Global Loose Leaf Tea Market Size, Share Analysis Report By Type (Black Tea, Green Tea, Oolong Tea, White Tea, Herbal And Specialty Tea), By Category (Conventional Loose Leaf Tea, Organic Loose Leaf Tea), By Distribution Channel (Supermarkets And Hypermarkets, Specialty Stores, Online Retail/E-Commerce, Convenience Stores, Others) , By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2034

- Published date: Oct 2025

- Report ID: 162706

- Number of Pages: 256

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

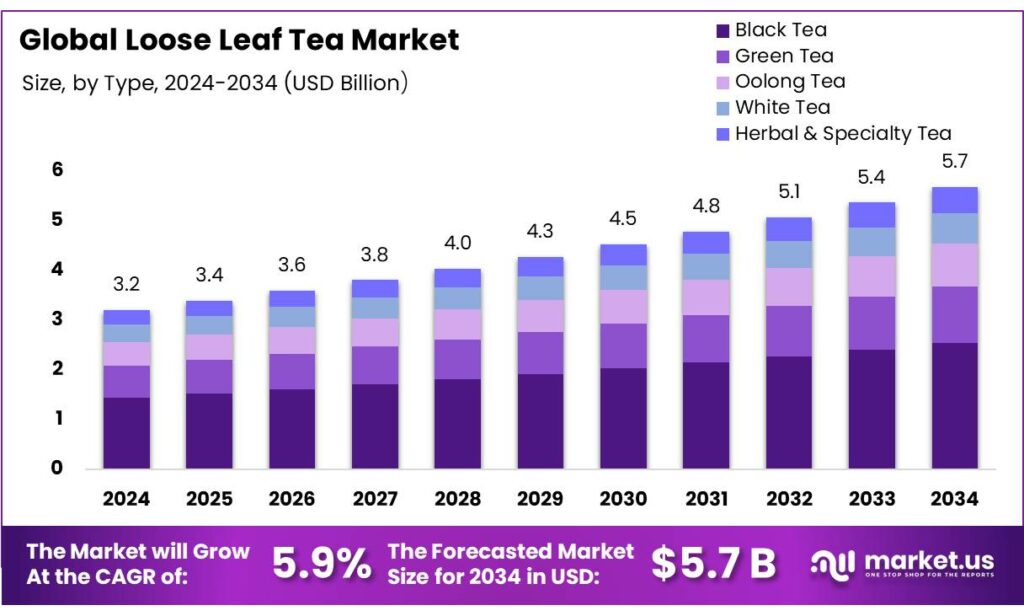

The Global Loose Leaf Tea Market size is expected to be worth around USD 5.7 Billion by 2034, from USD 3.2 Billion in 2024, growing at a CAGR of 5.9% during the forecast period from 2025 to 2034. In 2024 Asia-Pacific held a dominant market position, capturing more than a 44.8% share, holding USD 1.4 Billion in revenue.

Loose leaf tea sits at the premium end of the global tea value chain, supported by specialty formats, single-origin positioning, and at-home brewing equipment. After pandemic volatility, fundamentals have stabilized: FAO notes global tea consumption expanded 2.0% in 2022 versus 2021 as import demand recovered, while output increased on the strength of green and “other” teas offsetting weaker black tea in Sri Lanka. Importantly for loose leaf players, the market is largely domestic: only ~26% of world tea was exported in 2023, meaning three-quarters was consumed at origin—conditions that favor premium in-market loose leaf trade and origin branding.

The industrial picture in leading producers underscores tightening supply and firm pricing that benefit higher-margin loose leaf. India’s tea production fell 7.8% in 2024 to 1,284.78 million kg, with weather disruptions in Assam, lifting average auction prices ~18% to ₹198.76/kg; constrained bulk supply tends to channel consumer trade-ups into orthodox and loose leaf lines.

- Exports also improved: India’s tea shipments rose 9.92% to 254.67 million kg in 2024, helped by higher output in South India and resilient demand in West Asia and the CIS, supporting orthodox/loose-leaf flows. On the demand side, downstream markets are broadening: in South Korea, tea import value reached US$67 million in 2024, reflecting café culture and at-home brewing momentum that skews toward higher-quality leaf.

