Global MHETase Market Size, Share Analysis Report By Application (Beverage Packaging Recycling, Food Packaging Recycling, PET Textile And Fiber Recycling, PET Film And Sheet Recycling, Industrial PET Scrap Recycling, and Others), By End-User (Waste Management, Plastic Recycling Facilities, Packaging, Textile And Polyester, Biotechnology And Research Institutes, and Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2026-2035

- Published date: Mar 2026

- Report ID: 181421

- Number of Pages: 386

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

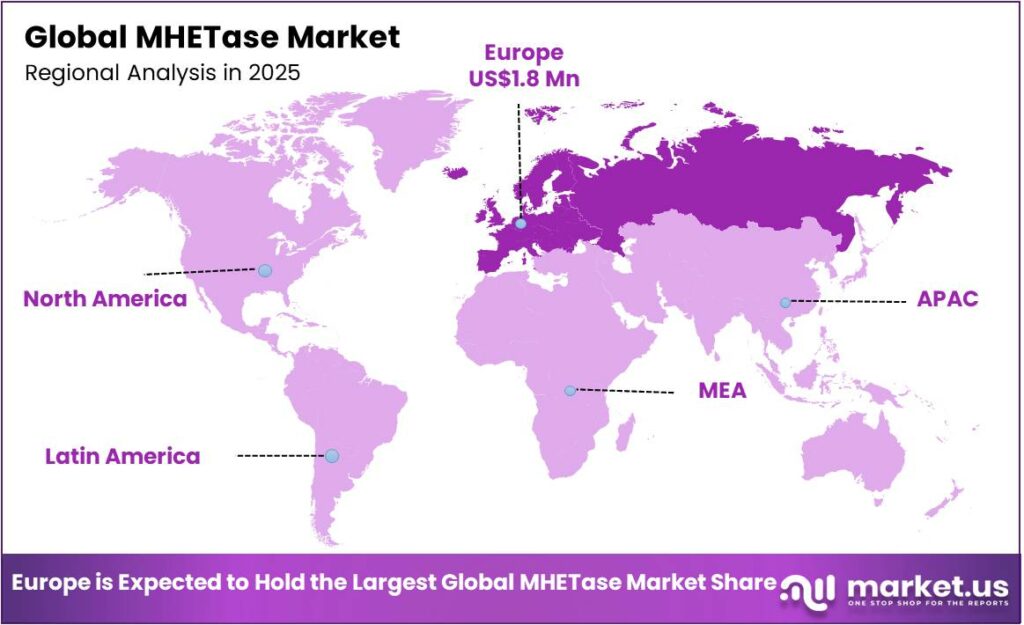

The Global MHETase Market size is expected to be worth around USD 47.7 Million by 2035, from USD 4.2 Million in 2025, growing at a CAGR of 27.5% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 41.6% share, holding USD 1.7 Million revenue.

MHETase (mono(2-hydroxyethyl) terephthalate hydrolase) is a specialized enzyme that plays a critical role in the biological degradation of polyethylene terephthalate (PET), the common plastic used in beverage bottles and synthetic fibers. It was first identified in the bacterium Ideonella sakaiensis 201-F6, which was discovered in 2016 at a Japanese plastic recycling facility. Its market is shaped by the increasing need for efficient enzymatic recycling of PET, particularly in beverage packaging, which provides standardized, low-crystallinity substrates conducive to high conversion rates.

- According to a 2025 report by Plastics Europe, total plastics production in 2024 reached approximately 430.9 million metric tons, out of which PET accounted for around 6.2%, creating a necessity to explore solutions to reduce the waste.

Europe leads in adoption due to substantial plastic waste generation annually, 14.5 million tons in the U.S., and around 5 million tons in Canada, and supportive regulatory frameworks such as the U.S. Plastics Innovation Challenge. Key drivers include global initiatives to reduce plastic waste and the growth of the synthetic textile industry, which generates high volumes of PET suitable for enzymatic degradation.

- According to the National Association for PET Container Resources (NAPCOR), in the United States alone, the PET bottle recycling rate was 30.2% in 2024, following 2023’s peak of 32.5%.

Market participants focus on research and development to improve enzyme stability, activity, and scalability, often deploying dual-enzyme systems combining MHETase with PETase to maximize depolymerization efficiency. Operational deployment is concentrated in plastic recycling facilities, which provide controlled reaction environments and pre-sorted feedstock necessary for effective enzyme application. However, challenges include enzyme sensitivity to industrial conditions, substrate heterogeneity in textiles and industrial scrap, and supply chain constraints for cofactors and purification reagents.

