Quick Navigation

Report Overview

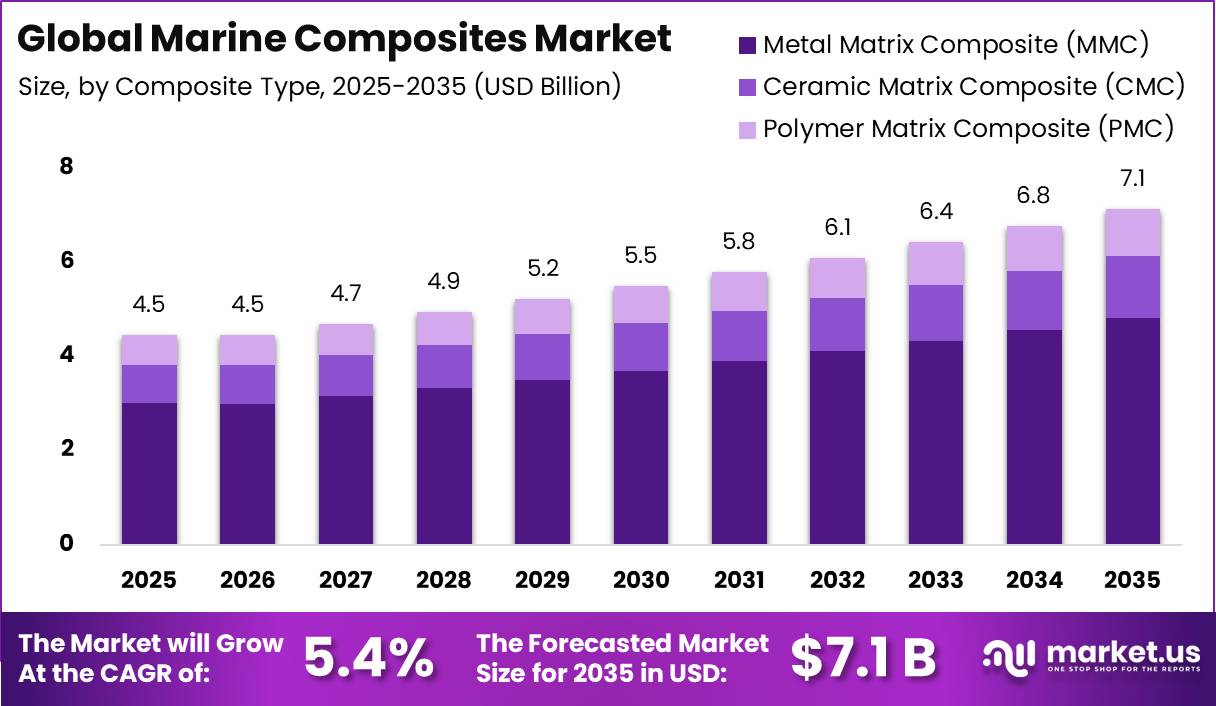

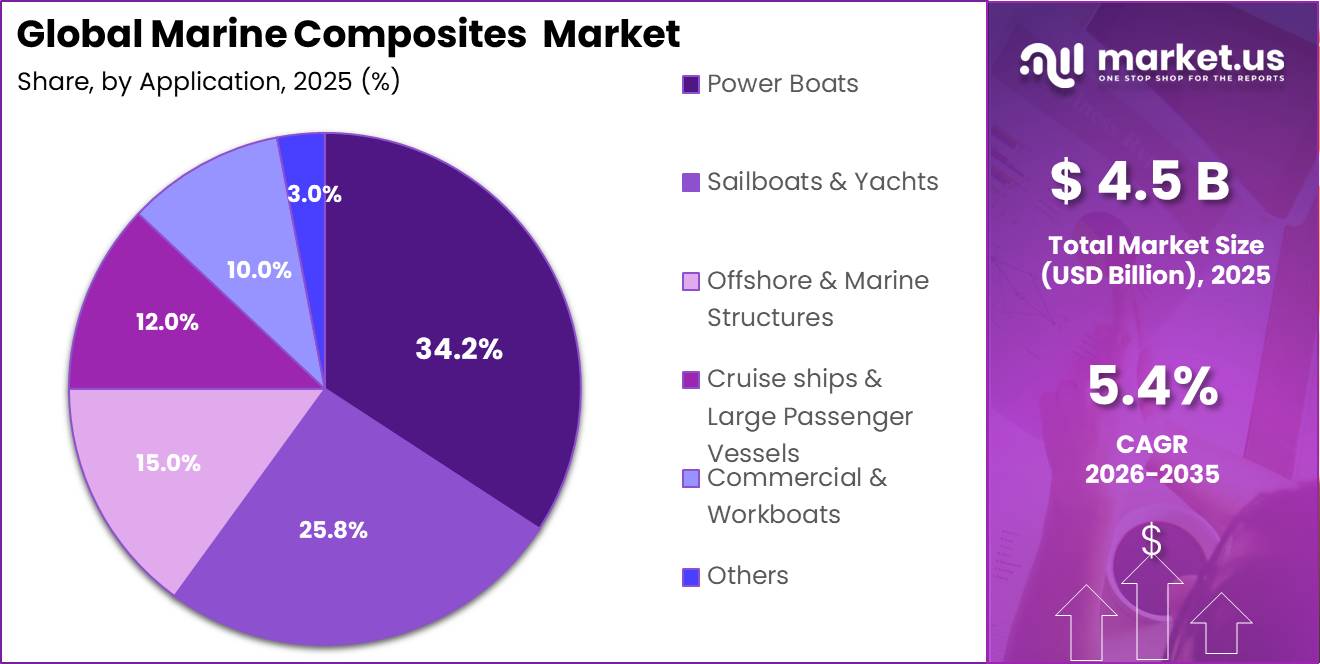

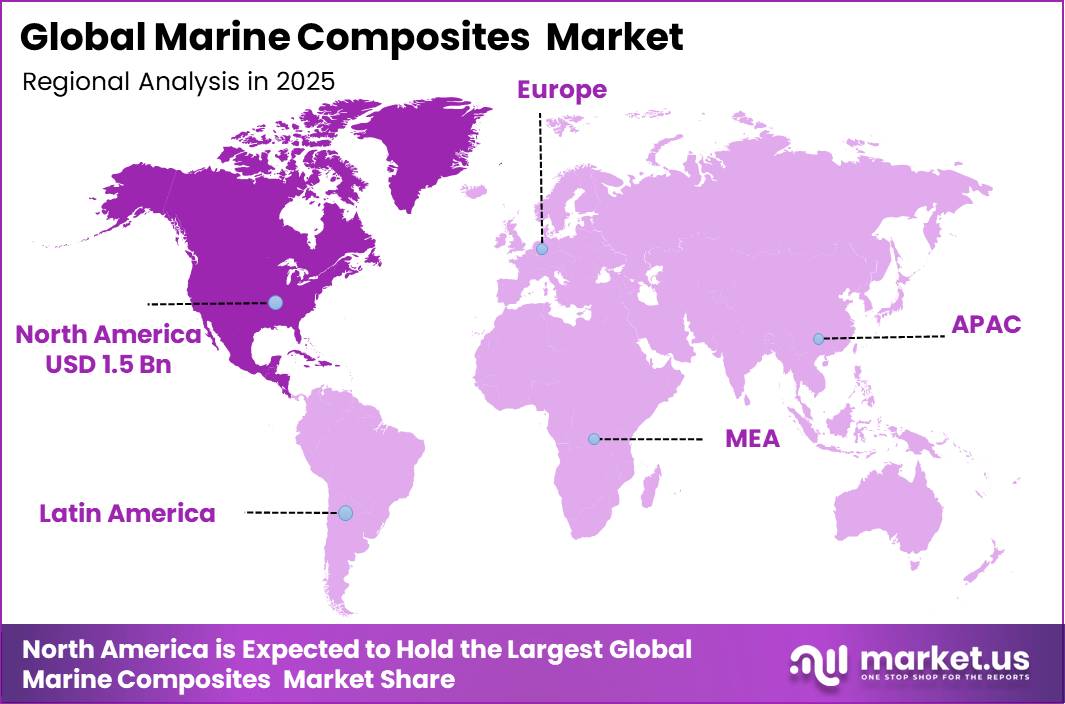

The Global Marine Composites Market is valued at around US$ 4.5 billion in 2025 and is expected to grow steadily at a CAGR of 5.4% from 2026 to 2035, reaching about US$ 7.1 billion by 2035. North America held a dominant market position, capturing more than a 33.7% share, holding USD 1.5 billion in revenue.

