Global Organic Semiconductor Market Size, Share Report By Type (Polyethylene (Polymers), Poly Aromatic Ring (Small Molecules), Copolymer), By Application (System Component, Organic Photovoltaic (OPV), OLED Lighting, Printed Batteries, Organic RFID Tags, Display Applications, Others), By Regional Analysis, Global Trends and Opportunity, Future Outlook By 2025-2034

- Published date: Dec. 2025

- Report ID: 169005

- Number of Pages: 293

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

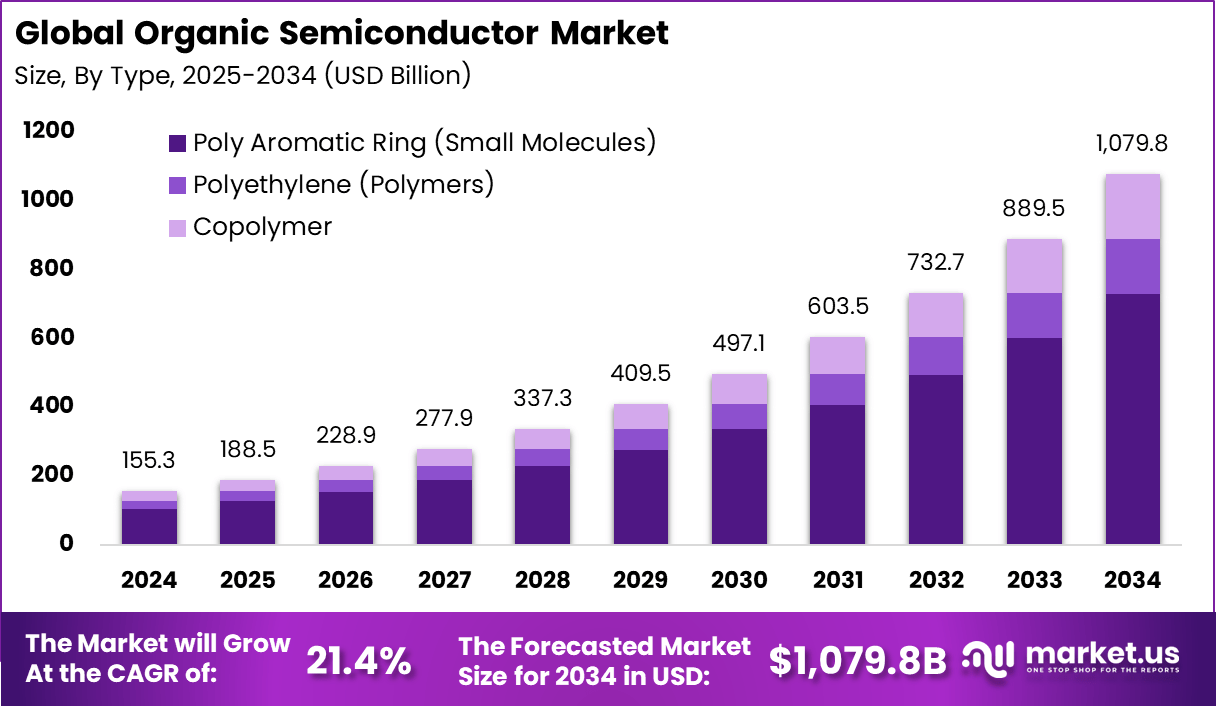

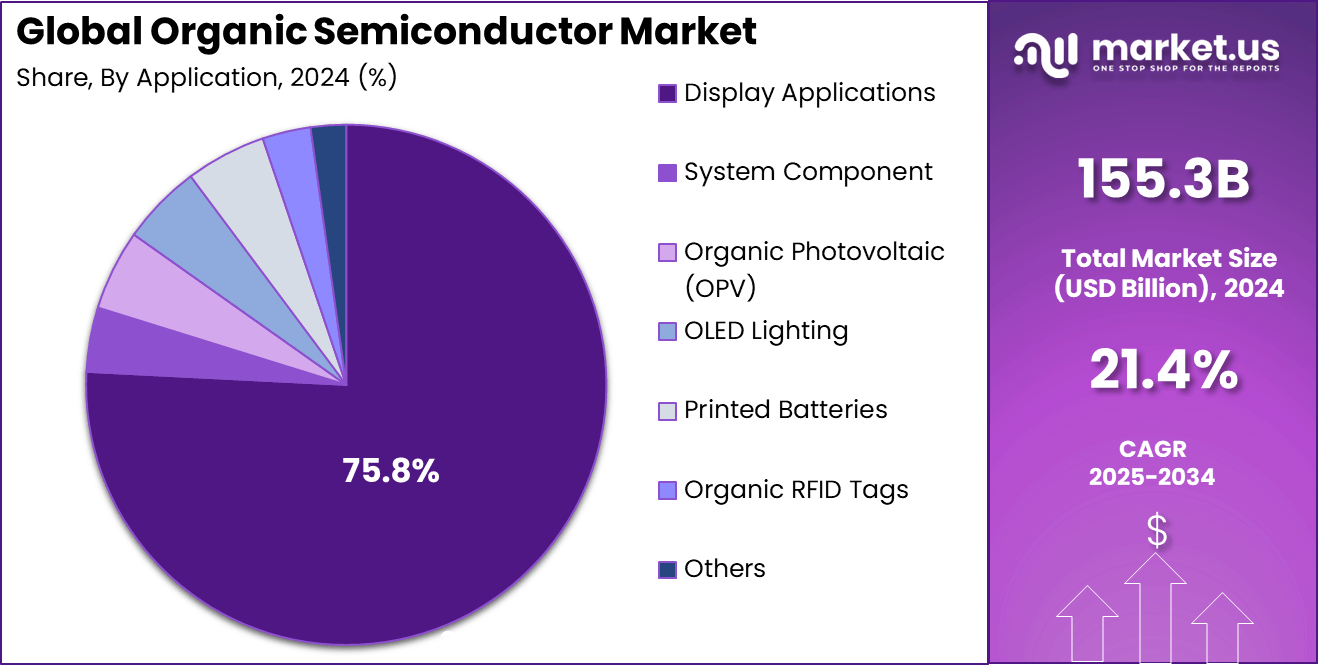

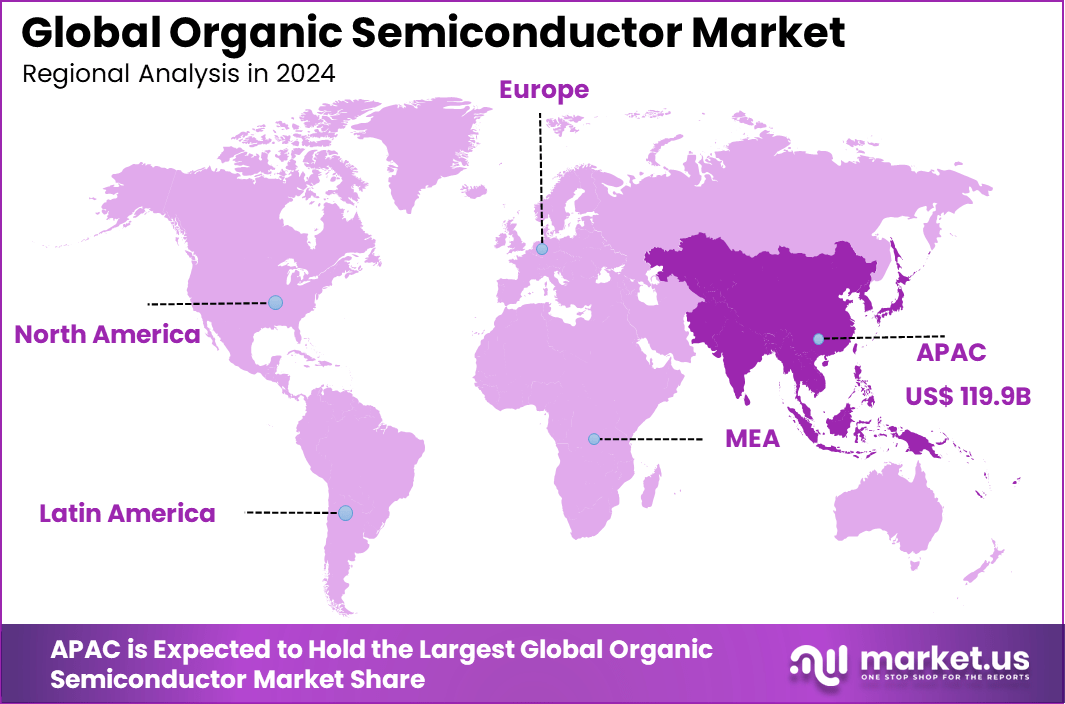

The Global Organic Semiconductor Market generated USD 155.3 billion in 2024 and is predicted to register growth from USD 188.5 billion in 2025 to about USD 1,079.8 billion by 2034, recording a CAGR of 21.4% throughout the forecast span. In 2024, APAC held a dominan market position, capturing more than a 77.2% share, holding USD 119.9 Billion revenue.

The organic semiconductor market has expanded as industries explore lightweight, flexible and cost efficient electronic materials for next generation devices. Growth reflects rising interest in organic thin film technologies, printable electronics and low temperature processing methods that support new product designs. Organic semiconductors are now used in displays, sensors, photovoltaic modules and emerging wearable systems.

The growth of the market can be attributed to increasing demand for flexible electronics, rising focus on sustainable materials and advances in organic thin film fabrication. Manufacturers prefer organic semiconductors for their ability to enable lightweight, bendable and energy efficient components. Progress in printing techniques and material stability further supports wider adoption.

Top Market Takeaways

- Poly aromatic ring small molecules accounted for 67.5%, reflecting their strong suitability for high-performance organic semiconductor fabrication.

- Display applications held 75.8%, showing that most commercial demand continues to come from OLED panels, flexible screens, and next-generation visual interfaces.

- Asia Pacific captured 77.2%, supported by large-scale production ecosystems and strong government-backed electronics manufacturing clusters.

