Global Oyster And Clam Market Size, Share, And Industry Analysis Report By Type (Clam Type (Hard Clam, Taca Clam, Stimpson Surf), Oyster Type (Slipper Oyster, Pacific Cupped Oyster)), By Form (Fresh, Frozen, Canned), By Distribution Channel (Foodservice, Retail, Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Statistics, Trends and Forecast 2026-2035

- Published date: March 2026

- Report ID: 181655

- Number of Pages: 288

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

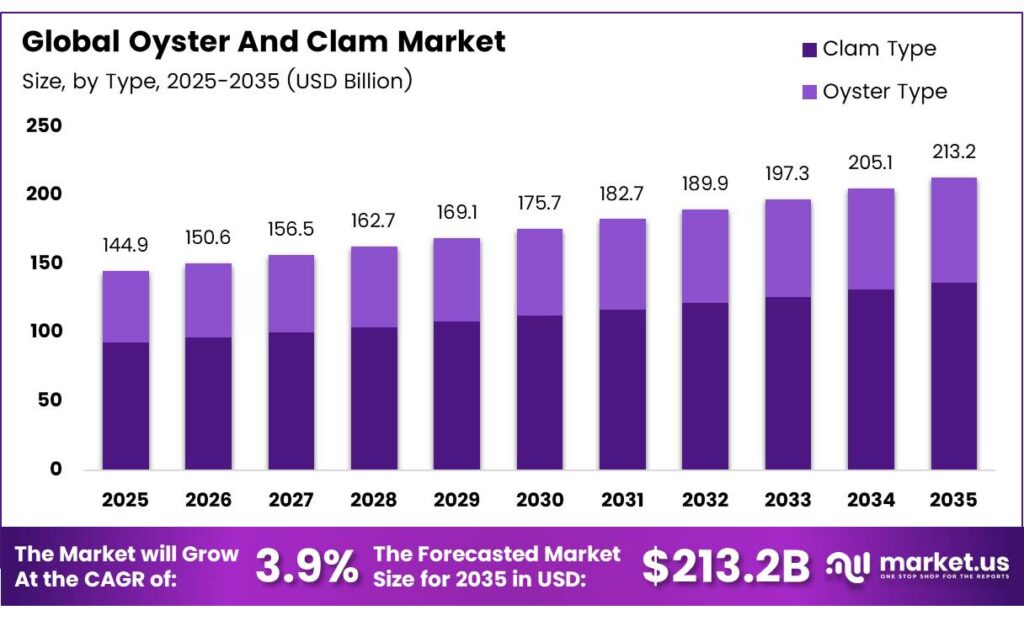

The Global Oyster and Clam Market size is expected to be worth around USD 213.2 billion by 2035 from USD 144.9 billion in 2025, growing at a CAGR of 3.9% during the forecast period 2026 to 2035.

The oyster and clam market covers the commercial cultivation, harvesting, processing, and distribution of bivalve shellfish species. These products serve a wide range of end-use applications. Moreover, they play a critical role in both food security and coastal aquaculture economies worldwide.

Oysters and clams rank among the most nutritionally dense seafood options available. They deliver high concentrations of zinc, iron, omega-3 fatty acids, and lean protein. Consequently, health-conscious consumers increasingly include shellfish in their regular diets across urban and suburban markets.

South Korea exported US$80 million worth of oysters in 2023, ranking as the world’s third-largest oyster exporter behind France and China. This export performance reflects strong global demand for premium shellfish products and highlights Asia’s growing role in international seafood trade flows.

The United States shellfish aquaculture segment generated US$294.6 million in 2023, produced by 28.1 million pounds of oysters, 8.0 million pounds of clams, and 650,000 pounds of mussels. This output confirms North America as a significant and commercially active shellfish production zone.

The European Union shellfish aquaculture segment recorded a turnover of €1.27 billion in 2023, with 553,000 tonnes in sales volume. Oysters, mussels, and clams accounted for 99% of EU shellfish aquaculture volume and value, confirming Europe’s deep structural dependence on bivalve species.