Energy is a non-trivial cost driver across withering, rolling, and drying lines, and credible energy metrics shape investment cases. REN21 estimates agriculture and forestry account for ~2.1% of world total final energy use (2021) and, together with fisheries/aquaculture, ~15% of energy use across the food value chain—context for tea processors pursuing energy-efficiency retrofits and renewables PPA strategies to protect margins. Electrification readiness is rising: IEA reports electricity comprised 19.7% of world total final energy consumption (2019), underscoring grid-based pathways for electric dryers and heat-pump integration as utilities decarbonize.

Policy support is material. India’s Tea Development & Promotion Scheme (TDPS) has been re-notified for 2024–25/2025–26 with active application lists and scheme documents on Tea Board’s official site, signalling funding lines for replanting, quality, and market promotion that benefit orthodox/loose-leaf segments.

- Complementing this, the Ministry of Power launched ADEETIE in July 2025—a ₹1,000 crore program implemented by the Bureau of Energy Efficiency to accelerate MSME energy-efficiency upgrades, offering 5% interest subvention for Micro/Small and 3% for Medium enterprises on EE loans; the rollout targets 60 industrial clusters across 14 sectors, relevant to tea factories and suppliers.

Key Takeaways

- Loose Leaf Tea Market size is expected to be worth around USD 5.7 Billion by 2034, from USD 3.2 Billion in 2024, growing at a CAGR of 5.9%.

- Black Tea held a dominant market position, capturing more than a 44.8% share in the global loose leaf tea market.

- Conventional Loose Leaf Tea held a dominant market position, capturing more than a 76.4% share of the global loose leaf tea market.

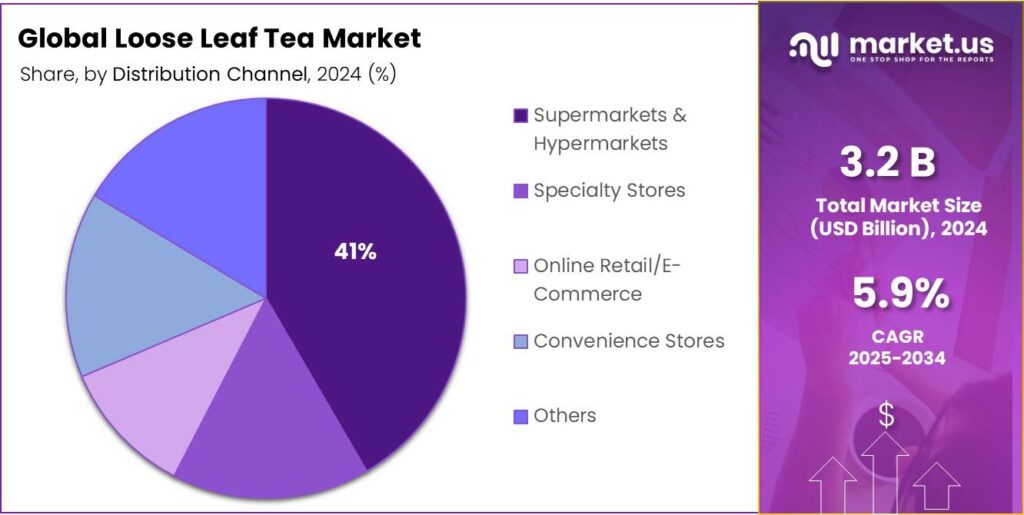

- Supermarkets & Hypermarkets held a dominant market position, capturing more than a 41.6% share in the global loose leaf tea market.

- Asia-Pacific region held a dominant position in the loose leaf tea market, capturing 44.8% of the market and amounting to approximately USD 1.4 billion.

By Type Analysis

Black Tea dominates with 44.8% share due to its strong global consumption base and rich flavor profile

In 2024, Black Tea held a dominant market position, capturing more than a 44.8% share in the global loose leaf tea market. The segment’s leadership can be attributed to its widespread consumer acceptance, strong cultural roots, and extensive availability across both traditional and modern retail channels. Black tea continues to be the most consumed type of loose leaf tea worldwide, supported by its deep flavor, longer shelf life, and perceived health benefits such as improved heart health and antioxidant properties.

In 2025, the demand for black loose leaf tea is expected to remain steady, driven by rising consumption in major tea-producing countries like India, China, and Sri Lanka, as well as increasing exports to Europe and North America. The preference for authentic, single-origin teas and the growth of premium tea cafés have further supported market expansion. Moreover, innovations in packaging and flavor variants, such as Earl Grey and Darjeeling blends, have helped attract younger consumers seeking both quality and variety.