Marine composites represent a mature yet fast-evolving class of engineered materials, combining high-performance fibers such as glass, carbon and basalt with tailored resin systems to deliver structures optimized for strength, stiffness and durability in demanding marine environments. At a technical level, standard PAN-based carbon fibers used in shipbuilding provide tensile strengths in the 3,340–6,200 MPa range and tensile moduli of 220–440 GPa, while ultra-high modulus pitch-based fibers can reach 685–965 GPa, enabling lightweight primary structures with excellent load-carrying capacity in global commercial, naval and recreational fleets.

Marine-grade thermoset epoxies complement these fibres with flexural strengths of 85–120 MPa, tensile strengths of 60–90 MPa and compressive strengths of 100–140 MPa, allowing designers to achieve balanced performance under bending, tension and compression across hulls, decks and superstructures.

From an operational perspective, the shift to advanced sandwich and FRP construction has already demonstrated tangible efficiency gains: on the commercial car carrier Siem Cicero, fiberglass-and-foam sandwich decks reduced mass by 25% versus steel and delivered a reported 4% fuel saving, directly impacting voyage economics and emissions.

In lifecycle cost terms, GFRP solutions increasingly outperform steel in harsh marine exposure; over 50 years, a GFRP marina pier has been shown to reduce total cost by about 35% thanks to virtually zero corrosion-related repairs, and GFRP rebar can deliver 30–40% lower life-cycle cost than steel despite higher initial material prices, with savings driven by maintenance avoidance rather than capital expenditure.

Key Takeaways

- The global marine composites market is projected to reach around US$ 7.1 billion by 2035 with a CAGR of 5.4%, rising from approximately US$ 4.5 billion in 2025.

- Metal Matrix Composites (MMC) dominated the market, constituting 67.3% of the total market share.

- Based on resin type, Polyester dominated the market, accounting for 38.4% of the total market share.

- On the basis of application, Power Boats led the market, comprising 34.2% of the total market share.

- Among regions, North America was the dominant market, accounting for 33.7% of the total global share.

Composite Type

The Marine Composites market continues to witness Polymer Matrix Composites (PMC) dominating with a market share exceeding 38.1%. These composites, comprising a blend of polymer resin and reinforcing fibers, remain the primary choice in marine applications due to their excellent performance characteristics.

Meanwhile, Ceramic Matrix Composites (CMC) are expected to show steady growth, driven by their high stiffness and chemical inertness, making them increasingly suitable for specialized marine applications. CMC accounted for 30.4% global market share in 2021, and its relevance continues to expand in advanced marine engineering applications in 2025 as well.

By Resin Type

Polyester Resin Dominates Marine Composites Market Due to Cost Efficiency and Wide Marine Applications

Polyester resin dominates the global marine composites market, accounting for 38.4% share, due to its low cost, easy processing, and strong suitability for large-scale marine manufacturing. It is widely used in boat hulls, decks, and structural components because it offers a balanced combination of mechanical strength, durability, and water resistance.

Epoxy resin holds a 29.5% share, driven by its superior mechanical strength, excellent adhesion, and high resistance to moisture and chemicals, making it suitable for high-performance and premium marine applications. Vinyl ester resin accounts for 17.5% share, valued for its enhanced corrosion resistance in harsh marine environments, while other resin types contribute 14.6% share, serving specialized and niche applications across the industry.

By Application

Power Boats Lead Marine Composites Market Driven by Demand for Lightweight and High-Performance Vessels

Power boats dominate the global marine composites market, accounting for 34.2% share, driven by strong demand for lightweight, high-speed, and fuel-efficient vessels. Marine composites are widely used in power boats due to their excellent strength-to-weight ratio, corrosion resistance, and durability in harsh marine environments.

Other key application areas include sailboats & yachts (15.0%), commercial & workboats (16.0%), cruise ships & large passenger vessels (12.0%), and offshore & marine structures (8.0%). These segments rely on marine composites to improve structural efficiency, reduce maintenance costs, and enhance operational performance.