Key Takeaways:

- The global MHETase market was valued at US$4.2 million in 2025.

- The global MHETase market is projected to grow at a CAGR of 27.5% and is estimated to reach US$47.7 million by 2035.

- Based on the applications of MHETase, beverage packaging recycling dominated the MHETase market, with a market share of around 52.4%.

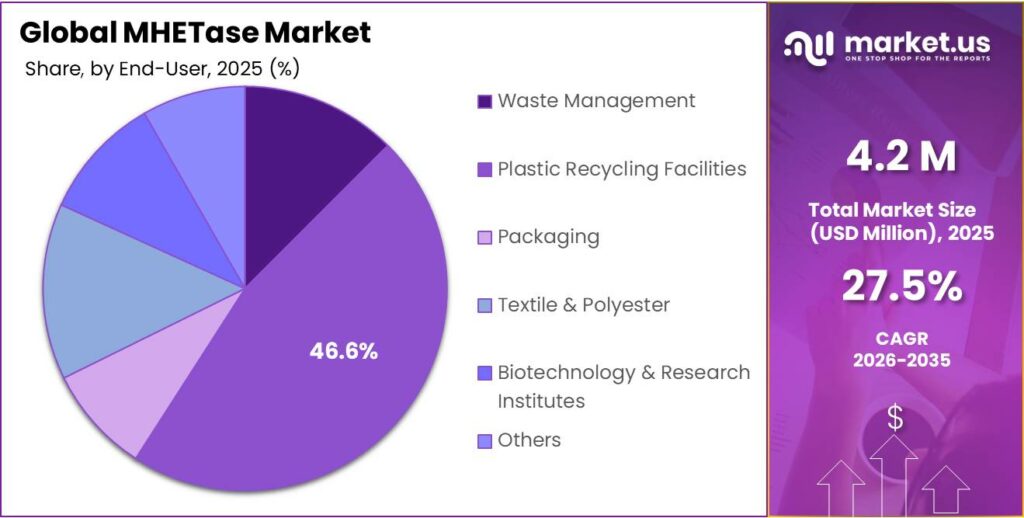

- Among the end-users of MHETase, plastic recycling facilities held a major share in the market, 46.6% of the market share.

- In 2025, Europe was the most dominant region in the MHETase market, accounting for around 41.8% of the total global consumption.

Application Analysis

Beverage Packaging Recycling Held the Largest Share in the MHETase Market.

The MHETase market is segmented based on compound type into beverage packaging recycling, food packaging recycling, pet textile & fiber recycling, pet film & sheet recycling, industrial pet scrap recycling, and others. The beverage packaging recycling dominated the MHETase market, comprising around 52.4% of the market share, as polyethylene terephthalate (PET) bottles are highly standardized in composition, crystallinity, and thickness, which allows consistent enzymatic degradation.

The beverage-grade PET typically has lower crystallinity than textile fibers or industrial PET scrap, enabling MHETase to achieve high depolymerization efficiency, often above 85% under laboratory conditions.

In contrast, PET textiles, films, sheets, and industrial scrap often exhibit heterogeneous compositions, additives, and high crystallinity, which reduce enzymatic accessibility and require extensive pre-treatment. Similarly, standardized beverage containers further generate concentrated, post-consumer waste streams, simplifying collection, sorting, and enzymatic processing. These factors make beverage PET the most operationally compatible and efficient substrate for current MHETase-based recycling systems.

End-User Analysis

MHETase is Mostly Utilized by Plastic Recycling Facilities.

Based on the end-users of MHETase, the market is divided into waste management, plastic recycling facilities, packaging, textile & polyester, biotechnology & research institutes, and others. The plastic recycling facilities dominated the MHETase market, with a market share of 46.6%, as these operations handle large volumes of post-consumer PET, providing the concentrated and pre-sorted feedstocks required for efficient enzymatic depolymerization. Studies indicate that MHETase requires controlled reaction conditions, including specific pH, temperature, and agitation, to achieve high PET conversion rates, conditions that are more readily implemented in recycling plants than in general waste management or packaging facilities.

Furthermore, textile, polyester, and industrial scrap facilities often deal with heterogeneous or high-crystallinity PET, which reduces enzyme efficiency. Similarly, biotechnology and research institutes primarily conduct laboratory-scale studies for innovation rather than continuous, high-volume processing. Consequently, recycling facilities provide the operational infrastructure, standardized inputs, and process control necessary for a practical, scalable MHETase application.

