Global Living Soil Market By Application (Agriculture, Horticulture And Nurseries, Home And Urban Gardening, Controlled Environment Agriculture, Landscaping And Turf, and Others), By End-Use (Commercial Farmers, Professional Landscapers, Retail/Home Gardeners, Urban Farms, and Others), By Region and Companies - Industry Segment Outlook, Market Assessment, Competition Scenario, Trends and Forecast 2025-2035

- Published date: Mar 2026

- Report ID: 181084

- Number of Pages: 224

- Format:

-

keyboard_arrow_up

Quick Navigation

Report Overview

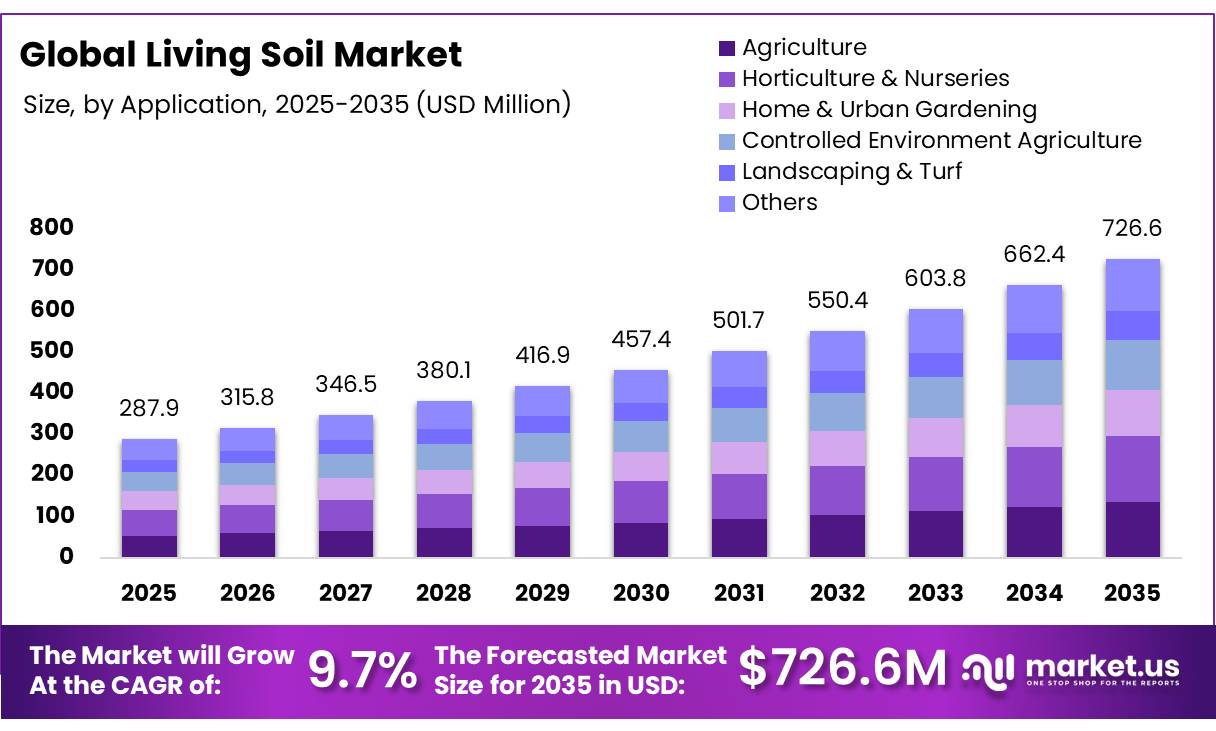

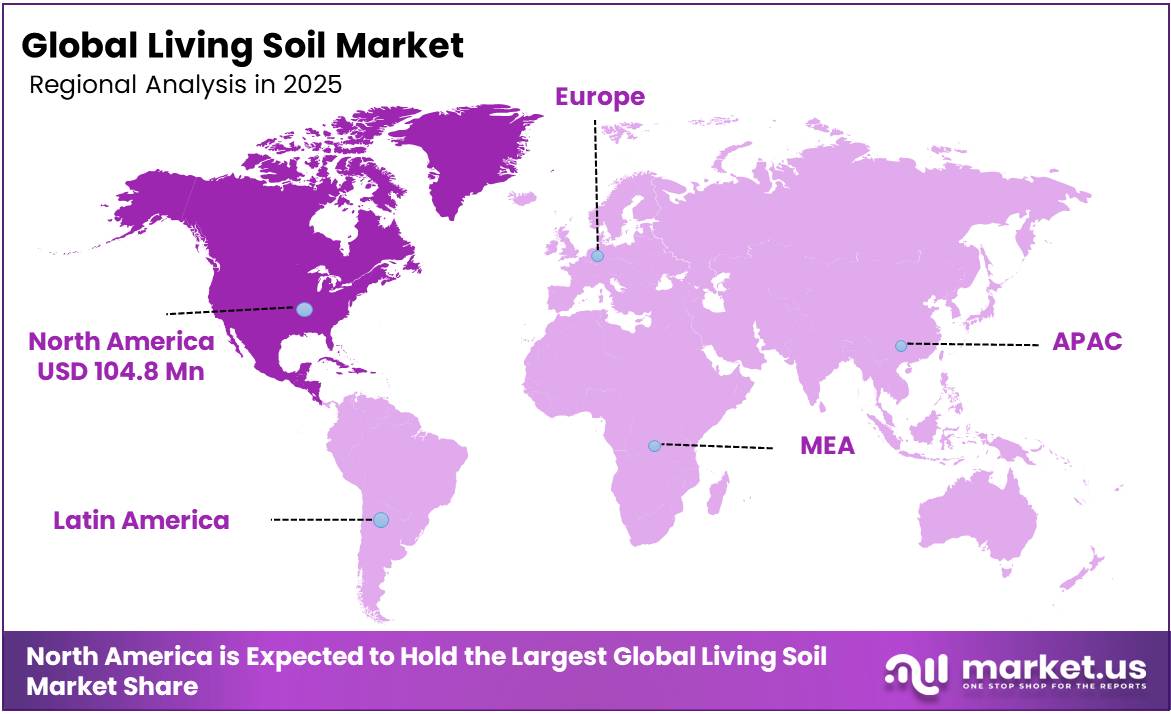

The Global Living Soil Market size is expected to be worth around USD 726.6 Million by 2035, from USD 287.9 Million in 2025, growing at a CAGR of 9.7% during the forecast period from 2026 to 2035. In 2025, North America held a dominant market position, capturing more than a 36.4% share, holding USD 104.8 Million revenue.

Living soil is a biologically active growing medium that functions as a self-sustaining ecosystem. Unlike sterile potting mixes that rely on synthetic liquid fertilizers, living soil contains a diverse community of beneficial microorganisms, such as bacteria, fungi, protozoa, and nematodes, and larger organisms such as earthworms. These organisms work together to break down organic matter into nutrients that plants can easily absorb, essentially feeding the soil to let the soil feed the plant.

The living soil market centers on biologically active soils, microbial inoculants, and compost-based amendments that enhance soil fertility, structure, and microbial diversity. Demand is driven by the expansion of organic and high-value crops, regenerative agriculture initiatives, and the rise of controlled environment agriculture (CEA), where root-zone microbiology is critical for nutrient cycling and plant health. North America represents a leading region, supported by extensive organic farmland, soil-health programs, and widespread compost application.

However, adoption faces economic, technical, and operational constraints. Smallholder affordability, variable microbial efficacy, short shelf life, and limited extension services restrict large-scale deployment in conventional agriculture, professional landscaping, and urban farms. Conversely, home and urban gardeners dominate usage due to manageable application conditions, small-scale control, and a focus on chemical-free, regenerative practices. Living soil’s relevance is amplified in systems emphasizing soil restoration, carbon sequestration, and sustainable horticulture, positioning it as a critical input in biologically driven farming and urban gardening systems.

Key Takeaways:

- The global living soil market was valued at USD 287.9 million in 2025.

- The global living soil market is projected to grow at a CAGR of 9.7% and is estimated to reach USD 726.6 million by 2035.

- Based on the applications of living soil, home & urban gardening dominated the living soil market, with a market share of around 34.6%.

