Quick Navigation

Report Overview

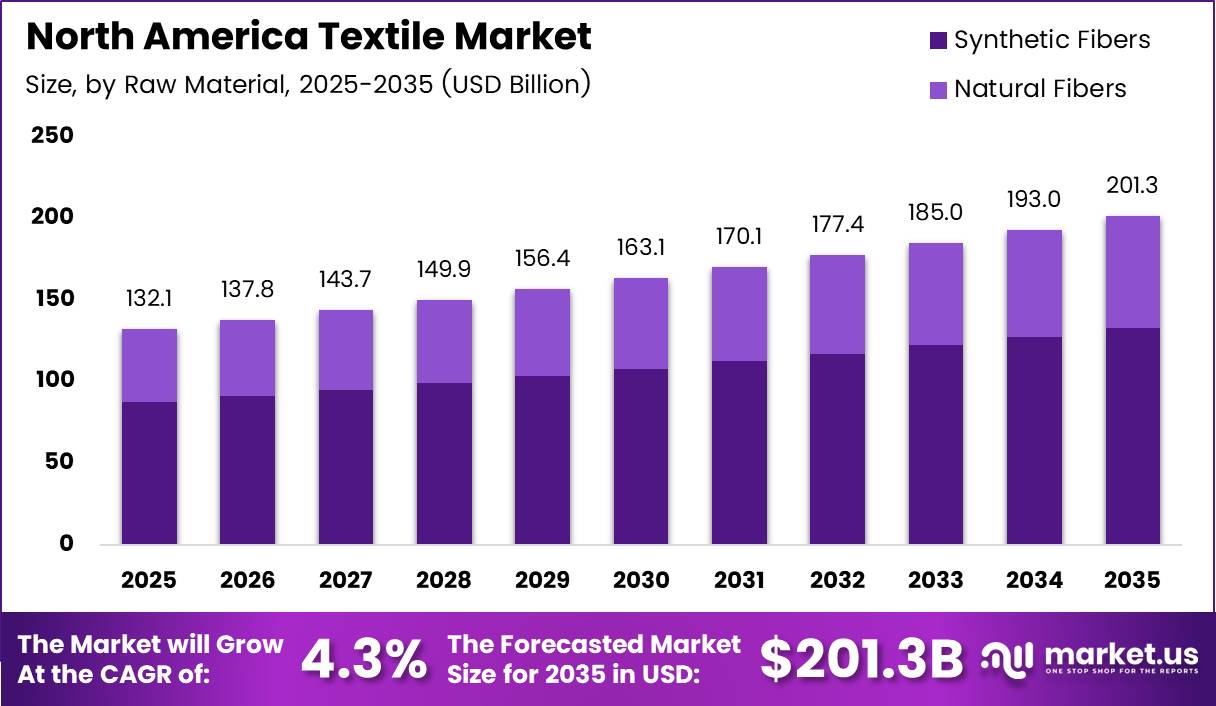

North America Textile Market size is expected to be worth around USD 201.3 Billion by 2035 from USD 132.1 Billion in 2025, growing at a CAGR of 4.3% during the forecast period 2026 to 2035. This trajectory reflects a market expanding by more than USD 69 Billion across the decade. Investors and manufacturers must position early to capture this compounding value before competitive density increases.

The North America textile market covers the full production and distribution chain for fiber-based materials. This includes raw fiber processing, yarn spinning, fabric manufacturing, and finished textile goods. The market serves fashion, industrial, medical, automotive, and household end-use segments across the United States, Canada, and Mexico.