Key Market Segments

By Composite Type

- Metal Matrix Composite (MMC)

- Ceramic Matrix Composite (CMC)

- Polymer Matrix Composite (PMC)

By Resin Type

- Epoxy

- Polyester

- Vinyl Ester

- Others

By Application

- Power Boats

- Sailboats & Yachts

- Commercial & Workboats

- Cruise ships & Large Passenger Vessels

- Offshore & Marine Structures

- Others

Market Dynamics

Drivers

| Driver | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IMO & Regional Emission Control Area Compliance Mandates | +1.4% | Global, with acute pressure in North Sea, Baltic, Mediterranean ECAs | Short term (≤ 2 years) |

| Offshore Wind Turbine Blade & Structural Demand | +1.2% | Europe, Asia Pacific (China, India), North America | Medium term (2–4 years) |

| Naval & Defense Fleet Modernization Programs | +0.9% | North America, Europe, Indo-Pacific | Medium term (2–4 years) |

| Fuel Efficiency & Lightweighting Imperatives in Commercial Shipping | +0.8% | Global, strongest in Asia Pacific shipbuilding hubs | Short term (≤ 2 years) |

| Recreational Marine & High-Performance Yacht Sector Expansion | +0.6% | North America, Europe, emerging in Southeast Asia | Short term (≤ 2 years) |

| Corrosion Resistance Advantage Over Steel in Saline Environments | +0.5% | Global, with highest relevance in tropical & offshore markets | Short term (≤ 2 years) |

IMO & Regional Emission Control Area Compliance Mandates

The progressive tightening of MARPOL Annex VI, including the global 0.50% sulfur cap enforced since January 2020 and the Mediterranean Sea ECA’s stricter 0.10% sulfur limit activated in May 2025, is structurally compelling shipowners to invest in vessel redesigns and newbuilds that incorporate composite superstructures, lightweight hull panels, and corrosion-resistant composite exhaust and scrubber housings.

Reducing vessel deadweight by switching from steel to glass- or carbon-fiber-reinforced composites on secondary structures can cut fuel consumption by 10–15% for comparable vessel types, directly improving compliance economics by lowering the volume of low-sulfur fuel (priced at a 20–35% premium over HSFO) required per voyage.

The FuelEU Maritime Regulation (EU 2023/1805) further mandates a -2% greenhouse gas intensity reduction from 2025, escalating to -6% by 2030 and -31% by 2040, creating a multi-decade capex cycle that rewards lighter, energy-efficient vessel construction with composite-intensive hull and topside retrofits becoming a commercially recurring revenue stream for composites fabricators serving European port operators and global container fleet owners.

Restraints

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Carbon Fiber vs. Conventional Marine Materials | -1.3% | Global, most acute in price-sensitive Asia Pacific & Latin America shipbuilding | Short term (≤ 2 years) |

| Absence of Harmonized Composite Repair & Certification Standards | -0.8% | Global, with regulatory fragmentation highest between IMO, USCG, and EU classification societies | Medium term (2–4 years) |

| Unsaturated Polyester & Epoxy Resin Feedstock Price Volatility | -0.7% | Global, with highest exposure in South & Southeast Asia fabrication markets | Short term (≤ 2 years) |

| Limited Access to Long-Term Project Finance for Composite Newbuilds | -0.6% | Emerging markets — India, Southeast Asia, Africa | Medium term (2–4 years) |

| EU Carbon Border Adjustment Mechanism Disrupting Import Cost Structures | -0.5% | Europe (import-facing), with knock-on exposure for Asian composite exporters | Short term (≤ 2 years) |

High Upfront Cost of Carbon Fiber vs. Conventional Marine Materials

Carbon fiber-reinforced polymer (CFRP) remains priced at approximately $20–35/kg for standard aerospace-tow grades and $12–18/kg for industrial large-tow variants, compared to structural steel at approximately $0.70–1.10/kg and marine-grade aluminum at $2.50–3.50/kg a cost differential of 10x–30x that places CFRP beyond the reach of mainstream commercial shipbuilding procurement budgets without a clearly defined total-cost-of-ownership (TCO) payback model.

Isophthalic unsaturated polyester resins, the dominant matrix for fiberglass marine hulls, are priced between $1,800–$2,400/MT globally, but volatile benzene and propylene feedstock costs, which swung by ±18–22% intra-year during 2023–2024 due to energy market disruptions, directly compress fabricator margins that are already thin at 8–12% for standard GRP hull construction.