By Category Analysis

Conventional Loose Leaf Tea dominates with 76.4% share owing to its affordability and strong consumer preference

In 2024, Conventional Loose Leaf Tea held a dominant market position, capturing more than a 76.4% share of the global loose leaf tea market. This dominance is largely due to its widespread availability, lower price point, and long-standing consumer trust in conventional cultivation and processing methods. Conventional tea remains the most accessible option for mass consumers, particularly in developing nations where price sensitivity remains a key factor influencing purchase behavior.

The segment is projected to sustain its lead as tea consumption continues to expand across Asia-Pacific and Africa. The consistent yield of conventionally grown tea and its compatibility with existing large-scale production systems contribute to its stable supply chain. Traditional tea estates, especially in India, China, and Kenya, continue to rely on conventional farming methods, which ensure consistent quality and output to meet global demand.

By Distribution Channel Analysis

Supermarkets & Hypermarkets dominate with 41.6% share due to strong product visibility and consumer convenience

In 2024, Supermarkets & Hypermarkets held a dominant market position, capturing more than a 41.6% share in the global loose leaf tea market. This dominance is attributed to the extensive product availability, organized retail structure, and the growing preference of consumers for one-stop shopping experiences. These large retail chains provide a wide range of loose leaf tea varieties, including premium, flavored, and specialty teas, offering consumers the opportunity to compare quality and prices before purchasing.

Supermarkets and hypermarkets are expected to maintain their leadership position as global retail infrastructure continues to expand, particularly in emerging economies across Asia-Pacific and the Middle East. The improved shelf visibility and promotional activities, such as discounts and sampling campaigns, have further enhanced consumer engagement. Moreover, partnerships between tea producers and modern retail outlets are enabling better placement and branding, contributing to the sustained growth of this distribution channel.

Key Market Segments

By Type

- Black Tea

- Green Tea

- Oolong Tea

- White Tea

- Herbal & Specialty Tea

By Category

- Conventional Loose Leaf Tea

- Organic Loose Leaf Tea

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Stores

- Online Retail/E-Commerce

- Convenience Stores

- Others

Emerging Trends

Sustainability-first, origin-transparent loose-leaf tea

A clear, fast-maturing trend in loose-leaf tea is the shift toward sustainability verification and origin transparency—from farm practices and factory energy to worker welfare—used as a premium signal on packs and in online listings. The scale of tea makes this trend meaningful, not niche: the Food and Agriculture Organization reports world tea production reached 6.8 million tonnes in 2023, with imports at 1.8 million tonnes—ample volume where certified, traceable lots can now stand out on quality and ethics.

Certification footprints underscore how mainstream this has become. The Rainforest Alliance indicates its tea program spans ~1.5 million hectares and ~2.5 million farmers and workers across 22 countries (2023)—a sizeable share of global supply now operating against auditable standards on biodiversity, pesticide use and social safeguards.

Energy decarbonization at origin is another pillar of this trend, directly relevant to leaf integrity. Kenya Tea Development Agency (KTDA) has invested billions of Kenyan shillings in small hydropower plants to cut factory electricity costs and stabilize withering/drying conditions—both critical to protecting whole-leaf quality. A representative KTDA note details commissioning of multiple small hydro schemes financed at KSh 4.8 billion, aimed at lowering operating costs and emissions intensity for factories supplying premium grades.

Public sector data and governance signals reinforce this trajectory. The Tea Board of India’s official statistics document All-India production at 1,382.03 million kg in 2023–24, giving exporters and domestic premium brands a reliable baseline to segment certified, origin-specific orthodox leaf for higher-value loose-leaf SKUs. FAO’s commodity outlook further notes tea’s ~USD 17 billion production value and ~USD 9–9.5 billion trade value, quantifying why governments and value-chain platforms are steering finance and policy toward sustainable upgrading rather than pure volume growth.

Drivers

Health-Driven Demand for Loose Leaf Tea

One of the major driving factors behind the growth of the loose leaf tea segment is the growing awareness of health and wellness among consumers, which is strongly influencing purchase decisions and product preferences. Over recent years, research from trusted nutritional and health-science organisations has highlighted that tea consumption is linked with measurable health benefits. For example, observational evidence indicates that drinking two or more cups of true tea per day is associated with a 9% to 13% lower risk of death from any cause compared with non-tea drinkers.