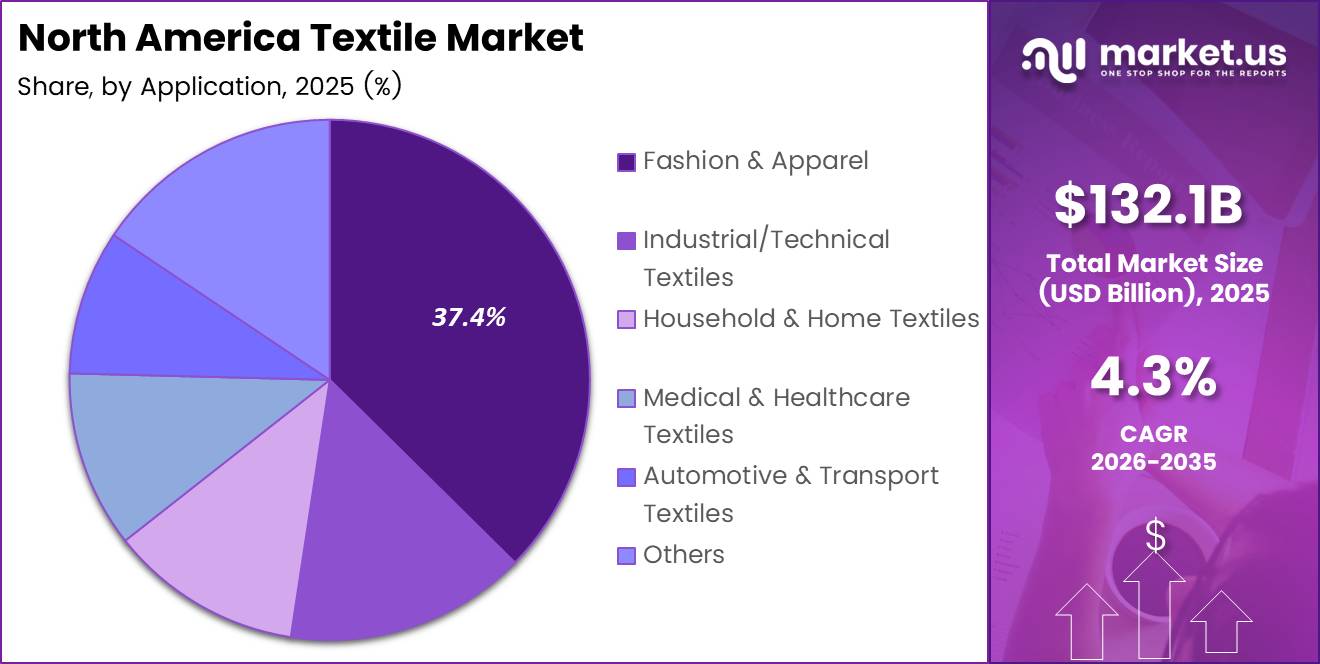

Synthetic fibers anchor the supply side of this market, commanding 65.9% of raw material share. Woven fabric production leads the process segment at 41.8%. Fashion and apparel represents the single largest application at 37.4%. This concentration signals where volume pricing power, supply agreements, and distribution relationships carry the most strategic weight.

Government policy and trade regulation shape the competitive floor for domestic manufacturers. Import volumes have tripled over two decades, pressuring local producers to differentiate on speed, specialization, and technology rather than cost. Domestic investment in manufacturing infrastructure remains the primary buffer against import displacement.

According to the National Council of Textile Organizations, investment in U.S. textile mills climbed from USD 1.85 Billion in 2013 to USD 2.98 Billion in 2022, a 61% increase over nine years. This capital deepening signals that domestic producers are upgrading capacity rather than exiting. Manufacturers who benefit from this infrastructure investment hold a structural cost and quality advantage entering 2026.

According to the National Council of Textile Organizations, the U.S. textile and apparel industry invested USD 22.3 Billion in new plants and equipment between 2013 and 2022, averaging USD 2.23 Billion per year. This sustained capital commitment builds a production base that underpins current operational capacity. Companies entering the market now compete against facilities built with a decade of continuous reinvestment.