Aquaculture operations drive the majority of the global supply for both oysters and clams. Farmers cultivate these species in controlled coastal environments using cage, longline, and bottom culture methods. Additionally, modern hatchery systems now support year-round production and more consistent meat quality at a commercial scale.

Key Takeaways

- The Global Oyster and Clam Market is valued at USD 144.9 billion in 2025 and is projected to reach USD 213.2 billion by 2035, at a CAGR of 3.9% during the forecast period 2026 to 2035.

- Clam Type dominates with a market share of 56.2% in 2025.

- Fresh holds the leading position with a market share of 59.6% in 2025.

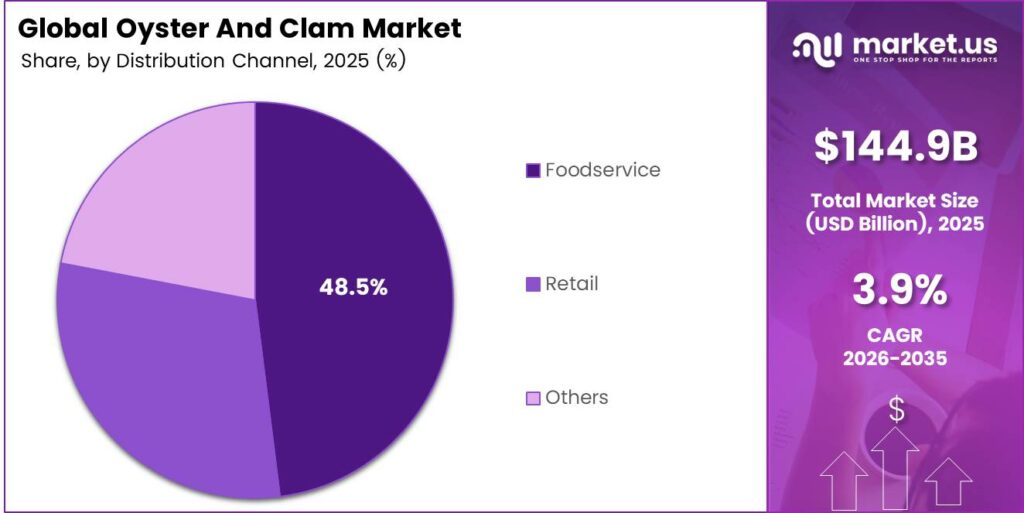

- Foodservice leads the segment with a share of 48.5% in 2025.