Key Market Segments:

By Application

- Beverage Packaging Recycling

- Food Packaging Recycling

- PET Textile & Fiber Recycling

- PET Film & Sheet Recycling

- Industrial PET Scrap Recycling

- Others

By End-User

- Waste Management

- Plastic Recycling Facilities

- Packaging

- Textile & Polyester

- Biotechnology & Research Institutes

- Others

Drivers

Demand to Reduce Plastic Waste Drives the MHETase Market.

Global regulatory and institutional initiatives to curb plastic waste are driving demand for MHETase, an enzyme that degrades polyethylene terephthalate (PET). As of 2024, over 80 million tons of PET are produced annually. The national mandates act as the primary mechanism for scaling enzymatic technologies such as MHETase. For instance, countries implementing Extended Producer Responsibility (EPR) frameworks, such as Germany and Japan, have achieved recycling rates exceeding 41% and reduced waste generation by up to 90%.

According to Plastics Recyclers Europe, in 2024, European PET recycling capacity slightly increased to 3.3 million tons, with a 24% average recycled content rate for PET bottles. Consequently, chemical recycling programs are increasingly incorporating enzymatic PET degradation. For instance, the U.S. Department of Energy-funded research emphasizes MHETase and PETase co-utilization to enhance PET depolymerization efficiency, achieving up to 90% substrate conversion in controlled laboratory trials. Various studies highlight MHETase as a critical agent for addressing persistent PET residues in post-consumer waste streams.

Restraints

Economic & Scaling Challenges Might Hamper the Demand for MHETase.

Transitioning MHETase from laboratory to industrial scale requires substantial infrastructure shifts. While traditional chemical recycling relies on established petroleum-based assets, enzymatic processes necessitate specialized bacterial fermentation facilities. Scaling MHETase production for industrial PET recycling faces economic and technical constraints. A primary scaling constraint is the production volume required for commercial viability. The enzymes must be produced at a scale of several tons per year to be cost-competitive. Most high-performance variants, such as FAST-PETase, show intrinsic limitations in depolymerization rates that may hinder large-scale application without further directed evolution.

Similarly, a 2022 report from the German Federal Environment Agency notes that enzymatic PET recycling requires high-purity substrates to achieve conversion rates above 80%, necessitating pre-sorting and cleaning steps that increase material handling complexity. Furthermore, enzyme stability is another limitation. The experiments published by the National Renewable Energy Laboratory indicate that MHETase loses 50% activity after 48 hours under industrial agitation conditions, limiting continuous processing. Energy inputs for maintaining reaction conditions and the need for cofactors further elevate operational expenditures.

Opportunity

Rapid Growth of the Synthetic Textile Industry Creates Opportunities in the Market.

The expansion of the synthetic textile industry, primarily driven by polyester, presents a material opportunity for MHETase-based PET recycling. According to the United Nations Environment Programme (UNEP), synthetic fibers comprise approximately 60% of global clothing materials.

Similarly, according to the Textile Exchange 2025 report, polyester continued to be the most widely produced fiber, making up 59% of total global fiber output, of which 88% is fossil-based. In terms of volume, polyester fiber production increased from around 71 million tons in 2023 to around 78 million tons in 2024. This creates a vast, underserved reservoir of complex waste for enzymatic depolymerization.

Furthermore, the U.S. Environmental Protection Agency reports that textiles contribute 5.3 million tons to U.S. municipal solid waste annually, of which polyester fibers constitute an estimated 60-65%. Polyester’s chemical composition, primarily polyethylene terephthalate, aligns with the substrate specificity of MHETase, facilitating enzymatic depolymerization. Research by the European Commission Joint Research Centre highlights that increasing post-consumer textile recycling is critical to meeting circular economy targets, underscoring enzymatic approaches as scalable solutions for polyester waste streams in the growing synthetic textile sector.

Trends

Adoption of Dual-Enzyme Systems.

The shift toward dual-enzyme systems, specifically the combination of PETase and MHETase, is driven by the need to overcome kinetic bottlenecks in plastic depolymerization. While PETase initiates the breakdown of polyethylene terephthalate, the resulting intermediate, mono(2-hydroxyethyl) terephthalate (MHET), often acts as a competitive inhibitor, stalling the reaction. The disclosures from the National Renewable Energy Laboratory (NREL) and the University of Portsmouth demonstrate that dual-enzyme systems achieve a synergistic relationship, significantly increasing the conversion rate of amorphous PET film into monomers across all tested concentrations.