Beyond simply living longer, some studies show that consuming approximately three cups per day (or about 6–8 g of tea leaves daily) may be associated with anti-ageing effects, including slower biomarkers of biological ageing. These data points resonate well with consumers who are increasingly treating tea not just as a daily habit but as part of a broader wellness regimen. As a result, premium formats—such as loose leaf tea—are benefiting from this shift: they are perceived to offer higher quality, more authentic leaf forms, and richer flavour profiles compared with mass-market tea bags.

In practical terms, this means that brands and retailers are now able to position loose leaf tea as a “health-and-lifestyle” product, leveraging the scientific links to cardiovascular health, metabolic wellness and longevity. For instance, the Harvard T.H. Chan School of Public Health Nutrition Source notes that regular tea consumption of 2-3 cups daily is associated with lower risks of premature death, heart disease, stroke and type 2 diabetes. Likewise, the Academy of Nutrition and Dietetics emphasises that true teas (caffeinated and herbal) provide polyphenols and antioxidants that help reduce risk of certain chronic diseases.

From the supply side, this health-driven demand encourages tea producers and processors to upgrade leaf quality , emphasise origin, craftsmanship and minimal processing, and adopt certifications (organic, fair trade) that further reinforce wellness narratives. Government agencies and industry bodies are supporting these efforts as well: for example, the Tea Board of India publishes annual statistics and conducts outreach around quality-assurance, nutritional messaging and export development.

Restraints

Climate volatility is squeezing loose-leaf tea supply

Loose-leaf tea relies on unbroken, high-grade leaves, which are the first casualty when weather turns extreme. The baseline is large: global tea output reached 6.8 million tonnes in 2023, underpinning livelihoods across Asia and Africa; when climate shocks hit, availability and quality tighten quickly. The World Meteorological Organization reports that 2024 was the warmest year on record in Asia, with heatwaves spreading across vast areas; the region’s warming trend since 1991 is nearly double that of 1961–1990. This accelerates heat and rainfall extremes that damage leaf flush, shorten picking windows, and increase pest pressure—outcomes that disproportionately reduce orthodox, loose-leaf grades.

We saw this play out in India, one of the world’s largest producers. During the 2024 peak season, May production fell by over 30% year-on-year amid heatwaves, and national output was projected to drop by ~100 million kg from 2023’s 1.394 billion kg. Prices reacted: average auction prices rose nearly 20% in June 2024, reflecting tight supply. For loose-leaf buyers, that means fewer premium lots and higher procurement costs, with quality variability that complicates blending and brand consistency.

Governments and sector bodies are responding, but adaptation takes time. India’s National Disaster Management Authority issued updated Heat-Wave 2024 guidance to strengthen early warnings and local action plans, aiming to reduce losses of life and productivity during extreme heat events that also disrupt agricultural labor and logistics. At the multilateral level, FAO continues to foreground tea in food-system resilience discussions; its most recent update confirms the sector’s scale—6.8 million tonnes of output and 1.8 million tonnes of imports in 2023—illustrating why climate adaptation in tea is a priority for producer economies.

Opportunity

Rising Domestic Consumption in Producing Countries

One major growth opportunity for loose-leaf tea stems from the rising domestic consumption within major tea-producing countries. According to the Food and Agriculture Organization (FAO), global tea consumption grew by 2.0% in 2022 compared to 2021, underscoring steadily increasing demand at the national level. In particular, China consumed around 3 million tonnes of tea in 2022, which represented approximately 46 % of the world’s total consumption. India, the second-largest consumer, used around 1.16 million tonnes, or about 18 % of global consumption in the same period.

In many producing nations, government and industry bodies recognise this potential. For instance, national tea boards and ministries are developing programmes to upgrade processing infrastructure, promote origin branding, and enhance domestic consumption. These actions create a favourable policy backdrop for loose-leaf tea. Because the product format involves higher leaf quality, minimal mechanical processing (compared to dust/fannings), and premium packaging, it stands to benefit disproportionately when domestic markets upgrade.

For tea brands and suppliers, the opportunity lies in integrating these demand patterns with supply chain advantages. Since output volumes in many producing countries remain solid—the FAO estimates production reached around 6.7 million tonnes in 2022 globally. —there is headroom to shift part of that output into premium loose-leaf formats rather than lower-grade bulk blends destined purely for export. Moreover, local consumers often value origin stories, sustainability credentials and authenticity—attributes well-aligned with loose-leaf positioning.