Technical textiles for automotive, aerospace, and medical applications represent the highest-margin growth frontier within this market. Consumer preference is also shifting toward premium, performance-oriented products that command better unit economics. These two forces together create a market environment that rewards specialization over commodity volume production.

Key Takeaways

- The North America Textile Market is valued at USD 132.1 Billion in 2025 and is forecast to reach USD 201.3 Billion by 2035.

- The market grows at a CAGR of 4.3% during the forecast period 2026 to 2035.

- By Raw Material, Synthetic Fibers dominate with a 65.9% share in 2025.

- By Process/Technology, Woven holds the leading position at 41.8% share in 2025.

- By Application, Fashion & Apparel leads with a 37.4% share in 2025.

- The United States represents the dominant country market within North America, supported by USD 22.3 Billion in textile plant and equipment investment from 2013 to 2022.

- U.S. textile mill labor productivity increased by 1.8% in 2024, reflecting output efficiency gains despite a 2.0% decline in aggregate sectoral output.

- The U.S. textile recycling rate stood at 14.7% in 2018, indicating substantial headroom for circular economy development through 2035.

Raw Material Analysis

Synthetic Fibers dominate with 65.9% due to cost efficiency and performance versatility across applications.

In 2025, Synthetic Fibers held a dominant market position in the By Raw Material segment of the North America Textile Market, with a 65.9% share. Their scalable production, consistent performance properties, and adaptability across apparel, industrial, and technical uses make them the default choice for volume manufacturers. Buyers who prioritize cost predictability and supply chain stability will continue to favor synthetics over natural alternatives.

Natural Fibers retain relevance in premium fashion, medical, and heritage textile applications despite synthetic fiber dominance. Consumer preference for natural, breathable materials sustains demand in specific product categories. Producers who position natural fiber products around comfort, certification, and provenance can defend higher price points against synthetic alternatives.

Process/Technology Analysis

Woven dominates with 41.8% due to structural versatility across apparel and industrial uses.

In 2025, Woven held a dominant market position in the By Process/Technology segment of the North America Textile Market, with a 41.8% share. Woven construction delivers dimensional stability and tensile strength that knitted and non-woven alternatives cannot match across a broad application range. Manufacturers who lead in woven production infrastructure maintain first-call supplier status across the highest-volume textile categories.

Knitted fabrics serve the activewear, casualwear, and hosiery segments through their inherent stretch, comfort, and rapid production cycle. Consumer preference for comfort-oriented clothing has expanded knitting’s footprint across both fashion and performance applications. In January 2025, Spanx launched SPANXsculpt™ ReDefine using LYCRA FitSense® Denim Technology, demonstrating commercial appetite for knit-based innovations that combine structure with stretch performance.

Non-woven fabrics serve medical, hygiene, filtration, and geotextile segments where bonded fiber sheets deliver performance at lower cost than woven alternatives. Their use in single-use healthcare products and protective equipment positions non-woven producers within a demand category that does not follow fashion cycles. This provides revenue stability that apparel-focused textile manufacturers cannot replicate.

3-D Weaving & Spacer Fabrics represent the technical frontier of woven construction, enabling multi-layer structures used in composite reinforcement, protective equipment, and medical implants. Their three-dimensional architecture delivers strength-to-weight ratios unachievable with conventional flat weaving. Manufacturers who invest in 3-D weaving capabilities enter a low-competition, high-specification market where technical barriers protect margin.

Application Analysis

Fashion & Apparel dominates with 37.4% due to volume consumption across all consumer demographics.

In 2025, Fashion & Apparel held a dominant market position in the By Application segment of the North America Textile Market, with a 37.4% share. Consumer spending on clothing sustains consistent base demand regardless of economic cycle. Textile suppliers who align production capacity with fast-fashion replenishment windows and premium brand supply chains capture the widest revenue exposure within this segment.