Similarly, laboratory studies published in the National Institutes of Health (NIH) demonstrate that co-application of PETase and MHETase can achieve PET conversion rates exceeding 90% under controlled conditions, compared to 60-70% when each enzyme is used individually. Moreover, a secondary trend involves whole-cell systems where both enzymes are expressed on the surface of microorganisms such as Saccharomyces cerevisiae or P. pastoris. These systems offer improved stability and reusability, with some yeast-based catalysts maintaining activity for seven repeated cycles.

Geopolitical Impact Analysis

Geopolitical Tensions Are Impacting the MHETase Infrastructure Investment.

Geopolitical tensions, particularly disruptions in international trade and supply chains, have implications for the development and deployment of MHETase-based PET recycling. The U.S. Department of Commerce reported that global supply chain delays, including in biotechnological and chemical reagents, increased average lead times for imported laboratory enzymes between 2021 and 2024. According to the International Monetary Fund (IMF), geopolitical uncertainty has led to a 1% increase in global financial stress indices, which elevates the cost of capital for the capital-intensive bioreactor infrastructure necessary to scale MHETase.

Similarly, in Asia, Japan’s Ministry of Economy, Trade, and Industry indicates that cross-border shipping disruptions caused by regional conflicts resulted in an increase in import clearance times for biochemicals. Moreover, a consistent supply of cofactors and purification reagents is essential for maintaining MHETase activity in controlled PET depolymerization trials. These data suggest that geopolitical disruptions can constrain raw material availability, delay scale-up operations, and affect the consistent application of enzymatic recycling processes, emphasizing the strategic need for localized production and diversified supply chains.

Regional Analysis

Europe Held the Largest Share of the Global MHETase Market.

In 2025, Europe dominated the global MHETase market, holding about 41.8% of the total global consumption, largely driven by regional regulatory frameworks and industrial adoption of PET recycling technologies. According to Plastics Europe, the EU produced approximately 2.5 million metric tons of PET in 2024, a 4.6% of the total plastics production of 54.6 million metric tons in the region. Germany alone reported 11.7 million metric tons of PET production in 2024, the highest among EU member states. In addition, Belgium, France, Spain, Italy, and the Netherlands demonstrated high production rates.

- According to Plastics Recyclers Europe, the plastics recycling industry in Europe represents over EUR8.6 billion in turnover, 13.5 million tons of installed recycling capacity, around 850 recycling facilities, and around 30,000 employees, indicating a robust base for enzymatic PET degradation.

Moreover, there are several ongoing industrial deployments in the region, which underscore Europe’s early-mover advantage in adopting MHETase-based recycling solutions, reflecting both regulatory alignment and technical infrastructure readiness. The public pilot-scale implementations and national-level recycling targets support the position of Europe as the leading operational market for MHETase applications.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of MHETase primarily focus on research and development to enhance enzyme efficiency, stability, and substrate specificity. Publicly disclosed laboratory programs, such as those funded by the U.S. Department of Energy, emphasize protein engineering to increase activity under industrial conditions, including high-crystallinity PET and variable pH or temperature environments.

In addition, firms prioritize scaling production processes, improving fermentation yields, and optimizing purification protocols to support continuous or large-volume enzymatic recycling operations. Moreover, collaboration with academic institutions and government research agencies is another key activity, enabling access to advanced biocatalysis techniques and pilot-scale testing.

The Major Players in The Industry

- Creative Enzymes

- Carbios

- GenScript

- Twist Bioscience

- Other Key Players

Key Development

- In April 2024, CARBIOS, a leader in biological technologies for sustainable plastics and textiles, inaugurated the world’s first PET biorecycling plant in Longlaville, France. The facility, capable of processing 50,000 tons of PET waste annually, aimed to advance circular economy initiatives, enabling industrial-scale enzymatic depolymerization and contributing to plastic pollution reduction.

Report Scope:

Report Features Description Market Value (2025) US$4.2 Mn Forecast Revenue (2035) US$47.7 Mn CAGR (2025-2035) 27.5% Base Year for Estimation 2025 Historic Period 2021-2024 Forecast Period 2025-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Application (Beverage Packaging Recycling, Food Packaging Recycling, PET Textile & Fiber Recycling, PET Film & Sheet Recycling, Industrial PET Scrap Recycling, and Others), By End-User (Waste Management, Plastic Recycling Facilities, Packaging, Textile & Polyester, Biotechnology & Research Institutes, and Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape Creative Enzymes, Carbios, GenScript, Twist Bioscience, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- Creative Enzymes

- Carbios

- GenScript

- Twist Bioscience

- Other Key Players

Our Clients

- 181421

- Mar 2026