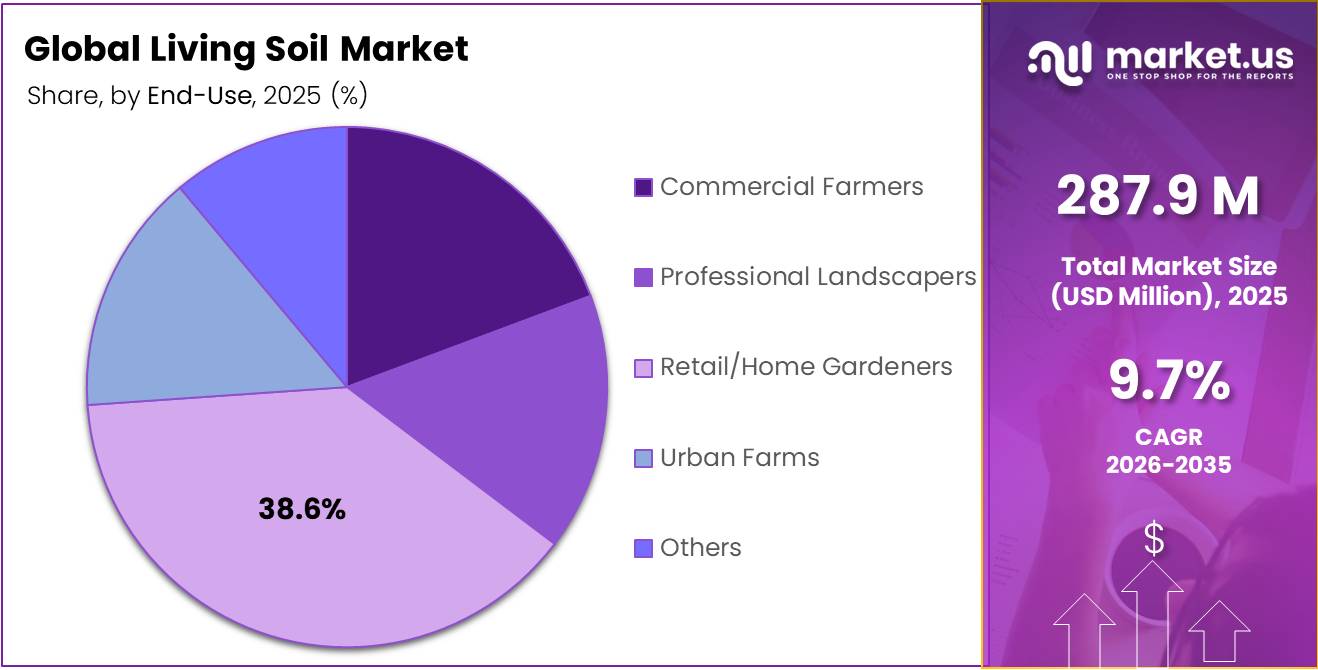

- Among the end-uses of living soil, retail/home gardeners held a major share in the market, 38.6% of the market share.

- In 2025, North America was the most dominant region in the living soil market, accounting for around 36.4% of the total global consumption.

Application Analysis

Home & Urban Gardening Held the Largest Share in the Living Soil Market.

The living soil market is segmented based on application into agriculture, horticulture & nurseries, home & urban gardening, controlled environment agriculture, landscaping & turf, and others. The home & urban gardening dominated the living soil market, comprising around 34.6% of the market share, as the application conditions are better suited to biologically active soil systems than large-scale agricultural operations. Living soil typically contains compost, organic matter, and diverse microorganisms that require stable moisture, limited disturbance, and controlled nutrient inputs to maintain microbial activity. Home gardens and container systems generally provide these conditions through small-scale management, manual watering, and minimal tillage.

In contrast, field agriculture often relies on mechanized cultivation, synthetic fertilizers, and large input volumes, which can disrupt microbial balance and make the large-scale handling of biologically active soils operationally complex. Additionally, transporting and applying compost-rich soil blends across extensive farmland is logistically challenging compared with concentrated fertilizers. However, urban gardeners frequently prioritize soil health, chemical-free cultivation, and small container or raised-bed systems, where living soil can be applied directly and reused across planting cycles, making it more practical and effective in these environments.