Industrial/Technical Textiles serve aerospace, defense, construction, and filtration applications where performance specifications replace aesthetic criteria as the primary purchasing driver. These textiles command significantly higher unit values than consumer-facing categories. Producers who build certified manufacturing processes for technical textile specifications gain long-term contract positions that commodity producers cannot displace on price alone.

Household & Home Textiles cover bedding, towels, upholstery, rugs, and curtains, where brand preference and retail distribution relationships determine market share. Consumer renovation activity and housing starts directly influence demand in this category. Manufacturers with established retail channel access face lower customer acquisition costs than new entrants competing on product alone.

Medical & Healthcare Textiles include surgical drapes, wound care fabrics, compression garments, and antimicrobial apparel, where regulatory compliance and clinical performance standards define the competitive bar. In October 2025, iFabric Corp. launched Doctor’s Choice® Next Generation scrubs integrating antimicrobial, moisture-management, and water-repellent technologies into healthcare apparel. This commercialization shows that medical textile innovation now extends from operating rooms into everyday clinical environments.

Automotive & Transport Textiles supply seat covers, headliners, airbag fabrics, insulation, and trunk liners across passenger and commercial vehicle platforms. Original equipment manufacturer qualification cycles mean that supplier relationships, once established, generate stable multi-year revenue streams. Manufacturers who achieve OEM approval status operate with a customer retention advantage that aftermarket-only suppliers lack.

Others in the application segment include agricultural textiles, sports and recreation fabrics, packaging materials, and electronic component textiles. These categories serve specialized buyers who require functional properties rather than aesthetic outcomes. Producers who diversify across multiple application niches within this group reduce revenue concentration risk compared to single-segment specialists.

Key Market Segments

By Raw Material

- Synthetic Fibers

- Polyester

- Nylon

- Rayon/Viscose

- Acrylic

- Polypropylene

- Recycled Fibers

- Others

- Natural Fibers

- Cotton

- Wool

- Silk

By Process/Technology

- Woven

- Knitted

- Non-woven

- Spunlaid (Spunbond/Melt-blown)

- Dry-laid Hydro-entangled

- Wet-Laid

- Needle-punched

- 3-D Weaving & Spacer Fabrics

By Application

- Fashion & Apparel

- Industrial/Technical Textiles

- Household & Home Textiles

- Medical & Healthcare Textiles

- Automotive & Transport Textiles

- Others

Drivers

High-Performance Fabric Demand and Advanced Manufacturing Adoption Drive North American Textile Revenue

Demand for high-performance fabrics across sportswear, healthcare, and industrial applications is pulling textile producers toward specialized product categories with stronger unit economics. Manufacturers who retool for performance fabric output compete on specification rather than cost. This shift favors capital-intensive domestic producers over low-cost import alternatives that cannot meet technical requirements.

According to the Bureau of Labor Statistics, labor productivity in U.S. textile mills increased by 1.8% in 2024, the latest data available as of 2025. According to FRED, the productivity index rose from 102.6 in 2023 to 104.5 in 2024 using a 2017 base of 100. Higher output per labor hour improves cost competitiveness for domestic mills, giving U.S. manufacturers a tangible efficiency argument against import-sourced alternatives.

Advanced manufacturing technologies, including automated looms, digital quality systems, and precision fiber engineering, are reducing defect rates and shortening production cycles across North American facilities. In October 2025, iFabric Corp. launched Doctor’s Choice® Next Generation scrubs embedding antimicrobial and moisture-management properties into healthcare apparel. This product demonstrates that manufacturing technology investment translates directly into premium-priced, clinically differentiated textile outputs.

Restraints

Rising Labor Costs and Environmental Compliance Requirements Compress Domestic Textile Margins

Rising labor costs erode the cost competitiveness of domestic textile manufacturing relative to offshore alternatives. Producers who cannot offset wage increases with automation or product premiumization face margin compression that limits reinvestment capacity. This dynamic places smaller domestic manufacturers at structural risk as import competition intensifies.