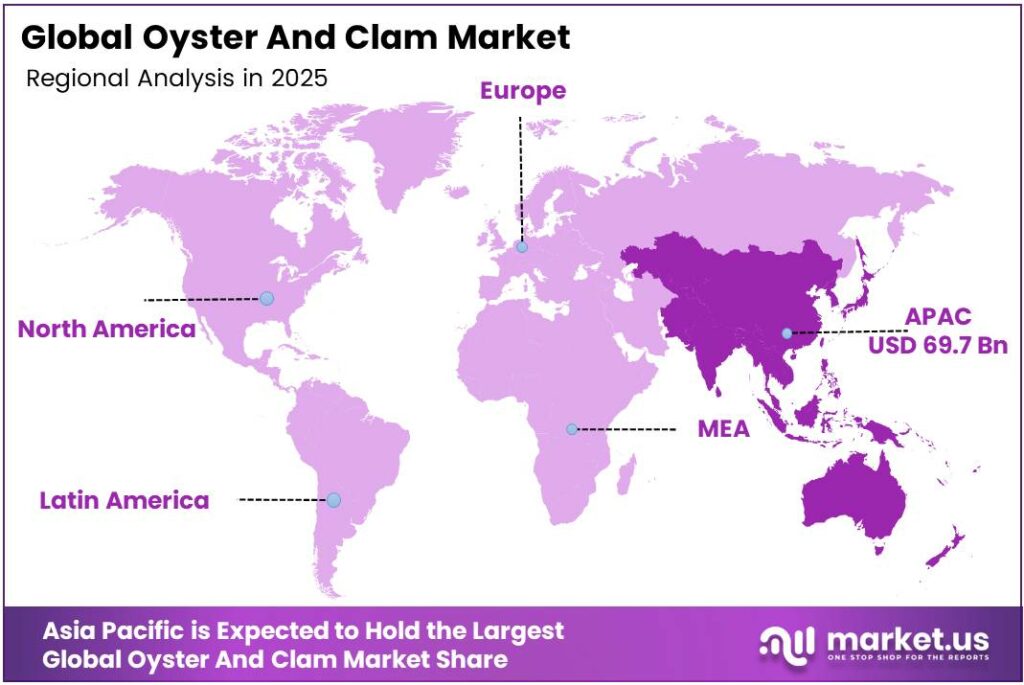

- Asia Pacific dominates the regional landscape with a market share of 48.1%, valued at USD 69.7 billion in 2025.

By Type Analysis

Clam Type dominates with 56.2% due to high aquaculture volume and widespread food service demand.

In 2025, Clam Type held a dominant market position in the By Type segment of the Oyster and Clam Market, with a 56.2% share. Clams benefit from large-scale commercial aquaculture systems across Asia and North America. Additionally, their affordability and versatility in culinary applications make them a preferred choice for processors and food service operators globally.

Oyster Type held a strong secondary position in the By Type segment, supported by premiumization trends and growing raw bar culture in urban hospitality markets. Oysters command higher average selling prices than clams. Therefore, oyster producers benefit from improving margins even as total volume remains lower than clam output.

By Form Analysis

Fresh dominates with 59.6% due to strong consumer preference for live and chilled shellfish products.

In 2025, Fresh held a dominant market position in the By Form segment of the Oyster and Clam Market, with a 59.6% share. Consumers across premium dining and retail channels consistently prefer live or chilled shellfish for quality and taste reasons. Moreover, the expansion of cold chain infrastructure globally continues to support fresh product distribution across longer distances.

Frozen oysters and clams serve a growing segment of convenience-oriented buyers in retail and food service. Freezing extends shelf life significantly and reduces waste across distribution networks. Consequently, producers increasingly invest in individually quick-frozen processing lines to capture demand from inland markets where fresh shellfish availability remains limited.

Canned oysters and clams represent a stable and accessible format for price-sensitive consumers globally. Canned formats offer extended shelf life, easy storage, and consistent flavor profiles. Additionally, innovation in value-added canned products such as smoked oysters and seasoned clams is creating new demand opportunities in both traditional and emerging retail markets.

By Distribution Channel Analysis

Foodservice dominates with 48.5% due to rising restaurant consumption and premium dining experiences.

In 2025, Foodservice held a dominant market position in the By Distribution Channel segment of the Oyster and Clam Market, with a 48.5% share. Restaurants, hotels, and catering companies drive substantial shellfish volume. Moreover, the rapid growth of raw oyster bars and tasting menus in urban hospitality sectors continues to support foodservice channel leadership globally.

Retail channels serve home cooks and health-conscious consumers who purchase fresh, frozen, or canned shellfish for household preparation. Supermarkets and specialty seafood retailers actively expand their shellfish assortments. Additionally, e-commerce platforms now offer direct-to-consumer shellfish delivery, broadening retail reach well beyond traditional store-based purchasing patterns.

Key Market Segments

By Type

- Clam Type

- Hard Clam

- Taca Clam

- Stimpson Surf

- Oyster Type

- Slipper Oyster

- Pacific Cupped Oyster

By Form

- Fresh

- Frozen

- Canned

By Distribution Channel

- Foodservice

- Retail

- Others

Emerging Trends

Raw Oyster Bars and Urban Dining Drive New Demand Patterns

Urban hospitality sectors across North America, Europe, and the Asia Pacific are rapidly expanding raw oyster bar concepts. Restaurants and boutique tasting venues attract premium-paying consumers seeking curated shellfish experiences. Great Britain imported 350 tonnes of Pacific oysters from Ireland in 2024, reflecting cross-border demand for traceable, premium shellfish within established trade corridors.