Challenges

| Challenge | (~) % CAGR Friction Drag | Geographic Relevance | Mitigation Horizon |

|---|---|---|---|

| Thermoset End-of-Life Waste Bottleneck | -0.9% | Europe (regulatory frontline), global fabrication hubs | Long term (≥ 4 years) |

| Composites Skilled Technician Deficit | -0.7% | Global, most acute in North America, Australia, and emerging Asian markets | Medium term (2–4 years) |

| Carbon Fiber Supply Chain Concentration | -0.6% | Global, with single-source risk concentrated in Japan, USA, Germany | Medium term (2–4 years) |

| Complex Multi-Material Joint Fatigue Performance | -0.5% | Global, with highest incidence in offshore & naval structural applications | Long term (≥ 4 years) |

| Inconsistent Quality Control Across Fabricators | -0.4% | Asia Pacific, Middle East, Latin America | Medium term (2–4 years) |

Thermoset End-of-Life Waste Bottleneck

The marine composites industry is structurally exposed to an accelerating end-of-life (EoL) crisis: thermoset glass-reinforced plastic (GRP) and carbon-fiber-reinforced polymer hulls cannot be melted, remolded, or landfilled without regulatory consequence, yet as of 2025, a maximum of only 5% of the estimated 228,000 metric tonnes of accessible thermoset composite waste generated annually in Europe alone is being recycled against a broader theoretical waste pool estimated at over 683,000 tonnes per year including accumulated legacy stock.

For marine fabricators, the absence of a functioning secondary fiber market means decommissioned hulls represent a hidden liability of approximately €150–350 per tonne for mechanical grinding or pyrolysis-based thermal recovery, compressing end-of-life provisioning margins and deterring fleet operators in the workboat and leisure segments from specifying composite hulls for vessels with sub-20-year design lives.

Long-term, corporates will be required to internalize circular-design requirements, investing in recyclable thermoplastic matrix or vitrimer resin reformulations, which currently carry a 25–40% unit cost premium over standard epoxy systems to maintain market access in regulated European and North American procurement environments.

Opportunities

| Opportunity | (~) % Potential CAGR | Geographic Relevance | Execution Window |

|---|---|---|---|

| Electric & Autonomous Vessel Composite Adoption | +1.6% | Europe, North America, South Korea, Japan | Medium term (2–4 years) |

| Composite Retrofitting of Existing Merchant Fleet | +1.1% | Global, with highest near-term volume in Europe & East Asia | Short term (≤ 2 years) |

| Recycled & Bio-Based Composite Material Commercialization | +0.9% | Europe (regulatory pull), North America (voluntary ESG demand) | Long term (≥ 4 years) |

| Inland Waterway & Short-Sea Shipping Fleet Build-Out | +0.8% | Europe (FuelEU & Green Deal corridor mandates), India, Southeast Asia | Medium term (2–4 years) |

| Subsea & Deep-Water Composite Pressure Vessel Expansion | +0.7% | North Sea, Gulf of Mexico, Asia Pacific offshore oil & gas | Long term (≥ 4 years) |

Electric & Autonomous Vessel Composite Adoption

The electric ship segment is currently valued meaningfully below its long-run addressable potential and growing at a compound rate approaching 24–25% annually through the early 2030s represents a white space for marine composite suppliers that remains largely uncaptured because vessel electrification programs are still in early design and procurement phases rather than full serial build cycles.

The structural logic is compelling: every 100 kg of hull or superstructure weight eliminated via composite substitution extends the operational range of battery-electric vessels by an estimated 3–6% for a given battery pack a unit-economic improvement that directly reduces battery CapEx per nautical mile of range, which at current marine-grade lithium iron phosphate pricing of approximately $180–250/kWh creates a composite-for-steel substitution ROI of under 30 months on short-sea and ferry routes.

Autonomous vessel architectures further amplify this dynamic: reduced crew accommodation spaces lower structural steel requirements by an estimated 12–18% of total hull mass, with composite panels for sensor-housings, radar-transparent superstructures, and lightweight deck modules constituting an emerging product category that no incumbent has yet standardized or scaled.

India’s electric ship CAGR is projected at 30.8% through 2035, and Germany’s at 28.3%, with neither market having yet developed dedicated composite supply chains for next-generation electric hull forms, creating a first-mover margin capture opportunity of 15–22% gross margin premium for fabricators that qualify into vessel OEM supply agreements before the 2027–2028 serial production ramp of European and Indo-Pacific electric ferry programs.

Geopolitical Impact Analysis

Geopolitical Impact Analysis of the Global Marine Composites Market

Geopolitical shifts and global trade realignments are increasingly influencing the Global Marine Composites Market, particularly through supply chain disruptions, raw material dependency, and regional manufacturing strategies. The production of marine composites relies heavily on key inputs such as fiberglass, carbon fiber, and resin systems, many of which are concentrated in a few major manufacturing regions.