According to FRED, sectoral output for textile mills (NAICS 313) declined from 21,686 index units in 2023 to 21,257 in 2024, a decrease of 429 units or approximately 2.0%. This output contraction occurred even as productivity improved, indicating that efficiency gains did not offset volume loss. The combination signals that cost pressures are shrinking the domestic production base despite operational improvements.

According to a U.S. Government Accountability Office assessment, imports of textile and apparel units into the United States increased by 182% between 2000 and 2023, representing a near-tripling of imported volumes over this period. This import pressure directly limits domestic manufacturers’ ability to raise prices to recover compliance and labor cost increases. Producers who cannot differentiate on quality, speed, or technical performance face permanent market share erosion from lower-cost import sources.

Growth Factors

Smart Textiles, Nearshoring, and Sustainable Fabric Demand Open New Revenue Streams Across North America

Smart textiles with integrated sensors and wearable technology capabilities represent a product category where North American manufacturers hold an innovation and IP advantage over lower-cost competitors. Consumer electronics convergence with apparel is creating a new purchase occasion that existing textile supply chains are not designed to serve. Producers who invest in electronic textile integration now establish first-mover customer relationships before the category scales.

According to the EPA, the U.S. recycled only 14.7% of all textiles in 2018, with 2.5 million tons recycled out of 17 million tons generated. This low baseline signals that the infrastructure and supply chains for circular textile production remain underdeveloped. Investors and manufacturers who build recycled-fiber processing capacity now enter a gap market with minimal domestic competition and rising corporate buyer demand. In February 2025, Acme Mills introduced Natura, a bio-based PLA textile portfolio designed to replace petroleum-based materials across automotive, healthcare, furniture, and industrial applications, demonstrating that bio-based material commercialization is actively closing the sustainability gap.

According to the Global Efficiency Intelligence low-carbon thermal energy roadmap, electrification of process heat combined with advanced controls can cut specific fuel use by an additional 5 to 15% beyond boiler upgrades, and total thermal energy demand reductions can reach 30 to 40% relative to baseline textile operations. Manufacturers who implement these energy efficiency measures reduce operating costs while meeting tightening sustainability procurement standards from large retail and industrial buyers. This dual benefit of cost reduction and ESG compliance creates a capital allocation case that facilities with aging thermal infrastructure can no longer defer.

Emerging Trends

Recycled Materials, AI Quality Systems, and Digital Printing Reshape North American Textile Competition

Recycled polyester and bio-based textile materials are replacing virgin synthetic inputs across apparel, home textile, and industrial product categories. Corporate sustainability mandates from large retailers and consumer brands are converting recycled-content specifications from optional to contractual requirements. Textile producers who build certified recycled-fiber supply chains before this shift becomes universal gain a compliance head start that translates into preferred-supplier status.

According to the EPA, 66.5% of U.S. textile waste was landfilled and 18.8% was incinerated in 2018, covering 11.3 million tons landfilled and 3.2 million tons combusted with energy recovery out of 17 million tons generated. These end-of-life figures underscore how little of the textile waste stream currently feeds back into production. Producers who develop take-back and reprocessing infrastructure can convert this waste volume into a low-cost recycled-fiber feedstock advantage. In November 2025, iFabric Corp. launched its Verzus All Apparel brand at a major Canadian wholesale retailer, expanding commercialization of proprietary performance textile technologies that serve exactly this sustainability-aligned consumer segment.

As stated by the Global Efficiency Intelligence roadmap, switching from conventional fossil fuel boilers to high-efficiency boilers combined with heat-recovery systems can reduce thermal energy consumption by 10 to 25% in textile dyeing and finishing processes. This energy cost reduction directly improves margin structure for producers in high-energy operations. AI-driven quality inspection and digital printing for short-run production further compound these efficiency gains by reducing material waste, rework labor, and minimum order constraints that have historically limited customer responsiveness.