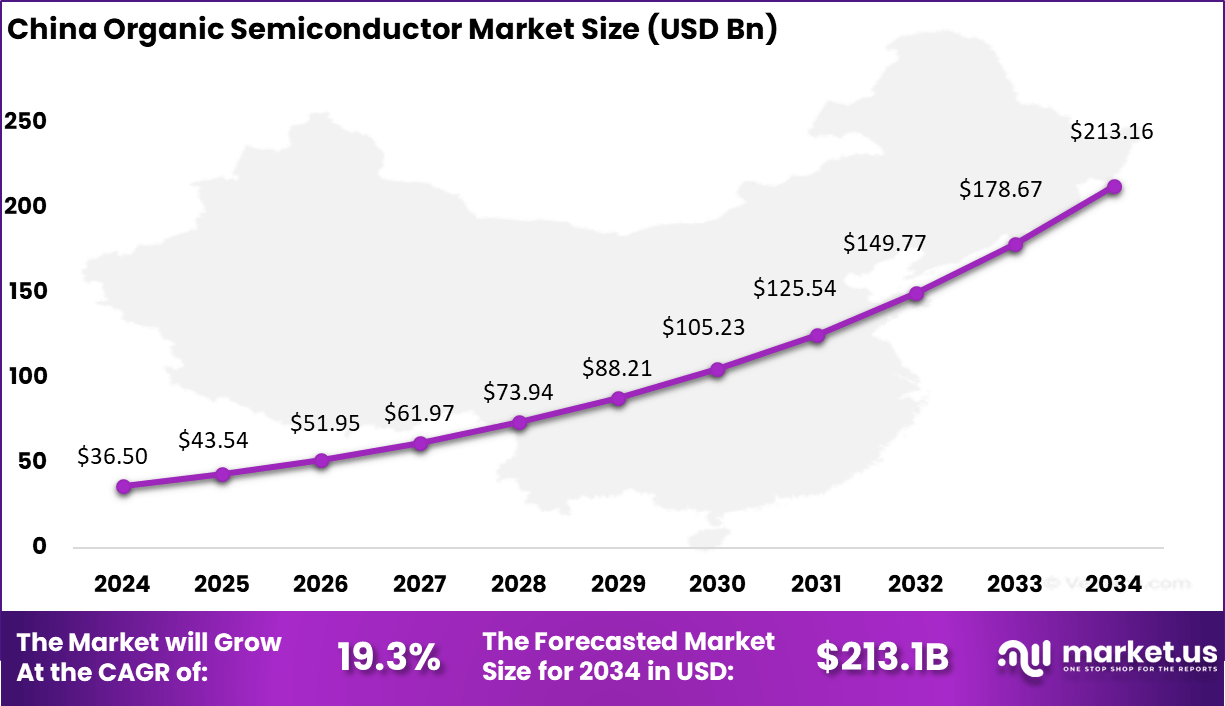

- China reached USD 36.5 billion, highlighting its advanced supply chain for organic electronic materials and device assembly.

- A CAGR of 19.3% signals fast expansion as flexible electronics, wearables, and energy-efficient display technologies gain wider adoption.

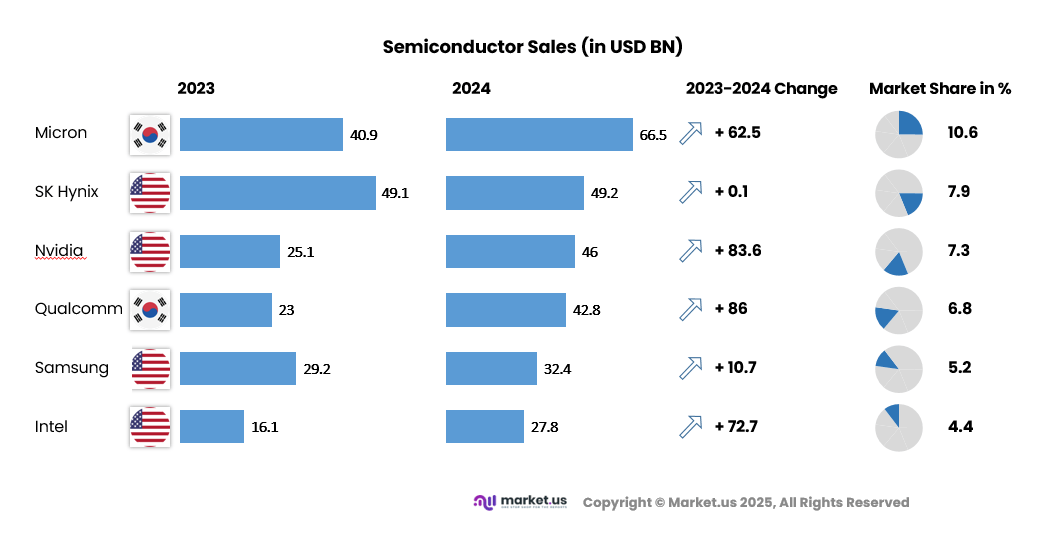

According to Market.us, The global Semiconductor market size accounted for USD 840.60 billion in 2024 and is predicted to increase from USD 907.4 billion in 2025 to approximately USD 2,010.6 billion by 2034, expanding at a CAGR of 9.20% from 2025 to 2034. In 2024, APAC held a dominan market position, capturing more than a 65.7% share, holding USD 552.2 Billion revenue.