Blockchain Traceability and HPP Innovation Reshape Supply Chains

Shellfish producers increasingly adopt blockchain-enabled traceability systems to verify farm origin and product safety from harvest to the consumer’s plate. Additionally, High-Pressure Processing technology extends raw product shelf life without heat treatment. Consequently, these twin innovations address both consumer trust requirements and food safety compliance needs across global distribution networks.

Drivers

Rising Global Demand for Protein-Rich Seafood Fuels Market Expansion

Developing economies across Asia and Africa show a rapidly growing consumer appetite for premium protein-rich seafood. China’s seafood imports reached 4.6 million metric tons worth US$18.8 billion in 2023, with mollusks contributing to the surge in higher-value seafood demand. This trend directly benefits oyster and clam producers targeting export-oriented supply chains.

Sustainable Aquaculture Certifications and E-Commerce Channels Accelerate Growth

Aquaculture certification schemes such as ASC and BAP drive consumer confidence in sustainably farmed shellfish products. Retailers and foodservice buyers increasingly require certified supply to meet procurement commitments. Moreover, the expansion of e-commerce platforms offering ready-to-eat packaged oyster products extends market reach to consumers who previously lacked access to fresh shellfish through traditional retail channels.

Restraints

Stringent Regulatory Frameworks Create Operational Complexity for Producers

Harvesting zone restrictions and water quality standards impose significant compliance burdens on shellfish producers worldwide. Regulatory bodies in the EU, the US, and the Asia Pacific enforce strict testing protocols before products enter commercial channels. Therefore, producers operating in multiple jurisdictions face higher administrative costs and production delays that reduce overall market efficiency and profitability.

Ocean Acidification and Climate Risks Threaten Shellfish Population Stability

Rising sea temperatures and ocean acidification directly harm shellfish larvae and shell formation, reducing aquaculture yields. China’s clam marine aquaculture production reached 4.4491 million tons in 2023, representing 27.03% of total shellfish marine aquaculture output. However, climate-driven environmental stress increasingly threatens the sustainability of such large-scale production systems globally.

Growth Factors

Triploid Oysters and Advanced Hatchery Technologies Expand Commercial Opportunities

Triploid oyster cultivation enables year-round production by eliminating summer spawning cycles that reduce meat quality. Hatchery operators increasingly supply disease-resistant seed stock to commercial farmers. Taylor Shellfish derived 40% of its pre-COVID business from Asian markets in 2021, demonstrating how technology-backed production capacity supports recovery and growth in premium export segments.

Value-Added Products and Untapped Regional Markets Drive Long-Term Revenue

Producers actively develop value-added shellfish products such as canned smoked oysters, marinated clam snacks, and ready-to-eat formats. Angel Seafood recorded Asia export sales of A$133,200 in FY2021, signaling early-stage but growing export market development for premium Australian oysters. Additionally, strategic entry into regions with developing aquaculture infrastructure creates long-term expansion opportunities for established producers and processors.

Regional Analysis

Asia Pacific Dominates the Oyster and Clam Market with a Market Share of 48.1%, Valued at USD 69.7 Billion

Asia Pacific leads the global oyster and clam market with a 48.1% share valued at USD 69.7 billion in 2025. China, Japan, and South Korea anchor regional production and consumption. Moreover, China alone accounts for an enormous share of global clam aquaculture output, making the Asia Pacific the undisputed center of global shellfish supply and trade activity.

North America maintains a well-developed commercial shellfish industry supported by strong regulatory oversight and premium consumer demand. The United States and Canada both operate active oyster and clam aquaculture sectors serving domestic foodservice and retail channels. Additionally, growing direct-to-consumer e-commerce platforms are expanding market access for small and mid-scale shellfish producers across the region.

The Middle East and Africa represent emerging markets for imported premium shellfish products. Growing hospitality industries in Gulf Cooperation Council countries drive foodservice demand for oysters and clams. However, limited domestic aquaculture infrastructure means the region depends heavily on imports from Asia Pacific and European producers to fulfill rising consumer demand.