End-Use Analysis

Living Soil is Mostly Utilized by Retail/Home Gardeners.

Based on the end-uses of living soil, the market is divided into commercial farmers, professional landscapers, retail/home gardeners, urban farms, and others. The retail/home gardeners dominated the living soil market, with a market share of 38.6%, as its characteristics align closely with small-scale, high-control growing environments. Living soil relies on active microbial populations and organic matter, which require careful moisture management, minimal mechanical disturbance, and stable nutrient conditions that are more easily maintained in home gardens, raised beds, and container planting.

Commercial farmers and large-scale urban farms often employ mechanized equipment, high-volume irrigation, and synthetic fertilizers, which can disrupt microbial activity and reduce the efficacy of living soil. Similarly, professional landscapers and turf managers prioritize uniformity, fast establishment, and maintenance efficiency, favoring traditional soils or pre-fertilized blends over biologically active soils.

Additionally, retail gardeners value the chemical-free, regenerative qualities of living soil, enabling repeated planting cycles and crop-specific amendments, making it particularly suited to small-scale, high-care horticultural applications.

Key Market Segments:

By Application

- Agriculture

- Horticulture & Nurseries

- Home & Urban Gardening

- Controlled Environment Agriculture

- Landscaping & Turf

- Others

By End-Use

- Commercial Farmers

- Professional Landscapers

- Retail/Home Gardeners

- Urban Farms

- Others

Drivers

Growth in Organic and High-Value Crops Drives the Living Soil Market.

The proliferation of organic and high-value crops (HVCs) serves as a primary driver for the living soil market, underpinned by regulatory shifts and consumer demand for residue-free produce. According to the USDA Economic Research Service, certified organic cropland in the U.S. increased by 79% to 3.6 million acres between 2011 and 2021, while certified operations grew by over 90% to 17,445 farms.

The USDA data indicates that organic systems, despite yielding 10-18% less than conventional counterparts, achieve 22-35% higher profitability due to market premiums. This economic advantage incentivizes the adoption of biological soil management to maintain certification. In emerging markets such as India, transition strategies for sustainable production suggest that increasing high-value crops, such as fruits, vegetables, and legumes, can raise farmer income.

Moreover, high-value crop systems are prominent in organic production due to higher margins and export demand. These crops are nutrient-intensive and sensitive to soil biological activity, increasing reliance on composts, biofertilizers, and microbial consortia that enhance soil organic matter and nutrient cycling. As certified acreage and horticultural diversification expand across major agricultural regions, soil-biological input demand grows in parallel with the agronomic requirements of organic and high-value cropping systems.

Restraints

Economic & Operational Challenges Might Hamper the Demand for Living Soil.

Economic, technical, and operational constraints limit the adoption of living-soil inputs such as microbial biofertilizers and compost-based inoculants. High initial investment and transition risks are the primary deterrents. According to the USDA Economic Research Service, the mandatory three-year organic transition period often results in lower yields and revenue without the benefit of price premiums. Input costs for biological amendments, such as biofertilizers and organic seeds, can exceed those of traditional counterparts.

Similarly, managing Biological Soil Amendments of Animal Origin (BSAAOs) introduces food safety risks. The FDA Produce Safety Rule mandates strict treatment standards to mitigate pathogens such as Salmonella, posing a technical compliance burden for producers. Furthermore, nutrient availability in organic amendments is less predictable than that of synthetic fertilizers due to complex mineralization processes.

Furthermore, living soil systems require intensive management. Key operational issues include increased weed pressure, consistently cited as the top agronomic challenge in organic farming, and the need for specialized infrastructure such as cold storage or on-site processing for biological inputs. Inadequate training, storage infrastructure, and distribution logistics can reduce product viability and field performance, slowing adoption of living-soil inputs.

Opportunity

Shift Toward Regenerative Agriculture Creates Opportunities in the Living Soil Market.

The shift toward regenerative agriculture is creating structural demand for living soil inputs, including microbial biofertilizers, compost inoculants, and soil-biological amendments that restore soil organic matter and microbial activity. Regenerative systems emphasize practices such as cover cropping, reduced tillage, and crop diversification that rely on active soil microbiology for nutrient cycling and carbon stabilization.

A study by the Food and Agriculture Organization of the United Nations indicates that regenerative and diversified cropping systems can increase soil organic carbon by about 0.2-1% annually, depending on local conditions and management intensity. Additionally, the adoption of regenerative farming helps in land restoration and climate mitigation initiatives. Global agriculture occupies roughly 4.9 billion hectares of land, creating a large base for soil-regeneration practices that depend on biological soil processes.

In India alone, soil degradation affects approximately 147 million hectares, encouraging policy and farm-level adoption of regenerative practices to restore soil fertility and productivity. As regenerative agriculture expands through conservation agriculture, agroforestry, and integrated livestock systems, demand rises for living soil products that enhance microbial biomass, stabilize soil carbon, and sustain long-term soil health within biologically driven farming systems.

Trends

Rise in Controlled Environment Agriculture (CEA).

The expansion of controlled environment agriculture (CEA), including greenhouses, vertical farms, and indoor plant factories, is shaping input demand patterns in the living soil market by intensifying interest in biologically active substrates and microbial amendments used in container-based or hybrid soil systems.

Globally, protected cultivation has expanded substantially. The estimates indicate about 1.3 million hectares of greenhouse cultivation worldwide, with China alone accounting for over 60% of greenhouse horticulture. These CEA systems emphasize high productivity and precise nutrient management. Greenhouse crop yields can substantially exceed typical open-field yields.

The expansion of controlled environment agriculture (CEA), including greenhouses, vertical farms, and protected cultivation systems, is influencing input requirements in the living soil market by increasing demand for biologically active substrates and microbial soil amendments used in intensive root-zone management. The protected cultivation covers more than 5 million hectares globally, with rapid expansion in Asia, where greenhouse vegetable production dominates intensive horticulture systems. Such systems depend on optimized root microbiomes to maintain nutrient cycling and plant resilience under high planting densities.

CEA systems typically involve repeated cropping cycles and confined root zones, which can reduce natural soil biodiversity. Consequently, growers increasingly use microbial inoculants, compost-derived media, and biologically active soil blends to stabilize plant-microbe interactions and maintain soil-like ecological functions within controlled production environments.

Geopolitical Impact Analysis

Global Fertilizer Supply Chains Disruption Is Impacting the Living Soil Market Amidst Geopolitical Tensions.

The geopolitical tensions affecting fertilizer supply chains are indirectly shaping the living soil market by altering input availability, production costs, and policy priorities toward soil-biological alternatives. The disruption is most evident in the mineral fertilizer trade. According to the United States Department of Agriculture Economic Research Service, Russia and Belarus together accounted for nearly 20% of global fertilizer exports and about 40% of global potash exports in 2020, making global agriculture highly sensitive to supply interruptions from the region.

The United States Department of Agriculture Foreign Agricultural Service reported that export restrictions and uncertainty following the Russia-Ukraine conflict temporarily removed roughly 15% of global fertilizer supply from trade flows in 2022, contributing to price spikes and procurement uncertainty for importing countries. Similarly, the geopolitical risks in energy-producing regions further affect nitrogen fertilizer production as natural gas can represent most of the nitrogen fertilizer production costs, amplifying supply vulnerability during energy disruptions.

These supply shocks have encouraged governments and agricultural programs to prioritize soil-health strategies that reduce dependence on imported synthetic fertilizers. Living soil inputs, such as microbial inoculants, compost-based amendments, and biologically active soil conditioners, are increasingly incorporated into nutrient-management frameworks to stabilize soil fertility and buffer farms against geopolitical volatility in conventional fertilizer markets.

Regional Analysis

North America Held the Largest Share of the Global Living Soil Market.

In 2025, North America dominated the global living soil market, holding about 36.4% of the total global consumption, due to extensive organic agriculture, established soil-health programs, and large-scale adoption of biological soil management practices. According to the United States Department of Agriculture, the organic farmlands in the region have grown significantly. Organic systems often rely on compost, microbial inoculants, and biologically active soil amendments to maintain nutrient cycling and soil fertility in the absence of synthetic fertilizers.