Based on data from Semiconductor Industry Association, global semiconductor sales reached USD 208.4 billion in the third quarter of 2025, reflecting a 15.8% increase compared with Q2. Monthly sales for September 2025 totaled USD 69.5 billion, which was 25.1% higher than the USD 55.5 billion recorded in September 2024 and 7.0% above August 2025.

Type Segment

Poly aromatic ring materials accounted for about 67.5% of the organic semiconductor market. Their dominance comes from high charge mobility, chemical purity, and thermal stability, which make them ideal for advanced electronic uses. Small molecules allow precise molecular arrangement, improving electrical conductivity and uniform thin-film formation in flexible devices.

These materials are widely used in optoelectronic devices such as light-emitting diodes, sensors, and solar cells. The ability to modify the structure of aromatic rings helps researchers tune electronic and optical features. This flexibility supports innovation in organic materials used for next-generation energy-efficient and flexible products.

Application Segment

Display applications represented close to 75.8% of the total share, showing their importance in the organic semiconductor industry. Growth is supported by the quick move toward flexible, lightweight, and power-saving display panels. Organic layers enable vivid color output and clear contrasts essential for OLED displays used in consumer devices.

Manufacturers prefer organic semiconductors for their low-temperature processing and compatibility with thin substrates. The technology also supports foldable and bendable screens that are gaining popularity worldwide. Continuous material upgrades are improving stability, lifespan, and brightness performance for large-screen and mobile devices.

Regional Segment: Asia Pacific

Asia Pacific captured nearly 77.2% of the organic semiconductor market, emerging as the leading region for production and innovation. Strong industrial infrastructure, government investments, and rapid development in flexible electronics have helped build this leadership. The region leads in material supply, research centers, and end-use manufacturing facilities.

China, in particular, plays a central role due to significant research spending and large-scale domestic demand. The region continues to attract new investments for organic display and sensor production lines. With steady growth and increasing local expertise, Asia Pacific remains the center of global progress in organic semiconductor materials.

Emerging Trends

Emerging trends in the organic semiconductor market reflect a clear move towards enhancing the flexibility and adaptability of electronic devices. One significant trend is the widespread adoption of printing technologies to create organic semiconductor layers. This method resembles printing ink on paper and allows manufacturers to produce circuits and components in a more cost-effective way while reducing material waste.

The ability to print on diverse surfaces gives rise to innovative applications like foldable phones, wearable health monitors, and other compact, portable electronics. Furthermore, printed organic semiconductors show improved structural integrity, as over 75% of prototypes demonstrate smoother, more uniform layers. This translates into longer-lasting devices capable of withstanding daily wear and tear without performance loss.

Another critical trend is the growth in wearable technology powered by organic semiconductors. These materials offer a lightweight and flexible alternative to rigid traditional semiconductors, enabling health and fitness devices that comfortably conform to the shape of the body. Such wearables can track vital signs like heart rate and blood oxygen levels continuously, improving user convenience and expanding usage in remote health monitoring.

Additionally, legislation and consumer preferences for eco-friendly products are driving development efforts focusing on greener manufacturing processes. Organic semiconductors require lower processing temperatures and less energy, cutting production energy consumption by approximately 60% compared to traditional silicon semiconductors, aligning well with global sustainability goals.

Growth Factors

The growth of the organic semiconductor market is mainly driven by the rising demand for flexible and lightweight electronic devices. Consumers increasingly prefer gadgets that are not only powerful but also comfortable to wear and easy to carry. Organic semiconductors make this possible by allowing electronics like wearables and foldable displays to be thin, bendable, and durable.

Another important growth factor is the increasing focus on sustainability and eco-friendly technologies. Organic semiconductors are emerging as a greener alternative because their production consumes less energy and generates less waste. The expanding use of these materials in flexible solar cells and bio-degradable medical devices also opens new applications, accelerating market adoption.