Regional Insights

Asia-Pacific dominates with 44.8% share (USD 1.4 billion) as the principal production and consumption hub

In 2024, the Asia-Pacific region held a dominant position in the loose leaf tea market, capturing 44.8% of the market and amounting to approximately USD 1.4 billion; this leadership is grounded in very large domestic consumption, concentrated production capacities and expanding modern retail and e-commerce channels.

Large producers such as China and India continue to account for the majority of global tea output — global tea production was about 6.7 million tonnes, with Asia supplying nearly 80% of that total, which underpins local availability and export scale.

Structural drivers include strong cultural consumption habits, rising urban middle-class demand for premium and specialty loose leaves, and the growth of café and ready-to-brew occasions that lift per-unit value capture. Market dynamics in 2024 were also shaped by production shocks in key origins — for example India experienced a 7.8% decline in 2024 tea output, which tightened supply and supported price increases in auction and export channels.

Key Regions and Countries Insights

- North America

- US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Ahmad Tea: Established in the UK by a family tea-trader, Ahmad Tea has become a global brand available in over 80 countries, bringing more than 30 million cups of tea daily to consumers worldwide. The company emphasises luxury blending, strict sourcing of top 1% tea leaves, and premium packaging in its mission “to inspire the love of tea.” Ahmad Tea’s strong export orientation and quality focus make it a notable competitor in the loose-leaf market.

Bigelow Tea Company: Founded in 1945 and still 100% family-owned and based in Connecticut, Bigelow is a leading U.S. manufacturer of teas (black, green, herbal) and is recognised for its flagship “Constant Comment” blend. The company produces over 150 varieties, emphasises sustainability (Certified B Corp status) and has built a strong specialty-tea presence across retail channels. Its longevity and diversified product base offer stability in the loose-leaf market.

Dilmah Ceylon Tea Company PLC: Founded in Sri Lanka in 1985 by Merrill J. Fernando, Dilmah was the first truly vertically integrated, producer-owned brand offering “picked, perfected and packed” single-origin Ceylon tea. The firm’s global distribution spans more than 100 countries and the company underscores ethical practices, sustainability and premium Ceylon tea quality. Its heritage and control of the value chain position it strongly in the global loose-leaf tea premium arena.

Top Key Players Outlook

- Adagio Teas

- Ahmad Tea

- Bigelow Tea Company

- Choice Organic Teas

- DAVIDsTEA

- Dilmah Tea

- Harney & Sons

- Kusmi Tea

- Mighty Leaf Tea

- Numi Organic Tea

- T2 Tea

Recent Industry Developments

In 2024, Adagio Teas reported annual revenues of approximately USD 7.5 million, supported by a dedicated team of 61 employees across four continents.

In 2024, Ahmad Tea achieved an estimated annual revenue of approximately USD 40.7 million and maintained operations in over 80 countries, serving more than 30 million cups of tea daily.

In 2024, Choice Organic Teas reported annual revenues in the range of USD 1 – 10 million, with a small but dedicated workforce of approximately 30 employees prior to its acquisition by East West Tea Company in 2019.

Report Scope

Report Features Description Market Value (2024) USD 3.2 Bn Forecast Revenue (2034) USD 5.7 Bn CAGR (2025-2034) 5.9% Base Year for Estimation 2024 Historic Period 2020-2023 Forecast Period 2025-2034 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Type (Black Tea, Green Tea, Oolong Tea, White Tea, Herbal And Specialty Tea), By Category (Conventional Loose Leaf Tea, Organic Loose Leaf Tea), By Distribution Channel (Supermarkets And Hypermarkets, Specialty Stores, Online Retail/E-Commerce, Convenience Stores, Others) Regional Analysis North America – US, Canada; Europe – Germany, France, The UK, Spain, Italy, Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, Singapore, Rest of APAC; Latin America – Brazil, Mexico, Rest of Latin America; Middle East & Africa – GCC, South Africa, Rest of MEA Competitive Landscape Adagio Teas, Ahmad Tea, Bigelow Tea Company, Choice Organic Teas, DAVIDsTEA, Dilmah Tea, Harney & Sons, Kusmi Tea, Mighty Leaf Tea, Numi Organic Tea, T2 Tea Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF)

-

-

- Adagio Teas

- Ahmad Tea

- Bigelow Tea Company

- Choice Organic Teas

- DAVIDsTEA

- Dilmah Tea

- Harney & Sons

- Kusmi Tea

- Mighty Leaf Tea

- Numi Organic Tea

- T2 Tea

Our Clients

- 162706

- Oct 2025