Medical Specialty Bags Market By Product Type (Intravenous Fluid Bags, Sterile Collection & Drainage Bags, Ostomy Bags, Continuous Ambulatory Peritoneal Dialysis Bags, and Others), By Material (PVC, PE & PP, and Others), By End-user (Hospitals, ASCs, and Others), Region and Companies – Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Aug 2025

- Report ID: 156425

- Number of Pages: 344

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

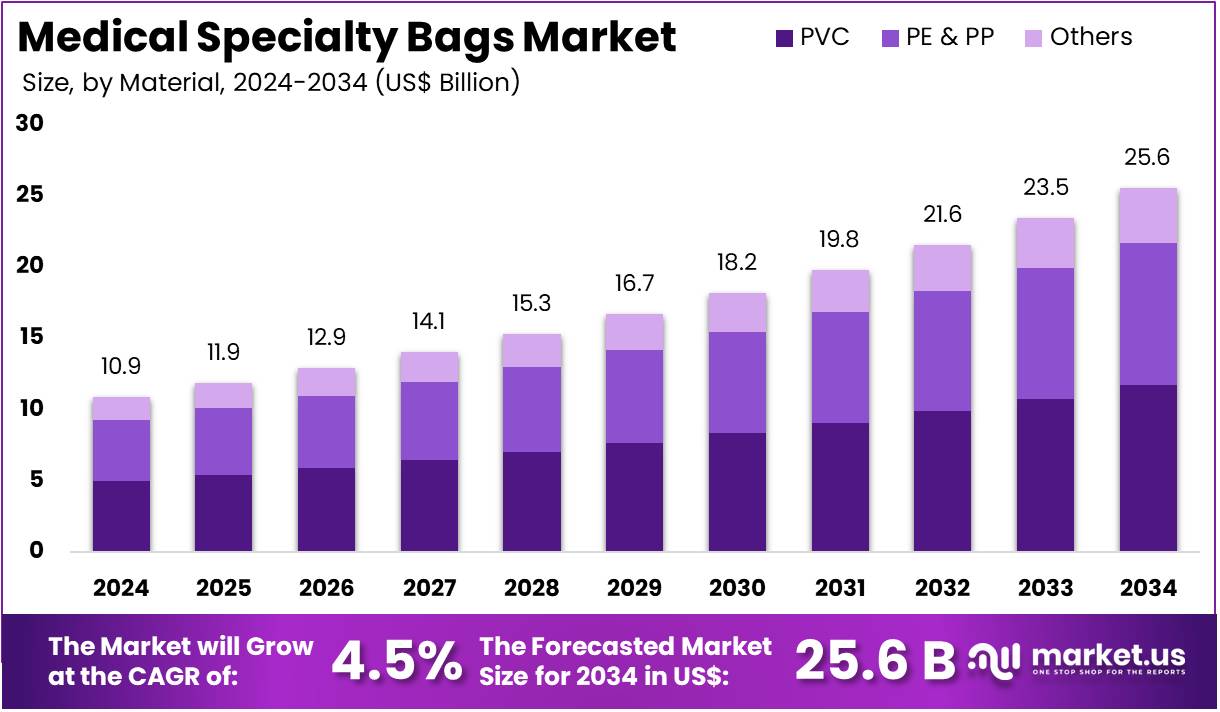

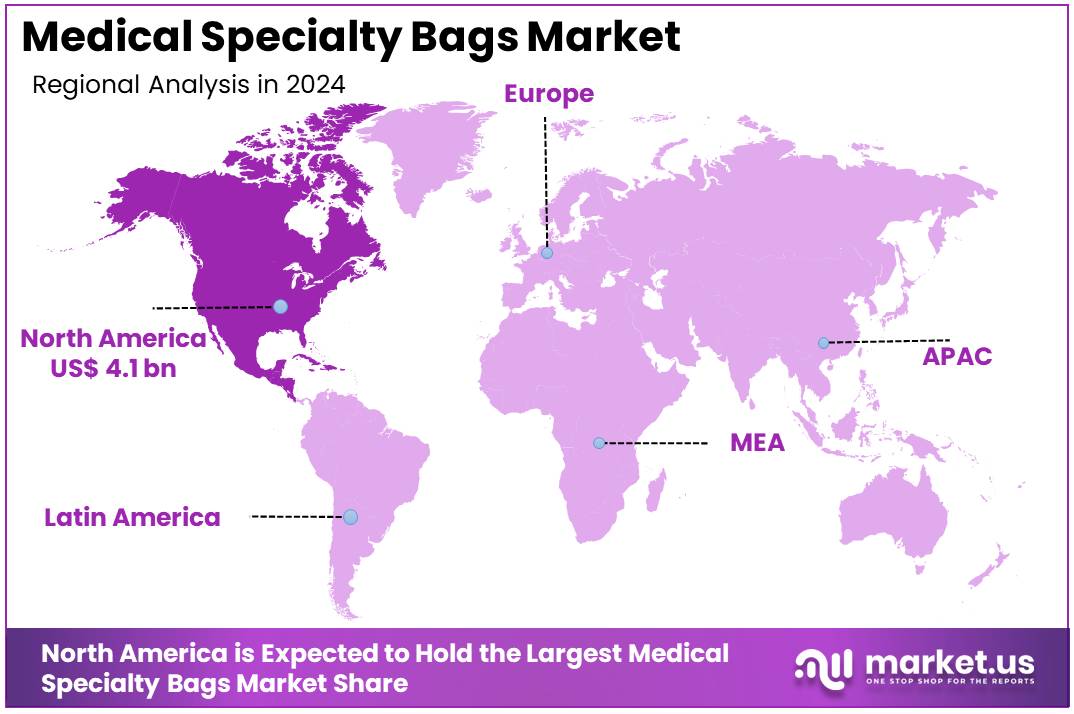

The Medical Specialty Bags Market Size is expected to be worth around US$ 25.6 billion by 2034 from US$ 10.9 billion in 2024, growing at a CAGR of 4.5% during the forecast period 2025 to 2034. North America held a dominant market position, capturing more than a 37.8% share and holds US$ 4.1 Billion market value for the year.

The medical specialty bags market is experiencing a period of robust growth, driven primarily by the global rise in the elderly population and the increasing prevalence of acute diseases. A key factor is the high incidence of conditions such as urinary bladder cancer and other related disorders, which disproportionately affect older individuals.

The American Cancer Society reports that bladder cancer is most common in older individuals, with approximately 90% of cases occurring in people over the age of 55, and men having a significantly higher lifetime risk than women. This demographic shift, coupled with the ongoing need for fluid management in treating such conditions, is creating a sustained demand for a variety of specialized medical bags.

The market’s expansion is further propelled by a strong emphasis on infection control and prevention. Healthcare facilities are increasingly adopting single-use, disposable bags to mitigate the risk of cross-contamination and healthcare-associated infections (HAIs). This focus on patient safety is driving the demand for high-quality, hygienic medical bags that adhere to stringent regulatory standards.

