Quick Navigation

- Report Overview

- Top Market Takeaways

- Drivers Impact Analysis

- Restraints Impact Analysis

- By Orbit Type Analysis

- By Platform Analysis

- By End-User Analysis

- Investor Type Impact Analysis

- Technology Enablement Analysis

- Key Challenges

- Emerging Trends

- Growth Factors

- Key Market Segments

- Regional Analysis

- Competitive Analysis

- Future Outklook

- Recent Developments

- Report Scope

Report Overview

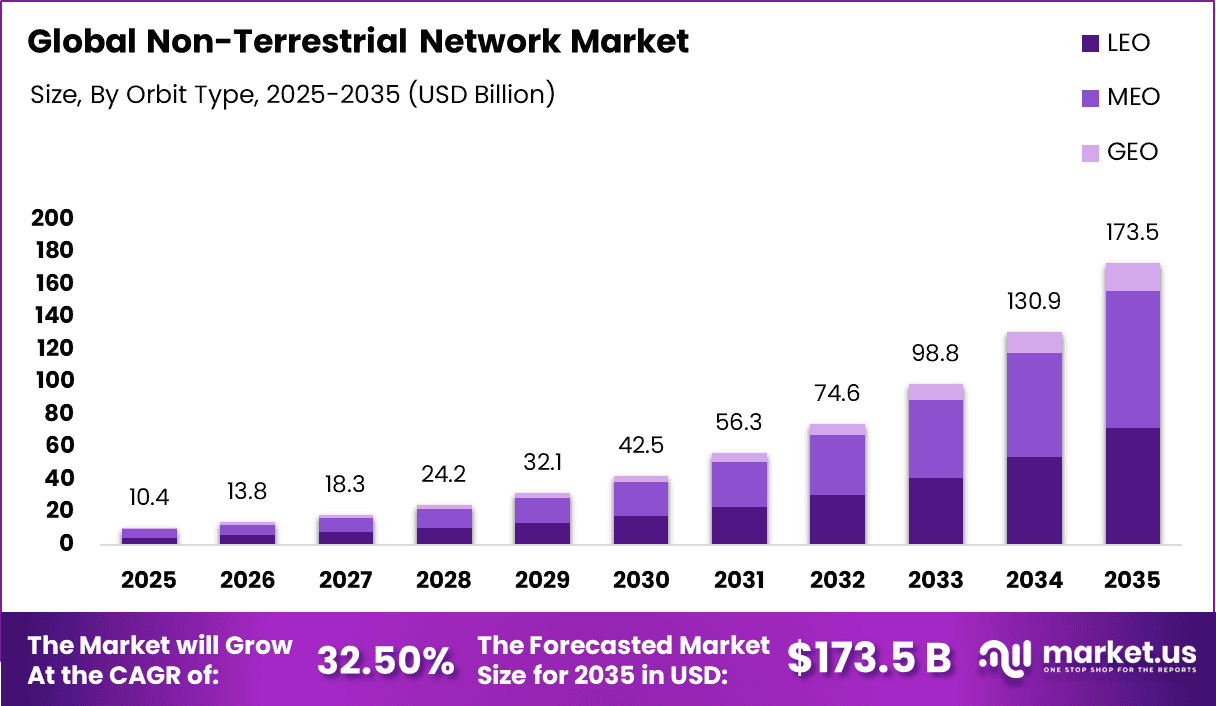

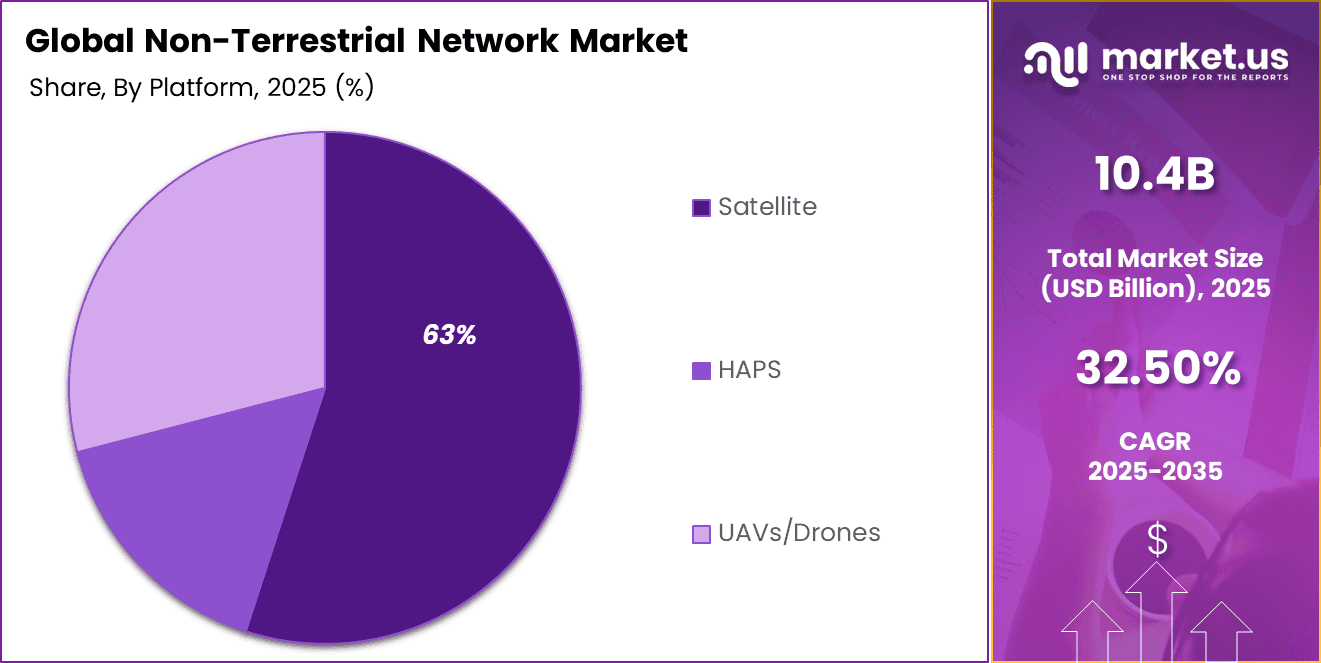

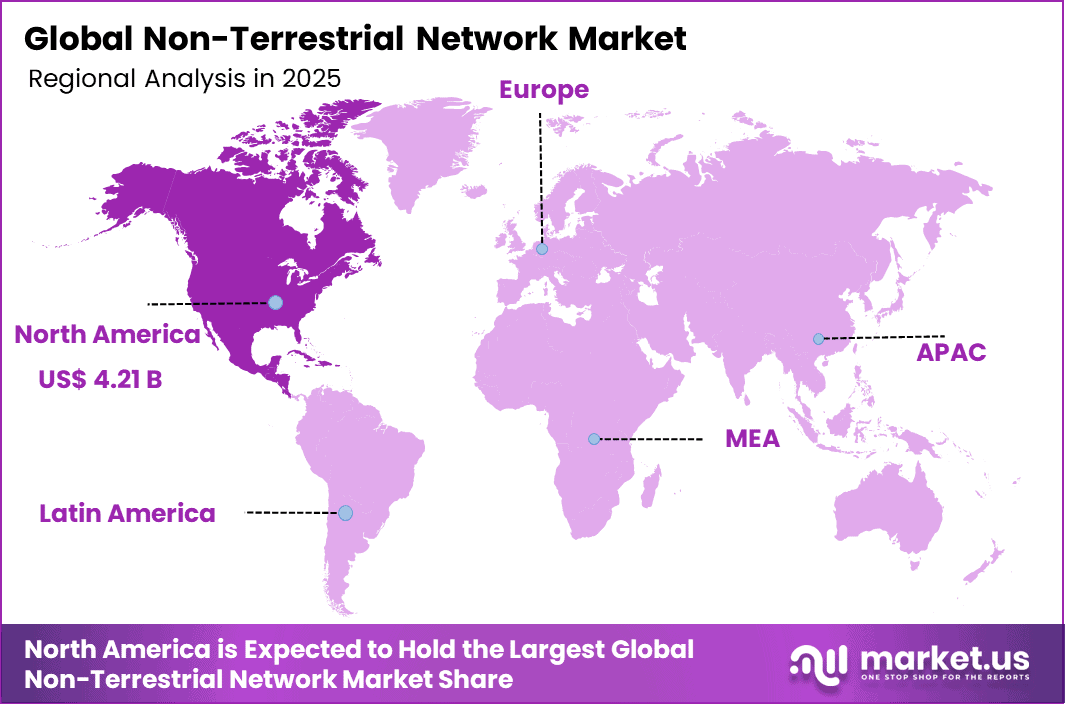

The Global Non-Terrestrial Network Market generated USD 10.4 billion in 2025 and is predicted to register growth from USD 13.8 billion in 2026 to about USD 173.5 billion by 2035, recording a CAGR of 32.50% throughout the forecast span. In 2025, North America held a dominant market position, capturing more than a 40.5% share, holding USD 4.21 Billion revenue.