Driver

Growing demand for flexible, lightweight, energy-efficient electronics

The demand for consumer electronics that are lightweight, energy-efficient, and flexible has surged globally. Organic semiconductors, being carbon-based materials that can be processed into thin, flexible films, are especially well suited for such devices. Their application in displays (e.g., OLED screens), wearable electronics, and flexible sensors leverages their mechanical flexibility and low-cost processing.

This suitability is driving market growth, as manufacturers seek materials that support slimmer, lighter, and more energy-efficient devices. The growth in adoption of organic semiconductors in both display applications and emerging flexible electronics markets underpins the overall market expansion.

Restraint

Lower mobility and limited material stability

Organic semiconductors face limitations due to lower charge carrier mobility compared to traditional inorganic materials. This restricts their ability to move electrical charges efficiently, which reduces performance in devices that require fast or stable operation. Their sensitivity to moisture and oxygen also affects long term reliability, making durability a concern for manufacturers.

These material limitations raise the cost of protective layers and engineering work needed to improve performance. Devices may degrade faster in outdoor environments or high stress conditions. The need for extra structure and testing slows adoption in critical applications where reliability is a priority.

Opportunity

Growing use in renewable energy and sustainable electronics

Organic semiconductors provide strong potential in renewable energy systems, especially in organic photovoltaic cells. Their compatibility with lightweight and flexible surfaces allows for new kinds of solar panels that can be integrated into clothing, portable items, and building surfaces. Rising demand for clean energy solutions supports wider interest in these materials.

The market also benefits from the move toward eco friendly and low impact electronics. Many organic semiconductor materials can be produced with less environmental strain than traditional semiconductors. This gives manufacturers a chance to invest in products that align with sustainability goals and regulatory expectations.

Challenge

Difficulty in scaling production with consistent quality

Large scale manufacturing of organic semiconductor devices remains challenging because the materials are highly sensitive during processing. Small variations in purity, temperature, or exposure to air can affect performance. This makes mass production harder and increases the risk of inconsistent results. Manufacturers must manage strict controls to maintain uniform quality.

A lack of standard testing methods and clear long term reliability data creates further uncertainty. Companies often face difficulty proving that organic semiconductor devices will remain stable over years of use. This slows commercial expansion and limits wider acceptance in industries that require predictable and reliable performance.

Key Market Segments

By Type

- Polyethylene (Polymers)

- Poly Aromatic Ring (Small Molecules)

- Copolymer

By Application

- Display Applications

- System Component

- Organic Photovoltaic (OPV)

- OLED Lighting

- Printed Batteries

- Organic RFID Tags

- Others

Regional Analysis and Coverage

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of Latin America

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

BASF, Cambridge Display Technology, DuPont, Eni, Heliatek, Hodogaya Chemical, and Konica Minolta lead the organic semiconductor market with strong material portfolios used in OLED displays, flexible electronics, and photovoltaic applications. Their focus remains on improving charge mobility, stability, and energy efficiency. These companies support growing demand for lightweight, bendable, and eco-friendly electronic components.

LG Chem, Merck, Mitsubishi Chemical, Novaled, Polyera, Samsung SDI, Sony, and Sumitomo Chemical strengthen the competitive landscape with advanced organic layers for OLED panels, organic transistors, and lighting solutions. Their materials enable vivid displays, thin-film devices, and low-power operation across consumer electronics. These providers concentrate on improved lifetimes, enhanced color purity, and scalable production.

Universal Display Corporation, BOE Technology, MBRAUN, Hicenda Technology, Youritech, and other participants expand the market with specialized manufacturing systems, encapsulation tools, and high-performance organic compounds. Their technologies support commercial-scale production of flexible displays, sensors, and printed electronics. These companies emphasize process consistency, device reliability, and integration with emerging form factors.

Top Key Players in the Market

- BASF SE

- Cambridge Display Technology Ltd.

- DuPont de Nemours, Inc.

- Eni S.p.A.

- Heliatek GmbH

- Hodogaya Chemical Co., Ltd.

- Konica Minolta, Inc.