The Centers for Disease Control and Prevention (CDC) provides data that underscores this critical need, reporting that on any given day, about 1 in 31 hospital patients in the US has at least one HAI. This highlights the importance of disposable medical products in maintaining sterile environments and ensuring patient safety. The World Health Organization (WHO) also notes that the global blood supply relies on the donation of approximately 120 million units of blood annually, and all of these blood storage and transfusion activities require sterile blood bags, reinforcing the continuous need for these specialty products.

The market is also being reshaped by continuous improvements in product design, materials, and manufacturing processes. Manufacturers are integrating advanced technologies, such as real-time monitoring systems and RFID tracking, to enhance the durability, sterility, and convenience of these bags. A prime example of this innovation is the introduction of novel drug delivery systems like Gufic Biosciences’ dual-chamber bags in June 2022. These bags allow for the safe storage of unstable medications that can be reconstituted immediately before administration, improving medication stability and patient convenience. This strategic focus on technological advancements makes medical specialty bags more attractive to both healthcare providers and patients, further fueling market growth.

Key Takeaways

- In 2024, the market for medical specialty bags generated a revenue of US$ 10.9 billion, with a CAGR of 4.5%, and is expected to reach US$ 25.6 billion by the year 2034.

- The product type segment is divided into intravenous fluid bags, sterile collection & drainage bags, ostomy bags, continuous ambulatory peritoneal dialysis bags, and others, with ostomy bags taking the lead in 2023 with a market share of 38.5%.

- Considering material, the market is divided into PVC, PE & PP, and others. Among these, PVC held a significant share of 45.8%.