Top Market Takeaways

- LEO orbit type commands 41.3% market share, delivering low-latency global coverage, optical inter-satellite links, and resilient mesh networking for real-time tactical communications.

- Satellite platforms capture 62.5%, enabling direct-to-device 5G NTN, hybrid terrestrial-space architectures, and rapid constellation scalability through reusable launch vehicles.

- Defense & security end-users hold 34.2%, leveraging NTN for contested environment operations, proliferated LEO architectures, and jam-resistant beyond-line-of-sight connectivity.

- North America drives 40.5% global value, with U.S. market at USD 3.77 billion and 30.4% CAGR, fueled by SpaceX Starshield, DoD LEO initiatives, and commercial-military convergence.

Non terrestrial networks are emerging as an extension of traditional communication systems by using satellites, high altitude platforms, and other space based technologies to provide connectivity beyond ground infrastructure. These networks are designed to support communication in remote, rural, and hard to reach areas where conventional networks face limitations.

They are also being integrated with existing mobile networks to improve coverage, reliability, and service continuity. As global connectivity becomes more important for economic activity and digital access, non terrestrial networks are gaining attention as a practical solution to bridge coverage gaps.

One of the main driving factors is the growing need for universal connectivity across regions that lack strong network infrastructure. Governments and service providers are focusing on expanding digital access to underserved areas, which is encouraging investment in satellite based communication systems.

In addition, the increasing demand for reliable communication in sectors such as aviation, maritime, defense, and disaster management is supporting the adoption of these networks. The advancement of satellite technologies and the integration of space based systems with terrestrial networks are also making deployment more efficient and scalable. The rising use of connected devices in remote operations is further strengthening the need for continuous and wide area coverage.

Demand for non terrestrial network solutions is increasing as industries and users look for dependable communication beyond traditional network limits. There is strong interest in solutions that can provide seamless connectivity across land, sea, and air without interruption. Organizations are also seeking systems that can support data transmission in challenging environments where network stability is critical.

The demand is particularly high in applications that require constant communication, such as logistics, emergency response, and remote monitoring. As the need for global and uninterrupted connectivity continues to grow, the adoption of non terrestrial network technologies is expected to expand steadily.

Drivers Impact Analysis

| Key Driver | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| Rising demand for universal connectivity in remote areas | +6.3% | North America, Asia Pacific, Africa, Latin America | Short to long term | Expands network reach beyond terrestrial limits |

| Increasing integration of satellite communication with 5G networks | +5.8% | North America, Europe, Asia Pacific | Medium to long term | Supports seamless next-generation connectivity |

| Growing defense and government investment in secure communication | +5.1% | US, Europe, Middle East, Asia Pacific | Medium term | Public sector demand strengthens deployment activity |

| Expansion of IoT and machine-to-machine communication | +4.7% | Global | Medium to long term | NTN supports connected devices in hard-to-reach zones |

| Rising use of low earth orbit satellite constellations | +5.4% | Global, led by US and Europe | Medium to long term | LEO networks improve latency and coverage |

Restraints Impact Analysis

| Key Restraint | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| High deployment and infrastructure costs | -4.6% | Emerging markets and developing regions | Short to medium term | Capital intensity limits faster rollout |

| Spectrum allocation and regulatory complexity | -3.9% | Global | Medium term | Policy barriers slow commercial expansion |

| Technical challenges in interoperability with terrestrial networks | -3.4% | Global | Medium to long term | Integration issues affect service efficiency |

| Limited affordability for end users in price-sensitive regions | -2.8% | Asia Pacific, Africa, Latin America | Medium term | Cost concerns reduce adoption potential |

| Signal latency and reliability concerns in some applications | -2.5% | Global | Medium to long term | Performance gaps affect critical use cases |

By Orbit Type Analysis

The LEO segment accounted for 41.3% of the market share, reflecting its strong role in enabling low-latency and high-speed communication services. This dominance is supported by the ability of low earth orbit systems to operate closer to the Earth, which improves signal strength and reduces transmission delays. These advantages make LEO suitable for applications that require real-time connectivity and reliable data transfer.

Another factor driving this segment is the increasing deployment of satellite constellations designed to provide global coverage. LEO systems support scalable network expansion and can deliver connectivity in remote and underserved regions. Their flexibility and performance benefits are encouraging wider adoption across both commercial and government applications.

By Platform Analysis

The satellite segment held 63% share, driven by its essential role in providing wide-area communication coverage beyond traditional terrestrial infrastructure. Satellites enable connectivity across oceans, remote locations, and challenging terrains where ground networks are limited or unavailable. This makes them a critical component of non-terrestrial communication systems.

In addition, advancements in satellite technology have improved capacity, reliability, and operational efficiency. Modern satellite platforms support higher data throughput and better integration with terrestrial networks. These improvements are strengthening their position as a backbone for global communication and expanding their use across various sectors.

By End-User Analysis

The defense and security segment captured 34.2% of the market, driven by the growing need for secure and reliable communication systems in critical operations. Military and security organizations rely on non-terrestrial networks to maintain connectivity in remote or high-risk environments. These systems support surveillance, intelligence sharing, and mission coordination without dependence on ground-based infrastructure.

Furthermore, the increasing focus on national security and advanced communication capabilities is encouraging investment in non-terrestrial technologies. These solutions provide resilience against disruptions and ensure continuous communication during emergencies or conflicts. Their ability to operate independently of traditional networks makes them highly valuable for defense and security applications.

Investor Type Impact Analysis

| Investor Type | Growth Sensitivity | Risk Exposure | Geographic Focus | Investment Outlook |

|---|---|---|---|---|

| Venture capital firms | Very high | High | US, Europe, Israel | Investing in satellite and NTN startups |

| Private equity firms | High | Moderate | North America and Europe | Targeting scalable communications infrastructure |

| Corporate investors | Very high | Moderate | Global | Strategic interest in telecom and space ecosystems |

| Institutional investors | Moderate to high | Moderate | Developed markets | Prefer firms with long-term network potential |

| Government and public funding bodies | High | Low | US, EU, Asia Pacific, Middle East | Supporting strategic communication infrastructure |

Technology Enablement Analysis

| Technology | Impact on CAGR Forecast (~%) | Geographic Relevance | Impact Timeline | Additional Insight |

|---|---|---|---|---|

| Low earth orbit satellite architecture | +6.1% | Global | Medium to long term | Improves coverage and latency |

| 5G NTN standard integration | +5.5% | North America, Europe, Asia Pacific | Medium to long term | Supports standard-based deployment |

| AI-based network traffic optimization | +4.3% | US, Europe, China | Medium term | Enhances routing and resource use |

| Advanced phased array antennas | +4.0% | Global | Medium term | Improves signal performance |

| Edge computing in satellite communication networks | +3.7% | Global | Long term | Enables faster local data processing |

Key Challenges

- High infrastructure cost for satellites and ground stations makes adoption expensive.

- Complex technology and system design require advanced expertise.

- Limited coverage consistency in some remote or harsh environments.

- Latency issues compared to traditional terrestrial networks.

- Regulatory challenges across different countries and regions.

- Spectrum allocation and interference management remain difficult.

- Integration challenges with existing terrestrial communication networks.

- High maintenance and operational costs for space-based systems.

- Dependence on weather and environmental conditions affecting performance.

- Security risks in satellite communication and data transmission.

Emerging Trends

The non terrestrial network market is evolving with a strong focus on expanding connectivity beyond traditional ground based infrastructure. One key emerging trend is the integration of satellite communication with existing terrestrial networks to create hybrid communication systems that provide seamless coverage. This is improving connectivity in remote and underserved regions where conventional networks face limitations.

Another important trend is the use of low earth orbit satellite constellations that offer lower latency and better performance compared to traditional satellite systems. There is also growing interest in direct to device communication, where satellites can connect directly with smartphones and IoT devices without the need for additional ground equipment. In addition, advancements in software defined networking are enabling more flexible management of network resources across space and ground segments. The increasing use of non terrestrial networks for applications such as disaster recovery, aviation connectivity, and maritime communication is further shaping the direction of this market.

Growth Factors

The growth of this market is driven by the rising demand for reliable connectivity in areas where terrestrial infrastructure is limited or not feasible. Governments and organizations are focusing on bridging the digital divide by extending network coverage to rural and remote locations, which is supporting the adoption of non terrestrial solutions. The expansion of IoT applications across industries is also creating demand for wide area connectivity that can operate across vast and challenging environments.

Another major factor is the need for resilient communication systems that can function during natural disasters or network failures, making non terrestrial networks an important backup solution. The growing importance of real time data transmission in sectors such as defense, transportation, and logistics is further encouraging investment in this space. Additionally, ongoing advancements in satellite technology and launch capabilities are improving the accessibility and efficiency of non terrestrial networks, supporting their wider adoption across different use cases.

Key Market Segments

By Orbit Type

- LEO

- MEO

- GEO

By Platform

- Satellite

- HAPS

- UAVs/Drones

By End-User

- Defense & Security

- Agriculture

- Maritime

- Oil & Gas

- Transportation & Logistics

- Others

Regional Analysis

North America accounted for 40.5% of the Non-Terrestrial Network market, supported by strong advancements in satellite communication and increasing integration of space-based connectivity with terrestrial networks. The region benefits from early adoption of next generation communication technologies and significant investments in satellite constellations for broadband, defense, and remote connectivity.

Growing demand for uninterrupted coverage in rural and hard-to-reach areas is encouraging the use of non-terrestrial networks to complement existing infrastructure. In addition, rising use of connected devices across aviation, maritime, and emergency services is strengthening the need for reliable and wide-area communication solutions.

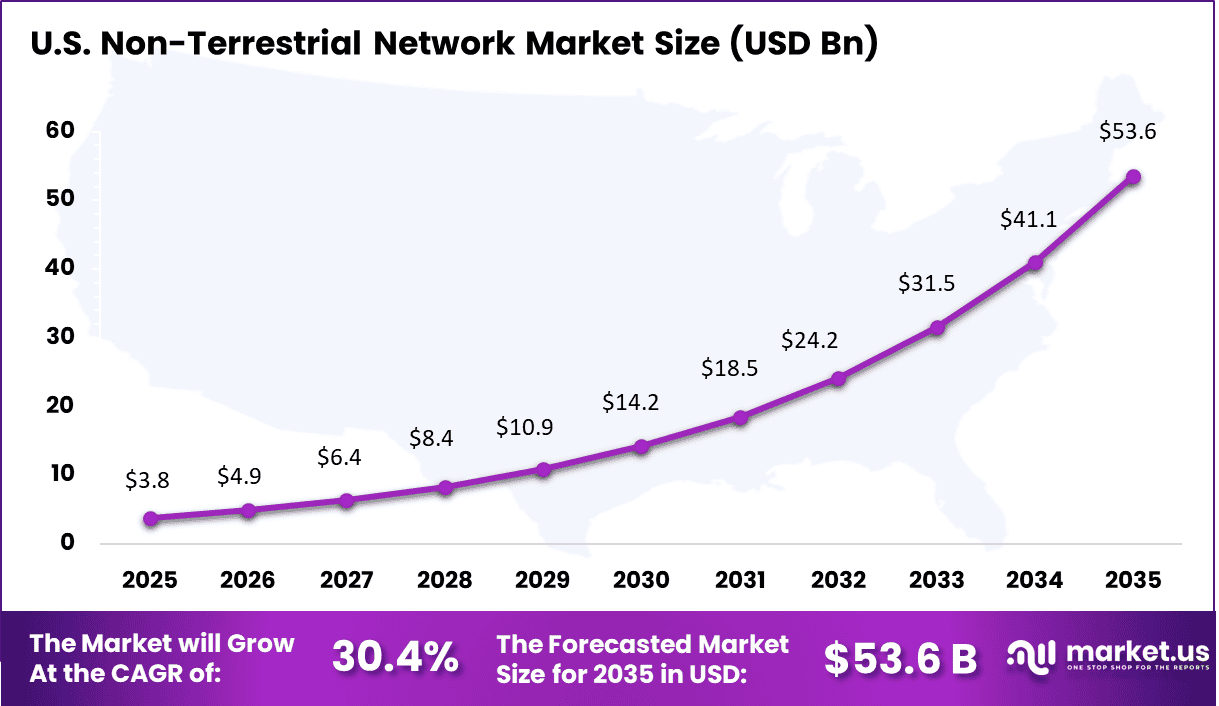

The U.S. market reached USD 3.77 Billion and is projected to grow at a CAGR of 30.4%, driven by rapid expansion of satellite-based internet services and increasing focus on resilient communication systems. Demand is rising from sectors that require continuous connectivity, including defense operations, disaster management, and remote industrial activities.