In addition, soil-health initiatives further reinforce demand for living soil inputs. The Natural Resources Conservation Service administers conservation programs promoting practices such as cover cropping, reduced tillage, and organic matter restoration. These institutional programs and large-scale soil-health practices support widespread integration of living soil inputs across North American agriculture.

Key Regions and Countries

- North America

- The US

- Canada

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Russia & CIS

- Rest of Europe

- APAC

- China

- Japan

- South Korea

- India

- ASEAN

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Key Players Analysis

Manufacturers of living soil products focus on several strategic activities, such as product innovation, including the development of microbial consortia, compost-based soil blends, and bio-inoculants tailored to specific crops, soil types, or controlled-environment systems. In addition, companies invest in research collaborations with universities and agricultural institutes to validate microbial efficacy, improve shelf life, and demonstrate agronomic benefits through field trials.

Furthermore, vertical integration in composting and raw-material sourcing, enabling greater control over organic feedstocks and microbial quality, is focused. Similarly, firms frequently pursue certifications and regulatory compliance, such as organic input approvals, to access organic and regenerative agriculture markets.

In addition, partnerships with greenhouse operators, organic farms, and agricultural distributors expand market reach and application knowledge. Operationally, manufacturers emphasize farmer training, soil testing services, and digital agronomy tools to guide correct application and strengthen long-term customer adoption of biologically active soil systems.

The Major Players in The Industry

- BuildASoil

- KiS Organics

- Redbud Soil

- FoxFarm Soil & Fertilizer Co

- soilsunrise

- Dirtcraft Living Soils

- APSU Soil

- Organic Matters Soil

- Terra Preta

- SoilBiotics

- ProGro BIO

- LiveSoil

- Other Key Players

Key Development:

- In January 2026, ProGro BIO launched two new microbial products, Rhizol JumpStart and Phoenix. These products are developed to support nitrogen fixation in peanut crops and to promote the recovery of soil biology. Rhizol JumpStart is a dry Bradyrhizobium inoculant specifically designed for peanut growers, while Phoenix is intended to restore soil biological health following intensive or disruptive agricultural practices.

- In February 2026, LiveSoil announced the launch of its proprietary microbe-rich living soil, developed after more than twelve years of research, development, field trials, and evaluation. Independent analysis by the Cornell University soil laboratory confirmed that LiveSoil requires up to 60% less water than conventional soil.

Report Scope

Report Features Description Market Value (2025) US$287.9 Mn Forecast Revenue (2035) US$726.6 Mn CAGR (2025-2035) 9.7% Base Year for Estimation 2025 Historic Period 2021-2024 Forecast Period 2025-2035 Report Coverage Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments Segments Covered By Application (Beverage Packaging Recycling, Food Packaging Recycling, PET Textile & Fiber Recycling, PET Film & Sheet Recycling, Industrial PET Scrap Recycling, and Others), By End-User (Waste Management, Plastic Recycling Facilities, Packaging, Textile & Polyester, Biotechnology & Research Institutes, and Others) Regional Analysis North America – The US & Canada; Europe – Germany, France, The UK, Spain, Italy, Russia & CIS, Rest of Europe; APAC– China, Japan, South Korea, India, ASEAN & Rest of APAC; Latin America– Brazil, Mexico & Rest of Latin America; Middle East & Africa– GCC, South Africa, & Rest of MEA Competitive Landscape BuildASoil, KiS Organics, Redbud Soil, FoxFarm Soil & Fertilizer Co, soilsunrise, Dirtcraft Living Soils, APSU Soil, Organic Matters Soil, Terra Preta, SoilBiotics, ProGro BIO, LiveSoil, and Other Players. Customization Scope Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. Purchase Options We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF)

-

-

- BuildASoil

- KiS Organics

- Redbud Soil

- FoxFarm Soil & Fertilizer Co

- soilsunrise

- Dirtcraft Living Soils

- APSU Soil

- Organic Matters Soil

- Terra Preta

- SoilBiotics

- ProGro BIO

- LiveSoil

- Other Key Players

Our Clients

- 181084

- Mar 2026