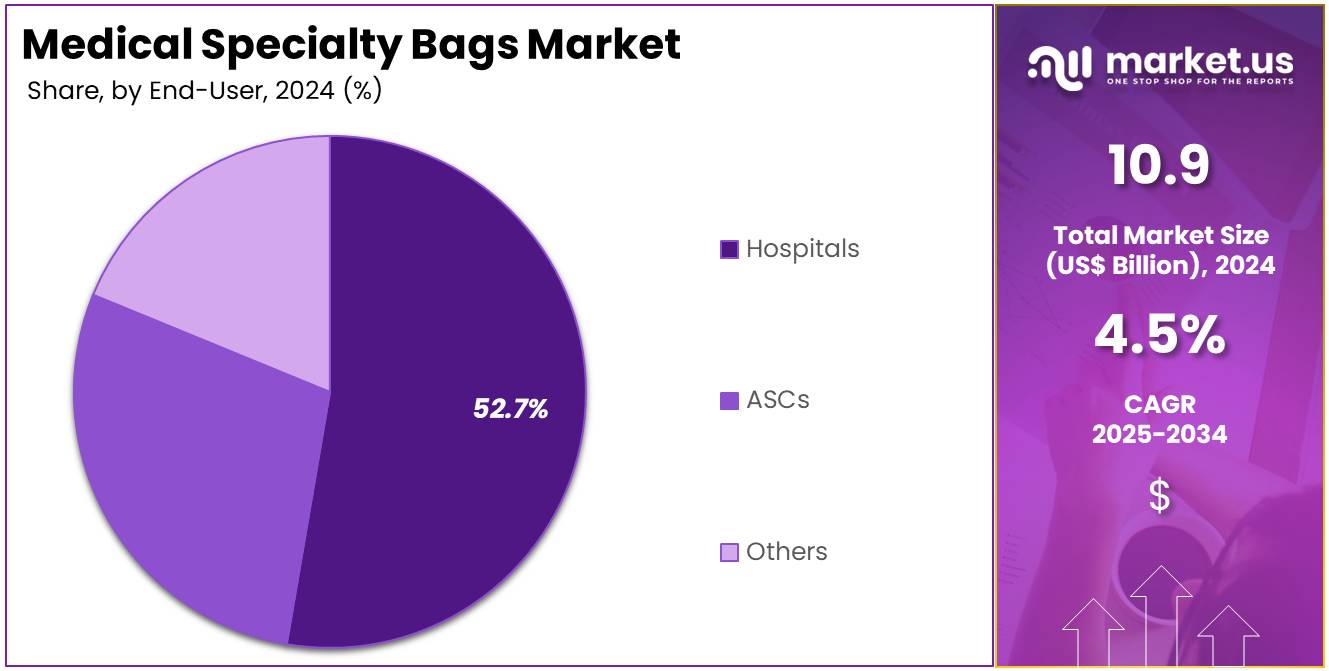

- The end-user segment is segregated into hospitals, ASCs, and others, with the hospitals segment leading the market, holding a revenue share of 52.7%.

- North America led the market by securing a market share of 37.8% in 2023.

Product Type Analysis

Ostomy bags hold the largest share of 38.5% in the medical specialty bags market. This growth is expected to continue due to the increasing incidence of chronic conditions such as colorectal cancer, inflammatory bowel disease (IBD), and urological disorders, all of which frequently require ostomy procedures. The demand for ostomy bags is projected to rise as the global aging population increases, leading to a greater number of individuals requiring ostomy care.

Technological advancements in ostomy bag design, including improved comfort, leakage prevention, and skin-friendly features, are likely to drive market adoption. Additionally, the growing emphasis on post-operative care and quality of life for ostomy patients is expected to further contribute to the segment’s growth.

The increasing availability of specialized ostomy products and patient education programs will likely enhance adoption rates, especially in emerging markets where healthcare access is improving. Furthermore, healthcare initiatives that focus on improving the management and treatment of chronic conditions are anticipated to increase the overall demand for ostomy bags.

Material Analysis

PVC accounts for 45.8% of the material segment in the medical specialty bags market. This segment’s growth is projected to continue as PVC remains the preferred material for medical specialty bags due to its durability, flexibility, and low cost. PVC’s ability to be easily molded into various shapes and sizes makes it ideal for a wide range of medical applications, including intravenous fluid bags, ostomy bags, and drainage bags. The material’s resistance to chemicals and its biocompatibility contribute to its widespread use in hospitals and clinics.