Latin America hosts developing shellfish aquaculture industries in Chile, Brazil, and Mexico. These markets benefit from long coastlines and suitable marine environments for bivalve cultivation. Consequently, increasing investment in aquaculture infrastructure and export-oriented processing capacity positions Latin America as a future contributor to global oyster and clam supply networks.

Key Regions and Countries

North America

- US

- Canada

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Clearwater Seafoods operates as one of North America’s largest vertically integrated seafood companies with a strong presence in shellfish harvesting and processing. The company manages its own fishing fleet and processing facilities, enabling consistent quality control across its product range. Moreover, Clearwater’s established export relationships with Asian and European buyers position it well within premium shellfish trade channels.

Colville Bay Oyster Co. Ltd specializes in premium hand-harvested oysters from Prince Edward Island, Canada, and has built a strong reputation for product quality and traceability. The company supplies high-end restaurants and specialty retailers across North America. Additionally, its focus on sustainable harvesting practices and direct relationships with foodservice buyers reinforces its competitive positioning in the premium shellfish segment.

High Liner Foods operates as a leading North American seafood processor with a diversified portfolio that includes shellfish alongside finfish and value-added products. The company distributes through foodservice and retail channels across Canada and the United States. Consequently, its broad distribution network and processing scale give it competitive advantages in meeting institutional and retail buyer requirements consistently.

Island Creek Oysters has established a strong direct-to-consumer and premium foodservice brand centered on sustainably farmed oysters from Duxbury Bay, Massachusetts. The company runs farm tours, oyster tasting events, and a direct shipping program. Therefore, its brand-building approach differentiates it from commodity shellfish producers and captures premium pricing in both online retail and top-tier restaurant markets.

Top Key Players in the Market

- Clearwater Seafoods

- Colville Bay Oyster Co. Ltd

- High Liner Foods

- Island Creek Oysters

- Mazetta Company, LLC

- Pacific Seafood

- Pangea Shellfish Company

- Royal Hawaiian Seafood

- Taylor Shellfish Farms

- Ward Oyster Company

- Woodstown Bay Shellfish Ltd

Recent Developments

- In 2025, Clearwater reported strong recoveries in catch rates for clams, which helped offset revenue declines from other factors like poor scallop catches and the exit from inshore lobster operations. Sold its Macduff Shellfish land-based processing operations (Scotland) and entered a strategic alliance with Seafood Ecosse to continue involvement in the business.

- In 2025, Island Creek Oysters announced a new seasonal outdoor raw bar in Boston’s Seaport District (99 Autumn Lane; opened early, temporary/warmer-months only). It features farm-grown oysters plus tinned fish, caviar, and snacks (e.g., clam dip), mirroring the Duxbury farm raw bar.

Report Scope

Report Features Description Market Value (2025) USD 144.9 Billion Forecast Revenue (2035) USD 213.2 Billion CAGR (2026-2035) 3.9% Base Year for Estimation 2025 Historic Period 2020-2024 Forecast Period 2026-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Clam Type (Hard Clam, Taca Clam, Stimpson Surf), Oyster Type (Slipper Oyster, Pacific Cupped Oyster)), By Form (Fresh, Frozen, Canned), By Distribution Channel (Foodservice, Retail, Others) Regional Analysis North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) Competitive Landscape Clearwater Seafoods, Colville Bay Oyster Co. Ltd, High Liner Foods, Island Creek Oysters, Mazetta Company LLC, Pacific Seafood, Pangea Shellfish Company, Royal Hawaiian Seafood, Taylor Shellfish Farms, Ward Oyster Company, Woodstown Bay Shellfish Ltd Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Clearwater Seafoods

- Colville Bay Oyster Co. Ltd

- High Liner Foods

- Island Creek Oysters

- Mazetta Company, LLC

- Pacific Seafood

- Pangea Shellfish Company

- Royal Hawaiian Seafood

- Taylor Shellfish Farms

- Ward Oyster Company

- Woodstown Bay Shellfish Ltd

Our Clients

- 181655

- March 2026