The integration of non-terrestrial networks with emerging wireless technologies is enabling seamless connectivity across diverse environments. Strong innovation in space technology and increasing deployment of low-earth orbit satellites are expected to support high growth in the US market over the coming years.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherlands

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Competitive Analysis

The competitive landscape of the Non-Terrestrial Network Market is shaped by a mix of satellite operators, telecom equipment providers, and technology companies. Companies such as SpaceX, Amazon, Iridium Satellite Communications, Inmarsat, Intelsat S.A., SES S.A., Eutelsat Communications S.A., and Viasat, Inc. focus on building and operating satellite constellations to provide global connectivity.

These players invest heavily in low earth orbit and geostationary satellite systems to improve coverage, reduce latency, and support broadband and communication services in remote areas. Their strong infrastructure and ongoing satellite deployments help them maintain a key position in the market.

At the same time, technology and telecom firms such as Apple, Qualcomm Technologies, Inc., Telefonaktiebolaget LM Ericsson, Huawei Technologies Co., Ltd., Nokia Corporation, Samsung Electronics Co., Ltd., ZTE Corporation, and Thales Group are focusing on integrating non-terrestrial connectivity into mobile networks and devices.

Emerging players like AST SpaceMobile and OQ Technology are working on direct-to-device satellite communication solutions, aiming to connect standard smartphones without additional hardware. Competition in this market is driven by advancements in satellite technology, integration with 5G networks, and the ability to deliver reliable connectivity across both urban and remote regions.

Top Key Players in the Market

- SpaceX

- Amazon

- Apple

- Iridium Satellite Communications

- AST SpaceMobile

- Inmarsat

- OQ Technology

- Qualcomm Technologies, Inc.

- Telefonaktiebolaget LM Ericsson

- Huawei Technologies Co., Ltd.

- Nokia Corporation

- Samsung Electronics Co., Ltd.

- ZTE Corporation

- Thales Group

- Intelsat S.A.

- SES S.A.

- Eutelsat Communications S.A.

- Viasat, Inc.

- Others

Future Outklook

The future outlook for the Non-Terrestrial Network Market looks very strong as the need for seamless global connectivity continues to grow. The market is expected to expand with the integration of satellite networks into next-generation communication systems, enabling reliable coverage in remote and hard-to-reach areas. Increasing deployment of low earth orbit satellites and advancements in space communication technologies are anticipated to improve network performance and reduce delays. In the coming years, closer integration between terrestrial and satellite networks, along with the use of AI for network management, is expected to support wider adoption across telecom, defense, transportation, and IoT applications.

Recent Developments

- April 2, 2026 – SpaceX launches Starlink-375 with 29 satellites from Cape Canaveral. Falcon 9 B1085 completes 15th flight and UK gateway approvals boost Europe capacity. Orbit lowering to 480km enhances safety.

- February, 2026 – Apple partners Globalstar for iPhone satellite SOS expansion. Emergency texting scales to 100M users and direct-to-device 5G trials start. Wearables get NTN connectivity.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | USD 10.4 Billion |

| Forecast Revenue (2035) | USD 173.5 Billion |

| CAGR(2025-2035) | 32.50% |

| Base Year for Estimation | 2024 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue forecast, AI impact on Market trends, Share Insights, Company ranking, competitive landscape, Recent Developments, Market Dynamics and Emerging Trends |

| Segments Covered | By Orbit Type (LEO, MEO, GEO), By Platform (Satellite, HAPS, UAVs/Drones), By End-User (Defense & Security, Agriculture, Maritime, Oil & Gas, Transportation & Logistics, Others) |

| Regional Analysis | North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, New Zealand, Singapore, Thailand, Vietnam, Rest of Latin America; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA |

| Competitive Landscape | SpaceX, Amazon, Apple, Iridium Satellite Communications, AST SpaceMobile, Inmarsat, OQ Technology, Qualcomm Technologies, Inc., Telefonaktiebolaget LM Ericsson, Huawei Technologies Co., Ltd., Nokia Corporation, Samsung Electronics Co., Ltd., ZTE Corporation, Thales Group, Intelsat S.A., SES S.A., Eutelsat Communications S.A., Viasat, Inc., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three license to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF) |