- LG Chem Ltd.

- Merck KGaA

- Mitsubishi Chemical Corporation

- Novaled GmbH

- Polyera Corporation

- Samsung SDI Co., Ltd.

- Sony Corporation

- Sumitomo Chemical Co., Ltd.

- Universal Display Corporation (UDC)

- BOE Technology Group Co., Ltd.

- MBRAUN.

- Hicenda Technology Co.

- Youritech

- Others

Recent Developments

- September 2025: BASF SE launched an upgraded version of its QDYES™ technology, offering a greener and more efficient way to produce wide color gamut displays. This upgrade sets a new benchmark in display performance using organic materials, reflecting BASF’s commitment to sustainable innovation.

- May 2025: FlexEnable received the 2025 Display Component of the Year award for its FlexiOM™ organic thin-film transistor technology. This breakthrough enables highly flexible, lightweight, and curved active-matrix displays and optics, which can be produced at lower temperatures compared to silicon TFTs, allowing energy savings and new product designs.

- November 2025: DuPont de Nemours reported strong growth in semiconductor technologies driven by advanced nodes and AI applications. The company is expanding manufacturing capacity in China to meet rising demand for industrial water purification linked to advanced electronics production, showcasing strategic investment in supporting semiconductor-related demand.

Future Outlook

The future outlook shows a positive trajectory as flexible, lightweight, and sustainable electronics continue to attract investment. The rising alignment between material science, automation, and AI driven modelling is expected to support stronger innovation, and the diversity of applications across displays, sensors, photovoltaics, and smart packaging signals long term potential.

Regional research initiatives are also expected to encourage development, as laboratories expand work on stability, film uniformity, and improved mobility. As production techniques become more refined, organic semiconductor products are likely to gain wider acceptance in both high performance and low cost device segments.

New opportunities lie in:

- Flexible medical sensors

- Smart labels and intelligent packaging

- Low power wearable devices

- Printed photovoltaic materials

- Organic circuits for IoT nodes

Quick Market Scope

Report Features Description Market Value (2024) USD 155.3 Bn Forecast Revenue (2034) USD 1,079.8 Bn CAGR(2025-2034) 21.4% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends Segments Covered By Type (Polyethylene (Polymers), Poly Aromatic Ring (Small Molecules), Copolymer), By Application (System Component, Organic Photovoltaic (OPV), OLED Lighting, Printed Batteries, Organic RFID Tags, Display Applications, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape BASF SE, Cambridge Display Technology Ltd., DuPont de Nemours, Inc., Eni S.p.A., Heliatek GmbH, Hodogaya Chemical Co., Ltd., Konica Minolta, Inc., LG Chem Ltd., Merck KGaA, Mitsubishi Chemical Corporation, Novaled GmbH, Polyera Corporation, Samsung SDI Co., Ltd., Sony Corporation, Sumitomo Chemical Co., Ltd., Universal Display Corporation (UDC), BOE Technology Group Co., Ltd., MBRAUN, Hicenda Technology Co., Youritech, Others. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Organic Semiconductor MarketPublished date: Dec. 2025add_shopping_cartBuy Now get_appDownload Sample

Organic Semiconductor MarketPublished date: Dec. 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- BASF SE

- Cambridge Display Technology Ltd.

- DuPont de Nemours, Inc.

- Eni S.p.A.

- Heliatek GmbH

- Hodogaya Chemical Co., Ltd.

- Konica Minolta, Inc.

- LG Chem Ltd.

- Merck KGaA

- Mitsubishi Chemical Corporation

- Novaled GmbH

- Polyera Corporation

- Samsung SDI Co., Ltd.

- Sony Corporation

- Sumitomo Chemical Co., Ltd.

- Universal Display Corporation (UDC)

- BOE Technology Group Co., Ltd.

- MBRAUN.

- Hicenda Technology Co.

- Youritech

- Others

Our Clients

- 169005

- Dec. 2025