Rising trade barriers and industrial policies in major economies are encouraging companies to diversify their supply chains and reduce dependence on single-source regions. Countries in North America and Europe are actively promoting domestic production of advanced composites to strengthen industrial resilience and reduce import reliance.

At the same time, Asia-Pacific remains a dominant production hub due to its strong shipbuilding industry and cost-efficient manufacturing base, particularly in China, Japan, and South Korea. Additionally, fluctuations in energy prices and raw material exports from key producing nations influence overall production costs for marine composite manufacturers.

Regional Analysis

North America dominates the global marine composites market, accounting for a 33.7% share, driven by strong demand for high-performance marine vessels, luxury yachts, and advanced naval applications.

The region benefits from a well-established shipbuilding industry, high investment in defense and marine infrastructure, and increasing adoption of lightweight composite materials to improve fuel efficiency and durability. The presence of advanced manufacturing technologies and strong R&D capabilities further strengthens North America’s leading position in the market.

Europe shows strong growth due to its luxury yacht manufacturing and sustainable marine material adoption, while Asia Pacific is emerging as a key production hub driven by expanding shipbuilding activities in countries like China, India, and South Korea.

Key Regions and Countries Covered in this Report

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

The global marine composites market is highly competitive due to the presence of numerous regional and international players operating across the value chain. Manufacturers are continuously focusing on improving product performance while reducing weight and overall production costs to meet growing demand from the marine industry.

To strengthen their market position, companies are actively investing in research and development, advanced material technologies, strategic partnerships, and mergers and acquisitions. In addition, players are increasingly focusing on innovation in resin systems, fiber reinforcement technologies, and sustainable composite solutions to enhance durability, corrosion resistance, and fuel efficiency of marine structures.

Expansion into emerging markets and collaboration with shipbuilders and naval contractors are also key strategies being adopted. These combined efforts are expected to intensify competition while driving technological advancements and supporting long-term market growth in the global marine composites industry.

Major Players in the Industry

- 3M Company

- AOC

- BASF SE

- Gurit Holding AG

- Hexcel Corporation

- Hexion Inc

- Huntsman Corporation

- Mitsubishi Chemical Group Corporation

- Owens Corning

- Scott Bader Company Ltd

- SGL Carbon SE

- Solvay S.A.

- Teijin Limited

- Toray Industries, Inc.

- Other Key Players

Key Development

-

In February 2026, Gurit announced the expansion of its Dallas, Texas facility with a new building dedicated to Corecell structural foam core production to support growing U.S. subsea and marine demand, with the expanded site scheduled to be fully operational by Q3 2026.

-

In March 2026, Hexcel unveiled a suite of next-generation composite solutions including HexPly® M51 rapid-cure prepreg for high-rate press molding, HexTow® IM11-R carbon fiber, HexPly® M949 cosmetic prepreg, and HexShape® woven net-shape textiles for complex 3D geometries — product lines with direct applicability to high-performance marine and naval structures requiring optimized fiber architecture.

Report Scope

| Report Features | Description |

|---|---|

| Market Value (2025) | US$ 4.5Bn |

| Forecast Revenue (2035) | US$ 7.1Bn |

| CAGR (2026-2035) | 5.4% |

| Base Year for Estimation | 2025 |

| Historic Period | 2020-2024 |

| Forecast Period | 2026-2035 |

| Report Coverage | Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered | By Composites (Ceramic Matrix Composites, Metal Matrix Composites, Polymer Matrix Composites, Polymer Matrix Composites), By Resin Type (Epoxy, Polyester, Vinyl Ester, Others), By Application (Power Boats, Sailboats & Yachts, Commercial & Workboats, Cruise ships & Large Passenger Vessels, Offshore & Marine Structures, Others) |

| Regional Analysis | North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC- China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America- Brazil, Mexico & Rest of Latin America; Middle East & Africa- GCC, South Africa, & Rest of MEA |

| Competitive Landscape | 3M Company, AOC, BASF SE, Gurit Holding AG, Hexcel Corporation, Hexion Inc, Huntsman Corporation, Mitsubishi Chemical Group Corporation, Owens Corning, Scott Bader Company Ltd, SGL Carbon SE, Solvay S.A., Teijin Limited, Toray Industries, Inc., Other Key Players |

| Customization Scope | Customization for segments and region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Purchase Options | We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |