty professionals who require durable, high-performance brushes for daily use across multiple clients. This segment favors brand credibility and product consistency over price sensitivity. Professional buyers often act as influencers — their tool choices directly shape consumer purchasing behavior in the personal segment.

Key Market Segments

By Material

- Synthetic

- Organic

By End-User

- Women

- Men

- Children

By Application

- Personal

- Professional

Drivers

Hair Breakage Concerns and Home Styling Adoption Accelerate Paddle Brush Demand

Consumer awareness of hair damage has become a measurable purchase driver. Buyers now actively seek tools that reduce breakage during detangling — a functional requirement that directly positions paddle brushes ahead of conventional round or cushion brush formats. According to the APA, over 50% of consumers cite personal appearance as a key factor in daily confidence, reinforcing habitual grooming investment.

The shift toward home-based professional styling routines has further expanded the addressable buyer pool. Consumers replicate salon outcomes using the same tool categories professionals use — and paddle brushes sit at the center of that transition. In February 2025, Cécred expanded into hair tools alongside its core product line, signaling that beauty brands recognize the brush category as a natural extension of consumer hair care loyalty.

E-commerce platforms have structurally lowered the barrier for premium paddle brush discovery and purchase. Online channels allow brands to demonstrate product benefits through video content and user reviews — formats that convert education into sales more effectively than traditional retail shelf placement. This distribution shift benefits both premium incumbents and new entrants competing on product differentiation.

Restraints

Price Sensitivity and Low-Cost Competition Suppress Premium Paddle Brush Conversion

The paddle hair brush market faces a persistent structural tension: most buyers treat grooming tools as low-involvement purchases, resisting premium pricing without clear functional evidence. According to the Bureau of Labor Statistics (BLS), 60% of consumers are price-sensitive when purchasing personal care products. This majority behavior limits the addressable market for premium and mid-tier paddle brush brands.

Counterfeit and unbranded paddle brushes flood mass-market and online channels at significantly lower price points, eroding perceived value differentiation. These products mimic the physical form of established brands without the material quality or bristle performance. For buyers who cannot evaluate brush quality before purchase — particularly online — price becomes the default selection criterion, disadvantaging legitimate premium manufacturers.

Additionally, over 65% of women regularly use electrical styling devices such as dryers and straighteners, according to NCBI. This behavior patterns positions paddle brushes as accessories rather than primary tools, reducing purchase urgency and limiting how frequently consumers trade up to higher-priced brush formats. In July 2025, Primark’s budget detangling paddle brush gained viral traction among consumers with thick hair — confirming that the value end of the market captures significant attention even among style-aware buyers.

Growth Factors

Sustainability Demand, Male Grooming Expansion, and Technology Innovation Open New Revenue Segments

The clean beauty movement has translated into concrete product demand for eco-friendly paddle brushes made from bamboo, recycled plastics, and natural bristles. Buyers in this segment demonstrate higher willingness to pay for certified sustainable materials — a pricing dynamic that benefits brands with credible supply chain transparency. This segment creates a premium tier within the organic material category that remains undercrowded relative to demand signals.

According to UNCTAD, global e-commerce accounted for 19% of total retail sales in 2023. For hair tool brands, this means nearly one in five consumer purchases now occurs through a channel that supports detailed product storytelling, targeted advertising, and direct-to-consumer margin capture. Brands that build e-commerce-native product strategies gain structural pricing and reach advantages over those dependent on traditional retail distribution.

Male grooming awareness is creating a previously underdeveloped consumer segment for hair styling tools. As men adopt more structured grooming routines, paddle brush formats — particularly those marketed for scalp health and natural styling — gain entry points into a segment that currently accounts for a small fraction of market volume. Innovation in anti-static and scalp-massaging brush technologies further differentiates product offerings and supports trade-up behavior across all buyer segments.

Emerging Trends

Clean Beauty Aesthetics, Ergonomic Innovation, and Multi-Function Formats Reshape Buyer Expectations

Wooden and natural bristle paddle brushes have moved from niche to mainstream within the clean beauty segment. Buyers in this category evaluate brushes on material sourcing, not just performance — a shift that creates brand differentiation opportunities for manufacturers with transparent supply chains. In May 2024, BondiBoost launched the Infrared Bounce Brush, a heat-integrated styling brush that sold out rapidly, demonstrating strong buyer appetite for functional innovation in the brush category.

According to PwC, 76% of consumers consider product functionality — such as damage prevention — before making a purchase decision. This behavior confirms that buyers are not purchasing on aesthetics alone. Brands that lead with measurable functional claims, such as breakage reduction rates or detangling efficiency data, convert more effectively than those relying on visual or brand-only positioning.

Additionally, PwC data shows that 35% of consumers actively look for ergonomic or comfort-based features in personal care tools. This preference drives demand for paddle brushes with redesigned handle shapes, non-slip grips, and reduced wrist strain during use. Younger consumers further intensify this trend by seeking customizable aesthetics and social media-worthy product designs — creating a dual demand for both function and visual identity in the same purchase.

Regional Analysis

North America Dominates the Paddle Hair Brush Market with a Market Share of 38.2%, Valued at USD 135.9 Million

North America holds a 38.2% share of the global paddle hair brush market, valued at USD 135.9 Million. The region’s leadership reflects mature personal care spending habits, strong retail and e-commerce infrastructure, and high consumer awareness of hair health. Premium paddle brush brands find their most receptive buyer base here, supported by both professional salon networks and informed household buyers.

Europe Paddle Hair Brush Market Trends

Europe represents a structurally strong market for paddle brushes, driven by established grooming cultures in the UK, Germany, and France. Consumer preference for quality-made grooming tools with durable materials aligns with the premium and organic brush segments. Sustainability regulations across the EU also push manufacturers toward eco-friendly material sourcing, benefiting brands already positioned in the clean beauty segment.

Asia Pacific Paddle Hair Brush Market Trends

Asia Pacific holds significant volume potential, particularly across China, India, and South Korea, where rising disposable incomes and beauty industry expansion are reshaping grooming tool adoption. South Korea’s beauty culture exports — amplified through social media — drive product awareness beyond its borders. The region’s large middle-class population creates a high-volume opportunity at mid-range price points.

Middle East and Africa Paddle Hair Brush Market Trends

The Middle East and Africa market remains at an earlier stage of paddle brush adoption, but urbanization and rising personal care spending across GCC countries signal directional change. Younger, urban demographics in the UAE and Saudi Arabia show stronger alignment with global grooming trends. Retail channel development and brand distribution infrastructure remain the primary barriers to faster category penetration.

Latin America Paddle Hair Brush Market Trends

Latin America, led by Brazil and Mexico, benefits from strong cultural emphasis on hair care and styling. Brazil in particular has one of the highest per-capita salon densities globally, which supports professional segment demand for quality paddle brushes. However, price sensitivity across the broader consumer base and currency volatility constrain premium segment growth, directing most volume toward the mid-market and synthetic material formats.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Company Insights

G.B. Kent & Sons Plc. occupies a distinct strategic position as one of the world’s oldest brush manufacturers, with a heritage dating back centuries. This legacy allows the brand to command premium pricing in quality-conscious markets, particularly in Europe and North America. Their positioning as a craft-led manufacturer insulates them from mid-market price competition, though it limits volume scalability in cost-sensitive regions.

Denman has built durable market presence through consistent product performance across both professional salon and consumer channels. Their paddle and detangling brush formats maintain strong shelf presence in professional beauty supply networks — a distribution advantage that drives trial among salon professionals who then influence consumer purchasing behavior. This dual-channel strategy creates compounding brand reinforcement across segments.

Ningbo Biofriendly International Trading Co., Ltd. represents the manufacturing-led competitive model — operating at scale from China with cost structures that allow aggressive pricing across international markets. Their strategic advantage lies in supply chain efficiency and product volume capacity. However, brand equity remains limited compared to Western heritage players, making differentiation dependent on private-label partnerships and OEM relationships.

L’Oréal S.A. brings cross-category leverage into the paddle brush segment, integrating hair tools within broader hair care ecosystems. Their ability to bundle brushes with hair treatment and styling product lines creates purchase occasions that standalone brush brands cannot replicate. In December 2024, BIC’s acquisition of Tangle Teezer for approximately €200 million signals that large consumer goods players view the brush category as a strategic growth asset worth significant capital allocation.

Key Players

- G.B. Kent & Sons Plc.

- Denman

- Ningbo Biofriendly International Trading Co., Ltd.

- L’Oréal S.A.

- BaByliss

- TINA BEAUTY CO., LTD.

- SHASH

- Tong Fong Brush Factory CO., Ltd.

- Spornette International Inc.

- Revlon, Inc.

Recent Developments

- July 2025 – Primark launched a budget-friendly detangling paddle hairbrush targeting consumers with thick hair. The product gained viral popularity rapidly, confirming strong consumer demand for accessible, functional grooming tools at value price points.

- November 2025 – Premium brands Mason Pearson and Sisley Paris continued promoting high-end paddle-style brushes with a focus on durability and scalp care. Their sustained investment in premium positioning reflects confidence in a bifurcated market where luxury grooming tools maintain a dedicated buyer base.

Report Scope

Report Features Description Market Value (2025) USD 356.0 Million Forecast Revenue (2035) USD 720.1 Million CAGR (2026-2035) 7.3% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Material (Synthetic, Organic), By End-User (Women, Men, Children), By Application (Personal, Professional) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape G.B. Kent & Sons Plc., Denman, Ningbo Biofriendly International Trading Co., Ltd., L’Oréal S.A., BaByliss, TINA BEAUTY CO., LTD., SHASH, Tong Fong Brush Factory CO., Ltd., Spornette International Inc., Revlon, Inc. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- G.B. Kent & Sons Plc.

- Denman

- Ningbo Biofriendly International Trading Co., Ltd.

- L'Oréal S.A.

- BaByliss

- TINA BEAUTY CO., LTD.

- SHASH

- Tong Fong Brush Factory CO., Ltd.

- Spornette International Inc.

- Revlon, Inc.

Our Clients

- 181614

- Mar 2026