Additionally, PVC offers transparency, allowing healthcare providers to monitor contents visually, which is essential for certain medical procedures. Technological advancements in PVC formulations, such as the development of more eco-friendly and lightweight variants, are expected to drive growth. Hospitals, which make up a significant portion of the market, prefer PVC bags due to their affordability and reliability. As the demand for medical specialty bags rises globally, PVC’s role in maintaining product quality and safety is expected to further enhance its market share.

End-User Analysis

Hospitals represent 52.7% of the end-user segment in the medical specialty bags market. This growth is expected to continue as hospitals remain the primary settings for specialized medical treatments and surgeries, where medical bags are critical for patient care. The increasing number of surgeries and medical procedures requiring ostomy, drainage, and fluid management is expected to drive the demand for medical specialty bags in hospitals. Furthermore, hospitals are likely to adopt more advanced and patient-friendly specialty bags as part of their efforts to improve post-operative care and overall patient outcomes.

The growing prevalence of chronic diseases, such as heart failure, diabetes, and cancer, is likely to increase the need for medical bags in hospitals. As the healthcare infrastructure expands globally, particularly in emerging markets, hospitals will continue to drive the demand for reliable and cost-effective medical bags. Innovations in product designs, such as enhanced comfort and security features in ostomy bags, are expected to make hospital adoption even more widespread. Additionally, hospitals’ focus on ensuring patient safety and comfort, particularly during extended care periods, will sustain the demand for high-quality medical specialty bags.

Key Market Segments

By Product Type

- Intravenous Fluid Bags

- Sterile Collection & Drainage Bags

- Ostomy Bags

- Continuous Ambulatory Peritoneal Dialysis Bags

- Others

By Material

- PVC

- PE & PP

- Others

By End-User

- Hospitals

- ASCs

- Others

Drivers

The rising prevalence of chronic diseases requiring long-term care is driving the market

The market for medical specialty bags is experiencing significant growth, primarily driven by the rising global burden of chronic diseases and the subsequent increase in demand for long-term care solutions. Patients with conditions such as cancer, inflammatory bowel disease, and chronic kidney disease often require ostomy, urostomy, or drainage care, which necessitates the use of these specialized medical devices.

According to the United Ostomy Associations of America, there are an estimated 750,000 to 1 million people with an ostomy in the US alone, with approximately 120,000 to 150,000 new surgeries performed each year. Additionally, a 2023 World Health Organization (WHO) report on chronic kidney disease noted its rising prevalence, with an estimated 850 million people affected worldwide. The consistent increase in the patient population requiring these care modalities ensures a steady and growing demand for the specialty products that facilitate their daily lives and medical management, thereby sustaining a robust market.

Restraints

The risk of device-related infections and a focus on infection control are restraining the market

A significant restraint on the market is the ongoing risk of medical device-related infections, which can lead to serious patient complications and increased healthcare costs. Specialty bags, particularly those used for urinary drainage or fluid collection, can become a source of hospital-acquired infections (HAIs) if not managed properly. Catheter-associated urinary tract infections (CAUTIs), for example, are a major concern in clinical settings. The US Centers for Disease Control and Prevention (CDC) reported that in 2023, the number of catheter-associated urinary tract infections in US hospitals remained a serious concern.

The costs associated with treating these preventable infections are substantial, with some estimates placing the additional cost per patient between $1,768 and $22,568. This push for stricter infection control measures is prompting healthcare providers to scrutinize their use of indwelling devices and consider alternative, lower-risk solutions. This focus on infection prevention, a factor that can deter use, consequently acts as a restraint on the market.

Opportunities

The growing adoption of home healthcare is creating growth opportunities

The market is presented with significant opportunities from the rapid expansion of the home healthcare sector. As healthcare systems globally seek to reduce hospital stays and lower costs, more patients are receiving medical care and monitoring in the comfort and convenience of their own homes. These specialty products are uniquely positioned to serve this trend, as they provide a safe, effective, and easy-to-use solution for patients managing chronic conditions or recovering from surgery outside of a traditional clinical setting.

According to data from the US Bureau of Labor Statistics, employment in the home healthcare services sector added 178,200 jobs between February 2020 and February 2024, demonstrating a robust and sustained shift toward decentralized care. This growth is also supported by patient preference; a 2023 report from the National Council on Aging found that a majority of older adults express a desire to “age in place.” As the aging population and the prevalence of chronic diseases continue to rise, the shift toward home-based care provides a major avenue for the market’s expansion, particularly for manufacturers who can produce reliable, user-friendly products for non-clinical settings.

Impact of Macroeconomic / Geopolitical Factors

The medical specialty bags market is currently navigating a challenging macroeconomic and geopolitical environment. The cost of essential raw materials, particularly medical-grade plastics like PVC and polyurethane, is subject to significant price fluctuations. A 2024 report on commodity plastics highlights that polyvinyl chloride (PVC) is the third most produced polymer globally.

Geopolitical tensions have created supply chain instability, with a recent analysis noting that the cost of shipping a 40-foot container from Asia to the U.S. West Coast was priced at over $5,000 in early 2025 due to a combination of geopolitical issues and logistical pressures. US tariff policies are also impacting the supply chain, as specific US government tariff trackers indicate that medical devices imported from certain countries, including China, face duties that can exceed 100% on specific items like surgical gloves and syringes, affecting procurement budgets.

Despite these challenges, the market is showing resilience. The US government’s CHIPS and Science Act, which provides over $50 billion in funding for domestic semiconductor manufacturing, has a direct impact on the localization of critical components for medical devices. This, along with other programs promoting domestic production, is strengthening the US manufacturing base and ensuring a more secure and resilient supply chain.

Latest Trends

The trend toward digitalization and smart bags with integrated technology is a recent development

A significant trend in 2024 is the shift toward integrating digital and smart technologies into traditionally passive medical devices. Manufacturers are developing specialty bags that incorporate sensors for real-time monitoring of fluid levels, temperature, and other vital parameters. These “smart bags” can then transmit data wirelessly to a patient’s smartphone or a clinician’s dashboard, enabling remote monitoring and improving patient safety and care management.

A 2024 report by the American Medical Association (AMA) highlighted that digital health adoption among physicians reached 93%, with remote patient monitoring and connected devices seeing a significant increase in use. This trend is driven by the demand for more patient-centric care and a need to reduce the burden on healthcare professionals. The development of such innovative products is elevating the market by providing solutions that improve efficiency and clinical outcomes, thereby making a previously analog product part of the modern connected care ecosystem.

Regional Analysis

North America is leading the Medical Specialty Bags Market

The North American market for medical specialty bags accounted for a 37.8% share in 2023. This is a direct result of the region’s strong and well-established healthcare infrastructure and a high rate of technology adoption. Pharmaceutical and medical device companies are consistently investing in the development of advanced medical specialty bags to meet a rising demand.

The Centers for Medicare & Medicaid Services (CMS) reported that US National Health Expenditures reached US$4.9 trillion in 2023, representing a 7.5% increase from the previous year. This significant spending on healthcare, which constitutes over 17% of the nation’s GDP, underscores the robust financial ecosystem that supports the adoption of innovative medical products.

The US market is expected to grow substantially, driven by a highly competitive landscape where manufacturers are leveraging advanced materials and smart technologies to enhance the functionality and safety of their products. For example, major players are investing in automated and robotic manufacturing facilities. A key instance is Assure Infusions Inc.’s US$20 million investment in a new 60,000-square-foot robotics facility in Bartow, Florida, which broke ground in 2022. This facility is designed to produce intravenous fluid bags with a higher degree of precision and quality control, demonstrating the industry’s focus on technological innovation and supply chain efficiency.

The Asia Pacific region is expected to experience the highest CAGR during the forecast period

The Asia Pacific medical specialty bags market is anticipated to experience the fastest growth during the forecast period. This is largely a result of the region’s increasing focus on investing in its healthcare sector to support a large and rapidly growing population. For instance, in India, the Ministry of Health and Family Welfare’s expenditure was budgeted at US$11 billion for the 2024-2025 fiscal year, reflecting a 13% rise over the revised estimates for 2023-2024. This significant increase in government spending is projected to support the development of healthcare infrastructure and a corresponding demand for medical supplies.

China’s medical specialty bags market is witnessing robust growth, driven by the country’s expanding healthcare sector and government initiatives to improve quality and access. Manufacturers in China are leveraging strong research and development capabilities to create innovative bags with advanced features and materials. This trend is driven by the Chinese government’s emphasis on enhancing patient outcomes and promoting the use of cutting-edge medical technologies. Additionally, per capita expenditure on healthcare and medical services in China increased from 2,460 RMB in 2023 to 2,547 RMB in 2024, highlighting the rising consumer willingness to spend on healthcare.

Key Regions and Countries

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia

- Netherland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Singapore

- Thailand

- Vietnam

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

Key players in the medical bag market are driving growth by implementing a dual strategy of technological innovation and geographical expansion. Companies are consistently developing next-generation products with enhanced features, such as dual chambers for specific therapies and advanced materials for improved durability and patient comfort. They are also actively expanding their manufacturing and distribution networks into developing economies, where rising incidences of chronic diseases and improving healthcare infrastructure are fueling demand for cost-effective medical supplies.

Furthermore, manufacturers are increasingly collaborating with healthcare providers to develop customized solutions that meet specific clinical needs in a variety of care settings, from hospitals to home care. Braun is a German medical and pharmaceutical device company that operates globally. Founded in 1839, the company specializes in a wide range of healthcare products, including those used for infusion therapy and surgical applications.

B. Braun consistently focuses on developing innovative solutions that improve safety and efficiency for patients and healthcare professionals. The company’s strategic emphasis on providing comprehensive systems, from devices to consumables, strengthens its market position as a key provider of integrated healthcare solutions.

Top Key Players in the Medical Specialty Bags Market

- Xheme

- Westfield Medical Ltd

- Vonco Products LLC

- Terumo Corporation

- SB-KAWASUMI LABORATORIES, INC

- Pall Corporation

- Macopharma

- Hollister Incorporated

- Fresenius Medical Care AG

- Convatec Inc

- Coloplast A/S

- BD

- Baxter

- Braun SE

Recent Developments

- In July 2025: B. Braun Medical Inc. expanded its US product range by launching new heparin sodium premixed infusions. These new offerings include 25,000-unit bags available in 50 units/mL and 100 units/mL concentrations, further enhancing the company’s presence in the critical care market.

- In May 2025, Endo, Inc. introduced ADRENALIN, a premixed solution of epinephrine in 0.9% sodium chloride, available in 8 mg/250 mL bags. This new product is designed to cater specifically to the emergency medicine market, providing a ready-to-use formulation for rapid administration in critical situations.

- In February 2024: Xheme, a company with a reputation for creating advanced medical technologies, established a partnership with the Vitalant Research Institute. The collaboration is focused on developing a new, non-toxic blood bag that completely eliminates PVC. This initiative represents a substantial advancement in the field of blood storage and transfusion, offering a safer and more sustainable alternative to traditional methods.

- In January 2022, Vonco Products LLC, a prominent manufacturer of medical packaging solutions, executed a strategic acquisition of Flex-Pak Packaging Products, Inc. This maneuver was designed to expand Vonco’s product portfolio and manufacturing capabilities, particularly in the flexible and sterile barrier pouch segments. The acquisition strengthens Vonco’s market position and enhances its ability to provide a more comprehensive suite of solutions to its clientele.

Report Scope

Report Features Description Market Value (2024) US$ 10.9 billion Forecast Revenue (2034) US$ 25.6 billion CAGR (2025-2034) 4.5% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, COVID-19 Impact, Competitive Landscape, Recent Developments Segments Covered By Product Type (Intravenous Fluid Bags, Sterile Collection & Drainage Bags, Ostomy Bags, Continuous Ambulatory Peritoneal Dialysis Bags, and Others), By Material (PVC, PE & PP, and Others), By End-user (Hospitals, ASCs, and Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Russia, Netherlands, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, New Zealand, Singapore, Thailand, Vietnam, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – South Africa, Saudi Arabia, UAE, Rest of MEA Competitive Landscape Xheme, Westfield Medical Ltd, Vonco Products LLC, Terumo Corporation, SB-KAWASUMI LABORATORIES, INC, Pall Corporation, Macopharma, Hollister Incorporated, Fresenius Medical Care AG, Convatec Inc, Coloplast A/S, BD, Baxter, B. Braun SE. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)  Medical Specialty Bags MarketPublished date: Aug 2025add_shopping_cartBuy Now get_appDownload Sample

Medical Specialty Bags MarketPublished date: Aug 2025add_shopping_cartBuy Now get_appDownload Sample -

-

- Xheme

- Westfield Medical Ltd

- Vonco Products LLC

- Terumo Corporation

- SB-KAWASUMI LABORATORIES, INC

- Pall Corporation

- Macopharma

- Hollister Incorporated

- Fresenius Medical Care AG

- Convatec Inc

- Coloplast A/S

- BD

- Baxter

- Braun SE

Our Clients

- 156425

- Aug 2025