Key Company Insights

Shawmut LLC strengthened its vertical integration in September 2024 by acquiring Fairystone Fabrics through its newly formed Shawmut Infinite affiliate, committing USD 8 million to modernize knitting, warping, and prototyping operations in North Carolina. This investment deepens control over the supply chain from fabric development to finished technical textile output. Manufacturers who own vertically integrated production reduce lead times and quality variability that arm’s-length sourcing arrangements cannot eliminate.

Hansae Co. Ltd. acquired U.S.-based Texollini in October 2024 to extend its synthetic-fiber textile capabilities and build a vertically integrated platform serving the North American apparel market. This acquisition positions Hansae to supply domestic and nearshore apparel brands with end-to-end production capability. Buyers who consolidate vendor relationships with vertically integrated suppliers reduce coordination costs and gain tighter control over delivery and quality outcomes.

Loop Industries launched Twist™ in July 2025, a high-performance polyester resin brand produced entirely from textile waste and targeting apparel, sportswear, home textile, and fashion manufacturers seeking circular textile solutions. This product directly addresses the commercial gap between waste generation and recycled-fiber supply that EPA data quantify at scale. Textile producers who integrate Twist™ into their supply chains can credibly meet corporate buyer recycled-content mandates without developing their own waste reprocessing infrastructure.

Cintas Corporation announced the acquisition of UniFirst in March 2026 in a USD 5.5 Billion cash-and-stock transaction, creating one of the largest textile-based uniform and workwear service providers across the United States and Canada. This scale consolidation concentrates purchasing power, distribution reach, and service contract coverage in a single operator. Smaller uniform and workwear textile suppliers will face intensified pricing pressure as Cintas-UniFirst leverages its combined scale in supplier negotiations and customer retention programs.

Key Players

- Shawmut LLC

- Hansae Co. Ltd.

- Loop Industries

- Cintas Corporation

- Spanx

- Acme Mills

- iFabric Corp.

- Intelligent Fabric Technologies (North America)

Recent Developments

- September 2024 – Shawmut LLC acquired Fairystone Fabrics through its newly formed affiliate Shawmut Infinite, strengthening its vertically integrated textile supply chain in North America and announcing an USD 8 million investment to modernize knitting, warping, and fabric prototyping operations in North Carolina.

- October 2024 – Hansae Co. Ltd. acquired U.S.-based textile manufacturer Texollini to enhance its synthetic-fiber textile capabilities and strengthen its vertically integrated textile manufacturing platform serving the North American apparel market.

- July 2025 – Loop Industries launched Twist™, a high-performance polyester resin brand made entirely from textile waste, targeting apparel, sportswear, home textile, and fashion manufacturers seeking circular textile solutions.

- March 2026 – Cintas Corporation announced the acquisition of UniFirst in a USD 5.5 Billion cash-and-stock transaction, creating one of the largest textile-based uniform and workwear service providers across the United States and Canada.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 132.1 Billion |

| Forecast Revenue (2035) | USD 201.3 Billion |

| CAGR (2026-2035) | 4.3% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Raw Material (Synthetic Fibers: Polyester, Nylon, Rayon/Viscose, Acrylic, Polypropylene, Recycled Fibers, Others; Natural Fibers: Cotton, Wool, Silk), By Process/Technology (Woven, Knitted, Non-woven: Spunlaid, Dry-laid Hydro-entangled, Wet-Laid, Needle-punched; 3-D Weaving & Spacer Fabrics), By Application (Fashion & Apparel, Industrial/Technical Textiles, Household & Home Textiles, Medical & Healthcare Textiles, Automotive & Transport Textiles, Others) |

| Competitive Landscape | Shawmut LLC, Hansae Co. Ltd., Loop Industries, Cintas Corporation, Spanx, Acme Mills, iFabric Corp., Intelligent Fabric Technologies (North America) |

| Customization Scope | Customization for segments will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |